Medtronic files for IPO of Diabetes business, to operate as MiniMed – S-1 translates business to date –

S-1 filing advances planned separation; IPO followed by split-off remains the preferred path

Medtronic announced that it has filed a registration statement on Form S-1 with the US Securities and Exchange Commission (SEC) for an initial public offering (IPO) of its Diabetes business, which will operate under the name MiniMed. The filing confirms Medtronic’s previously announced plan to divest the Diabetes business, with leadership reiterating its preferred path of an IPO followed by a split-off. Unlike prior to its acquisition by Medtronic, MiniMed would list its common stock on the Nasdaq Global Select Market under the ticker symbol MMED, rather than MNMD[1].

Table of Contents

- S-1 filing adds detail to MiniMed’s global scale and financial profile

- S-1 filing reflects net loss of nearly $200 million in fiscal year 2025, ended April 2025

- MiniMed Reports $8 million in cash and cash equivalents ahead of IPO

- CGM attachment rate grows to 65% with addition of newest sensors

- MiniMed highlights strong glycemic outcomes with MiniMed 780G

- Innovation roadmap emphasizes choice, automation, and reduced user burden

- Innovation roadmap also shows focus on FCL – fully closed loop, via Vivera

- Close Concerns’ Questions

S-1 filing adds detail to MiniMed’s global scale and financial profile

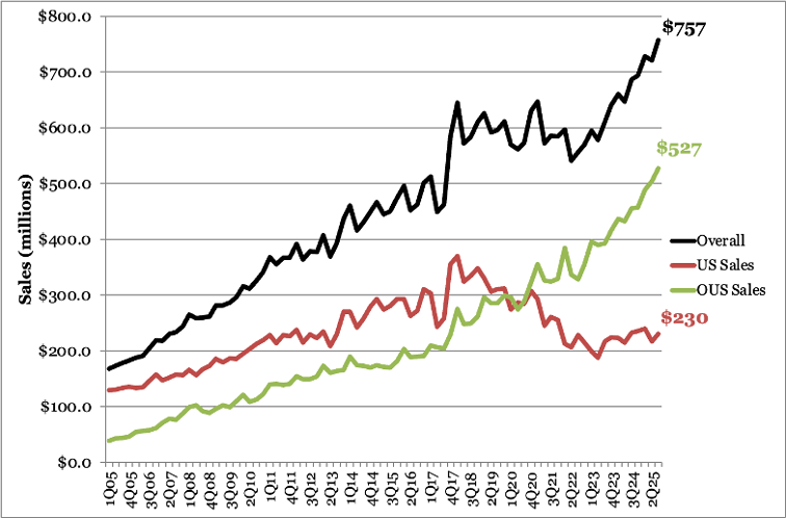

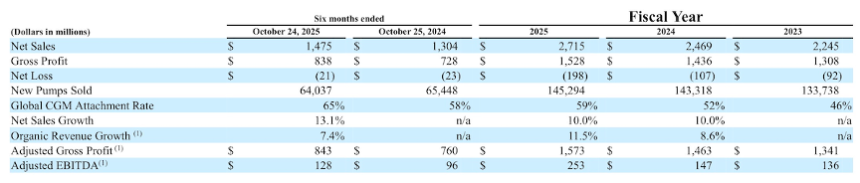

The S-1 filing provides visibility into the scale and financial profile of MiniMed as a standalone business. MiniMed reported $2.7 billion in fiscal year 2025 (FY25) revenue, with approximately 50% generated from continuous glucose monitoring sales, and approximately 30% reflecting sales from insulin sets (called “consumables”), software, and services (note we are not sure what is reflected in “service” revenue – see Q&A below). Consistent with commentary in our Medtronic 3Q25 report, the filing describes MiniMed’s strong international presence, a company that has approximately two-thirds of revenue generated outside the US (see graph below). This aligns management’s emphasis on sustained OUS momentum, particularly in Europe, where MiniMed 780G adoption and Simplera Sync uptake have driven sustained growth. We continue to hear great things about the MiniMed 780G’s algorithm in particular.

Medtronic Diabetes shared in the S-1 that its business serves more than 640,000 insulin pump users across 80 countries as of October 2025. By the end of 3Q25, we estimate over 1.5 million AID users globally, compared to over 11 million CGM users globally. Most recent updates from other companies (at the end of 2024) include Tandem, who shared an updated userbase of 480,000 in-warranty t:slim X2 users, and Insulet, who reported a global userbase of 365,000 Omnipod 5 users. Ypsomed last announced in May 2025 that the mylife Loop AID system achieved 70,000 active users, and Beta Bionics’ userbase is approaching 30,000. This translates to an estimated 3Q25 Aaron Ratio – the ratio of AID to CGM users, termed in honor of Breakthrough T1D CEO Dr. Aaron Kowalski’s efforts to make AID a reality – of ~14%, flat from 2024 and 2023. See below to better understand how international sales have become a much higher percentage of sales – now about two-thirds of all sales! – since we began tracking sales in 2005, when international sales represented just a small percent.

Medtronic Diabetes Revenue (1Q05 - 3Q25)

Source: Close Concerns Knowledgebase

S-1 filing reflects net loss of nearly $200 million in fiscal year 2025, ended April 2025

MiniMed reported FY25 adjusted EBITDA of $253 million (~9% margin), higher than $147 million in FY24 and $136 million in FY23. However, the company also reported a net loss of $198 million (1% of total revenue), which widened compared to $107 million in FY24 and $92 million in FY23. This reflects increased investment in R&D, manufacturing, and major marketing spend around pump and sensor launches.

In its S-1, MiniMed reported that its CGM products, including the newer Simplera and Simplera Sync, have placed pressure on its margins in the near term. As sensor volumes ramp, the company expects temporary margin compression, with margins expected to improve as manufacturing processes improve and become more efficient.

To offset these pressures, MiniMed plans to cost reductions across both Cost of Products Sold and operating expenses, including savings in variable and overhead costs. Longer term, the company is targeting high-volume and increasingly automated manufacturing, which it believes will help lower unit costs and improve gross margin, particularly as sensor and pump volumes grow.

As the business prepares to operate independently, we are curious how this might change, given investment required for legal, HR, and other elements required in independent companies. MiniMed will, of course, be paying royalties on sensors it does not manufacture, made by Abbott, and we applaud the company for providing choices to patients in this way. Following the IPO, Medtronic will still possess majority voting power, which is interesting – we’re curious what founder Mr. Al Mann would have thought about that, though presumably that will change over time.

MiniMed Key Business Metrics (FY23 – FY25)

Source: MiniMed S-1 filing

MiniMed Reports $8 million in cash and cash equivalents ahead of IPO

MiniMed reported $8 million in cash and cash equivalents as of October 24, 2025. Historically, the company’s working capital needs and capital expenditures have been met through Medtronic’s centralized cash management and funding programs, an arrangement that will remain in place through the anticipated separation. Following the separation, however, MiniMed will no longer have access to Medtronic’s corporate funding infrastructure. To support its standalone liquidity, the company plans to use a portion of the net IPO proceeds to repay an undisclosed amount of debt owed to Medtronic and retain the remainder. MiniMed also expects to enter into a five-year, senior secured revolving credit facility with total commitments of $500 million.

MiniMed expects the net proceedings from the IPO, its existing cash balance, positive cash flow from its operations, and funds available through the revolving credit facility will be sufficient to meet all of the company’s obligations for at least one year after the separation.

CGM attachment rate grows to 65% with addition of newest sensors

MiniMed’s reported global CGM attachment rate — the percentage of insulin pump users also using a Medtronic CGM — has increased steadily over the past three years, highlighting deepening engagement with the company’s diabetes technology ecosystem and growing uptake of its newest sensors. Simplera Sync has been available in Europe since 2Q24, and the Instinct sensor launched with MiniMed 780G in the US in December 2025. Since FY23, CGM attachment has risen by nearly 50%, increasing from 46% in FY23 to 52% in FY24, 59% in FY25, and 65% in the first half of FY26.

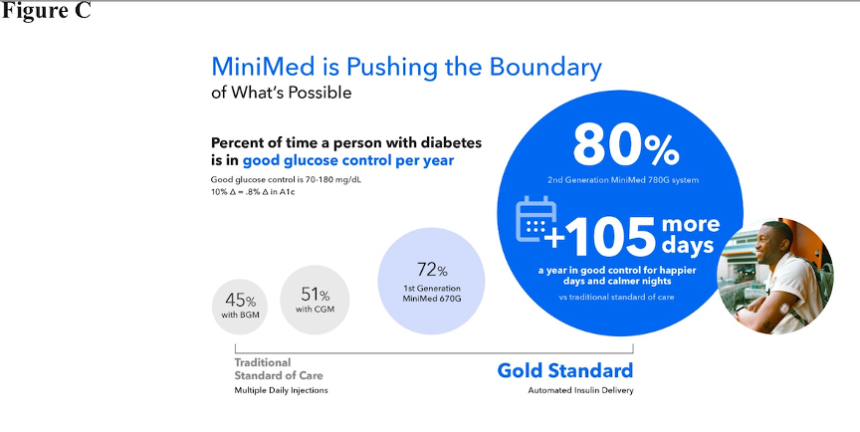

MiniMed highlights strong glycemic outcomes with MiniMed 780G

In its S-1, MiniMed highlights strong glycemic benefits of MiniMed 780G use compared with traditional standard care using MDI. Real-world use of MiniMed 780G translates to approximately 105 additional days per year in range, with TIR increasing from 45% with MDI to ~80%. This improvement exceeds what has been reported with CGM alone (~51%) and with the first-generation MiniMed 670G (~72%). Together with expanding real-world evidence across multiple geographies and with use of the system’s optimal settings, these outcomes are likely to support continued system adoption as MiniMed prepares to operate independently from Medtronic.

Source: MiniMed S-1 filing

Innovation roadmap emphasizes choice, automation, and reduced user burden

The S-1 reinforces the innovation roadmap Medtronic has outlined in recent earnings calls, while framing these programs within a standalone MiniMed growth strategy. Near-term priorities remain focused on (i) scaling MiniMed 780G with SmartGuard; (ii) expanding compatibility with both Simplera Sync and Abbott-partnered Instinct; and (iii) deepening its reach across the US and OUS markets, presumably starting with InPen.

The filing reiterates MiniMed’s 3Q25 update of pipeline and timeline for hardware innovations including:

- MiniMed Flex: A next-generation durable pump that will be 50% the size of MiniMed 780G and has already been submitted for FDA clearance, with a CE Mark submission planned by the end of 1Q26;

- MiniMed Fit: A patch-based AID system with extended wear, which the company in 3Q25 targeted for FDA submission by fall 2026; and

- MiniMed Go: A Smart MDI system intended to broaden access through initial pharmacy distribution, already submitted for FDA approval.

All platforms are expected to integrate with Simplera Sync and Instinct at launch, consistent with the company’s emphasis on interoperability across form factors. The company has also submitted Instinct for CE Mark approval, setting the stage for availability to expand beyond the US.

Innovation roadmap also shows focus on FCL – fully closed loop, via Vivera

In software, the S-1 references the recent FDA authorization of a US pivotal trial for Vivera, a fully closed-loop (FCL) algorithm designed to eliminate meal announcements and further reduce user burden. As the company shared in 3Q25, the pivotal trial is expected to begin in 1Q26. For us, the idea of FCL is still something where we have to imagine quite a lot. We can’t wait to see what happens next for Medtronic’s diabetes business, particularly with such a strong team, and with Que Dallara at the helm.

Close Concerns’ Questions

- How does MiniMed define “services” revenue in the S-1 and what components are included in this category?

- How will Medtronic and MiniMed manage operational separation challenges during the transition period, specifically across manufacturing and customer support?

- As MiniMed transitions toward independence, how will the company balance near-term investment in sensor launches and pipeline programs with longer-term expansion goals?

- How will MiniMed prioritize geographic growth as US sensor availability for both Instinct and Simplera Sync expands?

- How does MiniMed approach pricing strategy across international markets and to what degree are differences big enough from US pricing to that they impact gross margin?

- What is likely to happen with the Blackstone agreement over time? Why is there discussion of payments back to Blackstone, stemming from the investment made available back in 2020)?

--by Riya Chatterjee, Jeremy Alkire, Monica Oxenreiter, and Kelly Close

[1] While erstwhile fans of MiniMed, Inc. who remember the stock ticker for MiniMed pre-2001 was MNMD, before it was purchased by Medtronic, alas, the MDMD stock ticker now belongs to a company called MindMed whose mission is to provide psychedelic therapy to those with major depressive order, generalized anxiety, and autism.