Roche 4Q25 – Phase 3 for dual GLP-1/GIP RAs CT-388 and CT-868 to initiate in 1Q26; Vabysmo sales up 7% with US market recovery expected in 2026; BGM sales decline 2% –

Executive Highlights

- Roche announced its 4Q25 financial results on a call today led by CEO Dr. Thomas Schinecker, CFO Dr. Alan Hippe, Roche Pharmaceuticals CEO Ms. Teresa Graham, and Roche Diagnostics CEO Mr. Matt Sause. See Roche’s press release, company presentation, and webcast.

- Roche reported a decline in BGM sales in 4Q25, with Near Patient Care Revenue down 3% for the full year and BGM down 2%, continuing a multi-year trend driven by the global shift toward CGM adoption. Mr. Sause framed this decline as structural rather than competitive, saying that Roche is intentionally investing in CGM ahead of the continued market shift.

- Accu-Chek SmartGuide CGM will remain a long-term growth driver for the Near Patient Care division, as the company confirmed continued investment in a CGM manufacturing in Indianapolis. This is part of Roche’s previously announced $50 billion US investment commitment, positioning the US as a core manufacturing hub.

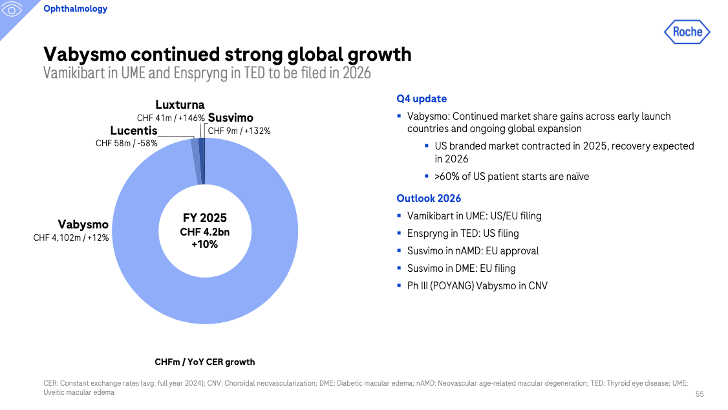

- In ophthalmology, Vabysmo continued to grow globally, despite a persistent US contraction of the branded market in 2025. The company expects US market recovery this year. Internationally, Vaybsmo is up 21% and 22% CER in Europe and Japan, respectively. In Rest of World, sales more than doubled.

- Susvimo (ranibizumab) sales totaled CHF 9 million ($12 million), up over 2x from 4Q24 and 50% sequentially. Susvimo 100 mg/dL is a refillable eye implant that delivers an anti-VEGF as an alternative to injections. The therapy is available in the US and was submitted to the European Medicines Agency (EMA) for review last quarter.

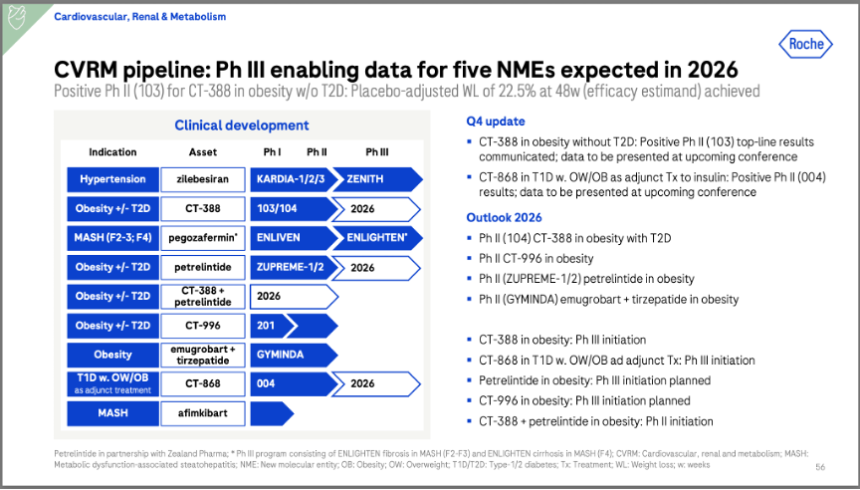

- In the cardiovascular-renal-metabolic (CVRM) pipeline, Roche announced that phase 3 trials for CT-388 (once-weekly GLP-1/GIP RA) for obesity and CT-868 (once-daily GLP-1/GIP RA) for T1D with BMI ≥25 kg/m2 will begin in 1Q26. Based on phase 2 results of CT-388 and amylin analog petrelintide (co-developed with Zealand Pharma), Roche also plans to launch a phase 2 trial of the combination therapy this year.

- On its cardiovascular pipeline, the phase 3 CVOT ZENITH trial (n=11,000) was launched in 3Q25 and is evaluating zilebesiran 300 mg in patients with unmanaged hypertension on a diuretic and at least one other antihypertensive medication. Positive data is expected enable a launch around 2030, though no new updates were given on today’s call.

- On MASH, Roche announced in September 2025 that it will acquire San Francisco-based 89bio, developer of the FGF21 analog pegozafermin. Pegozafermin is currently evaluated in three phase 3 studies.

- Roche doubled its investments in a new site in Holly Springs, NC, which will support its obesity portfolio, and tripled its footprint at Harvard’s Enterprise Research Campus (ERC) in Boston, MA.

Table of Contents

- Technology Highlight

-

Therapy Highlights

- 1. Cardiometabolic pipeline: Phase 3 trials for GLP-1/GIP RAs CT-388 and CT-868 starting in 1Q26

- 2. Roche’s acquisition of 89bio adds a leading MASH asset and lifts its cardiometabolic portfolio value to $1.6 billion; phase 3 readouts expected in 2027 and 2028

- 3. Vabysmo makes the top five key growth drivers with 7% CER growth

- 4. Susvimo: EU regulatory milestones remain key upcoming focus; sales up 132% CER

- Analyst Q&A

Technology Highlight

1. BGM sales decline 2% as Roche prepares for CGM-driven growth; Roche reiterates investment in US CGM manufacturing

While Diabetes Care revenue was not shared[1], Roche reported a decline in BGM sales in 4Q25, with Near Patient Care Revenue down 3% for the full year and BGM down 2%, continuing a multi-year trend driven by the global shift toward CGM adoption. Mr. Sause framed this decline as structural rather than competitive, saying that Roche is intentionally investing in CGM ahead of the continued market shift. Given this reported decline, we estimate BGM revenue of CHF 300 million (~$380 million), consistent with recent quarters and down just 1% sequentially. Roche’s BGM revenue change has seen a year-over-year decline for nearly 20 quarters now (since 2Q21), though nearly every quarter since 3Q21 has fluctuated between ~CHF 300-400 million.

- Dr. Schinecker reiterated confidence that Roche’s Accu-Chek SmartGuide CGM will become a long-term growth driver for the Near Patient Care division and highlighted ongoing investments in manufacturing and commercial readiness. As part of Roche’s previously announced $50 billion US investment commitment, the company confirmed continued investment in a CGM manufacturing facility in Indianapolis. It positioned the US as a core manufacturing hub for its future diabetes technology portfolio. We remain interested in Accu-Chek SmartGuide’s US regulatory status and launch timeline.

Therapy Highlights

1. Cardiometabolic pipeline: Phase 3 trials for GLP-1/GIP RAs CT-388 and CT-868 starting in 1Q26

Roche shared exciting updates to its CVRM pipeline, including advancement to incretin-based therapies, CT-388 and CT-868, to phase 3 in 1Q26. See detailed updates below:

Source: Roche 4Q25 presentation, page 36

- CT-388 (once-weekly dual GLP-1/GIP RA): In January 2026, Roche announced phase 2 results for CT-388. An additional phase 2 trial (n=360) for CT-388 is underway in people with obesity and T2D, with expected completion in August 2026. On today’s call, the company confirmed that the phase 3 ENITH-1 and ENITH-2 trials are expected to start in 1Q26.

- In a phase 2 trial, CT-388 demonstrated 22.5% weight loss at 48 weeks with no plateau in people with obesity (n=469). On the highest dose, 54% of participants on the 24 mg dose demonstrated resolution of obesity, defined as BMI <30 kg/m2. Metabolic benefits were also notable, with 73% of participants with prediabetes returning to normoglycemia, compared to only 7.5% on placebo.

- As a reminder, in a phase 1b trial, CT-388 demonstrated ~12% weight loss at Week 12 and ~19% weight loss at Week 24 in people with obesity but without diabetes. In those with obesity and T2D, CT-388 demonstrated a 3.0% reduction in A1c over 12 weeks compared with 0.2% on placebo. In addition, a subgroup analysis (n=129) presented at ADA 2025 found benefits in metabolic dysfunction-associated steatohepatitis (MASH) and fibrosis. At 24 weeks, 85% of participants with obesity and MASLD experienced a placebo-adjusted reduction in liver fat by 59% and one-stage improvement in fibrosis.

- Ms. Graham also stated that the phase 2 trial of a fixed-dose combination of petrelintide and CT-388 is expected to launch this year, with trial design informed by phase 2 results of petrelintide and CT-388 monotherapies.

- CT-868 (once-daily dual GLP-1/GIP RA): Roche also announced that the phase 3 trial of CT-868 will launch in 1Q26, for people with T1D and BMI ≥25 kg/m2. The decision is based on the 16-week phase 2 trial (n=111) completed in July 2025. The company stated that full results will be shared at an upcoming medical conference this year.

- CT-996 (once-daily oral GLP-1 RA): A phase 2 trial (n=340) of CT-996 for people with obesity and without diabetes launched in July 2025. The trial is expected to be completed in July 2026, with the first trial readout expected later this year. Previously, in a phase 1 trial, CT-996 demonstrated ~7% weight loss at four weeks.

- Petrelintide (long-acting amylin analog): Petrelintide, which is a Zealand-partnered long-acting amylin analog, is in two phase 2 trials, including: (i) the 42-week phase 2b ZUPREME-1 trial (n=494) for people with overweight or obesity, expected to complete in March 2026; and (ii) the 28-week phase 2 ZUPREME-2 trial (n=216) in people with overweight or obesity and T2D, expected to complete in June 2026. The company stated that it expects these trials to be read out later this year. These trials follow phase 1b results, where petrelintide demonstrated placebo-adjusted weight loss of up to 6.9% after 16 weeks, with most adverse events reported as mild.

- Emugrobart (GYM 329, anti-latent myostatin antibody): While GYM 329 was not mentioned on today’s call, the therapy, co-developed with Roche-owned Japanese drug developer Chugai, is designed to preserve muscle mass and prevent post-treatment weight regain, addressing a key limitation of GLP-1 RA therapies. The phase 2 GYMINDA trial (n=234), evaluating the combination of GYM 329 and tirzepatide in obesity, was initiated in 2Q25 and is expected to complete in September 2027. GYM is also evaluated in phase 2/3 trial (n=259) for spinal muscular atrophy and phase 2 trial (n=48) for facioscapulohumeral muscular dystrophy.

- Zilebesiran (angiotensinogen inhibitor). Though also not mentioned on today’s call, the phase 2 KARDIA-1, KARDIA-2, and KARDIA-3 trials found that zilebesiran is most effective for those with unmanaged hypertension and when used with diuretics. Specifically, in participants with unmanaged hypertension despite prior treatment, zilebesiran conferred significant reductions in systolic blood pressure by 7-9 mmHg, which were sustained for over six months. The phase 3 CVOT ZENITHtrial (n=11,000) was launched in 3Q25 and is evaluating zilebesiran 300 mg in patients with unmanaged hypertension on a diuretic and at least one other antihypertensive medication. Positive data is expected enable a launch around 2030.

In January 2026, Roche doubled its investment to $2 billion in its Holly Springs, North Carolina, manufacturing site, which broke ground in August 2025. In addition, the company is tripling its footprint at Harvard’s Enterprise Research Campus (ERC) in Boston, MA, as announced in January 2026. We are happy to see multiple candidates starting to advance to phase 3, as well as an expanded manufacturing footprint.

2. Roche’s acquisition of 89bio adds a leading MASH asset and lifts its cardiometabolic portfolio value to $1.6 billion; phase 3 readouts expected in 2027 and 2028

Roche announced in September 2025 that it will acquire San Francisco-based 89bio, developer of the FGF21 analog pegozafermin for MASH. The company has launched a tender offer of $14.50 per share plus a non‑tradeable contingent value right worth up to an additional $6 per share, an 85% premium, and a potential total transaction value of $3.5 billion. The offer period closed October 29, 2025.

The deal brings pegozafermin into Roche’s cardiometabolic pipeline, adding a liver‑targeted, glycoPEGylated FGF21 analog with compelling phase 2b data. In the 24‑week phase 2b ENLIVEN study (n=222), pegozafermin produced improvements in both fibrosis and MASH resolution. Fibrosis improvement of at least one stage without MASH worsening was 26% (vs. 7% with placebo) with 30 mg dose of pegozafermin and 27% (vs. 7%) with the 44 mg twice‑monthly dose. In addition, the percentage of patients with MASH resolution without worsening of fibrosis also favored pegozafermin over placebo in both the 30 mg pegozafermin group (23% vs. 2%) and the 44 mg pegozafermin group (26% vs. 2%).

Pegozafermin is currently evaluated in three phase 3 studies:

- ENLIGHTEN-Fibrosis trial (n=1,050) for the treatment of moderate-to-severe fibrosis (F2-F3) related to MASH. Topline histology data are expected in 1H27, and the trial is set to complete in February 2029.

- ENLIGHTEN-Cirrhosis trial (n=762) for the treatment of cirrhosis (F4) related to MASH. Topline histology data are expected in 2028, and the trial is set to complete in 2031.

- ENTRUST trial (n=360) for the treatment of severe hypertriglyceridemia. The trial is expected to be completed in April 2026.

3. Vabysmo makes the top five key growth drivers with 7% CER growth

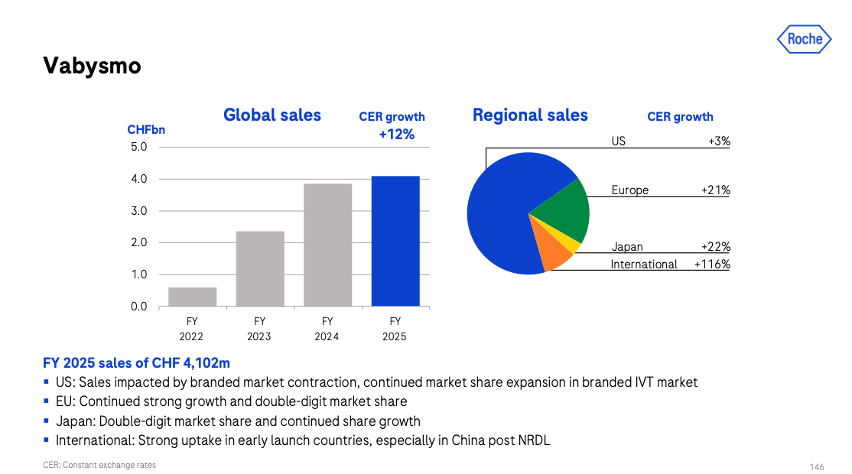

Vabysmo (faricimab) continued to drive robust growth in 4Q25, entering the top five of the company’s key growth drivers, with more than 60% of US patients starting therapy being naïve. 4Q25 sales totaled CHF 1.1 billion ($1.4 billion), up 7% CER from 4Q24 and 10% sequentially. This brings full-year 2025 revenue to CHF 4.2 billion ($5.3 billion), up 12% CER from 2024. Vabysmo, which inhibits two signaling pathways Ang-2 and VEGF-A, has now been on the market since January 2022, following the simultaneous FDA approval in nAMD and DME. Ms. Graham stated that Vabysmo performance was impacted by the contraction of the US branded market for intravitreal therapy. Roche had previously warned that these factors would limit US growth throughout 2025, but US market recovery is expected in 2026.

- In 3Q25, Roche revised its global full-year growth guidance for Vabysmo to 15% from 20%, reflecting the ~15% contraction of the US branded intravitreal market seen last year. US sales grew 3% CER in 4Q25.

- Outside the US, the therapy continued to perform well.

- In Europe, despite temporary impacts from mandatory price cuts, revenue increased by 21% CER from 4Q24. The ongoing rollout of the prefilled syringe (PFS) formulation is expected to drive further growth in the region.

- In Japan, Roche saw 22% CER growth in 4Q25. Roche Group member Chugai received approval for an expanded indication to treat angioid streaks (breaks or cracks in the layer of tissue behind the retina) in May 2025.

- In rest of the world, sales more than doubled, similar to 3Q25. Roche especially reported strong uptake in China, following Vabysmo’s NRDL listing in January and rapidly expanding market share. Following the readout of the phase 3 POYANG trial (n=280) for a choroidal neovascularization (CNV) indication, a planned regulatory submission will occur this year, ahead of the company’s initial planned submission in 2027.

Source: Roche 4Q25 presentation, page 55

Source: Roche 4Q25 presentation, page 146

4. Susvimo: EU regulatory milestones remain key upcoming focus; sales up 132% CER

In 4Q25, Susvimo (ranibizumab) sales totaled CHF 9 million ($11.7 million), up 132% CER from 4Q24 and 50% sequentially. Susvimo 100 mg/dL is a refillable eye implant that delivers an anti-VEGF as an alternative to injections. The therapy is available in the US and was submitted to the European Medicines Agency (EMA) for review last quarter. While no mention of Susvimo was made on today’s call, the therapy’s progress and historic regulatory updates were highlighted in Roche’s investor presentation.

- Roche is pursuing several European regulatory pathways for Susvimo, including potential EU approval in neovascular age-related macular degeneration (nAMD) and an EU filing in diabetic macular edema (DME). These regulatory milestones could meaningfully expand the therapy’s addressable market outside the US.

Analyst Q&A

On obesity candidates GLP-1/GIP RA

Q (Rajesh Kumar, HSBC Bank Plc): First on CT- 388, thanks for clarifying discontinuation rate in the highest dose was similar to the overall group. You also mentioned that you could consider a flexible dosing in Phase 3 trials as an option. So, could you give us some color on how you're thinking about Phase 3 progression? Would flexible dosing or an active comparator be something you might consider, or is it, at the moment too early to comment on that?

A (Ms. Teresa Graham, CEO Roche Pharmaceuticals): In terms of the dosing for CT-388, what we have disclosed is that CT-388, it will be administered once a week, and we're aiming to develop it at three maintenance doses. We are not disclosing at this time the details of that dosing strategy. But just to avoid any misunderstanding, we have not indicated that we will be doing flexible dosing within the trial. But right now, the details of that Phase 3 design, that specifically have not been disclosed.

On 2026 growth expectations for ophthalmology and Vabysmo

Q (Sachin Jain, Bank of America): Firstly on Vabysmo, any color on what you’re assuming in the 2026 guide? What does “doubling” in 2025 versus 2024 mean relative to historic levels? Where is that funding relative to three-four year average? Any color on how that flows back to patients when we should see an impact to sales?

A (Ms. Teresa Graham, CEO Roche Pharmaceuticals): Yes, great. In terms of VABYSMO, I'm not going to give you specifics on the amount of money that we contributed, because as you have heard me say, many, many times before, our charitable giving is not in any way related to our commercial, expectations for the product. Those two things are and must be completely separate.

I can tell you that we doubled our donations last year, and that was a significant increase for us over the last couple of years as you alluded to. We do believe that 2025 represented a re-baselining of the branded market in the US. What we are hopeful is that 2026 will now allow the underlying growth of VABYSMO to actually be more visible. We would expect an acceleration in 2026. I don't believe, we've been more specific than that.

Q (Michael Leuchten, Jefferies): Going back to Vabysmo, just your comment about 2025 in the US being a reset, 4Q25 was still soft. It didn’t really improve upon 3Q24 sequentially. When you say you think that’s now stabilized and it can grow from here, just wondering how you look at that 4Q25 versus 3Q25 dynamic in the US?

A (Ms. Graham): Thinking about Vabysmo, in 2025, we saw a big reset in the branded market in the US, right? With the closure of the co-pay foundation, fewer patients were put on branded drugs, more patients were put on AVASTIN, and biosimilars. And you saw a big reset in how many new patients and continuing patients were actually going on a branded therapy. And that constricted the market by about 15%. That constriction went all the way through Q4, because normally when donations are given or grants are given, they're given for a year's worth of therapy.

Q (Richard Vosser, JPMorgan): On VABYSMO, thanks for the comments on the foundations. Could we go a bit further out and think about the future competition potentially from less frequently dosed injectable products? How you think about the competition? Closer to today, the biosimilars are really starting to come. They're having some impact in Europe as far as we can see. What are your thoughts globally, US, Europe on biosimilars from Eylea on VABYSMO?

A (Dr. Thomas Schinecker, CEO Roche Holding AG): Starting with Diagnostics, we talked about a couple of facts. There's the new technologies. There's the tariffs which Alan said we had half a year and we'll have a full year, this year. But the biggest effect on what hit us last year on the margin, was really the China effect. We expect to see this meaningfully diminish this year. 2027 again, we expect to decline, but it will be small enough that it won't really be meaningful, and then we expect to see a recovery. In terms of specific ambition on margin this year, I think I would refer you back to the to the group position that Alan mentioned earlier. I would say our consistent ambition is to grow profit faster than sales.

That is once we really get ourselves through the headwinds this year, that is our ambition going forward. It's also our continuous ambition to improve the margin in diagnostics. That's something that is a goal for the entire organization, what I would call it, though, in 2025 is you had our second largest margin market with a 25% reduction.

So, obviously there was an impact, but that's something that you can see with our discipline on the cost line, that you can also expect to see continue again in 2026. But we expect the gradual, washout of that. Anything you would add to that, Alan.

A (Dr. Alan Hippe, CFO): Well, for 2026 I think, well, we expect kind of a stabilization. I think that's a little bit, yes. But we would give that additional information. I think on the group level, you've seen that our intention is to expand margin in 2026. What I've said in the past still holds, which is that also going forward, we will at least keep margins stable also for the coming years.

Q (Rajesh Kumar, HSBC Bank Plc): One clarification on the Vabysmo, appreciate the working capital impact has gone up, and that sort of reflects a very strong December. Should we consider the exit rate of December a closer indication of how you're thinking about growth in 2026, or should we take an overall slower growth rate going forward on the Vabysmo?

A (Ms. Teresa Graham, CEO Roche Pharmaceuticals): So I would just go back to my earlier comments. For Vabysmo, we expect to see an acceleration of growth in 2026. So more to come on that.

On CGM

Q (Justin Smith, Bernstein): Matt, just wondered if you could talk a little bit about CGM and when the finger-prick recalibration will be removed and the impact that might have?

A (Dr. Sause): So, specifically to your question on auto calibration, which is the comparison of the CGM device with a blood glucose lancet. What we are planning to do is have that launch happen this year. I won't say exactly which quarter, but that is an improvement that we expect to deliver this year.

Close Concerns’ Questions

- With an expanded manufacturing and research footprint, how is the timeline for CT-388 likely to change, given that it is considered a fast‑track asset by the company?

- What might we expect from the US intravitreal injection market? Might sales recover as soon as in 1Q26?

- How is Roche device management thinking about Accu-Chek SmartGuide interoperability and future AID integrations to drive further growth for CGM?

- How will the recent acquisition of 89bio affect strategy within therapy?

- What impact will the stronger Euro have on Roche’s various businesses? What impact might the weaker US dollar have on US-based businesses?

-- by Kayla Mathieu, Riya Chatterjee, Jeremy Alkire, Kat Moon, Monica Oxenreiter, and Kelly Close