embecta 3Q25 (F4Q25) – Pen needle co-packaging for generic GLP-1 RAs expected in 2026 in Canada, Brazil, and India; reported revenue of $264 million (-8%) –

Executive Highlights

- embecta announced its 3Q25 (F4Q25) financial results (press release, presentation, webcast) on a call this morning led by embecta’s CEO Mr. Devdatt (Dev) Kurdikar and CFO Mr. Jake Elguicze.

- Mr. Kurdikar reaffirmed that embecta is collaborating with over 30 pharmaceutical companies to co-package embecta’s pen needles with generic GLP-1 RA offerings. These partnerships are expected to lead to launches in the Canadian, Brazilian and Indian markets during 2026, alongside the commercial launch of generic GLP-1 RAs. Previously, embecta had identified the UK as a market of promise for generic GLP-1 RAs, but no mention was made of this on today’s call.

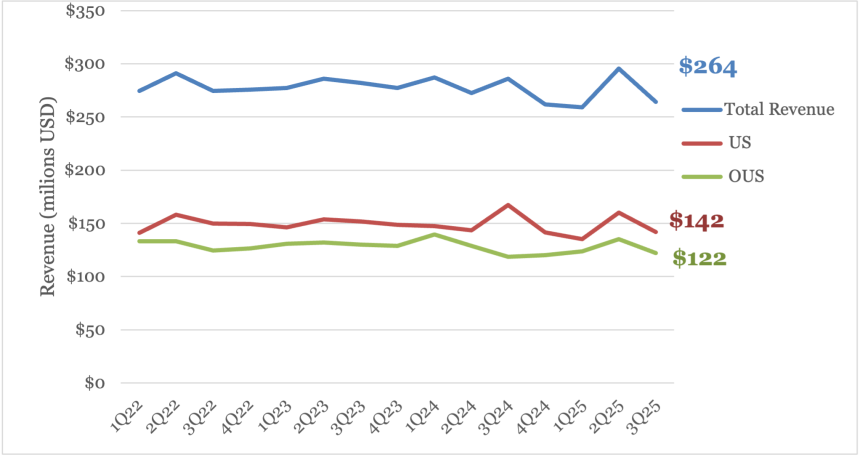

- In 3Q25 (F4Q25), embecta reported total revenue of $264 million, down 8% from 3Q24 (F4Q24) and down 11% sequentially. By product type, pen needle and syringe revenue fell to $189 million (-13%) and $32 million (-4%), respectively, while safety product and contract manufacturing revenue grew to $35 million (+5%) and $5.3 million (+13%), respectively. Mr. Kurdikar said that declines in pen needle revenue was driven largely by reduced demand from China, where customers are currently favoring domestic manufacturers. He also noted that previous short-term increases in US sales also contributed to the apparent decline in US sales this quarter.

- Declines in US sales were also attributed to an unfavorable comparison to 3Q24. The quarter benefited from unusual additional distributor orders totaling approximately $10 million. These occurred due to concerns of an anticipated US port strike at the time, as discussed in the company’s 3Q24 report.

- embecta also issued preliminary FY26 worldwide revenue guidance of $1.071-$1.093 billion, which would represent approximately -0.9% to +1.1% growth compared to FY25. Mr.Elguicze said that the company expects revenue growth to remain approximately flat from FY 2026 through FY 2028, as discussed at this year’s investor day.

- Modest declines of approximately 1% to 2% in core injection and contract manufacturing revenue are expected during this time period, which will be offset by new contributions from revenue streams such as expanded GLP-1 RA opportunities and distributed product partnerships.

embecta announced its 3Q25 (F4Q25) financial results (press release, presentation, webcast) on a call this morning led by embecta’s CEO Mr. Dev Kurdikar and CFO Mr. Jake Elguicze. Read our top highlights below.

Table of Contents

Pipeline Highlights

1. embecta expects co-package agreements for pen needles and generic GLP-1 RAs to become available in 2026 in Canada, Brazil, and India

Mr. Kurdikar reaffirmed that embecta is collaborating with over 30 pharmaceutical companies to co-package embecta’s pen needles with generic GLP-1 RA offerings, up from 10 originally announced in 1Q25. This rapid partnership growth may signal significant future offerings and security for the company. He said that co-packing agreements have already been signed with several companies and that the pen needles have already been included in multiple regulatory submissions managed by the partner companies. These are expected to lead to commercial launches in Canada, Brazil and India during 2026, alongside the launch of generic GLP-1 RAs in these markets. Previously, embecta had identified the UK as a market of promise for generic GLP-1 RAs, but no mention was made of this on today’s call.

- He added that embecta is also continuing to expand the availability of pen needles in small packs targeted at self-pay GLP-1 RA users. This is currently available in Canada and select European markets. Mr. Kurdikar reaffirmed that, along with its co-packaging agreements, the long-term impact of this development could lead to more than $100 million in annual revenue for embecta by 2033.

- During Q&A, Mr. Kurdikar said that embecta has already shipped pen needles in this capacity, mainly for co-packaging development work. The company expects to supply pen needles directly to its partners, who will then co-package the pen needles with pen injectors. embecta’s partners will also be responsible for marketing and regulatory submission.

- Mr. Kurdikar said that embecta has initiated new product development programs for market-appropriate syringes and pen needles to strengthen and expand the company’s portfolio. embecta intends to expand its reach into market segments in which it does not currently operate.

Financial Highlights

1. Worldwide revenue of $264 million (-8%); US revenue of $142 million (-15%); OUS revenue of $122 million (+3%)

- In 3Q25 (F4Q25), embecta reported total revenue of $264 million, down 8% from 3Q24 (F4Q24) and down 11% sequentially. By product type, pen needle and syringe revenue fell to $189 million (-13%) and $32 million (-4%), respectively, while safety product and contract manufacturing revenue grew to $35 million (+5%) and $5.3 million (+13%), respectively. Mr. Kurdikar said that declines in pen needle revenue reflected international preferences influenced by US-China relations and previous short-term increases in US sales (see more below). Syringe revenue decreases were attributed to broader end market volume declines as insulin vial prescriptions continue to decrease compared to insulin pens.

- US revenue totaled $142 million, down 15% from 3Q24 and down 11% sequentially. Mr. Kurdikar attributed this decline to an unfavorable comparison to 3Q24, which benefited from unusual additional distributor orders totaling approximately $10 million. These occurred due to concerns of an anticipated US port strike at the time, as discussed in the company’s 3Q24 report. Turning to sequential declines, Mr. Kurdikar said that favorable order timing in 2Q25 associated with the Independence Day holiday in the US positively impacted last quarter’s results with a benefit of about $7 million, leading to the tough comparison in 3Q.

- Internationally, embecta reported $122 million in revenue, up 3% from 3Q24 and down 10% sequentially. Mr. Kurdikar noted that international revenue declined 4% on an adjusted constant currency basis, which he attributed to lower volumes and YOY pricing headwinds within China. A significant, growing preference for local Chinese brands was discussed in the context of the evolving US-China geopolitical and trade environment, which has led to increased competition in China. However, Mr. Kurdikar said that this was partially offset by performance in other emerging markets.

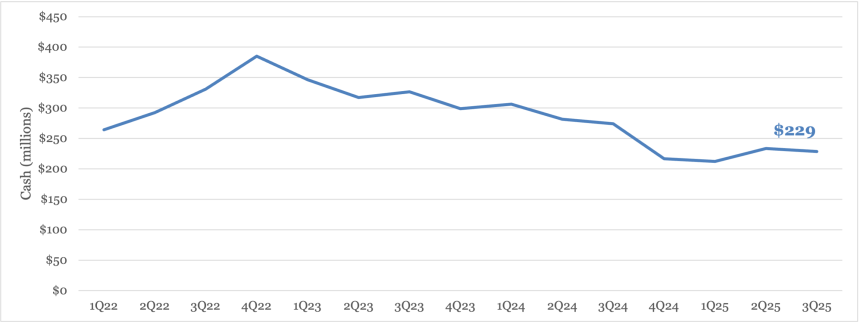

- embecta reported $229 million in cash and cash equivalents at the end of the quarter, down from $234 million in 2Q25. embecta reported $1.42 billion of debt principal outstanding, slightly down from what the company reported last quarter ($1.49 billion). embecta repaid an aggregate principal amount of $72 million during 3Q25. This brings full-year repayments to $184 million, which Mr. Kurdikar said exceeded the fiscal year target of $110 million set by the company. He described FY25 as a year of solid execution on multiple fronts, including in financial discipline and debt reduction.

2. Preliminary FY26 revenue guidance issued of $1.07-$1.09 billion (an estimated -0.9% to +1.1% growth); expected adjusted operating margin of 29%-30%

- embecta issued preliminary FY26 worldwide revenue guidance of $1.071-$1.093 billion, which would represent an approximate -0.9% to +1.1% growth compared to FY25. Mr.Elguicze said that the company expects revenue growth to remain approximately flat from FY26 through FY28, as discussed at this year’s investor day. Modest declines of approximately 1% to 2% in core injection and contract manufacturing revenue are expected during this time period, which will be offset by new contributions from revenue streams such as expanded GLP-1 RA opportunities and distributed product partnerships.

- embecta expects an adjusted operating margin of 29%-30% in FY26. Mr. Elguicze said that two factors are expected to contribute equally to this: adjusted gross margin is expected to decline due to increased cannula costs, while incremental tariffs are expected to have a negligible impact compared to FY25. R&D expenses are anticipated to be 2% of revenue as embecta explores the development of pen needles and syringes and efforts to use alternative cannula suppliers.

Analyst Q&A

On the GLP-1 opportunity

Q (Marie Thibault with BTIG): Good morning! I wanted to see if I could learn a bit more about the GLP-1 partnerships that you have. Can you give us a little more detail on how many partners you have signed deals with? Can you share anything on timing or how they might be ordering ahead of any regulatory approvals on their side, just so we can get a little more detail on how this might impact fiscal year 2026? And, how might these factors be assumed in your revenue guidance?

Mr. Devdatt Kurdikar, CEO: Thank you for the question. We are in discussions with 30 plus potential GLP-1 entrants. As you remember, this is all about co-packaging of pen needles. They are moving through various stages of discussions. We go through quality agreements, and we talk about MSAs. A handful of them have already provided orders, and we've shipped some product during 2025. Much of the volume is for their own development purposes as they work out what additional data they need for their regulatory submissions. Several of them have also submitted to the regulatory authorities already, and the rest are in control of the timing and the content of the submissions. We believe many of them will include specs that our products satisfy.

The timing of commercial quantities is contingent on when they get approval and which of the products get approval. As you might have heard publicly, generic GLP-1s could be available in calendar year 2026 in China, India, Brazil and Canada. There is obviously some uncertainty associated with timing. But overall, we are very pleased with the progress that we made in fiscal year 2025. I mean, you might remember, a year ago we were just starting discussions with these companies, and the team has made tremendous progress since then. We remain confident in the estimates that we had laid out during the Analyst Day of this being over a $100 million opportunity for us by 2033.

Mr. Jacob Elguicze, CFO: I'll also jump in on guidance. The low end of our guidance range assumes a negligible impact in terms of new revenue streams, mostly associated with GLP-1s, while the high end of our revenue guidance range assumes that new revenue streams, mostly coming from GLP-1s, would contribute positively by about 1%. We feel very good about where this is all going. Dev mentioned that over the longer term that we feel that this can be at least $100 million annual product revenue for embecta through 2033, and we feel like we're well on our way towards achieving that.

Q (Anthony Petrone, Mizuho Americas): To start on GLP-1s and the generic contracting phase, could you talk a little bit about how those contracts are going to be structured? Typically, when we have drug device combination solutions, you're in the clinical phase, but if you get to market, you essentially get written into the drug master file and its instructions for use, and that can be a multiyear contract. How does contracting work with the generic GLP-1 providers in the clinical development phase, and what will those look like once we get to a commercial phase? How long will there be minimum quantities baked in? And how do the economics work over a medium-term contract?

Mr. Kurdikar: I don't want to get too far ahead of myself with respect to commercial quantities and commercial contracts until some of these generic manufacturers get approved. But let me provide additional color. As we go through the contracting phase, we get NDAs in place. We get qualified as a vendor in our system that includes providing some quality and regulatory data on a product, and we put quality agreements in place. Then we start talking about contracting and get a contract complete. We'll talk about commercial contracts once some of these drugs become commercial.

The quantities that they are ordering now are really to do their own development work. We will be supplying bulk pen needles to these manufacturers. They are going to co-package bulk pen needles with their pen injector, and then they will be the ones to market that combined product to patients. They also are going to be responsible for the regulatory submission for the whole package, which includes the drug and the device. We'll help with providing data, but they are responsible for that submission and our pen needle will get factored in.

Once you are part of that combination, that imparts a level of stickiness to the product. Since their co-packaging lines will be configured to accept our pen needles, that provides some additional stickiness to our product as part of that combined package. Most importantly, I want to point out something that might seem obvious. We have a long history in demonstrating reliability of supply. And if you are a generic manufacturer that's introducing a generic GLP-1 drug, I would think that you would want your pen needle supplier to be somebody you can depend upon and that has long demonstrated reliability of supply. Additionally, our pen needles are already approved in markets where you would expect generic GLP-1s to launch.

With respect to profitability, I would also say is that these are bulk pen needles. We don't expect to spend any significant CapEx in meeting this demand. And so we would expect there to be some incremental margin drop as compared to our corporate averages of gross margin. Obviously, I won't comment on pricing.

In a final comment, we've established conversations with generic drug companies, and we are also expanding the conversation to work with them on supplying for other devices that they may use. On Analyst Day, I said the nearest adjacent device to us would be a pen injector. I'm hopeful that supplying devices to generic drug companies for their generic GLP-1 drugs is just the start as we transition from pure injection delivery for an insulin company to a broader medical supplies company.

On China

Q (Marie Thibault with BTIG): I'd also like to ask a follow up on China. You referred to some geopolitical tensions. What are you seeing on the ground in China in terms of consumer willingness to buy non-Chinese products? Of course, the product is made in China, but is not a Chinese brand. Do you have any additional updates on how that is playing out?

Mr. Kurdikar: To start, China in 4Q25 performed very close to, or almost exactly in line with, our expectations. When we revised our FY25 guidance, we incorporated a significant year-over-year decline, partially because of the pressures that you mentioned and partially because of some inventory rebalancing. We've taken steps to stabilize the situation, including reorganizing our sales team. We've introduced a more price competitive pen needle, which also has a lower manufacturing cost. Our guidance for 2026 does incorporate some expectations around new headwinds, but our current expectation is that it's going to be much less than what we experienced in 2025. As we all read in the press, the situation continues to evolve, but we are focused on controlling what we can to stabilize the situation there as quickly as possible.

I did want to note, though, that over the long term we still believe that this is going to be an important market for us. The market itself is growing mid-single digits. As you know, we have strong commercial and manufacturing infrastructure in China. You've heard us refer to the development of a market-appropriate pen needle. That pen needle is being developed by our team in China, and I'm quite hopeful that it will serve a segment in China that we don't serve today. You also asked about GLP-1s earlier. There are generic GLP-1 companies in China that have global aspirations that we obviously want to serve as well. Over the long term, we still think it's going to be an important market for us, and we'll find a way to weather through the evolving landscape.

On revenue and guidance

Q (Michael Polark, Wolfe Research): I also wanted to ask about fourth quarter performance. I heard price was unfavorable year-on-year, and you mentioned a $7 million milestone payment to a large US pharmacy customer. I just want to make sure I understand what that is. If you could add any color on that dynamic, I'd appreciate it.

Mr. Kurdikar: I won't talk about the specific contract, but our contracts with US chains have a rebate level. There are sometimes spend items that we contribute to the marketing of our products. Finally, upon the achievement of certain volume levels, there typically is an additional payment, and we often refer to them as milestone payment. At the end of the day, it all comes down to price, but depending upon the timing of the payments, it can lead to year-over-year unfavorability or favorability for the course of that quarter.

Q (Anthony Petrone, Mizuho Americas): I had a follow up on capital deployment. You mentioned CapEx, but the leverage ratios are coming down. The company has previously talked about forging additional partnerships outside of GLP-1s or being more focused on tuck-in M&A. To take the temperature on capital deployment outside of GLP-1 and the immediate CapEx needs, do you see any tuck-in M&A opportunities over the next couple of years?

Mr. Kurdikar: I'm very pleased with how our profitability metrics ended up with respect to our guidance. As you saw, we exceeded the top end of our gross margin, adjusted EBITDA margin, and adjusted operating margin, and that allowed us to pay down significantly more debt in 2025. It also brought our net leverage down, as you pointed out, to 2.9 times. Our capital allocation plans remain unchanged from what I said on investor Day. With projected $600 million in free cash flow over the next three years, most of that will go to paying down our debt. We pay a dividend at this point, we are not considering changing that.

Our highest priority still remains paying down debt. But as our leverage comes down, it's already below 3, and as we drive it down further in 2026, we are very open to organic and inorganic investments. M&A by its nature is very opportunistic. We will continue to be alert and aware if such an opportunity arises. And we feel that it is going to be value accretive to our company, and help transition the company towards long term sustainable growth. We will be ready to act on it.

Q (Gracia Mahoney, Bank of America Securities): In your prepared remarks you mentioned selling certain intellectual properties of $10 million associated with the patch pump subsequent to year end. So just wondering if you could add any more details around this, and what's baked into your assumptions moving forward that is associated with this?

Mr. Kurdikar: We did sell certain IP and associated assets to Bayer for $10 million. We are pleased to be able to monetize these assets from the patch pump program that we discontinued about a year ago. I'll let Jake comment on, this was really a 1Q26 event for us. But I'll let Jack comment on how you should expect to see that run through the financials.

Mr. Elguicze: It will obviously be an increase to cash from a guidance standpoint. This isn't going to impact our adjusted results that we provided guidance metrics for today. There'll be a gain most likely on the sale of these assets. And as a result of that, we're just going to normalize that for purposes of our adjusted operating margins or earnings per share.

Q (Gracia Mahoney, Bank of America Securities): To follow up, you had the pharmacy closures earlier this year and the stocking dynamic for July 4th and ahead of the brand transition. So, a lot of one-time benefits. Can you just speak to any more detail of how you saw that play out in the second half of 2025, and maybe if there's any sort of visibility on that into 2026 on how the pharmacy volumes are moving forward?

Mr. Kurdikar: As you pointed out, earlier in the year we commented on planned store closures at a major US pharmacy chain. We don't sell directly to that pharmacy chain. We sell to a third-party distributor that also serves other customers. As I said at that point, our product is medically necessary. If a store closes, patients will shift to other chains and other sources to procure a product. As expected, we saw strength at some other chain outlets, and we incorporated our thoughts around what the impact of the closures will be into our 2026 guidance. In the guidance that Jake went through, he talked about 100-basis point range in the volume assumptions. That includes our thoughts on what might happen with the US pharmacy volume as well.

One final point on how 2025 played out. We had started the year with the original guidance, and we did see China year-over-year headwinds that were not incorporated in our original guidance. As the year played out, including the impact of store closures, we would have been within the range of our original guidance had it not been for China. I think the store closures are playing out as we thought they would. Patients will move to other outlets, where we'll see strength, and we incorporated our thoughts in the 2026 guidance.

On the cannula market

Q (Michael Polark, Wolfe Research): I have two smaller questions. I'm interested in your cannula comments. You talked about increased costs and an effort to source alternative suppliers. Could you unpack that for us a little bit? Why are the costs up, and what does the opportunity look like to find other sources to mitigate that creep?

Mr. Kurdikar: Just as a reminder, the entire supply of cannulas that we get is from our previous parent BD. We have a cannula supply agreement with them that goes until 2032. So, it's solely sourced from BD right now. We do want to have an alternate supplier for cannulas, though, and our team has been working on this for the last couple of years. We've identified a couple of alternate suppliers and made significant progress, including running some trials with alternate cannulas and doing some development work.

I feel confident that we will have our current supply of cannulas to 2032, and I feel reasonably confident that we are going to have at least one alternate supplier here qualified well before our current agreement runs out. That allows us an alternate supply with a different cost profile, because since we became independent, the increased cost to us has been a significant contributor to the pressure we've placed on gross margin.

Mr. Elguicze: Dev mentioned what the margin profile of the company looked like pre-spin-off, during 2025, and exiting 2025. Pre-spin-off, our gross margins were around 67%. For 2025, our adjusted gross margins finished just under 64%. The entirety of the decline over those years really came down to just increased cannula costs. So it really is important for us to find an alternate provider, both from a risk mitigation standpoint, and you never want to be beholden to one sole source, and then also to drive some price decreases in the future as well.

In terms of our fiscal year 2026 guidance in relation to 2025, we talked about our adjusted operating margins being down about 180 basis points at the midpoint compared 2025 levels. About half of that is in the gross margin line entirely due to increased cannula costs, and the other half of that is just increases in terms of R&D expense as we need to make some investments to come to market with an alternate cannula provider, as well as some of those market appropriate low cost products for pen needles and syringes to service some of our emerging markets.

Close Concerns’ Questions

- While embecta’s partners will be responsible for packaging and marketing the combined pen needle and GLP-1 RA offerings, how will embecta position this offering from its company perspective?

--by Nour Khachemoune, Monica Oxenreiter, and Kelly Close