Tandem 4Q25 – Record quarterly and full-year revenue of $290 million and $1+ billion, representing substantial quarterly and annual growth; expansive shift to “pay-as-you-go” model within the US pharmacy channel planned for 2026 –

Executive Highlights

- Tandem reported its 4Q25 and full-year 2025 financial results on a compelling call led this afternoon by CEO Mr. John Sheridan and CFO Ms. Leigh Vosseller. See the press release, presentation, and webcast.

- Revenue totaled $290 million in 4Q25, up 15% from 4Q24 and 17% sequentially, marking the company’s largest revenue generated in any quarter since its founding twenty years ago. US revenue rose to $210 million, up 14% from 4Q24 and up 20% sequentially, and OUS revenue totaled $80 million, up 18% from 4Q24 and 9% sequentially and representing nearly 30% of total revenue, its best quarter yet internationally.

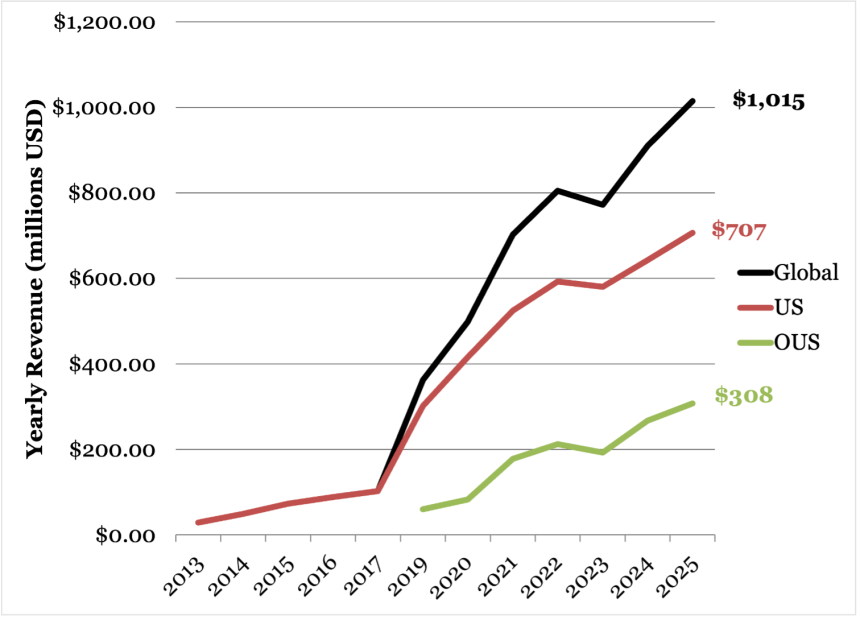

- Full-year 2025 revenue exceeded $1 billion for the first time, totaling $1.01 billion, up 12%.

- Tandem’s installed base now exceeds 500,000 customers worldwide, including approximately 325,000 in the US. Its worldwide pump shipments totaled 38,000 in 4Q25, the company’s best quarter to date. This is up 12% from 4Q24 and up 31% sequentially. Record US shipments accounted for over 70% of new pump shipments (27,000), up 6% from 4Q24 and sequentially. OUS shipments totaled 11,000 units, down 2% from 4Q24 and sequentially. Tandem continues to see strong renewal rates, at over 70% of pumps within 18 months of warranty expiration, exceptional given the competition. Among new customers, approximately two-thirds transitioned from MDI. Management noted that it initiated its full launch of Control-IQ+ for people with T2D in the US in 4Q25, which contributed to Tandem’s sequential step-up in new shipments.

- Management issued its full-year 2026 revenue guidance of 5% to 7% growth. If accomplished, this would represent $1.065 billion-$1.085 billion in revenue for full-year 2026. Broken down by geography, Tandem expects $730-$745 million in US revenue (+3-5%) and $335-$340 million (+9-10%) in international revenue in 2026. Management explained that the ongoing US transition to pharmacy distribution and a pay-as-you-go (PayGo) model will moderate revenue growth in 2026 because it eliminates the upfront revenue recognition associated with the DME channel. Given this, this expectation sounds strong.

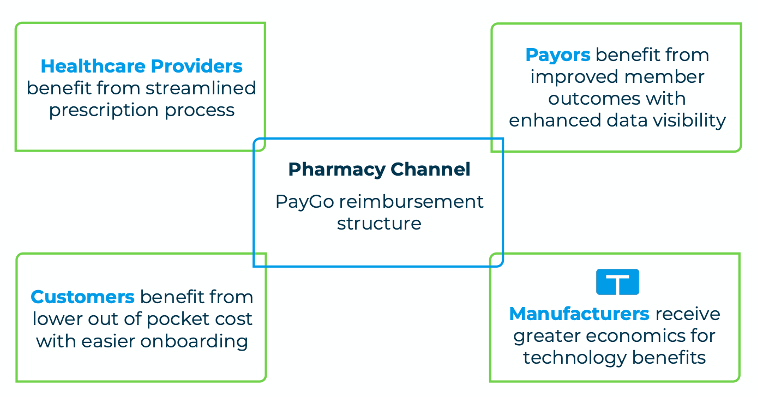

- Management extensively outlined a structural transition beginning in late 1Q26 to a pay-as-you-go (PayGo) model through the pharmacy channel in the US, in which Tandem pumps will be distributed with $0 upfront cost and revenue will shift toward recurring pharmacy reimbursement. Management said it expects a $70-$80 million revenue headwind in 2026, with most of the impact weighted to the back half of the year as pay-as-you-go model adoption scales. Approximately 20% of pump shipments are expected to go through Tandem’s PayGo model in 2026, with as many as 80% flowing through the model three years from now. We’re very glad to hear that the major upfront fee so hard for so many patients will not be required as a pre-requisite for pump therapy with Tandem.

- Mr. Sheridan highlighted a 2Q26 innovation cycle focused on exciting sensor interoperability and the geographic expansion of Tandem’s Mobi. Specifically, Tandem Mobi, launched two years ago nearly to the day in the US, will integrate with FreeStyle Libre 3 Plus in 2Q26. Tandem will integrate both Mobi and t:slim X2 with the Dexcom G7 15 Day CGM.

- On Mobi’s international footprint, Mobi will also expand further internationally, closely following Tandem’s new direct commercial operations in the UK, Switzerland, and Austria, where the company is now active and expects productivity to scale through 2026.

Tandem Yearly Revenue (2013 – 2025)

Table of Contents

-

Financial Highlights

- 1. Worldwide 4Q25 revenue totaled $290 million, up 15%; full-year 2025 revenue exceeds milestone $1 billion (+12%)

- 2. New pumps shipped in 4Q25 total 38,000 as installed t:slim X2 userbase nears 500,000, up 4% from 2024

- 3. Gross margin of 54%; return to a positive operating margin (+3%) with $8.3 million operating income; nearly $300 million in cash and cash equivalents

- 4. Full-year 2026 guidance of $1.065-1.085 billion (+5-7%); 1Q26 guidance of $236-$240 million (+1-2%)

- Control-IQ Highlights

- Pipeline Highlights

- Analyst Q&A

- Close Concerns’ Questions

Financial Highlights

1. Worldwide 4Q25 revenue totaled $290 million, up 15%; full-year 2025 revenue exceeds milestone $1 billion (+12%)

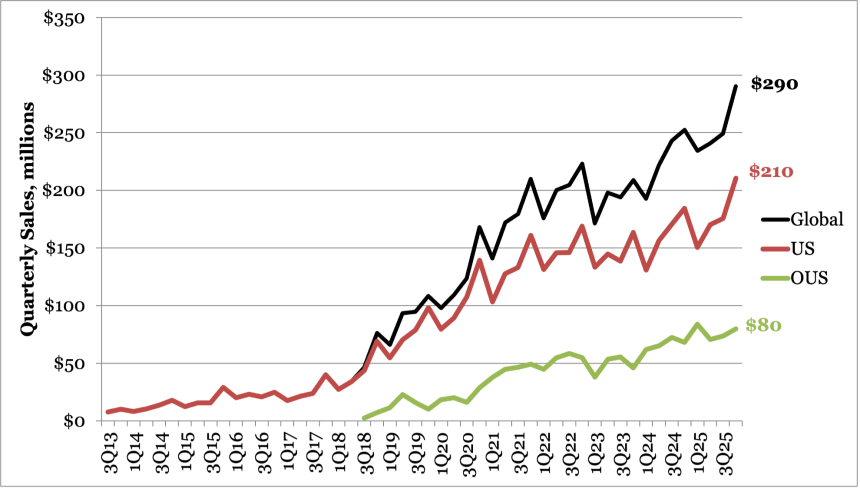

Tandem Quarterly Revenue (2Q13 – 4Q25)

Revenue totaled $290 million in 4Q25, up 15% from 4Q24 and 17% sequentially, marking the company’s strongest fourth quarter to date. Ms. Vosseller attributed topline strength to higher average selling prices (ASPs), improved efficiency across commercial operations, and the growing contribution of the pharmacy channel. Full-year 2025 revenue exceeded $1 billion for the first time, totaling $1.01 billion (+12%).

- US revenue rose to $210 million, up 14% from 4Q24 and 20% sequentially, marking Tandem’s highest US quarter ever. Pharmacy channel growth has also accelerated, with a near doubling of t:slim X2 supply sales (totaling $16 million) from 3Q25 in the quarter (see more below). Full-year 2025 US revenue totaled $707 million, up 10% from 2024.

- OUS revenue totaled $80 million, up 18% from 4Q24 and 9% sequentially. Full-year 2025 international sales totaled $308 million, up 15% from 2024. Ms. Vosseller explained that international revenue benefitted from favorable foreign exchange rates offset by $4 million associated with its transition to direct operations. For the full year, the total distributor destocking and inventory buyback impact was approximately $7 million, slightly lower than the $10 million the company had estimated due to a partial delay in timing from 2025 to the first quarter of 2026.

2. New pumps shipped in 4Q25 total 38,000 as installed t:slim X2 userbase nears 500,000, up 4% from 2024

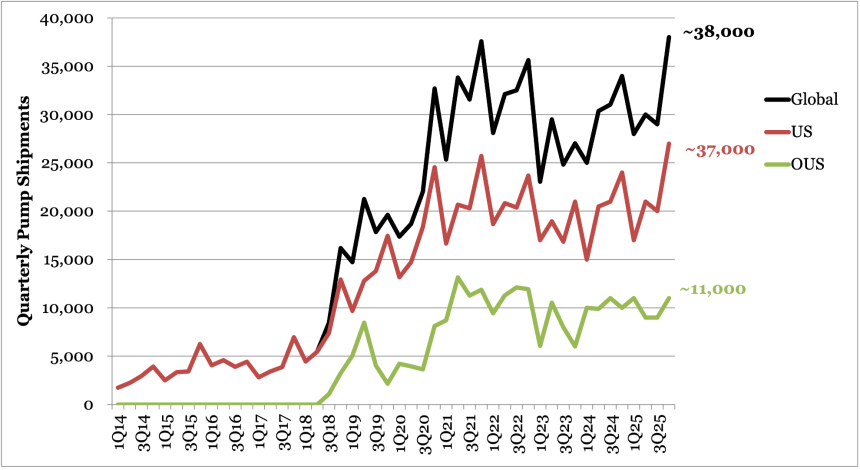

Tandem Quarterly Pump Shipments (2Q13 – 4Q25)

Tandem’s worldwide pump shipments totaled 38,000 in 4Q25, the company’s best quarter to date. This is up 12% from 4Q24 and 31% sequentially, in line with the company’s expectations that the quarter would comprise ~30% of the year’s pump shipments. Record US shipments accounted for over 70% of new pump shipments (27,000), up 6% from 4Q24 and sequentially. OUS shipments totaled 11,000 units, down 2% from 4Q24 and sequentially.

- Shipments were driven primarily by renewals, with Ms. Vosseller alluding to a little over half of all pump shipments in the quarter being renewals. In Q&A, she noted that Tandem continues to see reassuring renewal rates, at over 70% of pumps within 18 months of warranty expiration. Among new customers, approximately two-thirds transitioned from MDI, reflecting continued success broadening adoption beyond traditional pump users and consistent with previous quarters. Management noted that it initiated its full launch of Control-IQ+ for people with T2D in the US in 4Q25, which contributed to Tandem’s step-up in new shipments from 3Q25. Tandem’s installed base now exceeds 500,000 customers worldwide, including approximately 325,000 in the US.

3. Gross margin of 54%; return to a positive operating margin (+3%) with $8.3 million operating income; nearly $300 million in cash and cash equivalents

Tandem reported a non-GAAP gross margin of 58%, a seven-point increase from in 4Q24 and a four-point increase from 3Q25. Full-year non-GAAP gross margin was 54%, a three-point increase from 2024. Ms. Vosseller attributed the gross margin improvement to product cost reductions, manufacturing efficiency improvements, and execution on its pricing and channel initiatives (see more below).

- The company recorded its first return to positive operating margin since 2021 in 4Q25. Ms. Vosseller reported operating margin of 3% (up from -12% in 4Q24) and operating income of $22.9 million, improving upon the operating loss of $23 million in 3Q25 and $30 million in 4Q24. Operating expenses ($159 million) in 4Q25 were essentially flat from 4Q24. Investments in SG&A to expand the US sales force and prepare for direct operations in Europe were offset by declines in R&D spending.

- Tandem ended 4Q25 with $293 million in cash, cash equivalents, and short-term investments. This is down from $319 million in 3Q25 and $438 million in 4Q24.

4. Full-year 2026 guidance of $1.065-1.085 billion (+5-7%); 1Q26 guidance of $236-$240 million (+1-2%)

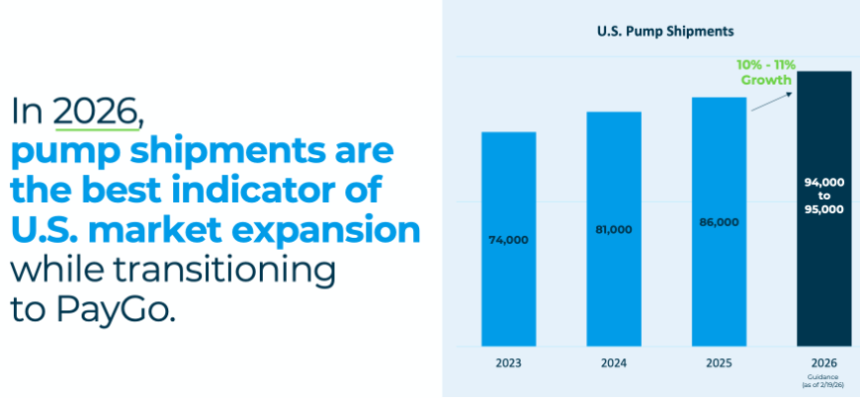

Management issued its full-year 2026 revenue guidance with an estimate of 5% to 7% growth. If accomplished, this would represent $1.065 billion-$1.085 billion in revenue for full-year 2026. Broken down by geography, Tandem expects $730-745 million in US revenue (+3-5%) and $335-340 million (+9-10%) in international revenue in 2026. Management explained that the ongoing US transition to pharmacy distribution and a pay-as-you-go (PayGo) model will moderate revenue growth in 2026 because it eliminates the upfront revenue recognition associated with the DME channel. Consequently, Ms. Vosseller said that pump shipments will be a key indicator of Tandem’s progress in 2026. Growth is expected to be driven by new technology, expanded geographic reach, and broader pharmacy access. The adoption of PayGo is anticipated to create $70-$80 million in pricing headwinds. Pharmacy sales are projected to represent ~15% of total US sales in 2026, up from 4% in 2025, and are expected to exceed 70% over the long term. Internationally, ASP expansion is expected to partially offset a $15 million headwind from distributor destocking and inventory buybacks. Direct sales are projected to account for approximately 15% of total international revenue in 2026. In total, guidance incorporates $85-$95 million in revenue headwinds tied to strategic business model changes.

- US pump shipments are projected to increase 10-11% in 2026, led by continued conversions from MDI, with renewal shipments accounting for more than half of total volumes. Despite scaling pharmacy access, approximately 80% of 2026 pump shipments are still expected to move through the DME channel in 2026.

- Tandem issued full-year 2026 gross margin guidance of 56-57%, with margins expected to reach approximately 60% in 4Q26. First-quarter gross margin is projected at ~54%, up from 51% in the prior-year period. Management indicated that progress toward the long-term 65% gross margin target for Mobi will be the primary driver of expansion.

- Tandem also issued preliminary 1Q26 revenue guidance of $236-240 million, implying just 1-2% year-over-year growth. At the midpoint, this represents roughly 22% of full-year revenue. Pump shipments are expected to follow typical seasonality, similar to 2025, when volumes declined nearly 30% sequentially from 4Q24 to 1Q25 due to DME deductible resets. International direct sales are expected to comprise ~5% of 1Q26 revenue, consistent with 2025 levels.

Control-IQ Highlights

1. Broad shift to pay-as-you-go model through the pharmacy channel in the US planned for 2026, causing initial headwinds

Management outlined a structural transition beginning in late 1Q26 to a pay-as-you-go (PayGo) model through the pharmacy channel in the US, in which Tandem pumps will be distributed with $0 upfront cost and revenue will shift toward recurring pharmacy reimbursement. Management guided to a $70-$80 million revenue headwind in 2026, with most of the impact weighted to the back half of the year as pay-as-you-go model adoption scales.

- In the Q&A, Mr. Sheridan described the change as “very impactful,” but that 2026 revenue will reflect near-term revenue headwinds from pricing dynamics before the longer-term benefits become more visible. Ms. Vosseller said that ~10-11% growth in pump shipments better reflects underlying business performance, as reported revenue will be temporarily understating demand for Tandem’s pumps.

- These contracts through the pharmacy channel will largely become effective to most customers in late 1Q26, with management expecting ~$10 million of headwinds in 1Q26, split between early PayGo impact and international transition effects. Tandem already has contracts with the top three PBMs (~80% of covered lives), though formulary access is currently available to about one-third of these individuals, with expansions ongoing.

- Approximately 20% of pump shipments is expected to go through Tandem’s PayGo model in 2026. Pharmacy supply ordering across Tandem’s installed userbase is expected to average ~10% of customers, up from <5% in 4Q25. In Q&A, it was noted that this shift helps to partially offset upfront revenue pressure as more users transition from DME to pharmacy reimbursement over time.

Source: Tandem 4Q25 Presentation

- Mr. Sheridan highlighted favorable long-term effects with the PayGo model, saying that pharmacy supply reimbursements can be over four times that of the DME channel, with payback achievable within “a handful of months.” Management suggested roughly $350 per month per customer initially while mentioning that the shift reduces patient out-of-pocket burden, removes large deductibles, and improves prescribing simplicity. These factors are expected to support stronger adoption and double the lifetime value of each customer to Tandem.

Source: Tandem 4Q25 Presentation

2. Tandem launches direct sales in three European countries

Ms. Vosseller said Tandem began direct commercial operations in Switzerland, the UK, and Austria in 1Q26,marking Tandem’s first major step in its long-term international growth strategy. This move replaces distributor-led models with in-country sales and logistics, bringing Tandem even closer to its customers. Mr. Sheridan noted that the shift required building local commercial infrastructure and hiring in-country teams, as well as coordinating distributor separations and implementing reimbursement systems. With these elements now in place, Tandem is live and actively serving customers through these direct European operations.

- Management framed these three markets as a blueprint for broader international expansion, with all lessons learned guiding Tandem’s future transitions to direct operations in additional markets in 2026 and 2027. These transitions are expected to deepen engagement and support improved pricing.

- Looking ahead, Tandem expects to operate under a hybrid international structure, combining additional key European markets with select distributor partnerships and local market expertise.

3. Tandem submitted a 510(k) submission for a pregnancy indication for Control-IQ+

Tandem announced today that it filed a 510(k) submission with the FDA seeking clearance of Control-IQ+ for use during pregnancy, representing a meaningful step toward broadening the algorithm’s clinical reach beyond its current indications. The pregnancy indication targets a population with a significant unmet need, and if cleared, would further differentiate Tandem’s algorithm across the AID landscape.

- The submission builds on Tandem’s continued expansion of Control-IQ+, which already supports individuals with T1D from ages two and up, and adults with T2D. Management framed the pregnancy filing as one of several regulatory milestones expected to expand Control-IQ’s clinical impact.

- Across the AID landscape, pregnancy remains an early and relatively underpenetrated indication. Currently, CamAPS FX is the only AID system with a pregnancy indication in multiple international markets, while Medtronic’s MiniMed 780G has received CE-Mark to include individuals with pregnancy complicated by diabetes. Other major AID platforms, including Tandem’s Control-IQ+, Insulet’s Omnipod 5, and Beta Bionics’s iLet, do not yet have pregnancy indications in the US and are progressing through clinical and regulatory pathways (Medtronic, for example, has long said it expects to file an FDA submission to remove a warning for use in pregnancy). If cleared, Control-IQ+ would position Tandem among a small group of systems pursuing this high-need population, where tighter glycemic targets and automation may meaningfully improve maternal and fetal outcomes.

Pipeline Highlights

1. Three product launches targets for 2Q26: FreeStyle Libre 3 Plus integration with Mobi, G7 15 Day integration, and Mobi launch internationally

Mr. Sheridan highlighted a focused 2Q26 innovation cycle focused on sensor interoperability and geographic expansion of Mobi, positioning the platform as a multi-sensor, multi-region system with broad flexibility.

- Specifically, Tandem Mobi will integrate with FreeStyle Libre 3 Plus in 2Q26, and Tandem will integrate both Mobi and t:slim X2 with the Dexcom G7 15 Day sensor that launched in December 2025, expanding Tandem’s CGM choice and reinforcing platform differentiation across both US and international markets. Mobi will also expand internationally, closely following Tandem’s new direct commercial operations in the UK, Switzerland, and Austria, where the company is now active and expects productivity to scale through 2026.

2. Hardware pipeline: Mobi Tubeless launch targeted for 2H26

Mr. Sheridan confirmed plans to file a 510(k) in 2Q26 for Mobi Tubeless, with launch targeted for 2H26, marking Tandem’s first entry into the patch pump category.

- Mobi Tubeless introduces a new infusion site option enabling interchangeability between tubing and patch wear, allowing for more personalization and flexibility without requiring users to switch platforms. Leadership expressed strong confidence in regulatory timing, reiterating expectations for approval in 2H26. The launch will incorporate Tandem’s SteadiSet extended-wear infusion set technology, which suppors seven-day wear duration and further advances pump wearability.

- Tandem’s broader hardware pipeline includes a next-generation Mobi featuring further miniaturization derived from Sigi technology, signaling continued hardware refined beyond the initial tubeless launch.

3. Fully closed loop system advances, with FDA filing targeted for 2027

Tandem reiterated its plans to advance work on a fully closed-loop AID algorithm with a pivotal study expected to launch in 2026. Tandem has had a longstanding partnership with the University of Virginia (UVA) to work toward this goal. Tandem has previously said that the system will maintain compatibility with the CGMs that are currently compatible with Tandem’s products, and Mr. Sheridan said today that Tandem is targeting a regulatory filing with the FDA in 2027.

Analyst Q&A

On 2026 guidance

Q (Matt Miksic, Barclays): Congrats on a really strong finish year, both top line and on the EBITDA line. So I think you're going to get a lot of questions here around the new model. I appreciate all the information in the slide deck spelling it out and laying it out. And certainly that's certainly something that folks have talked about and thought about just in diabetes generally moving in this direction, particularly for automated insulin delivery systems. One question I guess is you gave pretty good guidance on Q1, which was clear for the full year in the US. The OUS growth with the $15 million headwind is sort of like a 9% to 10% underlying. Is the right way to think about that kind of in the mid-teens? So I guess you had like low-double digit US shipments, mid-teens OUS kind of underlying growth to get to sort of like a low-double digit underlying sort of performance metric for next year absent of the PayGo changes.

Mr. John Sheridan, CEO: I think that's correct, Matt. I think if you look at the overall revenue growth or shipment growth for the year, it's going to be in the line of about 10% to 11%. So it's going be double digit growth in shipments. And we're also expect to see a return to growth in in new shipments. I would say that that is the best indication of our performance next year, including the profitability, because when you look at the revenue numbers, the revenue numbers are impacted by the headwinds from the pricing that has that comes along with PAYGO. So, you know, this is a very impactful change in the business. We're very excited about it. I think when you when you look at it, I mean, basically, we double or more than double the revenue, the lifetime revenue from a patient. And that's a substantial change. While at the same time we are going to substantially reduce our out of out-of-pocket and improve the experience. So, you know, that's a that's a real win in both sides. And like I said, we're very excited about this. This is going to be impactful. And I think when you look at the impact on the P&L, I mean, certainly there's a revenue hit from the pricing, the pricing headwind. But when you look at gross margin, you look at adjusted EBITDA, we do show solid performance there. And as I said, you know, our shipment growth is the real numbers to look at in 2027 – 2026 for us.

Q (Matthew Blackman, TD Cowen): I'll ask the expectation of 20%, roughly 20% of pumps in 2026 going through the pharmacy. Give us some context on where you are from today on a coverage and contracting standpoint and where you'd expect to be exiting the year. Just trying to reconcile the 20% mix versus maybe where you are on the contracting side, what progress you've made there.

Ms. Leigh Vosseller, CFO: I would say there are two ways to think about coverage for us. I mean, we do have contracts with all the major PBMs, the top three, which gets you about 80% of covered lives under contract. And what we're really focused on is the formulary access where we have roughly a third of lives covered today. And think about that as just the beginning as we're launching into this, the pharmacy with the pay-as-you-go model, which those contracts will be effective late in the first quarter. So at the very beginning here I would expect low volume, but it will continue to scale up across the year to average to that 20% point that we that you mentioned in terms of pump shipments going out the door with a $0 upfront payment. That's a little bit separate or different from the amount of our installed base that we expect to be ordering through the channel. So think about this as a complement while we have that headwind on the upfront piece, we have the ability to mitigate some of those headwinds by transitioning or shifting more of our current DME customers into the pharmacy channel. And similarly, that percentage will start low. We came out of the fourth quarter with less than 5% ordering through the pharmacy channel and we expect that to scale up across the year as well. On average for the year, you can think about that as roughly 10% of our customers across the year that will be ordering their supplies through the pharmacy channel.

Q (Matthew O'Brien, Piper Sandler): I'd love to talk about the acceleration that you're expecting on the new pump shipment side here in 2026. It's one of the better numbers we've seen over the last several years. I know you have Mobi coming out with Libre 3 Plus and then the G7 15 Day, but you're not assuming any benefit from Tubeless here in 2026. Why the confidence in the ability to do that without that kind of product in 2026? Can you deconstruct how you how you get there to see that kind of acceleration?

Mr. Sheridan: While we don't have Mobi in the revenue plan, that's typically the way we've done it in the past, a little bit more conservative when it comes to uncertainty. I would say that we have high confidence we're going to get this thing approved this year. When you consider Mobi users will now have multiple sensor integration, and they'll have Android and iOS, and then it will also have a tubeless implementation. There's nothing else like that on the market. I think as you look at the buildup, just to get to the tubeless product, we are adding a great deal of functionality to these products.

We're also expanding Mobi into the OUS markets and we're expanding FreeStyle Libre 3 into the OUS markets as well, which has been a point of competition. I think when both those products are there, it's going to be a completely different picture. I think the pipeline is certainly a big piece of it.

I would say that a lot of the work that we've done with the sales force in terms of improving their productivity, as we mentioned, we have a brand new system coming online here next month basically that's going to substantially improve their efficiency and productivity. So we expect to see that contribute to the to the new starts.

Finally, I think that pharmacy is something that we think is going to have an impact on our business this year. I think when you look at that, really, it's the new technology. It's the sales organization, the improvements that happened there last year. And then it's also pharmacy. I think the combination of those will drive the growth that we're going to see in 2026.

Q (Leon, Goldman Sachs): I wanted to double click on the gross margin trajectory, a lot of emphasis on sales and sales cadence moving forward. But you know, logically there's a headwind to gross margin this year with the sales transition. Can you talk about the trajectory or the exit rate from this year or when things normalize in 2027 for underlying gross margins and help quantify what the headwind is, maybe this year that's going to lift next year or beyond?

Ms. Vosseller: I'll just start with the fact that in 2025, before we even had a meaningful pharmacy opportunity, we already stepped-up gross margins substantially year-over-year by three points on an annual basis. And in 2026, I think important to understand that even with this moderated sales growth rate, we can still expand margins another 2 to 3 points. And so we expect to exit this year at about a 60% rate. And you make a good point about the headwinds, putting a little bit of pressure on margins. That just means that it gives us more opportunity to expand those faster in the future. And so we're very focused on driving that. I mean, it's a very important part of our business, and we've always been focused on sales growth, but we're going to show is that we have the ability to drive margins like you see competitive levels across the market.

Q (Joanne Wuensch, Citi): There's a lot going on in 2026, both in the US and outside the United States. You've sort of addressed sort of how to think about the first quarter, but can you help me understand revenue and I guess, gross margins, the progression throughout the year? I mean, not just specific second, third or fourth quarter guidance, but maybe ratios or something just to sort of lay the groundwork so we set the models up correctly.

Ms. Vosseller: I'll start with the US, as I think that's where you're trying to untangle all the parts and pieces and how they might influence the year from the perspective of US shipments. Let's start with that and remembering that still 80% of our shipments will be through DME this year. I would expect the same seasonal curve on pump shipments. So you think about the lowest point in Q1, the highest point in Q4, and that has a heavy influence on gross margins – I would say the way our margins have been structured historically. Where we've always seen that pumps have the highest gross margin and supplies are meaningfully lower than that. That's why you can expect a similar trajectory of gross margin across the year, starting at about 54%, scaling up to 60%. And when I say scaling up, I mean measurably stepping up across each quarter of the year, because even though we have these headwinds, if you will, on the pump price, with the pump going out the door at $0, we have that opportunity to continue to fuel margin expansion with the pricing benefit that will come from the supplies and the supplies we shift into the pharmacy channel.

We also have the OUS business to help there. We're going to be scaling up our direct business across the year and that is also positive and beneficial to gross margins despite those headwinds that we expect to see there.

I would say when you think about the revenue models and the margin models this year, they’re not too dissimilar from what you've seen from years past, but we do expect as we look ahead, as pharmacy becomes a bigger piece of our business, it will start to level out those seasonal curves to some extent. But for now, I think I would start with similar assumptions to what you've seen before.

On the shift to a pay-as-you-go model through the pharmacy channel

Q (Larry Biegelsen, Wells Fargo): This has been talked about for a long time, John, this pay-as-you-go model. So, you know, my questions are really, why now? Why is this the right time and the long-term pharmacy goals? You know, why is 80% the right number in two to three years? I assume that excludes Medicare fee for service? And how are you thinking about attrition changing with a pay-as-you-go model?

Mr. Sheridan: We have been thinking about this for a while. And I think in the fourth quarter, we gained a lot of experience just in our pharmacy business. We've had conversations with a number of payers and we think it's very doable. We've talked about pharmacy for a while now, and I think it's absolutely the right time to make this transition. You know, we've got a number of other things that are very positive when it comes to the business. So as I said, this is a very impactful, impactful decision for us, but it's the right one and we're very excited about it.

Ms. Vosseller: As we think about the goal, this is just the beginning and we're working to build up additional formulary access, and within the formularies we have to build up a cash attachment from the downstream payer plans. And what we see is over the two to three years is what it will take for us to build out to them to, you know, optimal coverage, if you want to call it that. Where at that point we probably will have at least 70% of our sales going through the pharmacy channel. So that's a complete flip of our business model, obviously, from where it is today.

Attrition is a question that we're often asked as we think about pharmacy channel at all, where people don't necessarily have what you would call lock-in periods like they have in DME. What we've seen in our experience in the DME channel is that even though people are stay with us for four years because of that warranty period, we see people staying well beyond the four years, whether it's through another pump purchase or just staying on the pump outside of warranty because high quality of the pump, it just keeps working. So there's no need to transition. We feel comfortable that when people try out our technology, they stick with it. Even in this model where maybe they won't have the same dynamics in terms of restrictions from switching from one to another, we think they'll stick with us.

Q (Matt Taylor, Jefferies): Can you can you talk about at a high level how the pharmacy shift is going to impact the P&L and sales growth in 2027 and 2028 in more detail? It's a little bit confusing as you're going to continue to have that shift through the next few years.

Ms. Vosseller: When you think about the headwinds this year, we expect that to be more pronounced as we're just launching into it. We don't yet have what I would call the cover for it coming from the supply sales or the reimbursement on supply. You can see first of all, for every PayGo customer we get into the model, we're going to be getting reimbursement on supplies more than four times what we get in DME today. As you build up that base of customers who benefit from getting a pump with no cost upfront, that's going to be a tailwind on revenue in the coming in the next couple of years. To add to that, we do have we have over 300,000 t:slim customers today in our existing installed base. The opportunity to shift those people from the DME to the pharmacy channel will also create a tailwind and that's immediate benefit from one day when they're ordering DME to the next day when they're ordering in pharmacy, you would immediately see that appreciation. I think what's really important this year is even though this is a near-term headwind and it does have a moderation effect on revenue growth, we're still demonstrating margin expansion at the same time. It's showing the power of what this shift can look like in that first year. And then just you can imagine how much better it gets in the coming years.

Q (Shagun Singh, RBC Capital Markets): Can you shed some light on cadence to the year to the $70 million to $80 million revenue headwind? How do we see it through the year? I think you indicated that that this will be effective, I believe you said in late 1Q26.

Ms. Vosseller: The way to think about it is obviously in the first quarter, it's going to be a very low percent of our shipment volumes that will have this effect from the PayGo reimbursement. The bulk of those headwinds are probably going to be hitting in the last couple of quarters of the year. Think about low-single digit percentage scaling up to a number that averages to 20% for the year. And in margins, we have the same opportunity to transition our supply customers, similar to what we've seen in years past. So call it nearly 54%, getting up to about 60% in the fourth quarter of the year. You can think about that scaling pretty linearly across the quarters this year. I should add that in the first quarter in particular, we factored in about $10 million of headwinds worldwide. And you can think about that as roughly split between our international operations and the transition to going direct and between the headwinds that we could see in the first quarter for the PayGo transition.

Q (Jeff Johnson, Baird): Leigh, you mentioned that pharmacy pricing is going to be consistent with what others are out there on a tube pump side, the pharmacy channel. You know, just to put a number on that for modeling purposes, $450 a month, is that a reasonable price to jump into our model as we try to build this out? And you talked about some of your installed base starting to get their supplies in the pharmacy channel. It sounded like they'd get that same price for their supplies. But ostensibly that higher supply price is also supposed to include some amortization of the pump. So if I'm a current user that jumps into the pharmacy channel, am I also going to get that $450 a month or whatever the right number is there to help out?

Ms. Vosseller: The way the way I'm asking people to think about it this year is we're just getting going with this. We're launching into the market with these new contracts effective late in the first quarter, and there's a mix of contracts contract terms within the contracts that we have. Whether we have preferred or non-preferred access influences what the rebate looks like, how much copay assistance we use. So long story short, what I'm suggesting to start with this year, at least from a modeling perspective, is to think about it as about $350 per month per customer. And that's going to give us the starting point as we take the time to monitor the trends, to see what is the real utilization in mix across the contracts that we have and further inform you in the future for how to think about where that average take could be. But I would say that's a really good starting point, and that alone is a really great benefit versus the DME pricing that we see today.

When you think about this and what this means for people who already have a pump versus people who are getting a pump for the first time, it's almost like a reset, if you will. And so basically going forward, the whole business will be structure agnostic to whether they're getting a pump today or not. It will be consistent pricing across the customers, if that makes sense. And so again, I would start with about $350 per month as a modeling point and we'll continue to inform you along the way as we get more information.

Q (William Plovanic, Canaccord Genuity): Could you help us out with this transition on the PayGo model? How many months to break even on that in your models? And then I don't think you talked about free cash flow in 2026. You know, do you expect free cash flow positive in 2026? How should we think of the quarterly cadence of the cash burn? You know, typically Q1 is a heavy cash burn quarter. So just so there's no surprises. Can you help us with that?

Ms. Vosseller: I'll start with the break even question. There are actually a number of ways to answer that question, but maybe one way that I can help you think about the impact on the business is when you think about a PayGo customer, there's a breakeven point for an individual customer as we offer the $0 pump, and it takes a number of months in order to cover that with the supply sales for that customer. But because we have this opportunity to shift our existing customer base, you can think about it as one PayGo customer plus two existing customers. You break even within payback within a handful of months. It doesn't take too long in order to pay back or to cover this headwind that we would see. And that also dovetails a little bit into the cash question. And we did exit 2025 free cash flow positive. And to your point, we usually see a dip in the first quarter of the year as we pay out annual incentive compensation and that sort of thing. This year on an annual basis, taking all this into consideration as we make the transition, we expect to be free cash flow neutral this year. And by the end of the year starting to ramp up back to a positive position as we move forward into 2027. We obviously, as we make this transition going to be very mindful of our cash balance. But I think that's a good way to think about it across the year.

Mr. Sheridan: I wanted to make another point about the move to PayGo that may not be as clear as I have spoken about a moment ago, but as we move to PayGo, we eliminate a significant number of the barriers that we have with DME. I think if you think about DME today, it's a problem for the physician to prescribe. It often has to go and jump through hoops to provide information to justify the purchase. It's troublesome for the patient because they've got to go back and forth, provide information. It takes time.

The other thing, too, is one of the most significant challenges, I think, for people these days in the DME channel is there's a large out of pocket. Some people might have to pay their full deductible and that can be $1,000 or more. The benefit of the pharmacy channel is that it eliminates the friction. It's easy. It's easy for the patient. And it's also very easy for the physician and their staff. And it eliminates that large upfront payment. And so, you know, the monthly payments can be lower. It really does address the problems that we have in DME. I think that is why we expect to see the pharmacy drive uptick in new patients and that's going to benefit the business.

Q (Seamus, Oppenheimer & Company): Can you talk about what you need to do to move patients from the DME to the pharmacy? Is there anything that you can do to make that faster? And then with pay as you go as you move towards pharma, do you have to account for anything as a percent of bad debt or uncollectible as you switch to those contracts?

Ms. Vosseller: I'll answer the last one. Nothing particular to think about in terms of unusual accounting treatment, I would say in that regard. Think about it as a normal revenue stream as supplies are purchased over time and the question about how to move patients. The first thing we do is we share with them how much better the benefit can be for them coming out of pocket perspective. And so when you compare it to DME supplies, they often have to make deductibles at the beginning of the year so it can be heavier out of pocket then maybe it's best at the beginning of the year, but on pharmacy it can be more consistent and we actually have the ability ourselves to help, to help buy down or subsidize, if you will, that copay. And so the main thing is helping them understand the benefit and how much better it can be for them financially.

We also have people tell us how much they love our customer service and they fear this change might take away that relationship they have with us. And we're reassuring them that this is good for you financially, and we will maintain the same level of customer service that we have today. The only other I would call small friction piece, if you will, is it does take another prescription from the physician. We do need to get the physicians involved to write a new prescription for that patient within the pharmacy channel. None of these are insurmountable in terms of moving people over there. Just work them in they can. That's why it's not an overnight change. It's something we have to work on over time. But we feel very confident in our ability to be able to shift those customers, and especially as we build more and more access, it can be a broader offering across the whole market.

On international growth

Q (Chris Pasquale, Nephron Research): Thanks and appreciate all of the different metrics. This quarter is going to be helpful to track these initiatives as they go forward. John, I wanted to ask about the international transition. When you first sort of talked about this, it seemed like it was only going to be 2025 headwind. But now it sounds like it's going have a significant impact on 2026 and possibly even beyond, depending on what other countries are getting into late this year. Could you talk about why this is a protracted process and how do we think about the point at which, you know, you completed this transition to direct?

Mr. Sheridan: First of all, I think our team did an amazing job this year. When you think about it, we made the transition from the distributors. We began to hire sales force in the in the new markets that we're going into. And then we built and installed the infrastructure that will enable us to ship a product and bill for it. All of those are major tasks. I think I think that we're biting off a significant amount of operations when we go into these new countries this year. Of course, we're going to three this year. I think that trying to do it all at once would be just too risky. I think that putting it into a two year period is the right way to do it. As we did progressed this year, we essentially got all of that done and we are now live in those three countries and we installed all of the infrastructure to do that. We're basically using that as a playbook, and we're going to do the exact same thing this year for the next countries that come in 2027. So, you know, I think that we feel good about it. I think it's staged properly.

I think that when we get to 2027, that's the majority of the transition that we plan to make. I think locked in sort of in the long term, we tend to have a hybrid model where we do have direct business and we intend to continue to work with many of the fantastic distributors that we have in the international markets. But it's gone very well, and I think it's going to it's going to go just as smoothly in 2026 and 2027.

Q (Jon Block, Stifel): Can you talk to some of those moving parts internationally? It seems like you've got 3% revenue growth from the extra 30% price on an incremental 10% of volumes. What's the underlying growth? It seems like it might be, you know, 7%, 8%, high-single digits. And compare that to how you exited the year, which you're on a really, really good trajectory of, you know, mid to high teens.

Ms. Vosseller: You're right. There are a lot of moving parts, I think at the highest level I'll just start with the fact that we are we are actually very strong in the international market and continuing to expand the market. The majority of our shipments today still come from new customers, and we're just beginning to see a more meaningful contribution from the renewal opportunities there. And then you take some of these structural pieces and you think about it. As you come into 2026, we have the benefit from those markets that are going direct already that are going to provide that price appreciation. This year, you're not going to see the full effect of that 30% that you mentioned. That's the way to think about long term. Any market that goes direct, we should see a premium of approximately 30% in any given year. The pricing when you blend it this year, direct to distribution is probably mid-single to high-single digit price increase building up across the year as we transition into those markets. That is, the headwinds that we're going to see in the additional markets that are going to go direct this year. So as we think about that headwind, we've sized that at about $15 million. And thinking about, as I just mentioned, roughly $5 million-ish in the first quarter and the rest of it will be hitting in the back part of the year, probably the fourth quarter. But underlying all of this, we're very confident and excited about the opportunity we have in the market. Part of the reason we're going direct in these markets is this puts us closer to the customer, better able to sell and the benefits of our technology and bring more people over to Tandem.

On future growth drivers

Q (Danielle Antalffy, UBS): On the leverage, that was really nice to see in the quarter, and good to see in the guidance. I'm just curious what the different levers are here. Obviously, ultimately pricing and in the pharmacy and the significantly higher ASP there is helping. But could you talk a little bit about the levers going forward in 2026, and as you think over the next few years?

Ms. Vosseller: You named probably one of the biggest levers we have right now, which is pricing as we look at the value that can come from this transition that we're making in the pay-as-you-go model, that will continue to bear great fruit for us in the next couple of years in terms of a growth perspective on revenue and profitability. But also so important to remind that we do have a number of product cost reduction initiatives in place. One of them really comes from Mobi as we continue to build and scale that part of the business. In the long term, Mobi and we're getting very close with the pumps to being at scale. The manufacturing cost of a Mobi versus t:slim is 10% to 15% lower. So that's one piece of it. If we continue to build up the cartridges and think about that contribution, that will be 20% or lower or higher, I should say, reduction in cost versus the t:slim. So as Mobi continues to grow in scale, that will continue to drive gross margin benefit too. And then you can just take that forward and think about any new product that we launch.

Part of our design principles in the R&D process are to consider that new products need to have a better margin profile than the products that we have in the market today and continue to improve upon them the products that we have in the market today. And so I would say between pricing and our initiatives within the manufacturing and R&D areas, that's really what's going to drive that leverage in gross margin.

And then take it a little further down the down the P&L to the operating margin. Similarly, we continue to look at our infrastructure and think about what's the best way, how to be most efficient. And we're constantly looking for opportunities and ways to reduce the need to hire more people in the future and just better serve our customers with a lower head count base going forward.

On Mobi Tubeless

Q (Mike Kratky, Leerink Partners): I wanted to circle back on some of the Tubeless Mobi commentary. Did I have that right? You said planning on submitting the 510(k) submission in the second quarter of this year is the first part?

Mr. Sheridan: That's correct. We plan on submitting in the second quarter. We have had a great deal of very responsive support from the FDA, so we do feel highly confident that we'll get it approved in the second half of the year.

Q (Travis Steed from Bank of America Securities): You're talking about accelerating sales growth in 2027 and beyond, and it's been a while since I've seen you guys talk about a year ahead. I just want to see what is driving that visibility and confidence. How much of that is pay-as-you-go versus Mobi and as you kind of look forward and plan ahead?

Mr. Sheridan: I think the most impactful element is going to be the ongoing implementation of pay as you go. You know, we do have the headwinds this year, but we are going to be making substantial progress. And as we know, as we move and get more and more of our install base, more and more of our new customers into the PayGo model, the revenue impact of that is substantial. And so that's going to grow in time. I think most impactful is certainly going to be the transition to pay as you go. As we as we mentioned, in addition to the pumps and supplies that come along with the new pumps, there's also the opportunity to convert the 325,000 people who are existing customers to pharmacy as well. Both of those are meaningful.

We also have a very exciting pipeline. We have a lot of technology coming to the market this year. We will have the first extended wear patch in the market and that's going to be meaningful. I think that right now there is nobody competing with our patch competitor. We will have a device that has the same form factor. It'll be in the pharmacy channel, and it has a better algorithm. We expect that to do quite well. Beyond that, we've got a very exciting pipeline that's going to continue to come, including our move to a fully closed loop system with a hopefully we see that in the market in 2027 or 2028. I think all of these things add up to a confidence as a management team that we will see growth going forward in 2027 and beyond.

On type 2 diabetes

Q (Jayson Bedford, Raymond James & Associates): I wanted to ask a question on type 2. Could you please give us some color on the progress there? There was also an update to the ADA guidelines recently on C-peptide testing, but is this new guideline help with their discussions with CMS? And can this lead to an inflection in type 2 new starts?

Mr. Sheridan: We're excited about the type 2 market. It doubles the size of our addressable market in both the US and OUS. In 2025, we obviously got the indication, we ran the pilot, and we went into full commercial availability in the fourth quarter. We learned a great deal in the pilot, and we actually saw a pretty difficult bump in starts between the third and fourth quarter, the quarter that we actually had full organization working on this. As we as we look at 2026, it's basically a core that we intend to focus on type 2 and invest in marketing and also some research relative to PCP and OUS markets. I think we've got tailwinds as we enter the market with Freestyle Libre 3 Plus and Mobi implementation. Obviously, Mobi Tubeless in pharmacy channel is also going to drive uptick.

And relative to the C-peptide decision, it's also a potential positive for us as the Senate has asked CMS to review the NCD and make a decision in August of 2026, which is not that far away. Having that go away will substantially improve Medicare's access. We have one quarter's worth of data and it's very positive and I think that we're looking forward to seeing good growth in 2026 based on everything that we've got going on.

On 2027 and beyond

Q (Philippe, Truist): In the context of renewal pump shipments, we get a lot of questions about a potential drop off in 2027, considering the prior year drop off in new patient starts. I'm just wondering if you could help give us some context on how you're thinking about outyear pump shipments and how that fits into your strategy with pharmacy, and maybe any potential offset you can get in pharmacy if there is a potential drop off in pump shipments in 2027?

Ms. Vosseller: It's a great thing that I'd like to highlight. I think people have looked at our model and seen that when you look back four years ago, the number of opportunities will decline in the coming years a little bit from what we've seen before where we were on an uptick. And so this year in particular, we still expect renewal shipments based on the normal model and the waterfall that comes with it, that that renewal shipments will still grow double digits year-over-year. So we have that tail of opportunities, even though new opportunities in 2026 are flat versus what came to market in 2025. But I think it's a great tie into pharmacy as we look ahead and think about this model, it greatly reduces the reliance on renewals as a driver for the business, it's important that we retain our customers and we have really great retention rates, but we don't have to worry about going out every four years, and if a patient's comfortable with the pump they're on and it's working just fine, trying to convince them that they should buy their next pump or bring it back insurance cycles that come with it. I think for us, it's really important to transition these folks into the pharmacy channel where for them it's a lower out-of-pocket. It's easier for a physician to prescribe. And there's none of this worry about when I get my next pump.

As we look ahead, where the opportunities in the US at least will start to decline, that won't be a concern about our ability to grow the business. You didn't ask me about international. It has nothing to do with pharmacy, but I just want to underscore our renewal opportunity outside. US is growing and becoming a more meaningful contributor there, and there's a lot of room to benefit from that in the coming years.

On US renewal opportunities

Q (Mike King, Leerink Partners): I wanted to ask you about the US renewal opportunities. I think in 2025, it was up around 18% just for the opportunities, if I have my numbers right, and renewal shipments was up closer to around 10%. So if renewal opportunities is effectively flat for 2026, you know what's giving you confidence that you can really grow that double digits this year? And is there any kind of risk around that?

Ms. Vosseller: I'll just maybe give a little more direction on the shipments. In 2025, they were up well above 10%, so we did see a higher growth rate on renewal shipments. And then when you think about 2026 the number of opportunities are flat compared to 2025, so that's one population. The growth comes from the fact that we have a tail of customers from years past. And so remembering how our renewal model works when warranties expire over the course of about 18 months, we get to a 70% or better capture rate of people buying that next pump outside of warranty. And so what we have are still a fair amount of people from 2025, especially if you think about the people in the fourth quarter whose warranties expire that we leave hard leave and talk to you yet. There's still a fair number of a nice sizable opportunity base coming from 2025 and some even leftover from 2024 that's going to fuel the growth, so we can still grow renewals shipments double digits in 2026.

And then just wrapping it up with that concept again about pharmacy and the ability to shift people or transition them to pharmacy supplies, it will be it will take away that reliance on driving those renewal purchases at a pump. And we can just keep them on their supplies as long as they would like without having to worry about that, that timing of when renewals come to market. We're very excited, if you haven't taken that away from today, about this pharmacy opportunity for us as a business. And this year is going to be a great year of transition for it. I think you're going to really see some really exciting outcomes in the coming years, and so we look forward to demonstrating those in the coming quarters.

Close Concerns’ Questions

- What clinical milestones remain before Tandem can expect the potential FDA clearance of Control-IQ+ for pregnancy?

- Following the shift to direct commercial operations in select European markets, how much pricing improvement does Tandem expect relative to the prior model?

- How does management expect customer retention to change under the pharmacy model?

- How will expanded CGM interoperability influence clinician prescribing patterns?

- What proportion of new customer starts in 1Q26 and 2026 are expected to come from individuals with T2D?

-- by Jeremy Alkire, Riya Chatterjee, Nour Khachemoune, and Kelly Close