Merck 3Q25 – Diabetes portfolio totals $703 million (+19%); Januvia franchise totals $624 million (+30%); phase 2 trial of MK-3000 for nAMD and RVO; BRUNELLO trial advanced for DME –

Executive Highlights

- Merck reported its 3Q25 results in a call led by CEO Mr. Robert Davis – see press release, presentation slides, webcast, financials, and prepared remarks.

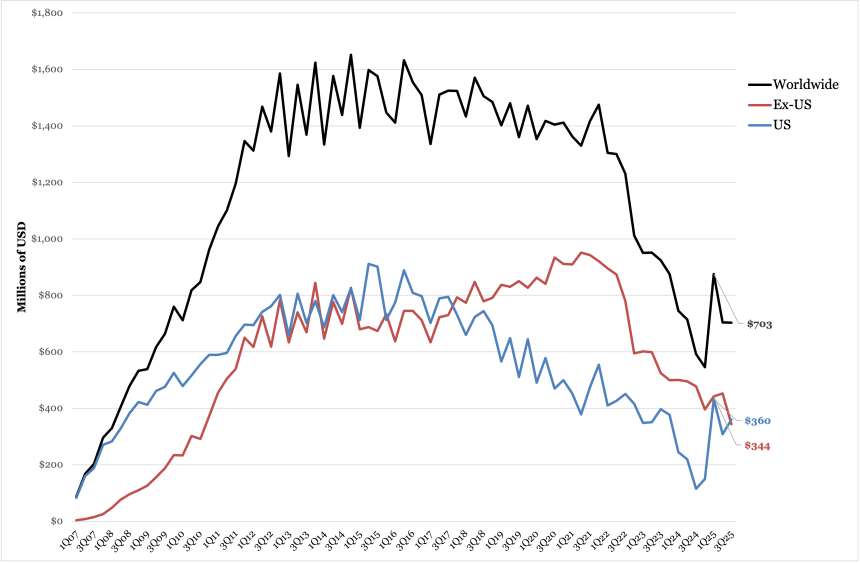

- In 3Q25, total Diabetes sales reached $703 million, up 19% from 3Q24 and roughly flat from 2Q25.

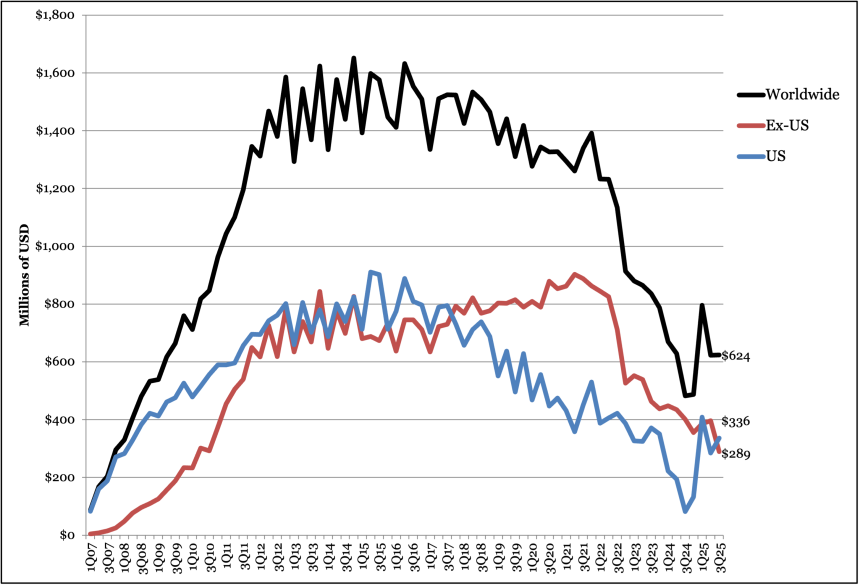

- The Januvia franchise (Januvia and Janumet) totaled $624 million, up 30% from 3Q24 and flat sequentially. US sales totaled $336 million, up a whopping 310% from 3Q24 and up 18% sequentially. OUS sales totaled $289 million, down 28% from 3Q24 and down 15% sequentially. The sharp increase in franchise sales in the US was attributed to higher net pricing in the US amid overall declines in the DPP-4 inhibitor market.

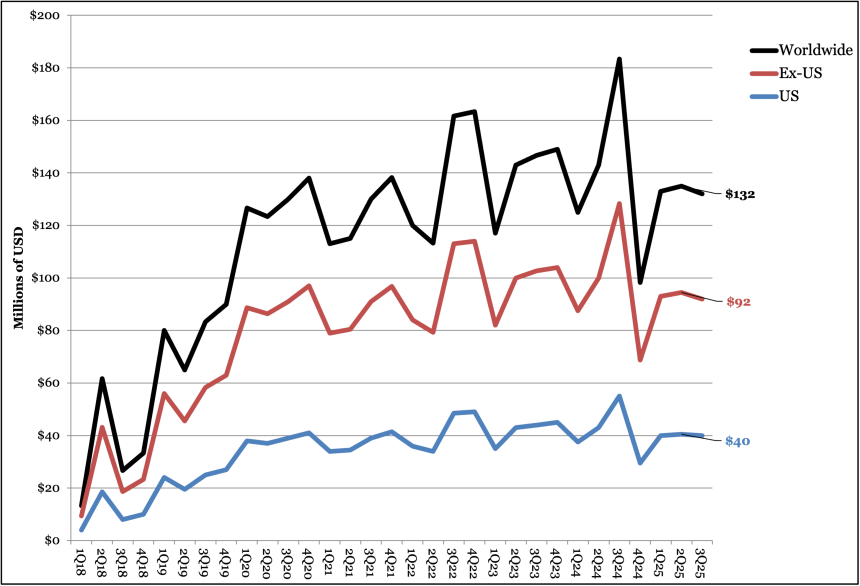

- Estimated revenue for SGLT-2 inhibitor Steglatro (ertugliflozin), which is partnered with Pfizer, totaled $132 million, down 28% from 3Q25 and down 3% sequentially. Estimated US revenue totaled $40 million (-28% YoY, -3% Q/Q) and OUS revenue totaled $92 million (-28% YoY, -2% Q/Q).

- In ophthalmology, Merck announced today that a phase 2 study evaluating MK-3000 for nAMD and RVO is currently enrolling, entitled SUPER TUSCAN. Late-stage trials are planned for 2026. The candidate joined Merck’s pipeline in its acquisition of EyeBio in 2024.

- The phase 2b/3 BRUNELLO trial in patients with DME was initiated in September 2024 and originally expected to complete in 2027. Merck announced today that enrollment has completed and the study’s primary completion date has been accelerated to September 2026.

- In incretin-based therapies, oral small molecule GLP-1 RA, MK-4082 (previously called HS-10535), was not mentioned on today’s call. The therapy is on track for clinical development this year.

- Merck’s GLP-1/glucagon receptor co-agonist MK-6024 (efinopegdutide) in MASH also continues progressing in a phase 2b trial (n=360), which is expected to complete in December 2025.

- Elsewhere in its cardiovascular pipeline, Merck is evaluating oral PCSK9 inhibitor enlicitide decanoate (previously called MK-0616) for hypercholesterolemia in phase 3 program. Two trials have been completed in 2Q25:

- CORALreef HeFH (n=303) evaluated enlicitide decanoate in adults with heterozygous familial hypercholesterolemia.

- CORALreef Addon (n=301) compared enlicitide decanoate ezetimibe, bempedoic acid, or combination therapy in participants with hypercholesterolemia already on lipid-lowering therapy. Merck’s topline results show that both trials met their primary and all key secondary endpoints, demonstrating statistically significant and clinically meaningful reductions in LDL cholesterol.

- The third phase 3 CORALreef Lipids trial (n=2,760), evaluating enlicitide decanoate vs. placebo in a broader population with hypercholesterolemia, completed in July 2025, in line with expectations. Merck announced that the study achieved all primary and secondary endpoints.

- Merck further updated its 2025 revenue guidance from $64.3-65.3 billion to $64.5-65.0 billion, tightening the range to just $0.5 billion after adjustments in 2Q25 as well. This range represents 1-2% growth, excluding a negative impact from foreign exchange of ~0.5%.

3Q25 Financial Results for Merck’s Diabetes Products

| Product | 3Q25 Revenue (USD millions) | Annual Growth | Q/Q Growth |

| Januvia Franchise | $624 | +30% | Flat |

| $382 | +37% | +3% |

| $243 | +19% | -3% |

Steglatro (ertugliflozin) *estimated | $132 | -28% | -3% |

*To date, neither Merck nor Pfizer has broken out revenue separately for Steglatro. We calculate sales based on the reported “total diabetes revenue” and the assumption that this revenue is split 60/40 between Merck and Pfizer.

Table of Contents

-

Financial Highlights

- 1. Januvia franchise sales total $624 million (+30% YoY, flat Q/Q); growth driven by higher net pricing in the US and partially offset by lower demand in China and other international markets due to generic competition

- 2. Estimated SGLT-2 inhibitor Steglatro (ertugliflozin) revenue totals $132 million (-28% YoY, -3% Q/Q)

-

Pipeline Highlights

- 1. Phase 2 SUPER TUSCAN study evaluating MK-3000 for nAMD and RVO is currently enrolling; BRUNELLO trial completion accelerated; phase 1 MK-8748 data

- 2. Incretin therapies: MK-4082 (oral GLP-1 RA) and MK-6024 (GLP-1/glucagon RA) for MASH remain in development

- 4. Summary of Merck’s diabetes/obesity/MASH-related pipeline

- 5. CORALreef Lipids trial meets primary and secondary endpoints for oral PCSK9 inhibitor enlicitide decanoate (MK-0616)

- Diabetes-Related Analyst Q&A

- Close Concerns Questions

Financial Highlights

Total Diabetes Revenue (1Q07-3Q25)

1. Januvia franchise sales total $624 million (+30% YoY, flat Q/Q); growth driven by higher net pricing in the US and partially offset by lower demand in China and other international markets due to generic competition

The Januvia franchise, which includes DPP-4 inhibitor Januvia (sitagliptin) and Janumet (fixed-dose sitagliptin+metformin), totaled $624 million, up 30% from 3Q24 and flat sequentially. US sales totaled $336 million, up a whopping 310% from 3Q24 and up 18% sequentially. OUS sales totaled $289 million, down 28% from 3Q24 and down 15% sequentially.

- The sharp increase in franchise sales in the US was attributed to higher net pricing in the US amid overall declines in the DPP-4 inhibitor market. Declines are thought to be partly driven by competition from other oral agents, such as SGLT-2 inhibitors, which are recommended by the ADA as a first-line therapy for people with diabetes and comorbidity risks. In a recent survey from dQ&A (n=2,796), just 9% of patients with T2D on oral diabetes therapies were taking a DPP-4 inhibitor.

- While other oral agents like SGLT-2 inhibitors are becoming increasingly popular, DPP-4 inhibitors may still have an important role in diabetes management and perhaps even diabetes prevention for select populations. In the VERIFY trial, early combination therapy with a DPP-4 inhibitor and metformin led to 26 more months with an A1c ≤7.0% compared to metformin monotherapy.

- Offsetting this growth, Merck said that international declines were explained by lower demand for the therapies in international markets due to generic competition, especially China. Generic versions of Januvia/Janumet are expected to enter the US market in May 2026 following patent expiration in China and Europe. Off-patent DPP-4 inhibitors include Tradjenta, Galvus, and Onglyza, with more patent expirations imminent.

Total Januvia Franchise (Januvia + Janumet) Sales (1Q07-3Q25)

Total Januvia Franchise Worldwide Financial Results – Past Five Quarters

| Total Januvia Franchise (Januvia + Janumet) | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – millions (USD) | $482 | $487 | $796 | $623 | $624 |

| Annual Reported Growth | -42% | -38% | +19% | -1% | +37% |

| Sequential Reported Growth | -23% | +1% | +63% | -22% | +19% |

3Q25 Januvia Franchise Geographic Breakdown

| Product | 3Q25 US Revenue (millions) | US Annual Growth | US Sequential Growth | 3Q25 OUS Revenue (millions) | OUS Annual Growth | OUS Sequential Growth |

| Januvia Franchise | $336 | +310% | +18% | $289 | -28% | -15% |

| Januvia (sitagliptin) | $258 | +285% | +19% | $124 | -41% | -20% |

| Janumet (sitagliptin/metformin) | $78 | +420% | +15% | $165 | -13% | -10% |

2. Estimated SGLT-2 inhibitor Steglatro (ertugliflozin) revenue totals $132 million (-28% YoY, -3% Q/Q)

Estimated revenue for SGLT-2 inhibitor Steglatro (ertugliflozin), which is partnered with Pfizer, totaled $132 million, down 28% from 3Q25 and down 3% sequentially. Estimated US revenue totaled $40 million (-28% YoY, -3% Q/Q) and OUS revenue totaled $92 million (-28% YoY, -2% Q/Q). As Merck and Pfizer do not break out revenue separately for Steglatro, we calculate Merck’s sales based on the assumption that the total revenue is split 60/40 between Merck and Pfizer with a 30/70 split between US and OUS. Accordingly, we estimate Merck’s total revenue of $79 million, with $24 million from the US and $55 million from OUS.

A phase 3 trial (n=165) of Steglatro in pediatric patients with T2D (ages 10-17 years) was completed in April 2025, with no mention on today’s call or in provided materials. We will continue to monitor for updates to study results and potential advances towards regulatory approval for an indication that includes children.

Total Steglatro Sales (1Q07-3Q25)

*US/OUS split estimated at 30/70 based on Januvia split

Pipeline Highlights

1. Phase 2 SUPER TUSCAN study evaluating MK-3000 for nAMD and RVO is currently enrolling; BRUNELLO trial completion accelerated; phase 1 MK-8748 data

Merck announced today that a phase 2 study evaluating MK-3000 for nAMD and RVO is currently enrolling,entitled SUPER TUSCAN. The therapy is a potential first-in-class tetravalent, tri-specific antibody that acts as an agonist of the Wingless-related integration site (Wnt) signaling pathway. Late-stage trials are planned for 2026. The candidate joined Merck’s pipeline in its acquisition of EyeBio in 2024.

- The phase 2b/3 BRUNELLO trial in patients with DME was initiated in September 2024 and originally expected to complete in 2027. Merck announced today that enrollment has completed and the study’s primary completion date has been accelerated to September 2026.

- Merck also announced phase 1 results of the RIOJA study this month, evaluating MK-8748, a tetravalent bispecific targeting antibody Tie2 and VEGF in patients with macular edema secondary to branch RVO and nAMD. Late-stage trials are planned for 2026.

2. Incretin therapies: MK-4082 (oral GLP-1 RA) and MK-6024 (GLP-1/glucagon RA) for MASH remain in development

Oral small molecule GLP-1 RA, MK-4082 (previously called HS-10535), was also not mentioned on today’s call. The therapy is on track for clinical development this year. In December 2024, Merck announced a partnership with Hansoh Pharma for MK-4082. Hansoh Pharma will receive an upfront payment of $112 million and is eligible to receive up to $1.9 billion in milestone payments. Hansoh Pharma may co-promote or solely commercialize HS-10535 in China, subject to certain conditions. Merck has previously suggested that MK-4082 offers opportunity as a “next wave” of obesity treatment.

Merck’s GLP-1/glucagon receptor co-agonist MK-6024 (efinopegdutide) in MASH also continues progressing in a phase 2b trial (n=360), which is expected to complete in December 2025.

- In June 2023, MK-6024 received FDA Fast Track Designation as a potential treatment for MASH. Merck has since initiated a phase 2b trial for this indication.

- At EASD 2023, results from the phase 2a trial (n=145) showed promising results. Efinopegdutide significantly reduced liver fat content (LFC) by 73% compared to 42% with semaglutide at Week 24. In the T2D and non-T2D subgroups, efinopegdutide reduced LFC by 67% and 79% compared to 45% and 39% by semaglutide, respectively.

3. Phase 2 trial continues of Hengrui x Merck’s HRS-5346, an oral small molecule Lp(a) inhibitor

HRS-5346, an oral small molecule Lp(a) inhibitor, was not mentioned today. In March 2025, Merck announced a partnership with Hengrui Pharmaceuticals for the development of the therapy. This candidate is currently being evaluated in a phase 2 trial (n=120) in China among adult participants with elevated Lp(a) at high risk for cardiovascular events. The trial has finalized enrollment and is expected to complete in December 2025.

- Under the terms of the agreement, Merck has exclusive rights to develop, manufacture, and commercialize HRS-5346 worldwide, excluding regions in China. Hengrui will receive an upfront payment of $200 million and is eligible to receive milestone payments associated with certain development, regulatory, and commercial milestones up to $1.8 billion, as well as royalties on net sales of HRS-5346, if approved.

4. Summary of Merck’s diabetes/obesity/MASH-related pipeline

See below for a timeline of Merck’s diabetes/obesity/MASH-related pipeline.

| Product | Product Details | Status | Timeline |

| Steglatro (ertugliflozin) | SGLT-2 inhibitor | Phase 3 – completed | Phase 3 trial in youth with type 2 diabetes (ages 10-17 years), initiated October 2019, completed in April 2025. |

| MK-6024 (efinopegdutide) | GLP-1/glucagon dual receptor | Phase 2 | Full phase 2a results presented at EASD 2023. Positive phase 2aresults announced, phase 2b trial initiated, and FDA Fast Track Designation granted in June 2023; phase 2 trialcompleted October 20, 2022, first announced in 3Q21; MASH candidate efinopegdutide being evaluated against semaglutide for liver fat reductions in participants with MASLD |

| MK-0616 (enlicitide decanoate) | Oral PCSK9 inhibitor | Phase 3 | In September 2025, Merck announced that all primary and key secondary end points were met in the CORALreef Lipids study. A reduction in LDL cholesterol for the treatment of adults with hypercholesterolemia was demonstrated. Phase 3 CORALreef HeFH completed in April 2025; phase 3 CORALreef Addoncompleted in March 2025; Enrollment complete in 2Q25 for phase 3 CORALreef Outcomes trial; Phase 3 trials initiated in August 2023; Data presented at ACC 2023; Phase 2 trialin hypercholesterolemia completed November 2022, data to read out at ACC 2023; Positive phase 1 results announced in November 2021; phase 1 trial in patients with moderate renal impairment initiated November 20021 with expected completion in February 2023 (pushed back from September 2022) |

| Verquvo (vericiguat) | Soluble guanylate cyclase (sGC) inhibitor | Approved for HFrEF | Phase 3 VICTOR study completed in February 2025; Included in the 2022 AHA/ACC/HFSA guidelines for HFrEF; approved in HFrEF in January 2021 based on positive results from phase 3 VICTORIA trial; phase 3 VICTOR study initiated November 2021, expected completion 2025 |

| Restoret (MK-3000) | Antibody targeting the Wingless-related integration site (Wnt) signaling pathway | Phase 2b/3 | The SUPER TUSCAN Phase 2 study is currently enrolling for patients with nAMD and RVO. Late-stage trials planned for 2026. Phase 2b/3 BRUNELLO trial initiated in September 2024 and expected to complete in 2027; acquired from EyeBio in May 2024 |

| MK-4082 | Oral GLP-1 RA | Preclinical | Added to pipeline from partnership with Hansoh Pharma in December 2024; expected to enter clinical trials in 2025 |

| HRS-5346 | Oral small molecule Lp(a) inhibitor | Phase 2 | Added to pipeline from partnership with Hengrui Pharmaceuticals in March 2025; Hengrui recently initiated phase 2 trial in China; partnership to advance global development program |

5. CORALreef Lipids trial meets primary and secondary endpoints for oral PCSK9 inhibitor enlicitide decanoate (MK-0616)

In its cardiovascular pipeline, Merck is evaluating oral PCSK9 inhibitor enlicitide decanoate (previously called MK-0616) for hypercholesterolemia in phase 3 program. Excitingly, two trials have been completed in 2Q25:

- CORALreef HeFH (n=303) evaluated enlicitide decanoate in adults with heterozygous familial hypercholesterolemia.

- CORALreef Addon (n=301) compared enlicitide decanoate ezetimibe, bempedoic acid, or combination therapy in participants with hypercholesterolemia already on lipid-lowering therapy.

Merck’s topline results show that both trials met their primary and all key secondary endpoints, demonstrating statistically significant and clinically meaningful reductions in LDL cholesterol.

The third phase 3 CORALreef Lipids trial (n=2,760), evaluating enlicitide decanoate vs. placebo in a broader population with hypercholesterolemia, is expected to complete in August 2025. Merck announced that the study achieved all primary and secondary endpoints.

CORALreef Outcomes (n=14,550) trial, assessing cardiovascular outcomes, has completed enrollment and is expected to be completed in November 2029.

- As background, in a phase 2b trial (n=381) in adults with hypercholesterolemia, enlicitide decanoate significantly lowered LDL-cholesterol levels by 41-61% in a dose-dependent manner and was safe and well-tolerated over the eight-week treatment period (presented at ACC 2023). Moreover, 80-90% of patients receiving enlicitide decanoate reached their LDL-cholesterol goals.

Diabetes-Related Analyst Q&A

On ophthalmology

Q (Alexandria Hammond, Wolfe Research): On EyeBio, can you help with the Phase 3 BRUNELLO results in context? What's the bar to deem the trial a success? And I guess given the competitive nature of this indication, how do you plan to execute commercially?

Dr. Dean Li, EVP: Well, let me just say that we're really excited about pushing this first-in-class MK-3000 novel candidate targeting the Wnt pathway. I would just remind, I believe this is the first time a novel mechanism has been pushed through in relationship to having clear human genetic evidence for it. And we plan to evaluate that MK-3000 not just in diabetic macular edema, but also in neovascular age-related macular degeneration as well. In terms of commercial sort of execution, I would hold off until we see the data from these trials. But we're pushing very fast and very forward in relationship to this, because this could be one of the first new mechanisms, kind of like the WINREVAIR story, where it's the first generally new mechanism that can make a profound effect on such a broad disease.

Mr. Robert Davis, CEO: To add a little bit on the commercial opportunity, and if you look at where we are today in the United States, there's about 1.6 million patients with diabetic macular edema. So, this is the leading cause of vision loss in people with diabetes. And so, as you look at that population, still there's a very large opportunity, because 30% to 40% of patients on therapy are not responsive to the current anti-VEGF. So, the ability potentially to see conversions is significant. If you look, it's about a $13 billion market today, and we believe that our ability to drive that kind of conversion with this new molecular entity is important. As far as the commercial infrastructure, we're really combining the EyeBio's leadership strengths and our expertise in ophthalmology and pushing these forward, and I'm quite confident that we will have the global infrastructure to be able to drive this. We're investing pretty heavily behind this. And when you look at this and combined with the Tiespectus, this is a multibillion-dollar opportunity for the company. We're very excited. I think this is one of the underappreciated areas of what we have, and I credit Dean and the team. They've advanced these by a couple of years from what we originally anticipated when we did the deal. So, this is a win in my book.

On financial outlook

Q (Terence Flynn, Morgan Stanley): I know you commented somewhat on expenses for 2026. I was just wondering if you can give us any comments on the top line in terms of some of the pushes and pulls as we think about that, recognizing you probably don't want to give guidance yet at this point, but just maybe help us think through some of the levers there.

Ms. Caroline Litchfield, CFO: As we go into 2026, we are expecting solid top line growth for our company, and that growth will increasingly be fueled by the number of new launches that we have. So, we're expecting continued patient impact and revenue growth from WINREVAIR. OHTUVAYRE now is also part of the Merck portfolio. We have CAPVAXIVE, which is off to a very strong start, and ENFLONSIA. And on top of that, we have our Animal Health business, where growth will also be driven by new launches, including BRAVECTO QUANTUM, the 12-month injection, as well as NUMELVI, our new dermatology product. We also have the expectation of continued growth in oncology. To the last question, WELIREG has strong growth with greater potential ahead of it, as we get into other successful studies and treat a broader range of patients. And we do expect continued growth in KEYTRUDA, albeit at a slightly slower pace than we've seen, as we are getting to peak penetration in some of the indications, and we do expect some headwind from price in our ex-US markets. The other headwinds that we will face will be related to loss of exclusivity and generic entrants, and that really is DIFICID that's seen generic entrant halfway through 2025 in the US; BRIDION, which will have its LOE partway through 2026. And we also expect the headwind of IRA price-setting on the JANUVIA family and the generic entrant for JANUVIA midway through next year. But overall, confident in our ability to continue to positively impact patients and drive solid growth.

On tariffs and MFN pricing

Q (Chris Schott, JPMorgan): Following some of the recent deals of the administration both with Pfizer and AstraZeneca, should we be thinking about this type of structure as a reasonable framework for the industry? And just any updates in terms of where Merck is in terms of its discussion with the administration on MFN?

Mr. Robert Davis, CEO: Overall, we're aligned with what the administration is trying to achieve, which is to lower the out-of-pocket costs for patients at the pharmacy counter, and at the same time, to get foreign prices up to ensure that foreign governments are paying their fair share. So, those broad-based principles, we're aligned with. We are in continuing discussions with the administration. I'm not going to give any specific updates, other than to say, I am very optimistic that we're going to have a constructive outcome to those discussions. And the framework, we'll wait until we actually have something to talk about there to be more specific to how we see ours coming out.

Q (Courtney Breen, Bernstein Institutional Services): Just coming back to some of the White House price policy pressures and comments you've made already, I wanted to ask this in a slightly different way. If we look at kind of Merck's ratio of revenue today, it's about 50/50 inside the US versus outside the US. How different do you expect that to be in five years' time? And how much of that could be attributed to product mix and how much down to kind of equalization of price?

Mr. Robert Davis, CEO: I'm not going to get into specific guidance. Obviously, if you look at where our business is driving, we're excited about the diversity of the pipeline we're bringing. A lot of those opportunities disproportionately will be US-based, primarily just because of the nature of the drugs and the uptakes and the value you can assert to the US market. So, mix will affect how we look forward. How MFN or other pricing dynamics change, it's too early to say, because we need to see what it is. And so, I would leave it at that for right now.

Close Concerns Questions

- How is Merck preparing for Januvia’s loss of exclusivity in 2026? Might Merck promote Januvia in emerging markets in different ways than expected?

- Will Merck share phase 3 results (n=165) of Steglatro in pediatric patients with T2D (ages 10-17 years) and seek regulatory approval for this population?

- Which treatment, in combination with PCSK9 enhibitor enlicitide decanoate, would demonstrate the strongest efficacy for cardiovascular outcomes?

- How might efinopegdutide compare to other GLP-1/glucagon compounds in development, regarding efficacy and tolerability in MASH?

How does Merck view its additional ophthalmology offerings in tandem with its cardiometabolic pipeline?

--by Nour Khachemoune, Monica Oxenreiter, and Kelly Close