Lexicon 3Q25 – FDA end-of-phase 2 meeting for pilavapadin in DPNP by end of year; all IND-enabling studies for non-incretin oral LX9851 for obesity completed; SONATA-HCM trial of sotagliflozin on target for completion in 2026 –

Executive Highlights

- Lexicon Pharmaceuticals announced 3Q25 results this morning in a call led by CEO Dr. Mike Exton, CMO Dr. Craig Granowitz, and CFO Mr. Scott Coiante – see the press announcement, presentation, and webcast.

- Lexicon continues to pursue non-incretin approaches to obesity. The company confirmed that all IND-enabling studies of LX9851 are complete and have been submitted to licensee Novo Nordisk. As background, LX9851, a non-incretin oral candidate that inhibits Acyl-CoA Synthetase 5 (ACSL5), is in preclinical development for obesity and weight management. Lexicon and Novo Nordisk announced an exclusive licensing agreement for LX9851 in March 2025.

- Pilavapadin, an oral non-opioid AAK1 inhibitor for the treatment of diabetic painful neuropathy (DPN), advances. In the phase 2 PROGRESS trial, presented at EASD 2025, pilavapadin 10 mg resulted in a two-point reduction from baseline in average daily pain scores (ADPS) by Week 12. Moreover, a pooled analysis of the phase 2 RELIEF-DPN-1 (n=319) and phase 2 PROGRESS (n=416) trials support advancing the 10 mg dose into phase 3 development for DPN. In today’s call, management shared that its end-of-phase 2 meeting is scheduled with the FDA during 4Q25, with a phase 3 trial expected to launch in 2026. Parternship discussions for the drug are ongoing.

- Enrollment continues to accelerate for the phase 3 SONATA-HCM trial (n=500) of sotagliflozin in symptomatic obstructive or nonobstructive hypertrophic cardiomyopathy (HCM), which can lead to heart failure. Lexicon has initiated all 130+ of its sites in 20 countries across the US, EU, Israel, and Latin America. Lexicon plans to complete the study by the end of 2026 and file for regulatory approval in 2027.

- In Q&A, management shared the potential for sotagliflozin in large-scale cardiology clinics where HFpEF and HCM patients present very similarly. A differentiated option for both conditions, particularly for non-obstructive HCM, will help support broad utilization in a significant population of cardiology patients.

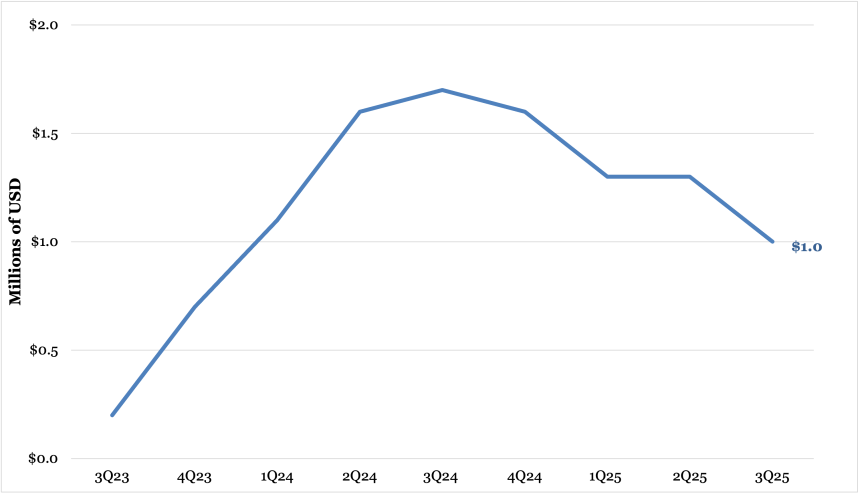

- Revenue for dual SGLT-1/SGLT-2 inhibitor Inpefa (sotagliflozin) for heart failure and T2D with CKD or CVD totaled $1 million in 3Q25, down 41% from 3Q24 and down 23% from 2Q25.

Table of Contents

-

Financial Highlights

- 1. Inpefa (sotagliflozin) revenue totals $1 million in sales (-41% YoY, -23% Q/Q)

- 2. Cash and cash equivalents total $145 million (-44%)

- 1. Full study site initiation completes for the phase 3 SONATA-HCM trial of sotagliflozin in hypertrophic cardiomyopathy; data expected in August 2026

- 2. All IND-enabling studies of oral ACSL5 inhibitor LX9851 completed and submitted to licensee Novo Nordisk

- 3. Potential partners engaged for development of AAK1 inhibitor pilavapadin (LX9211) for DPN; end-of-phase 2 FDA meeting scheduled in 4Q25

- Analyst Q&A

- Close Concerns Questions

Financial Highlights

1. Inpefa (sotagliflozin) revenue totals $1 million in sales (-41% YoY, -23% Q/Q)

Revenue for dual SGLT-1/SGLT-2 inhibitor Inpefa (sotagliflozin) for heart failure and T2D with CKD and CVD totaled $1 million in 3Q25, down 41% from 3Q24 and down 23% from 2Q25.

As background, Lexicon removed all commercial operations for Inpefa in November 2024 in response to the FDA’s “deficiencies preclude discussion” letter on the application for Zynquista’s (sotagliflozin) in T1D and CKD. Lexicon determined that Inpefa sales alone could not sustain commercial operations due to challenges in heart failure market access, which is currently saturated by SGLT-2 inhibitors like Lilly’s Jardiance (empagliflozin) and AZ’s Farxiga (dapagliflozin).

Globally, Viatris acquired exclusive licensing for Lexicon’s sotagliflozin in all markets outside of the US and Europe in October 2024. Lexicon’s commercial partner Viatris continues to pursue approval in OUS markets. Lexicon announced today that it had shipped the first commercial order of Inpefa to Viatris in the UAE – the first country to obtain regulatory approval outside the US.

2. Cash and cash equivalents total $145 million (-44%)

Lexicon ended 3Q25 with $145 million in cash and cash equivalents, down 44% from 3Q24 and up 4% sequentially. Management further detailed that the projected R&D expenses will be between $70-$75 million, down from a potential range of $100-$105 million projected in 1Q25. In comparison, R&D expenses in 2024 were approximately $85 million. The decreased spending primarily reflects slower external research expenses on the PROGRESS clinical trial, partially offset by increased investment in the SONATA phase 3 trial.

Pipeline Highlights

1. Full study site initiation completes for the phase 3 SONATA-HCM trial of sotagliflozin in hypertrophic cardiomyopathy; data expected in August 2026

Lexicon has completed its full study site initiation for the phase 3 SONATA-HCM trial (n=500) of sotagliflozin in symptomatic obstructive or nonobstructive hypertrophic cardiomyopathy (HCM), as enrollment continues to accelerate. The trial has now initiated in all 130+ sites in 20 countries across the US, EU, Israel, and Latin America. Lexicon plans to complete the study by the end of 2026 and file for regulatory approval in 2027.

- Approximately 1.1 million people in the US have HCM, with obstructive and nonobstructive HCMrepresenting 70% and 30% of the population, respectively. Notably, 43% of patients with HCM progress to heart failure. In 2Q25, Lexicon shared that only 1% of this market has been penetrated with novel therapies, emphasizing the potential for sotagliflozin to enter an underpenetrated market with significant needs.

- Lexicon launched the SONATA-HCM trial in July 2024 with a primary endpoint measured with the change from baseline in the Kansas City Cardiomyopathy Questionnaire (KCCQ) score. SONATA-HCM is currently enrolling participants based on HCM symptoms, their KCCQ score, and regardless of background therapy, such as beta blockers or cardiac myosin inhibitors (CMI).

2. All IND-enabling studies of oral ACSL5 inhibitor LX9851 completed and submitted to licensee Novo Nordisk

Lexicon shared today that all IND-enabling studies of LX9851 are complete, with results submitted to licensee Novo Nordisk. LX9851 is a non-incretin oral candidate that inhibits Acyl-CoA Synthetase 5 (ACSL5). It is in preclinical development for obesity and weight management. In March 2025, Lexicon and Novo Nordisk announced an exclusive licensing agreement for LX9851. Under the terms of the agreement, Lexicon is responsible for completing the Investigational New Drug (IND) application-enabling studies, while Novo Nordisk will file the IND and advance the candidate through clinical development, manufacturing, and global commercialization. Lexicon will receive $75 million in upfront and near-term payments and up to $1 billion in development, regulatory, and commercial milestone payments from Novo Nordisk. As of today’s call, Novo Nordisk is preparing for IND submission and initiation of clinical development, which would trigger up to $30 million in near-term milestone payments to Lexicon.

- Lexicon received an upfront payment of $45 million in April and is eligible to receive up to $1 billion in upfront and potential development, regulatory sales, and milestone payments. Lexicon is also eligible for tiered royalties on net sales of LX9851.

- Management reaffirmed that its partnership will leverage Novo Nordisk’s global expertise in obesity and related conditions to maximize the potential of LX9851. The company remains on track to submit an IND for LX9851 in obesity by the end of this year under its license with Novo Nordisk.

3. Potential partners engaged for development of AAK1 inhibitor pilavapadin (LX9211) for DPN; end-of-phase 2 FDA meeting scheduled in 4Q25

Lexicon has completed additional pooled analyses of phase 2 studies for pilavapadin, an oral non-opioid AAK1 inhibitor (LX9211) for adults with moderate-to-severe diabetic peripheral neuropathy (DPN). In today’s call, management characterized this candidate as “a portfolio in a pill with multiple near-term catalysts.” By analyzing the phase 2 data (n>600), management shared that the results support the broad potential for this novel mechanism and the advancement of pilavapadin 10 mg to phase 3. Specifically, management highlighted:

- Validated biological efficacy. Greater exposure, as measured by plasma blood concentration of pilavapadin, led to greater reduction in the pain score (ADPS) from baseline.

- Clinically meaningful efficacy. Pilavapadin conferred a two-point reduction in the pain score from baseline at 12 weeks – an increase from the 1.7-point reduction with the 10 mg dose observed in the phase 2b PROGRESS trial.

- Acceptable tolerability. 7% of participants reported dizziness (vs. 2% in placebo), 9% reporting nausea (vs. no reports), and 6% reporting constipation (vs. no reports). Both treatment and placebo groups had discontinuation rate of 12%, suggesting that adverse events did not outweigh therapeutic benefits.

- Acceptable safety. Pilavapadin did not cause serious ventricular arrhythmias, indicating cardiac safety. Moreover, patients with varying degrees of kidney function (mild to moderately impaired) experienced no significant differences in pilavapadin pharmacokinetics.

Lexicon has scheduled a phase 2 meeting with the FDA for 4Q25, with written feedback anticipated in early 2026. Previously, the company had planned to complete an end-of-phase 2 meeting with the FDA in 2Q25. Pilavapadin’s patent extends through 2041 including an anticipated five-year extension, which would offer a long period of exclusivity to maximize the commercial value of the asset.

- As the potential first nonopioid therapy in DPN in over two decades, pilavapadin could help meet the needs of nine million people in the US with progressive DPN. Among this population, 60% have tried multiple treatments, and a third have resorted to opioid treatments for short-term pain relief, which increases the risk of subsequent dependencies or use disorders.

- The company noted a chronic pain roundtable from October 7, wherein representatives across clinical, patient advocacy, and other experts gathered in Washington D.C. to advocate for health policies on chronic pain. The meeting focused on expanding access to non-opioid pain medications to Medicare Part D patients.

- Lexicon reiterated its interest in seeking partners to develop pilavapadin across global markets and multiple indications. Specifically, management stressed that Lexicon’s approach to partnership is flexible as the company remains focused on its internal cardiometabolic pipeline. Lexicon hopes to continue its partnership engagements after the end-of-phase 2 meeting in 4Q25.

Analyst Q&A

On pilavapadin

Q (Mr. Yigal Nochomovitz, Citi Group): Regarding the Partnership Opportunity and DPNP, can you arrange us on how far along you're identifying your partner and remind us whether or not you are waiting to complete the discussions for the end of Phase 2 meeting with FDA before completing any partnership agreements.

A (Dr. Mike Exton, CEO): Over the last, I'd say four weeks to six weeks, we've re-engaged with a range of partners who we had originally discussed the top line data with. Obviously, the data that we presented over the last month, including the totality of the phase 2 program, we've had the opportunity to talk with all of these partners. The end of phase 2 meeting is a very important milestone in those discussions.

I think it's fair to say, in a space where there's been nothing developed for two decades, in a space where new draft guidance has come out, it's important to have that confirmation as a part of those overall discussions. We're really looking forward now that that in the phase 2 meeting is scheduled for this year to continue to progress around that. We feel very confident actually with the dossier that we've submitted and are really looking forward to having the FDA's endorsement on what we think is a robust phase 3 program that reflects the draft guidance and that will certainly be a part of the partnering discussions that we're having.

On sotagliflozin

Q (Mr. Andrew Tsai, Jeffries): For the Zynquista in type 1 diabetes, you're seeking regulatory feedback in Q4. Are you looking for like a simple yes or no, for whether a resubmission would make sense, or is there perhaps more color that you're seeking? And then, if you're able to resubmit in 2026, would it be a class one or class two resubmission?

A (Dr. Craig Granowitz, CMO): As [Dr. Exton] has mentioned and we've discussed previously, we're really leveraging ongoing trials – particularly the standard trial in Denmark – to use the exposure data in a very large number of patients to address the single concern that FDA raised at their end of review meeting: a prospective study to document rates of diabetic ketoacidosis. And as you might recall, and as the CRL letter that was made public by the FDA a few months ago mentioned, the FDA accepts that there is efficacy with this drug as meaningful reductions in A1C, meaningful reductions in severe hypo effects, and obviously, the proven outcome that we've already seen in the labeling we have in patients with Type 1 diabetes and heart failure. We are using the standard trial with adequate levels of exposure, which is what we're really discussing with the FDA to prepare a submission really focus on that one single issue. To answer your second question. We don't have final written confirmation of this with the FDA, our expectation is that this would be as a resubmission, a six month review.

A (Dr. Exton): To provide a little more color from my side, I think what's really pleasing here is that the FDA has endorsed and accepted the steno protocol. Patients that they're capturing are acceptable and the way they're capturing DKA is acceptable. As we move forward, it really is around appropriate exposure levels to be able to give them confidence that the positive data that we are seeing gives them confidence for resubmission.

Q (Mr. Joseph Plunkett, HC Wainwright): With regard to the upcoming end to Phase 2 study, you've already provided some nice details around that. I want to make sure I understood you already have a lot of great feedback. Is there anything you would describe as questions that are left to address or finalize? And then, if Zynquista would move forward on the regulatory front in a positive fashion, what kind of commercial plan would you potentially be looking at? Bringing it forward on yourself, a potential partner, or what have you?

A (Dr. Granowitz): In the end of phase 2, when it comes to the endpoint – the duration of the study and the patient population –we feel very comfortable with that and I think that's been validated as well for other companies that are in phase 3 in neuropathic pain and diabetic neuropathic pain. It will be two trials of roughly 300 to 350 patients each with a 12-week visual analog pain score with an average daily pain score outcome. With any centrally acting agent, some of the areas of discussion are going to be regarding potential for central effects such as drowsiness. There's always going to be a question with any agent in this regard, even though there is no reason to believe and we don't believe that there is any issue of human addiction, potential type activities. We don't believe that there are any meaningful or significant next day drowsiness or other central effects of this agent and there is no indication in the large phase 2 program that we've run, including blinded withdrawal, that there is any issue around addiction potential. But, those certainly are areas that that could be points of discussion with the FDA.

A (Dr. Exton): Allow me a couple of moments here to talk a little bit more generally, philosophically about how we're commercializing surgical flows. As you know, one of the first things that we did when I came into Lexicon was unfortunately having to relook at how we commercialize Inpefa. I want to state categorically that both Zynquista and for HCM are not going to be Inpefa situations for a couple of reasons, as you know Inpefa was third to market, or actually fourth really, in a space where they would be three, particularly two major incumbents. That made market access incredibly difficult. What we're seeing actually is that when physicians use this medicine and patients use them, it's incredibly sticky. Access was a very difficult situation. That is not the case for Zynquista or HCM. Why is that? Because it will be the first and only SGLT inhibitor potentially indicated in each of these indications. That does a couple of things. First, it allows us to completely rethink pricing in both of these indications. That has certain implications, particularly in HCM, where the CMIs are priced at a significant multiple to what other medicines are being used. Secondly, and perhaps more importantly, there's not an ability at the pay level to substitute or to step through. And so, the access conditions for Zynquista and HCM are very, very different now. That does not mean that we intend to go with a full-blown traditional commercial model. In fact, that's part of our installing the Inpefa virtual sales support system that we've got, which is all encompassing. We'll have an opportunity perhaps to talk you through that, which is a good way for us to learn over the coming months of how we do this in a non-traditional way, whether that be a completely virtual field presence, whether that be looking at a hybrid, or whether it be even partnering on co-promotion – which could be an option. We're exploring all of these details in parallel. Of course, the other thing that makes us really excited is we have partnered with patient groups over years now, well before I joined the company. There's interesting commercial models that we can use and utilize some of this patient driven advocacy like, for example, in my experience we've seen with migraine and other conditions, where patients just have this pent up demand and we can do it in a very unique way. More to come on that. We're certainly exploring how we intend to potentially promote Zynquista should it come on the market.

Q (Mr. Andrew Tsai, Jeffries): For those third-party IST studies for sota and HCM and HFPAF, how do you expect the non-HCM data to perhaps give you greater conviction in the phase 3 SONATA study success?

A (Dr. Granowitz): Clearly, there's an overlap between have HFPAF and HCM. From a clinical standpoint, they are in essence indistinguishable. You see a very similar profile. You have normal ejection fraction, but you have patients that have symptomatic dysfunction, particularly diastolic dysfunction. And I think as you've seen with the CMIs, they're actually trying to go from HCM into HFPAF. I think they're having some challenges with that because a lot of patients are then developing ejection fractions that are dropping below 50%. We believe that by demonstrating data and you'll see some of that as early as this weekend in an oral late breaker at AHA, as well as our continued mechanistic data that it will be presented on Friday at HCM. We are distinguishing the effects of sort of proposing in both the preclinical models on energetics and cardiac remodeling that will fit very nicely with some of the clinical results that you might be seeing in HFPAF patients. They'll be presented at the SOTA-P-CARDIA data on Saturday at HCM. It continues to build a wall of evidence that is similar between HFPAF and HCM regarding cardiac energetics, cardiac remodeling, cardiac fibrosis and ultimately improved functionality and symptomatology in patients either with HFPAF or with HCM. And again, and symptomatology in patients either with HFpEF or with HCM.

Allow me to sort of pile on there from a commercial bent of how we see this. Now, we have this program in HCM for both obstructive non obstructive thinking that a medicine that is an oral once-daily, easy-to-use and a well-known and understandable side effect profile, particularly given the data coming out of Maple really gives us a great opportunity potentially to work alongside CMIs, but in a first line position in HCM. That first line position particularly is used sort of expanding outside of the of the HCM centers into real cardiologists and large-scale cardiology practices allows HFpEF and HCM, the patients present very similarly in those offices. Having an option for both HFpEF and a differentiated option for HFpEF and HCM gives the cardiologist peace of mind that they can use this medicine very successfully in either condition and particularly in non-obstructive, where diagnosing the difference between the two is a little more challenging. Both from a utilization as well as scientifically, we continue to generate additional data that will help support the use of this in a broad range of cardiology patients in, in across the cardiology community in the US.

Q (Mr. Yigal Nochomovitz, Citi Group): Understanding that you're seeking a broad HCM label in your discussions with the FDA, have they suggested the possibility that you would also be able to get approval for specifically in non-obstructive or obstructive HCM if data from SONATA is stronger in one particular subgroup?

A (Dr. Exton): We're approaching it similar to how we approached heart failure, where we had a broad label. We're really taking that same approach with the FDA and the commitment we have on them. When we met with them to discuss the protocol before initiating the trial, was that this, if the study is positive as conducted, would give us a label that would include both obstructive and non-obstructive patients. So, we are seeking that. We are looking to have two groups of 250 patients each within the study there is a stratification by obstructive versus non-obstructive, but the overall endpoint is anchored to the overall population.

Q (Mr. Joseph Plunkett, HC Wainwright): First, I think it would be helpful if you remind us when sotagliflozin moves forward? If it were to be positive, can you discuss the positioning with the continued growing excitement in the HCM space? Where would sotagliflozin be positioned with regard to these other assets?

A (Dr. Exton): I think it's first important to note that patients on a CMI are actually eligible to enroll in patients on a CMI are actually eligible to enroll in SONATA. And we've purposefully taken the approach again of using a very pragmatic trial that so that can be used in conjunction with underlying meds that are used in hypertrophic cardiomyopathy. Now, where I would say the positioning is typical across a lot of chronic medications. As much as those medicines that are somewhat more laborious, somewhat more costly, often depending on sort of where it ranges and, you know, often positioned as sort of later lines in therapy. We would see sotagliflozin as we discussed a little bit earlier as being broad potential, not only being used in the somewhat restrictive academic centers that have HCM study sites and clinical sites, but really across the broad scope of cardiology. It’s a known mechanism that's easy to use. If we get positive results out of SONATA in both obstructive and non-obstructive, it allows this broad utilization. And particularly given the results of the MAPLE trial, which showed that in fact, beta blockers don't necessarily add any value. There's a question as to whether they may be causing some harm in HCM. I think that offers for us a really good opportunity to become a first line agent in HCM, both obstructive and non-obstructive.

A (Dr. Granowitz): To add one other point, I think it's becoming more clear, Joe, and I think you've seen and heard some of these presentations even very, very recently that all of the CMIs that are currently under regulatory review will have REMS of some sort. That certainly does put significant paperwork in process in place for patients being initiated. I think that inherently is going to limit the sites that are willing to do that because you need to have a critical mass in order to create the paperwork flow. There'll be many places that will have HCM patients in relatively low numbers that will not be willing to take on that burden. I do think the fact that the CMIs will have REMS and there might be differentiated REMS between them, but there will be significant limitations that are always a part of a REMS. We don't have any inclination that that would be the case with sota, which is a well-known agent that has already an indication for heart failure.

Q (Ms. Yasmeen Rahimi, Piper Sandler): We know it's an exciting year this year and especially considering that there can be a few presentations on the SGLT1 and SGLT2 inhibitors in HCM and the preclinical models. Could you help us understand how much proof-of-concept data we could gain from these presentations in HCM?

A (Dr. Granowitz): We look at any one of these presentations and particularly a pre-clinical model as part of a broader tableau around the mechanism of action. Particularly, the functionality of both the SGLT1 and SGLT2 effects of SONATA. Whether we're looking at the effects on stroke and MI, whether we're looking at the FX and have passed over looking at the FX in HCM. As you know, we've generated data on all of those over the past year and have published on that extensively.

The data from the Boston Group that will be presented tomorrow at the HCM meeting continues that narrative. In a particular murine model, this group has a lot of experience and a long track record and the effects that they've seen with sota in that model. I don't want to presage their presentation, but I think are quite dramatic. I'll just provide the overview is that it's affecting the energetics. There are some mechanistic data around the energetics effects of sota in that model. By affecting and improving cardiac energetics, you're approving improving fibrosis and other cardiac remodeling, but most importantly, ultimately diastolic function. As you know, the major physiologic issue in HCM is diastolic stiffness. There's really two main issues physiologically in human hypertrophic cardiomyopathy. In obstructive, there is a physical barrier to outflow track obstruction. That really is what distinguishes between obstructive and non-obstructive HCM. Fundamentally the issue that is common, whether it's obstructive or non-obstructive, is cardiac hyperdynamic function, where the actin and myosin are overly active. There's also an issue around altered energetics. We believe that sotagliflozin is acting on both of those fundamental physiologic characteristics. That's why we believe and we had strong support from the medical community and the FDA that we could study both obstructive and non-obstructive in the same trial because the underlying pathophysiology is the same regardless of whether they are obstructive or non- obstructive, which is really defined anatomically as opposed to physiologically.

Q (Ms. Yasmeen Rahimi, Piper Sandler):. Once the phase 2 meeting is completed, how soon do you envision a partnership materializing? And what are your thoughts on the type of deal that you could explore that you would be interested in?

A (Dr. Exton): I think we will continue those engagements after the end of phase two meeting and certainly into the start of 2026. The type of partnership and the type of partners that we're engaging with are really pretty diverse. I think that gives us optionality as to how we take our involvement with delivery moving forward. We'll continue to engage with them. We'll wait for the minutes of this later to have that formalized, which will be in early 2026, and then we'll take it from there.

Close Concerns Questions

- What is Lexicon looking for in a partner for the development of pilavapadin?

- How does Lexicon plan to penetrate the HCM market? Would Novo Nordisk’s market expertise help inform the launch of sotagliflozin for HCM?

- Will Novo Nordisk explore other indications such as MASH and cardiovascular disease for LX9851? How might this align with the expressed interest in combination therapy?

- Given the 4Q25 FDA meeting timeline, when does Lexicon anticipate beginning phase 3 trials for pilavapadin?

--by Elizabeth Rose, Kat Moon, Monica Oxenreiter, and Kelly Close