JPM 2025 Full Report –

Executive Highlights

- The 43rd Annual JP Morgan Healthcare Conference wrapped up in mid-January at the Westin St. Francis Hotel in San Francisco. With what appeared to be sharply increased security compared to JPM 2024 and years earlier (we’ve been very lucky to have attended this conference for over two decades), the conference nevertheless progressed very seamlessly. We extend our appreciation to JPM for organizing an especially strong agenda, featuring standing-room only keynote addresses and fireside chats, along with many SRO addresses, in addition to engaging panel discussions, and extremely insightful presentations by industry leaders. A series for women investors in a new “Union Square” room was very popular, featuring very original commentary and discussions - the “sea of pink” was very striking!

- GLP-1 RAs dominated discussion throughout much of the week, as the diabetes and obesity fields continue to be even more dominant over time, moving to become one of the forefronts of the conference. Though the pace of innovation to much better address the diabetes and obesity epidemics continued to both expand and to receive more attention, we were surprised not to hear more about SGLT-2 inhibitors as well as GLP-1 agonists and GLP-1/GIP combinations.

- Of note, some of the days were simply packed with CEOs from the diabetes and obesity “worlds” – for example, on Monday, Vertex’s CEO, Dr. Reshma Kewalramani, opened the entire meeting, speaking in the Colonial Room, followed by Dexcom’s CEO Mr. Kevin Sayer. Both set a pattern for the rooms being absolutely packed during many sessions of the conference! Novartis’ CEO Dr. Vasant (Vas) Narasimhan spoke in the giant Grand Ballroom, and those interested in CV and metabolic health stayed put, as AstraZeneca’s and Sanofi’s top management followed (though we were hoping to hear something from Sanofi on the novel disease-modifying therapy Tzield, of course we know it is still a very small business compared to the typical ones discussed at this giant meeting). Bayer was next, where we were delighted to hear more about Kerendia momentum, then lunch, which featured General (Ret.) Mark Milley, who was the 20th Chair of the Joints Chiefs of Staff (2019-2023) and Ms. Rivka Friedman, Morgan Health’s Head of Innovation. In the afternoon, there was more to learn, with Lilly’s CEO Mr. Dave Ricks speaking, followed by Insulet’s CEO, Mr. Jim Hollingshead.

- See many of our top highlights below with eight conference themes across pipeline innovation in diabetes therapy and technology, clinical trial advancements, US public health policy, AI’s role in healthcare, the economic and geopolitical climate, security, and the riveting women’s health series that started this year. For a look at our on-the-ground view of the conference, see our Day #1, Day #2, and Day #3 coverage. We’ll be back with more on private companies and nonprofit organizations, some of which also had very valuable discussions.

Table of Contents

-

Themes

- 1. Refined focus and priorities to advance promising candidates for diabetes, obesity, and liver health

- 2. Spotlight on upcoming clinical and regulatory approvals in 2025, with great interest in weight loss management

- 3. Commitment to improving AID algorithms and sensing capabilities to improve outcomes and reduce user burden

- 4. Artificial intelligence: From startups to regulators to national security

- 5. The potential evolution of the US public health policy under the Trump administration

- 6. A time of transition: Tumultuous geopolitical environment generates economic uncertainty

- 7. Women’s Health Series breaks new ground

- 8. Increased security presence following death of UnitedHealthcare CEO

-

Diabetes Therapy Highlights

- 1. Akero Health: Dr. Andrew Cheng highlights updates on MASH candidate, EFX; phase 2b data expected in February 2025, and phase 3 data in 1H26

- 2. Amgen: T2D and obesity candidate MariTide takes center stage, phase 2 readouts and phase 3 initiation in 2025; primary prevention trials for PCSK-9 inhibitor Repatha and olpasiran for Lp(a)

- 3. Amphastar: Increased projected 2025 sales of Baqsimi by $25 million, following promotional agreement with MannKind; GDUFA date for generic injectable GLP-1 RA set for 2Q25

- 4. AstraZeneca: Obesity program to drive growth beyond 2030; continued commitment to the development of small molecules

- 5. Bayer: Eylea HD as standard treatment for retinal disease; strong momentum of Kerendia (finerenone) in heart failure, with new prespecified analysis

- 6. Biomea: Refined pipeline focus on diabetes and obesity with icovamenib, a first-in-class menin inhibitor

- 7. Daiichi Sankyo: Nothing new from Dr. Sunao Manabe on pain

- 8. Ionis: Preparing for the launch of Tryngolza (olezarsen) as the first FDA-approved treatment for familial chylomicronemia syndrome

- 9. J&J: CEO Mr. Joaquin Duato discusses elements for success with a diversified portfolio, increasing attention for MedTech and Innovative Medicine

- 10. Lilly: Continued momentum with Mounjaro and Zepbound, advancing incretin treatments for diabetes, obesity, and beyond; upcoming “big assets” include oral GLP-1 orforglipron and “triple G” retatrutide

- 11. Madrigal: “Foundational MASH treatment” Rezdiffra sales total $180 million in the first nine months, with over 11,800 patients treated

- 12. Merck: Diversifying portfolio in diabetic macular edema; upcoming key readouts with PCSK9 and GLP-1 RA

- 13. Novartis: Innovation across four therapeutic areas, with significant progression of Entresto and Leqvio for heart failure and CVD

- 14. OPKO Health: Dr. Elias Zerhouni highlights the promising potential of dual GLP-1/glucagon RA in development for oral and injectable formulations

- 15. Pfizer: Dr. Albert Bourla expects phase 3 trial of once-daily oral GLP-1 in 2H25; confidence in capturing oral GLP-1 RA market

- 16. Regeneron: Dr. Leonard Schleifer highlights strategies to increase Eylea HD uptake; phase 2 data of trevogrumab (anti-myostatin antibody) with semaglutide expected in 2H25

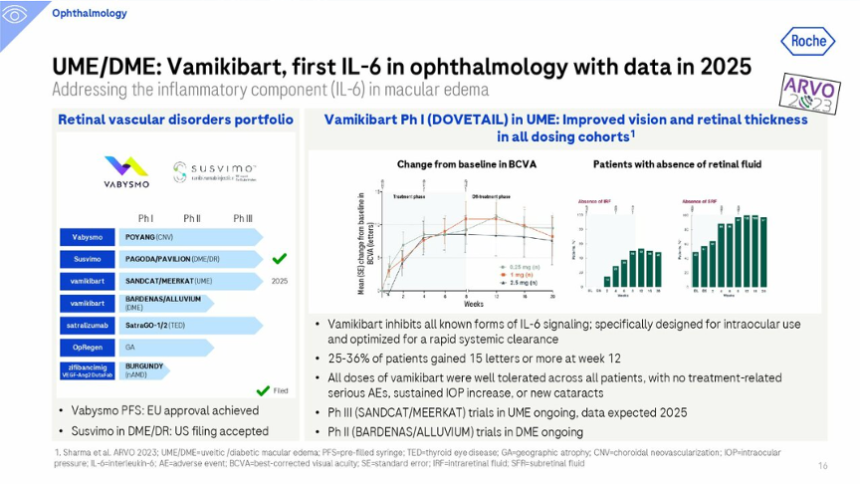

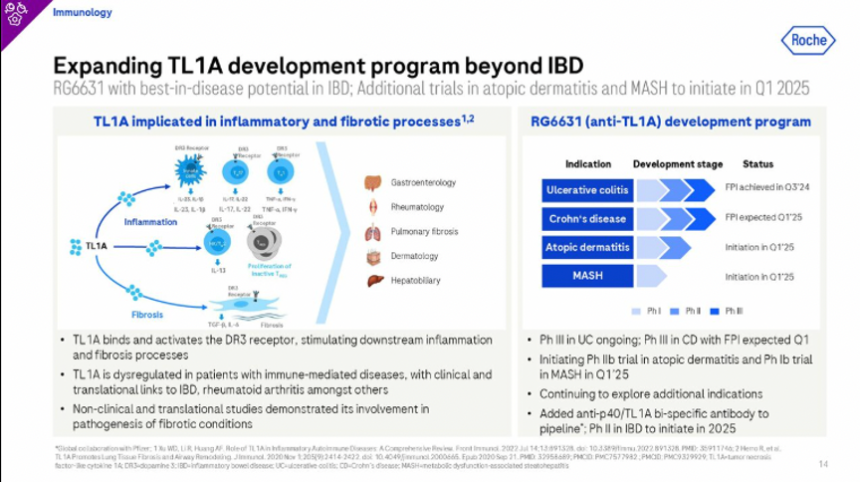

- 16. Roche: Continued clinical progress in ophthalmology and cardiovascular-renal-metabolic portfolio; phase 1b trial of anti-TL1A therapy in MASH to initiate in 1Q25

- 17. Sanofi: Strides to become the world leader for immunology; regulatory decision of Tzield in China expected in 2H25

- 18. Terns Pharmaceuticals: High confidence in oral GLP-1 RA TERN-601, compared to competitors; phase 2 data expected in 2H25

- 19. Vertex: Suzetrigine to launch for acute pain following PDUFA date in January 2025; T1D phase 3 trial of VX-880 (now named zimislecel) to complete enrollment and initial dosing in 2025

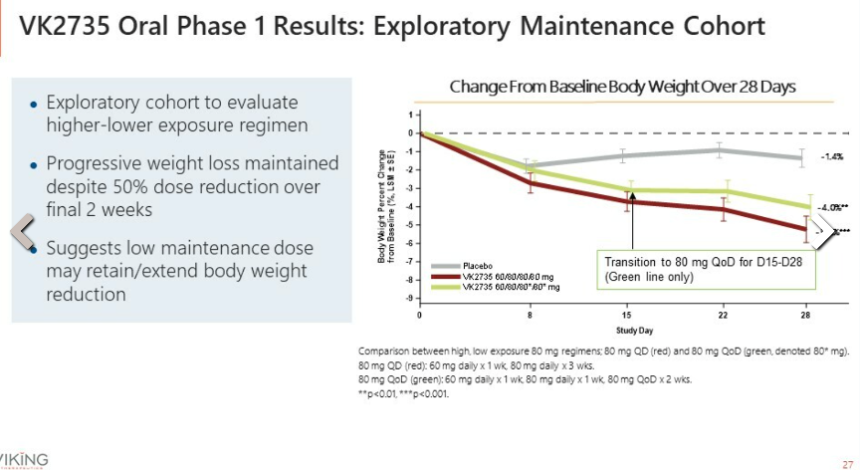

- 20. Viking: first appearance at JPM highlights VK2735 (dual GLP-1/GIP RA) advancing to phase 3 obesity trials in 1H25, following end-of-phase 2 FDA meeting

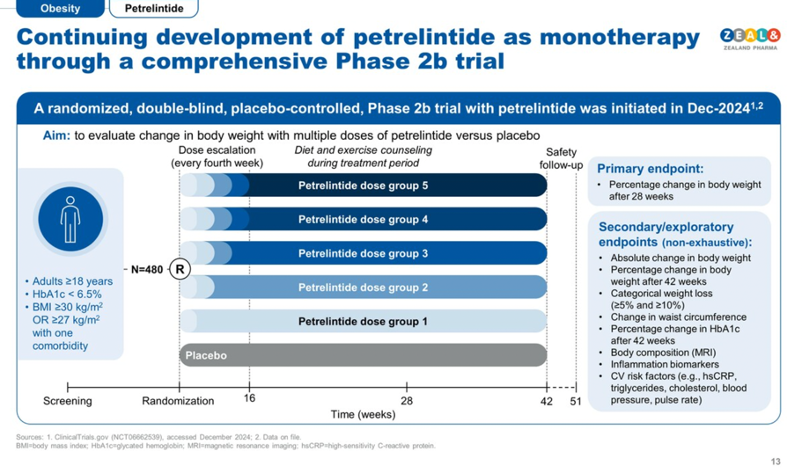

- 21. Zealand: CEO Dr. Adam Steensberg highlights “strongest pipeline in obesity” with differentiated approach with amylin analog

-

Diabetes Technology Highlights

- 1. Dexcom: Preliminary full-year 2024 revenue of $4.03 billion (+11%) and 4Q24 revenue of $1.11 billion (+8%); global userbase grows 25% to 2.8-2.9 million; developmental multi-analyte sensors confirmed

- 2. embecta: Gaining financial stability, international GLP-1 opportunities, and revitalization

- 3. Insulet: Omnipod 5 launched in five additional European countries, with an additional five launches to follow this year; significant growth opportunity in highly underpenetrated T2D population

- 4. Medtronic: Focus on expanding MiniMed 780G indications for T2D, biosimilars, preschoolers, and pregnancy; goal to introduce Simplera in US by end of 2025

- 5. Teladoc: Collaboration with Amazon’s Health Benefits Connector to increase access to virtual cardiometabolic programs announced

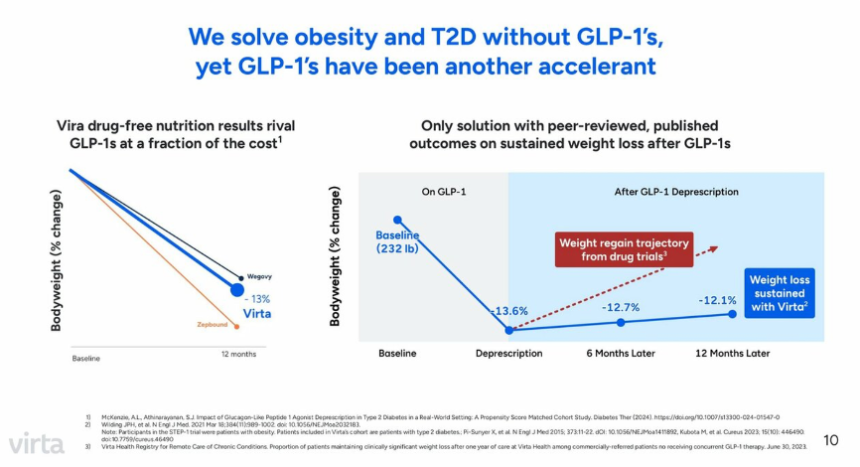

- 6. Virta Health: GLP-1 RAs positioned as non-essential for metabolic success but still beneficial; over $100 million in revenue by end of 2024

-

Diabetes Big Picture Highlights

- 1. JPMorgan Chase CEO Mr. Jamie Dimon talks China, GLP-1 RAs, AI, the Trump administration, healthcare frustrations, and more in noontime conversation

- 2. The early innings of AI in healthcare: Panel discussion emphasizes the need for data cleaning and transparency to guide AI’s implementation

- 3. Inside the FDA: Panel discussion offers insight into approval processes, serving as an opportunity for connection between developers and regulators

- 5. Retired General Mark Milley tackles geopolitics and the military’s role in health innovation

- 9. ARPA-H: Catalyzing biomedical breakthroughs in women’s health through the Sprint for Women’s Health, NITRO, and POSEIDON

- 10. The US healthcare landscape: Former FDA Commissioner Dr. Scott Gottlieb speculates on the potential impact of Trump administration on biomedical innovation and public health

- 11. Fireside chat with HHS Secretary Xavier Becerra: Analyzing the Biden administration’s accomplishments, including MDPNP, ACA, and vaccines

- 12. AI in diagnostic testing: Panel demonstrates opportunities for innovation and equity, while calling for regulation and caution

- 13. Investment opportunities to drive innovation in emerging markets

Themes

1. Refined focus and priorities to advance promising candidates for diabetes, obesity, and liver health

Several companies outlined their refined focus and priorities to build a stronger pipeline for improving patient outcomes for diabetes, obesity, and liver health. Reflecting on all the positive results and approvals across the field, countless presentations spotlighted the strong momentum and high expectations for 2025. We particularly appreciated hearing updates on companies dedicating resources and improving their pipeline to advance impactful opportunities to the next stages of development.

- In one of the most packed sessions of the conference, Lilly’s CEO Mr. David Ricks highlighted significant milestones across 2024, with Mounjaro (tirzepatide for diabetes) and Zepbound (tirzepatide for obesity) showing strong growth in the guidance published Tuesday. While the guidance indicated lower-than-expected revenue, Lilly expects 2024 full-year worldwide revenue to be approximately $45 billion (+32%). In 4Q24, revenue for Mounjaro reached approximately $3.5 billion and $1.9 billion for Zepbound, compared to $3.1 billion in 3Q24 and $2.2 billion in 4Q23 for Mounjaro and compared to $1.2 billion in 3Q24 and $175 million in 4Q23 for Zepbound. To meet increasing demand, Lilly plans to bring additional manufacturing capacity and expects to produce at least 60% more scalable doses of incretins in 1H25 compared to 1H24. Especially with the FDA announcing the shortage resolution of tirzepatide in December 2024, we’re encouraged to see Lilly focus on continuing its robust growth.

- With Rezdiffra (resmetirom), the first and only FDA-approved treatment for MASH, CEO Mr. Bill Sibold highlighted Madrigal’s strong leadership and significant potential for continued success. According to Madrigal’s preliminary financials published on Monday, Rezdiffra revenue totaled $100-103 million in 4Q24 and $166-180 million in 2024, remarkable growth for only three quarters on the market. Furthermore, Mr. Sibold said that more than 11,800 patients are on Rezdiffra, also reflecting significant growth from over 6,800 patients in 3Q24 and just ~2,000 in 2Q24. Mr. Sibold also emphasized that Rezdiffra will be a foundational treatment for MASH, continuing to target 315,000 people diagnosed with F2 and F3. Madrigal plans to continue a strong launch of Rezdiffra in the US and awaits approval in the EU in 2025, planning for commercial launch in Germany and potentially expanding to other countries. Mr. Sibold also highlighted plans to build a pipeline to secure long-term growth, perhaps exploring the next best mechanism of action or combination treatments that enhance Rezdiffra’s efficacy.

- Refining the pipeline to increase focus on cardiometabolic health, Biomea CEO Mr. Thomas Butler reiterated the announcement on Monday that the company will become a diabetes and obesity treatment company based on promising results of recent clinical trials. Biomea plans to conclude its studies exploring icovamenib (potent and selective covalent menin inhibitor) in oncology and explore partnerships to further advance its oncology assets. Most recently, in December 2024, Biomea announced positive topline results of the phase 2 COVALENT-111 study of icovamenib in T2D. Biomea continues to advance icovamenib, aiming to address challenges with current standards of care with high discontinuation rates of GLP-1 RAs, SGLT-2 inhibitors, and DPP-4 inhibitors. In particular, icovamenib targets two specific populations: (i) people with severely-insulin deficient diabetes; and (ii) people on GLP-1 RA treatment.

2. Spotlight on upcoming clinical and regulatory approvals in 2025, with great interest in weight loss management

Companies celebrated achievements on pipelines from last year and discussed upcoming milestones for the new year. We were encouraged to see several regulatory approvals in 2024, including Madrigal’s Rezdiffra (resmetirom) for MASH in March 2024, Lilly’s Zepbound (tirzepatide) for obstructive sleep apnea in December 2024, and Bayer’s Eylea HD (aflibercept 8mg) and Roche’s Vabysmo (faricimab) prefilled syringes for eye diseases. Companies highlighted early performances of these products and strategies to capture a greater patient base by securing more formulary access, educating physicians, and establishing a strong supply chain.

- We were also excited about the upcoming trial readouts and regulatory milestones expected in 2025. We highlight several pipeline updates below:

- In T1D therapy and cures, Vertex plans to share phase 1/2 (n=17) results for VX-264, a cell-encapsulated device of stem cell-derived islets, in 2025. Sanofi expects a regulatory decision for Tzield (teplizumab) in China in 2H25.

- On weight loss management, Amgen plans to initiate its phase 3 program MARTIME between 1H25 and 2H24. Additional data from the ongoing phase 2 trial (expected to complete in early 2026) will be read out in 2H25, as well as phase 2 results in T2D. Zealand will launch a phase 2b ZUPREME-2 trial for petrelintide (amylin analog) for overweight or obesity in 1H25, and a phase 1b combination trial with petrelintide and GLP-1 RA in 2025. Regeneron’s phase 2 study of trevogrumab (anti-myostatin) and semaglutide combination therapy to minimize muscle loss during obesity treatment is expected in 2H25. AstraZeneca also expects a phase 2 data readout this year for an obesity program, although the candidate was not specified during the meeting. Terns Pharmaceutical’s phase 2 data of once-daily GLP-1 RA TERN-601 is expected in 2H25. Lastly, Amphastar’s generic injectable GLP-1 RA, AMP-018, awaits the FDA’s decision by the GDUFA date in 2Q25.

- In ophthalmology and liver health, Regeneron plans to launch pre-filled syringes of Eylea HD by mid-2025 in the US. Akero Health expects to share phase 2b data for efruxifermin (EFX) in February 2025 for MASH.

- For cardiovascular health, Amgen’s phase 3 VESALIUS-CV trial (n=12,301), investigating Repatha in adults at high cardiovascular risk and without prior myocardial infarction or stroke, is expected to complete in July 2025, and its data readout is expected in 2H25. Novartis’ data for the Lp(a)-HORIZON trial (n=8,323) assessing pelacarsen in major cardiovascular events in people with CVD is expected in May 2025.

- Companies expressed commitment to engage in lively discussions with the FDA to design trials, especially given the FDA’s draft guidance on developing weight-loss therapies and increasing diversity. For example, Viking CEO Dr. Brian Lian shared during Q&A that Viking had an end-of-phase 2 meeting with the FDA before these draft recommendations were published and knew where the agency stood on these topics. Additionally, a panel discussion by representatives from the FDA was fully dedicated to elucidating the agency’s approval processes and the Total Product Life Cycle (TPLC) Advisory Program (TAP) Pilot, which aims to streamline approval and increase communication between developers and regulators. The panel highlighted the differences in approval processes between medical devices and pharmaceuticals, the importance of building trust and relationships with the FDA.

3. Commitment to improving AID algorithms and sensing capabilities to improve outcomes and reduce user burden

Like therapy, innovation in diabetes technology continues at breakneck pace. Presentations from CGM and AID manufacturers underscored the industry’s commitment to developing more advanced algorithms, multi-analyte sensor probes, and smaller form factors to reduce user burden and further improve glycemic outcomes. Alongside this rapid innovation, the industry remains focused on expanding insurance coverage for diabetes technology, particularly in the T2D population, which has historically underused these devices.

- In CGM, Dexcom successfully submitted a 15-day Dexcom G7 to the FDA in 3Q24, which is expected to launch in 2H25. The company also has planned several software enhancements this year, including in the Dexcom Follow app. Development of the next-generation Dexcom G8 is also advancing with some individuals now wearing the sensor, which features more advanced electronics to accommodate multi-analyte sensors. CEO Mr. Kevin Sayer added that Dexcom is advancing several probes with extended lifespans – some of which can measure “two or three [analytes]” simultaneously.

- In AID, Medtronic’s CEO Mr. Geoff Martha briefly commented on the company’s next-generation AID pipeline, including a reveal of a potential form factor for an 800-Series pump and a patch pump. While details are scarce on these pumps, the company first unveiled the 800-Series pump at its Investor Day at ADA 2023 – a screenless, tethered pump that is roughly half the size of the 700-Series pump and will be fully controlled from a user’s smartphone. Insulet’s CEO Dr. Jim Hollingshead highlighted in his remarks that the company continues to advance development of next-generation AID algorithms, including SmartAdjust 2.0 and the fully closed-loop EVOLUTION algorithm.

- Beyond innovation, the technology industry continues to progress efforts to improve access to these life-changing technologies, particularly for T2D. Dexcom is committed to obtaining complete reimbursement for CGM for people with T2D on non-insulin therapy, which represents over 25 million people in the US alone. As of this month, Mr. Sayer announced that two of the three largest PBMs cover Dexcom CGM for anyone with diabetes, which will enable commercial coverage for over five million people with T2D on non-insulin therapy by the end of 2025. Several companies are expanding their sales forces to better reach the T2D population, including Dexcom and Insulet (after Omnipod 5’s FDA clearance for T2D in August 2024). Beyond T2D, Insulet remains focused on growing technology adoption among people with T1D, as the company will introduce Omnipod 5 into 10 international markets in 2025, with five launches already announced this week – Denmark, Finland, Italy, Norway, and Sweden. Launches in Australia, Belgium, Canada, Israel, and Switzerland are expected to follow later this year.

4. Artificial intelligence: From startups to regulators to national security

JPM 2025 highlighted AI’s impact on healthcare in multiple arenas, featuring multiple AI-focused panels with significant discussion across industry updates and broad-ranging keynotes. In his opening keynote, JPMorgan CEO Mr. Jamie Dimon reiterated the power of AI to accelerate significant breakthroughs in medicine, such as curing cancer and identifying disease-causing gene defects. He envisions AI eliminating a large portion of human medical error, citing a 2003 study showing 30,000 hospital deaths per year due to human error. AI seemed to weigh on the minds of presenters, as if speakers knew they must be at the forefront of AI innovation.

- JPM 2025 featured several riveting panels on the potential of AI to improve healthcare. A panel featuring Dr. Shiv Rao (CEO, Abridge), Mr. Hamid Tabatabaie (CEO, CodaMetrix), Ms. Seema Verma (EVP and General Manager, Oracle Health and Life Sciences), and Mr. Omri Yoffe (CEO, Vi) unanimously agreed that AI’s implementation in healthcare remains in its “early innings,” proposing several key considerations to guide ethical and effective use to support clinical decision making. In particular, they called for data cleaning and transparency to guide AI’s implementation in clinical settings. On Day #3, a separate panel analyzed AI’s role in diagnostic testing. Panelists deemed AI to be transformative, envisioning huge potential for rural medicine to connect more communities to academic medical centers. Despite the potential of AI, Mr. Troy Tazbaz (Director of Digital Health Center for Excellence, FDA) acknowledged the need for regulation and post-market monitoring at all hospitals, in a push for equity. Mr. Dimon similarly noted the need for regulation, likening AI to other dependable technologies, such as planes, cars, and pharmaceutical innovations, that can be abused but are safe and essential with proper government regulation.

- Several pharmaceutical and biotechnology companies stated their intentions to leverage AI to assist with R&D and improve user experiences. Pfizer’s CEO Dr. Albert Bourla discussed how the company can improve R&D productivity and operational efficiency through AI, while Dexcom’s CEO Mr. Kevin Sayer highlighted the company’s launch of a generative AI to provide more personalized insights in the Stelo app through its use. Virta Health’s CEO Mr. Sami Inkinen also described how its digital cardiometabolic platform leverages AI and drives users to achieve their weight loss goals.

5. The potential evolution of the US public health policy under the Trump administration

JPM 2025 featured significant discussion on potential reform to US public health landscape under the incoming Trump administration. Panelists acknowledged the possibility for significant changes to US healthcare policy, including health insurance, PBMs, vaccinations, and more. Despite potential changes to healthcare policy in the coming years, panelists appeared optimistic that the pace of innovation in the healthcare industry would continue to accelerate. Specifically, former FDA Commissioner Dr. Scott Gottlieb said that the field has reached an “inflection point” where regenerative medicine seems inevitable. Several FDA representatives did not foresee significant impact on regulatory approval processes. Dr. Laura Gottschalk suggested the presidency and the Administrator of the CMS have limited influence, and she noted that the agency possesses staff that served under both the prior Trump and Biden administrations.

- Potential coverage changes for medical care and treatment were top of mind. Outgoing Secretary of the US Department of Health and Human Services (HHS) Xavier Becerra highlighted progress in the Biden administration to further expand health insurance coverage for millions of Americans, noting that over 300 million people now have health insurance. For instance, Sec. Becerra said that women on Medicaid can receive postpartum care for 365 days after birth, up from 60 days previously, to address the high rates of maternal morbidity and mortality. However, throughout the conference, stakeholders expressed concern regarding the incoming Trump administration’s intentions to reform healthcare policy. Several sessions discussed the feasibility of reform in several areas:

- Affordable Care Act (ACA): Addressing the incoming Trump administration’s threats to weaken or repeal the ACA, Sec. Becerra suggested this legislation cannot be undone easily due to the millions of Americans who depend on the ACA for health insurance. He said a record number of individuals, nearly 24 million, are receiving their health insurance through this legislation; therefore, if the ACA is targeted for reform, he expects substantial public opposition that would forestall significant repeals or adjustments to ACA coverage.

- Drug pricing: Due to the establishment of the Medicare Drug Price Negotiation Program (MDPNP) through the Inflation Reduction Act (IRA), drug pricing reform was of high interest throughout the conference. Dr. Gottlieb does expect Medicare reimbursement for GLP-1 RAs in obesity to be withdrawn because most of the elderly population will become eligible for these therapies as their indications further expand, stating CMS “saw the writing was on the wall” when proposing this policy. Beyond GLP-1 RAs, Dr. Gottlieb suggested the IRA could be reformed to remove orphan drug exemptions. He was skeptical that small molecule exemptions would be adjusted to establish equivalent price negotiation exemption for small molecules and biologics (i.e., increase small molecules nine-year exemption window to 13 years to match biologics’ exemption window) since the government will primarily seek to save money.

- Pharmacy benefit managers (PBMs): With a PBM Reform Act introduced in Congress, potential regulation of PBM was a focus. Dr. Gottlieb suggested this legislation could be incorporated into the reconciliation bill; however, he expressed concern it could but impede more productive long-term reform by antagonizing PBMs and increasing their resistance to further action.

- Interest in potential regulation of the food industry to encourage healthier product production and consumption was high. Dr. Gottlieb said the FDA strongly supports these efforts, proposing several changes to regulation on food, including: (i) more forceful disclosures on unhealthy food attributes; or (ii) permitting food manufacturers to make broader claims on healthy attributes and therefore directly compete on product healthiness.

- Given previous criticism of vaccines by individuals nominated to critical public health positions in the incoming administration, several sessions probed possible changes to vaccination policy. Sec. Becerra emphasized that the HHS operates on “science, not intuition or politics,” stating that the evidence supports the success of vaccines. Dr. Gottlieb also expressed concern that efforts to soften childhood vaccination requirements, for example in schools, could lead to significant decreases in vaccination rates, although he believes that President-elect Trump understood the importance of childhood vaccination in his briefings with him.

6. A time of transition: Tumultuous geopolitical environment generates economic uncertainty

Like JPM 2024, several keynote addresses acknowledged a challenging and tense geopolitical environment and speculated on the potential influence of the incoming Trump administration. Panelists expressed subtle concern over the long-term health of the economy in the current geopolitical climate, emphasizing this period as a time of transition globally with likely ramifications for the healthcare industry. In his keynote address, Mr. Jamie Dimon projected limited change at the inauguration of the new Trump administration, arguing that the US president does not affect the economy in the first year of their administration. However, he shared his worries about the economic future beyond 2025.

- Mr. Dimon and retired Gen. Mark Milley likened the current geopolitical climate to the state of the world before World War II. Gen. Milley pointed to the rise of nationalism, protectionism, populism, and tariffs as factors that may potentially disrupt peace. He advocated for diplomacy and for the US to negotiate with “adversaries” such as China. Mr. Dimon similarly urged US leaders to steadfastly prepare to address any unexpected geopolitical and economic crises.

- Given the evolving economic climate, cost considerations for GLP-1 RAs were a hot topic of discussion after the Biden administration proposed expanded Medicare and Medicaid coverage of anti-obesity medications in November 2024. When asked about the balance between GLP-1 RAs’ effectiveness and the costs of long-term use, Mr. Dimon strongly expressed his belief that use of GLP-1 RAs would present less of a cost over time than the consequences of diabetes and heart disease, urging the industry to move towards disease prevention when possible. (Of note, JPMorgan Chase covers employee costs of the drugs for both obesity and diabetes.)

7. Women’s Health Series breaks new ground

In what’s a first at the conference, JPM 2025 featured what it called a Women’s Health Series – a collection of very interesting panel discussions with focus on women in healthcare. While improving women’s health outcomes and catalyzing new innovations for diseases that predominately affect women are certainly major goals, part of the aim also appeared to be gathering women leaders together. Attendees were encouraged to wear pink in solidarity on the second day of the conference in recognition of this focus and it was striking to see upwards of 400 women in pink standing together in the middle of Union Square. Men who wore pink won praise from the women we heard speaking! In addition to ARPA-H, conversations centered on leadership in biopharma, the future of women’s healthcare, and the flow of capital to women’s health.

- ARPA-H: ARPA-H, a federal agency formed in 2022 that aims to achieve transformative, sustainable, and equitable health solutions, hosted an afternoon panel discussion devoted to discussing the agency’s efforts to catalyze biomedical breakthroughs to support women’s health. In 2024, ARPA-H initiated the Sprint for Women’s Health to fund and accelerate development of biomedical therapies and technologies to improve women’s health outcomes, providing $113 million in funding across 24 awards to support novel solutions for unmet needs in women’s health. As one example, this initiative provided $10 million in funding to support Daré Bioscience’s development of a novel treatment to clear persistent high-risk human papillomavirus (hrHPV) infection, which causes cervical cancer. Dr. Ross Uhrich (Program Manager, ARPA-H) also highlighted the efforts of the NITRO and POSEIDON initiatives to develop breakthrough therapies for osteoarthritis, which predominately affects women, and cancer screenings, respectively.

8. Increased security presence following death of UnitedHealthcare CEO

JPM 2025 was marked by a noticeably increased security presence compared to last year’s conference, stemming from the murder of UnitedHealthcare CEO Mr. Brian Thompson in December 2024. See Mr. James S. Hirsch’s reflections on the death as well as his musings on the US healthcare industry in the wake of this event. Significantly more San Francisco police officers were stationed both outside and inside venue than JPM 2024, fence barricades were erected around the perimeter of the entrance, and security personnel occasionally reminded exiting attendees to remove their name badges outside the venue. This heightened security seemed to reflect the uneasiness of many executives and attendees amidst contentious public sentiment on the healthcare industry ignited by the death of Mr. Thompson, which was underscored by peaceful demonstrations in Union Square on the opening day. We extend our gratitude to the police officers and security personnel for their efforts to secure the event and ensure smooth operations.

Diabetes Therapy Highlights

1. Akero Health: Dr. Andrew Cheng highlights updates on MASH candidate, EFX; phase 2b data expected in February 2025, and phase 3 data in 1H26

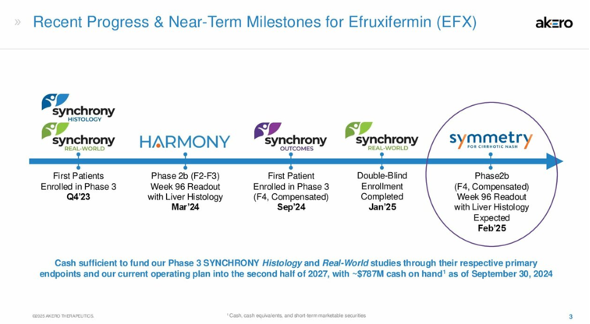

President and CEO Dr. Andrew Cheng provided promising updates on Akero Health’s lead MASH candidate, efruxifermin (EFX). See webcast here. As background, EFX is a bivalent fibroblast growth factor 21 (FGF21) analog that can regulate multiple metabolic pathways and cellular processes. With once-weekly dosing, EFX has the potential to treat MASH with or without cirrhosis. Celebrating Akero Health’s transition to phase 3 trials, Dr. Cheng highlighted advances in clinical trials and shared post-hoc analyses of phase 2 data. We’re excited to see Akero Health’s progress in MASH amid the evolving competitive landscape.

- In February 2025, Akero Health will share 96-week data of the phase 2b SYMMETRY study of EFX in patients with compensated cirrhosis (F4) from MASH. This is an exciting news, given limited treatment aside from liver transplantation for people with cirrhosis – this population has a significantly higher five-year mortality rate (~50%) than those without (less than 15%).

- As background, the primary readout of 36-week data was shared in October 2023, in which EFX demonstrated up to 10% placebo-corrected improvement in fibrosis without worsening of MASH. While these results did not meet statistical significance (n=0.279), Dr. Cheng noted that these were the best results seen yet in this clinically vulnerable population. EFX demonstrated the highest placebo-corrected improvement compared to competitors such as Novo Nordisk’s semaglutide (18%) and Gilead’s selonsertib (1%). Furthermore, one 69-year-old female participant recovered from F4 to F1 after nine months of treatment, in addition to a weight loss of ~2 kg (4 lbs), suggesting an antifibrotic activity of EFX.

- Dr. Cheng also highlighted results of the phase 2b HARMONY trial (n=128) announced in March 2024. The study demonstrated statistically significant fibrosis improvement of 75% in the EFX arm, compared to 24% on placebo in people with MASH but not cirrhosis at Week 96. Comparison to 24-week data, which demonstrated 41% improvement in fibrosis, suggests that longer dosing improves response. As well, 63% of initial non-responders responded to EFX.

- Finally, the phase 3 SYNCHRONY Real-World study (n=601), which evaluates safety and tolerability of EFX in patients with non-invasively diagnosed MASH or MASLD, completed patient enrollment in January 2024, and data is expected in 1H26. The other two trials of the SYNCHRONY program focus on efficacy. SYNCHRONY Histology evaluates the efficacy and safety of EFX in patients with biopsy-confirmed pre-cirrhotic MASH, with data including liver biopsy expected in 2027. The 260-week SYNCRONY Outcomes trial evaluates EFX on the time to first occurrence clinical events, in addition to histologic fibrosis improvement, in patients with non-invasively diagnosed MASH.

2. Amgen: T2D and obesity candidate MariTide takes center stage, phase 2 readouts and phase 3 initiation in 2025; primary prevention trials for PCSK-9 inhibitor Repatha and olpasiran for Lp(a)

Amgen’s CEO Mr. Bob Bradway highlighted upcoming pipeline milestones for the company in 2025, with particular emphasis on GIP antagonist/GLP-1 RA MariTide. Mr. Bradway began his presentation recognizing the devastation caused by the wildfires in Southern California, where Amgen is based, and said that the company is committed to rebuilding the community, starting with $10 million in support announced the day of his talk. We have been excited to see Amgen’s relatively large focus on obesity and obesity-related conditions, which falls under its “General Medicine” area – the other three areas are rare diseases, oncology, and inflammation. MariTide, PCKS9 inhibitor Repatha, and Lp(a)-lowering olpasiran were the main areas of focus of Mr. Bradway’s prepared remarks on the cardiometabolic treatment front. While Amgen is also developing half a dozen preclinical and early stage obesity candidates, including phase 1 AMG 513, Mr. Bradway did not discuss any specifics beyond sharing that the company is still in its early days on this front and that decisions on which molecules Amgen will promote will depend on the data.

- “We’ll be the first long-acting therapy in the treatment of obesity.” In response to JPM’s Mr. Chris Schott’s question about MariTide’s potential commercial hurdles and capabilities as the “third entrants into the market,” Mr. Bradway said he would instead position MariTide as the first in long-acting therapy for obesity. MariTide’s monthly (or even less frequent) dosing schedule, which he characterized as potentially “very attractive” to patients, was a key point in Mr. Bradway’s prepared remarks. He also highlighted positive phase 2 results reported in November 2024. Recall that MariTide conferred ~20% weight loss in people with obesity or overweight and ~17% weight loss in T2D at 52 weeks. Notably, Mr. Bradway pointed out that weight loss had not yet plateaued at 52 weeks, adding that Amgen will continue to share incremental data this year. In participants with T2D, MariTide conferred a 2.2% A1c reduction. Mr. Bradway said that over half of these participants achieved an A1c below 5.7%, indicating T2D remission.

- In 2025, Amgen plans to initiate its phase 3 program MARTIME between 1H25 and 2H24. Additional data from the ongoing phase 2 trial (expected to complete in early 2026) will be readout in 2H25 as will phase 2 results in T2D specifically. Looking ahead, Mr. Bradway also championed Amgen’s capability to meet potential supply demands, which it has been able to demonstrate across its portfolio in the past.

- On PCSK-9 inhibitor Repatha, we were excited to hear Amgen’s interest in a potential primary prevention indication. During the Q&A, Mr. Bradway emphasized the importance of lowering LDL levels to prevent heart attacks and strokes and that “the sooner, the better.” We imagine that a primary prevention indication will depend on results from the phase 3 VESALIUS-CV trial (n=12,301), which is investigating Repatha in adults at high cardiovascular risk and without prior myocardial infarction or stroke. The trial is expected to complete in July 2025, and its data readout is expected in 2H25. On Repatha broadly, Mr. Bradway emphasized the large need (>100 million patients) for effective treatment for heart disease. He said that Repatha’s remarkable growth (up 40% in 3Q24 with an expected 2024 annualization of over $2 billion) has been driven by its “enormous efficacy,” the unmet need for treatment, and access.

- On Lp(a)-lowering olpasiran, we were again delighted to hear Amgen’s interest in primary prevention, with plans to initiate a phase 3 study in 2H25. Mr. Bradway highlighted that olpasiran would be a first-in-class siRNA molecule targeting Lp(a), which affects ~20% of the population and is nonmodifiable with diet or exercise. Phase 2 results demonstrated that olpasiran can reduce Lp(a) concentration by over 95% in people with ASCVD, and its phase 3 Ocean(a)-Outcomes trial (n= 7,297) is ongoing and fully enrolled.

- On biosimilars, as with last year, Mr. Bradway highlighted the company’s global leadership in the area, sharing that he is proud of the fact that Amgen has a 100% success rate with the FDA approvals for biosimilars. He also highlighted that the company has been able to “supply every patient, every time with a biosimilar molecular when they come asking for one.” While there was no mention of Eylea biosimilar Pavblu, the company’s slides noted that it was launched last year.

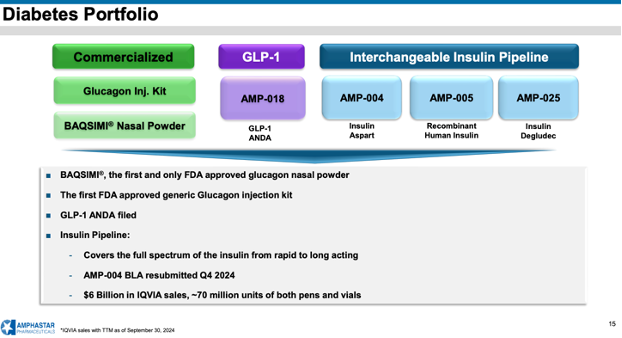

3. Amphastar: Increased projected 2025 sales of Baqsimi by $25 million, following promotional agreement with MannKind; GDUFA date for generic injectable GLP-1 RA set for 2Q25

CEO Dr. Jack Zhang and CFO Mr. Bill Peters shared Amphastar’s business strategies and pipeline updates, focusing on nasal glucagon Baqsimi, insulin analogs, and a generic GLP-1 RA candidate (see webcast and presentation slides). Dr. Zhang introduced Amphastar’s dual growth strategy, which involves both internal pipeline development as well as strategic acquisitions of product facilities. As background, the company developed the first and only FDA-approved generic traditional glucagon injection kit in 2020 and acquired Baqsimi from Lilly in June 2023. Amphastar has seen significant growth over the past several years, with revenue totaling $191 million in 3Q24, up 5% from 3Q23. Looking forward, Amphastar plans to shift its pipeline from predominantly generic products (comprising 63% of the pipeline in 2021) to proprietary and biosimilar products (50% and 35%, respectively, by 2026). Alongside this shift, Amphastar will continue investing significantly (~21% of revenue) to R&D and diversifying products and revenue base. See the company’s diabetes portfolio below.

- Baqsimi (nasal glucagon) continues to be Amphastar’s biggest branded product with growing sales, following its spin-out from Lilly in June 2023. As the only FDA-approved non-injectable glucagon, Baqsimi offers a user-friendly, ready-to-use solution for treating severe hypoglycemia, especially for caregivers, friends, and school staff who may be unfamiliar with injectable products during emergencies. Despite ADA recommendations, however, Mr. Peters noted that only 10% of people on insulin use glucagon, indicating a significant opportunity for much greater market expansion. To raise greater awareness, Amphastar has signed a promotional agreement with MannKind, a manufacturer of inhaled insulin Afrezza, in 3Q24. Amphastar has raised the peak sales projection for Baqsimi to $250-275 million, up from $225-250 million, to reflect the partnership with MannKind that would double the salesforce. The company also announced a 3% increase in the unit price this year – while no price increase would be better for patients and the system, we understand the price increase is important to offset price increases in raw materials and other increased expenses. Excitingly, Mr. Peters also shared that Baqsimi has expanded its international footprint.

- Amphastar awaits the FDA’s decision on the generic injectable GLP-1 RA, AMP-018, as the GDUFA (generic drug user fee amendments) is set for 2Q25. If approved, Amphastar expects AMP-018 to have revenue potential of ~$1.1 billion, according to IQVIA. That said, during Q&A, Dr. Zhang acknowledged that the company will face significant competition in the GLP-1 RA landscape.

- Amphastar’s interchangeable insulin pipeline aims to cover the full spectrum of insulin, including insulin aspart AMP-004 (Novolog), recombinant human insulin AMP-005, and insulin degludec AMP-025 (Tresiba). Mr. Peters updated that Amphastar resubmitted the Biologics License Application (BLA) for AMP-004 in 4Q24, following multiple FDA meetings to confirm submission requirements. He added that AMP-005 is manufactured at the company’s facility in France, while the API production for AMP-025 is based in China, reflecting on the company’s global manufacturing capabilities.

4. AstraZeneca: Obesity program to drive growth beyond 2030; continued commitment to the development of small molecules

CFO Ms. Aradhana Sarin delivered a comprehensive overview of AstraZeneca’s financial growth and late-stage pipeline, spanning oncology, biopharmaceuticals, and rare diseases (see webcast and presentation slides). AstraZeneca saw robust growth in 2024, totaling $39 billion for nine months (up 19% from 2023) and marking double-digit growth across all therapeutic areas and in the US, Europe, and emerging markets by geography. Of note, cardiovascular, renal, and metabolism (CVRM) sales totaled $9.4 billion for nine months of 2024, contributing 24% of total sales. Ms. Sarin boasted AstraZeneca’s broad pipeline, including 91 ongoing late-stage trials, each with peak year revenue greater than $1 billion. Continuing this momentum, AstraZeneca aims to deliver $80 billion in total revenue and launch at least 20 new molecular entities by 2030. The company is also preparing for growth beyond 2030 by investing in areas such as weight management, antibody conjugates, and cell therapy. During Q&A, however, Ms. Sarin added that AstraZeneca expects to face a headwind from Farxiga value-based purchasing 11 VBP 11).

- AstraZeneca made significant progress on obesity programs, including: (i) AZD5004 (oral GLP-1 RA); (ii) AZD6234 (long-acting amylin); and (iii) AZD9550 (GLP-1/glucagon RA). These candidates are expected to drive growth beyond 2030. As we heard from ObesityWeek®, these obesity candidates have moved into phase 2 trials, following positive phase 1 results. While Ms. Sarin did not clarify the candidate, there will be a phase 2 data readout for the obesity program in 2025. Based on the following completion dates (listed in 3Q24), we anticipate select trials of the following will have data readout this year: (i) VISTA trial (n=304) for AZD5004 in obesity/overweight, plus one comorbidity (expected to complete in December 2025); or (ii) CONTEMPO trial (n=88) for safety of AZD9550 in obesity/overweight with or without T2D (expected to complete in April 2025).

- Baxdrostat (aldosterone synthase inhibitor) is among the seven candidates that will have first phase 3 results in 2025. Approximately 45 million people in the US, Japan, and Europe have difficulty treating hypertension, despite standards of care. In phase 2b BrigHTN trial (n=275), baxdrostat conferred a 20% reduction in systolic blood pressure (SBP) at Week 12, compared to a 9% reduction with placebo. Phase 3 BaxHTN trial (n=720), investigating the drug’s effect on SBP at Week 12, has completed enrollment in 4Q24 and is expected to complete in 2H25. Data from the phase 3 Bax24 trial (n=212), investigating baxdrostat on ambulatory blood pressure is expected in 2H25. Ms. Sarin also briefly discussed that BaxDuo-Arctic trial (n=2500) assesses combination therapy of baxdrostat and SGLT-2 inhibitor Farxiga (dapagliflozin) and is expected to complete in December 2027.

- When asked about what modalities AstraZeneca will focus on, given the US Inflation Reduction Act 2022,[1] Ms. Sarin expressed continued commitment toward small molecules, which have the highest value and biggest opportunities, such as AZD5004 or oral PCSK9.

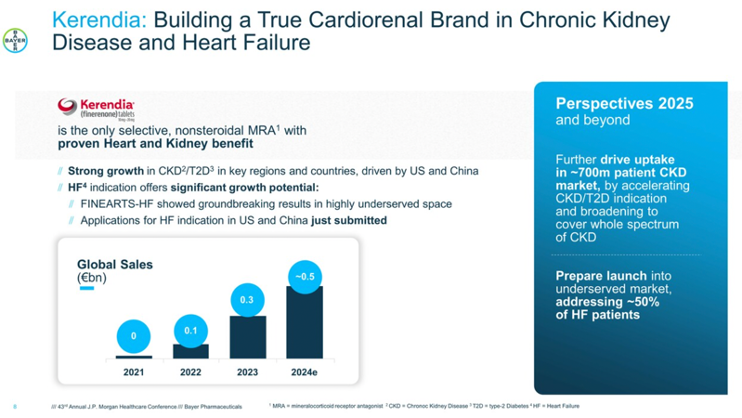

5. Bayer: Eylea HD as standard treatment for retinal disease; strong momentum of Kerendia (finerenone) in heart failure, with new prespecified analysis

In the afternoon, President Mr. Stefan Oelrich presented updates on Bayer’s promising therapies, including ones of high interest to us, Kerendia (finerenone) and Eylea (aflibercept).

- Eylea remains a leader in the retinal market and sustains its strong market position. Mr. Oelrich positioned Eylea as the number one anti-VEGF treatment since 2016 and called Eylea HD (aflibercept 8 mg) the new standard for retinal diseases. Last year, around the time of JPM 2024, Eylea HD received approval for neovascular age-related macular degeneration (nAMD) and diabetic macular edema (DME) in Europe and Japan. As a reminder, Bayer exclusively markets Eylea outside the US, while Regeneron is responsible for US sales. Regeneron received FDA approval for Eylea HD for nAMD, DME, and diabetic retinopathy (DR) in August 2023.

- As a differentiating factor among emerging competitors and biosimilars in the field, Mr. Oelrich emphasized that Eylea HD is the only drug approved for extended treatment intervals (up to five months) for nAMD and DME. During Q&A, Mr. Oelrich said that Eylea HD has received positive responses from HCPs, especially given larger dosing intervals, and therefore feels “bullish” about future progression. Additionally, he noted that Eylea HD pre-filled syringe (PFS) is now indicated and available for nAMD and DME, approved in September 2024. In the US, Regeneron shared in 3Q24 that it would launch the PFS by mid-2025.

- Non-steroidal MRA Kerendia (finerenone) has strong momentum across chronic kidney disease and heart failure. While Kerendia initially showed a slower uptake, Mr. Oelrich highlighted the strong growth of Kerendia in CKD and T2D, particularly in the US and China. We think the progression will go just one direction, up! Kerendia’s revenue totaled $125 million in 3Q24, up 91% from 3Q23 and up 10% sequentially, and has shown impressive growth since its launch in August 2021. In 2025 and beyond, Mr. Oelrich expects further uptake, particularly accelerating the CKD/T2D indication and seeking broader coverage for the whole CKD spectrum.

- Mr. Oelrich referred to the groundbreaking results of the FINEARTS-HF (n=6,001) trial presented at ESC 2024, in which finerenone demonstrated a 16% relative risk reduction of the primary composite outcome of total heart failure outcomes and cardiovascular death over 32 months among patients with HFmrEF or HFpEF. Application for a heart failure indication has been submitted in the US and China. In 3Q24, Bayer announced that the company is preparing to launch Kerendia for heart failure in 2026.

- The Lancet published a prespecified analysis of the FINEARTS-HF trial of Kerendia in new-onset diabetes in people with HFmrEF or HFpEF. During a median duration of a follow-up of 31 months, 7.2% of participants in the finerenone group and 9.1% of the placebo group developed new-onset diabetes. Finerenone significantly reduced the hazard ratio of new-onset diabetes by 24%. These results were similar in sensitivity analyses, in which new-onset diabetes was expanded to include initiation of SGLT-2 inhibitor treatment with diabetes as an indication, restricted to A1c measurements, and limited to new initiation of glucose-lowering treatments. These results highlight the efficacy of finerenone in reducing the hazard of new-onset diabetes, representing a potential benefit of treatment in this population.

6. Biomea: Refined pipeline focus on diabetes and obesity with icovamenib, a first-in-class menin inhibitor

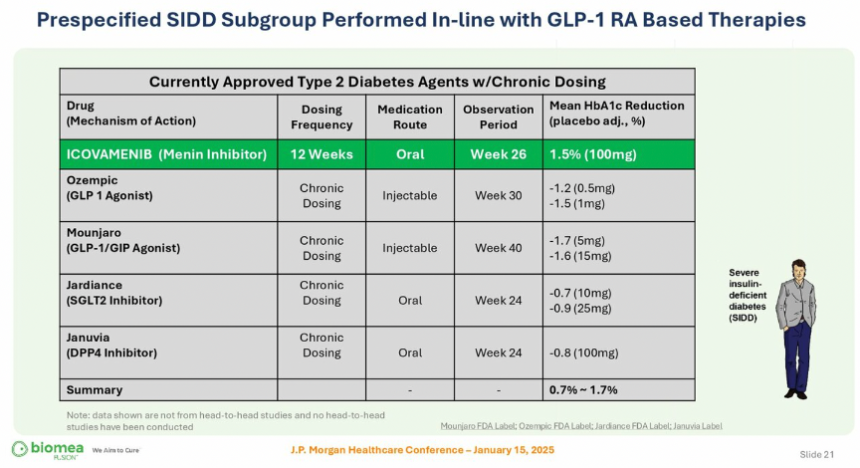

CEO Mr. Thomas Butler highlighted several updates and expectations for Biomea’s icovamenib (BMF-219), a potent and selective covalent menin inhibitor. On Monday, Biomea announced that the company will become a diabetes and obesity treatment company based on promising results of recent clinical trials. Dedicating internal resources to diabetes and obesity, Biomea plans to conclude its studies exploring icovamenib in oncology and explore partnerships to further advance its oncology assets. Most recently, in December 2024, Biomea announced positive topline results of the phase 2 COVALENT-111 study of icovamenib in T2D – full 52-week results are expected in 2H25. Among patients who completed dosing and had suboptimal diabetes management at baseline with one or more treatments, icovamenib showed an A1c reduction of 0.36%, a reduction that would be considered meaningful regardless of the baseline A1c (and more meaningful the lower the A1c). In the study analysis with T2D phenotypes, icovamenib showed further A1c reduction in people with severely insulin-deficient diabetes (SIDD) and those treated with GLP-1 RAs. Additionally, the prespecified SIDD subgroup performed as well as other FDA-approved treatments for T2D (e.g., Ozempic, Mounjaro, Jardiance, Januvia). Biomea plans to discuss results with the FDA in 1H25 and advance icovamenib into the phase 2/3 COVALENT-311 trial in people with SIDD. Icovamenib is also being studied in people with T1D in the open-label portion of the COVALENT-112 trial, which is expected to complete in 2H25.

- Aims to address challenges with current standards of care. Mr Sibold quoted data in his talk asserting that up to 50-75% of people on GLP-1 receptor agonists discontinue them in 12 months, that nearly 70% discontinue SGLT-2 inhibitors at 18 months, and nearly 75% discontinue DPP-4 inhibitors at 18 months. Factors that contribute to discontinuation include side effects, aversion to injection, inability to meet glycemic targets, cost, and affordability. Mr. Butler said icovamenib has the potential to address these challenges, as it provides durable treatment impact on beta cell function and incretin effect.

- Icovamenib to focus on two key patient segments. First, the development of icovamenib targets people with SIDD, which represents 18% of the T2D population according to Biomea Fusion. Mr. Butler explained that the SIDD population has the lowest insulin production of all adults with T2D, representing the highest unmet need with high all-cause mortality and worst CV outcomes. Icovamenib also targets patients on GLP-1 RA treatment, including those who struggle to meet glycemic targets with GLP-1 RAs alone.

- Significant potential for combination treatment. Mr. Butler shared that icovamenib has demonstrated enhanced responsiveness of human donors to Lilly’s tirzepatide and Novo Nordisk’s semaglutide. Icovamenib also enhanced the responsiveness of human donor islets to Lilly’s orforglipron and BMF-650, Biomea’s oral small molecule GLP-1 RA that is in preclinical development. Given these results that were also discussed at WCIRDC 2024, Biomea plans to meet with the FDA to discuss a phase 2 trial of icovamenib and GLP-1 RA combination in T2D.

7. Daiichi Sankyo: Nothing new from Dr. Sunao Manabe on pain

Daiichi Sankyo’s President and CEO Dr. Sunao Manabe provided updates on the company’s oncology portfolio, focusing on its proprietary antibody-drug conjugate (ADC) platform. Of note, the company’s breast cancer drug Enhertu won the 2024 Galien USA Award – which Dr. Manabe compared to the Nobel prize in biomedical innovations – for best biotechnology product.

- Neuropathic pain agent Tarlige was not discussed, nor were DPP-4 inhibitor Tenelia or Canalia, a combination DPP-4 and SGLT2 inhibitor. Tarlige remains part of the company’s “profit growth for current business and products” strategy in the five-year business plan – it was first approved in April 2019 for peripheral neuropathic pain and received an indication expansion in March 2022 to include central neuropathic pain. In May 2023, Daiichi Sankyo launched a disintegrating tablet formulation that dissolves on the tongue, particularly beneficial for people for whom swallowing tablets is difficult.

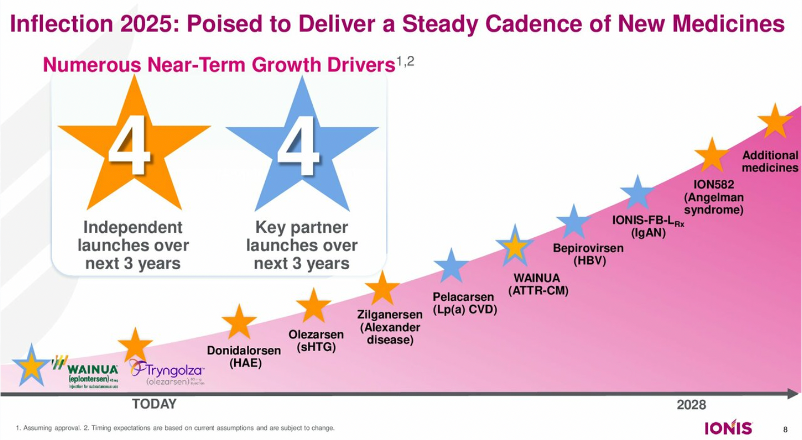

8. Ionis: Preparing for the launch of Tryngolza (olezarsen) as the first FDA-approved treatment for familial chylomicronemia syndrome

CEO Dr. Brett Monia presented Ionis’ progress, especially with the recent approval of Tryngolza (olezarsen) for familial chylomicronemia syndrome (FCS) – the company’s first independent product launch. Dr. Monia emphasized that Ionis is pioneering the field of oligonucleotide therapeutics with a rich history of discovering and developing RNA-targeted treatments. When he delivered his first presentation at JPM 2020 as the newly appointed CEO, Dr. Monia outlined four key objectives for the company: (i) prioritize and advance a wholly owned pipeline; (ii) build commercial capabilities; (iii) expand and diversify technology; and (iv) independently bring treatment to patients. Over the past few years, under Dr. Monia’s leadership, Ionis has, he said, advanced 10 treatments into mid- and late-stage development, established an innovative and scalable commercial organization, and delivered positive clinical results and product launches. Over the next three years, Ionis expects four other independent launches and four key partner launches.

- 2025 will include several key readouts. Ionis’ pipeline also includes pelacarsen [Lp(a)-lowering therapy] in the phase 3 HORIZON program (n=8,323), which is expected to complete in May 2025[2].

- Ionis plans to expand therapeutic opportunities. Looking forward, Ionis plans to expand research and investment in established areas, including cardiovascular disease. Ionis also hopes to expand toward new fields, including pulmonary and renal health.

9. J&J: CEO Mr. Joaquin Duato discusses elements for success with a diversified portfolio, increasing attention for MedTech and Innovative Medicine

This morning, CEO Mr. Joaquin Duato reinforced J&J’s progress for both MedTech and Innovative Medicine, outlining key updates on its ever-expanding diversified portfolio. Looking at long-term growth, Mr. Duato explained that J&J has two elements for success: (i) clear purpose with direction; and (ii) model that prioritizes diversified healthcare. Mr. Duato said that J&J continually works toward spanning capabilities to address needs, and looking forward, he mentioned several exciting opportunities to expand growth. Notably, Mr. Duato expressed confidence in meeting the projected 5-7% growth, especially in Innovative Medicine, a portfolio across therapeutic areas of oncology, immunology, neuroscience, cardiology, and ophthalmology. Given the intersection between diabetes and heart, brain, and eye health, we’re curious how J&J could leverage its existing pipeline for broader outcomes.

- J&J strengthens focus on neuroscience. Just today, J&J acquired Intra-Cellular Therapies for $14.6 billion to expand the development and production of treatments for central nervous system disorders. With this partnership, J&J adds Intra-Cellular Therapies’ Caplyta (lumateperone), a once-daily oral treatment for adults with schizophrenia, as well as depressive episodes associated with bipolar disorders. The acquisition also includes ITI-1284, a promising phase 2 candidate for generalized anxiety disorder and Alzheimer’s disease-related psychosis and agitation. Mr. Duato emphasized that this partnership helps strengthen J&J’s current focus areas.

- MedTech continues to strive toward strong growth. Reinforcing his remarks from last year, Mr. Duato said that J&J has made significant progress in robotics and digitals to advance the MedTech sector. In fact, J&J has met its goals with MedTech to grow in the top market and become more competitive, with 50% of the markets growing more than 5%. Mr. Duato partly attributed this growth to J&J’s acquisition of medical device company Abiomed, which was announced in November 2022 and completed in December 2022. J&J is particularly awaiting approval of the Impella heart pump, which finished clinical trials in 2023, for broader patient populations (e.g., people at risk for heart attack).

10. Lilly: Continued momentum with Mounjaro and Zepbound, advancing incretin treatments for diabetes, obesity, and beyond; upcoming “big assets” include oral GLP-1 orforglipron and “triple G” retatrutide

In an afternoon fireside chat, CEO Mr. David Ricks called 2024 a highly impressive year, with Mounjaro (tirzepatide for diabetes) and Zepbound (tirzepatide for obesity) showing robust growth, and he expressed confidence for this trend to continue (see webcast and presentation). Mr. Ricks discussed Lilly’s updates on the 2024 and 2025 revenue guidance published that morning. Lilly expects 2024 full-year worldwide revenue to be approximately $45 billion (+32%). In 4Q24, Lilly expects revenue of approximately $13.5 billion (+45%), including $3.5 billion for Mounjaro and $1.9 billion for Zepbound. Mr. Ricks acknowledged that the expected 2024 revenue is $400 million (about 3%) below the guidance range announced in 3Q24. Mr. Ricks said that while the US incretin market grew 45% compared to 4Q23, Lilly’s previous guidance had anticipated even faster growth. While 2024 revenue was lower than expected, Mr. Ricks highlighted several milestone achievements, including readouts of tirzepatide in obstructive sleep apnea (OSA) and diabetes prevention, as well as the shortage resolution announced by the FDA in December 2024. With Lilly’s 4Q24 earnings on February 6, 2025, we’re looking forward to hearing more detailed updates.

- Lilly expects to produce at least 60% more scalable doses of incretins in 1H25 compared to 1H24. Given robust sales of Mounjaro and Zepbound, Lilly plans to bring additional manufacturing capacity. Indeed, last year’s JPM 2024 was held when Zepbound had only been on the market for about four weeks, and since then, Zepbound has marked significant penetration in the obesity market. In particular, Zepbound demonstrated strong underlying prescription growth with broad commercial formulary access through employer opt-ins. As of October 1, 2024, Zepbound achieved around 87% of commercial insurance coverage in the US, and 50% of employers have opted into anti-obesity medicine coverage.

- Tirzepatide has promising potential to “unlock” new categories again and again. Beyond diabetes and obesity, Mr. Ricks said tirzepatide has shown significant efficacy in clinical trials for expanded indications. Most recently, in December 2024, the FDA approved Zepbound for moderate-to-severe obstructive sleep apnea and obesity. This approval reflected results on phase 3 SURMOUNT-OSA trial, in which tirzepatide conferred 20% weight reduction and prevented 25 breathing interruptions per hour of sleep. Following this approval, the CMS announced last week that Medicare will cover Zepbound for this expanded indication. Aside from OSA, in the phase 3 SURMOUNT-1 trial, tirzepatide conferred a 94% reduction in the risk of developing T2D in adults with prediabetes and overweight or obesity.

- Upcoming readouts include results for Lilly’s potential “big assets,” including orforglipron (oral GLP-1 RA) and retatrutide (GLP-1/GIP/glucagon triple RA). On orforglipron, Mr. Ricks said meaningful data could significantly impact people who prefer oral formulations. Given that Lilly plans to use different assets that already exist, he imagines scaling to be “multiples” above injectables. With successful results, Lilly plans to first launch orforglipron in the US and progress with “no limit,” as it will be “easy to make and easy to access.” On retatrutide, Mr. Ricks imagines the additional component of a glucagon RA will help those who need to achieve more weight loss and address comorbidities. Aside from orforglipron and retatrutide, Mr. Ricks highlighted Lilly’s expansive portfolio of nine other weight loss candidates.

- Remaining questions involve the duration of treatment, adherence, and maintenance. Mr. Ricks said that people on Mounjaro and Zepbound not only experience clinical outcomes fast but also “feel better quickly.” He said he imagines these treatments to be a “long-duration” therapy and might be even longer than other chronic treatments. Furthermore, Mr. Ricks addressed the importance of weight maintenance, especially among people who successfully achieve weight loss targets. On adherence, Mr. Ricks said it would be important to understand tolerability, as some people can’t tolerate even low doses of GLP-1 RAs.

- Increasing coverage and accessibility remains an important value. In November 2024, the Biden administration proposed a new health policy to expand Medicaid and Medicare coverage of obesity medications. Mr. Ricks said it’s unclear how the incoming Trump administration would implement and finalize this goal with competing priorities. Nevertheless, Mr. Ricks expressed encouragement that the administration has been receptive to conversations and discussions, especially in comparison to the past.

- It was interesting to hear toward the end of the discussion the areas on which Lilly reinforced that it will be particularly focused:

- Increasing transparency on pricing and distribution;

- Addressing the Inflation Reduction Act (IRA); and

- Expanding obesity coverage.

Focusing on the latter, Mr. Ricks said that while diet and exercise are crucial for prevention, these interventions are ineffective treatments for most – and, of course, we know that all can benefit from better heart, kidney, and liver health stemming from GLP-1 and multi-agonists. Mr. Ricks said that Lilly hopes to work with the new US administration to increase broad population targets, changing the trajectory of healthcare and continually impacting patient outcomes.

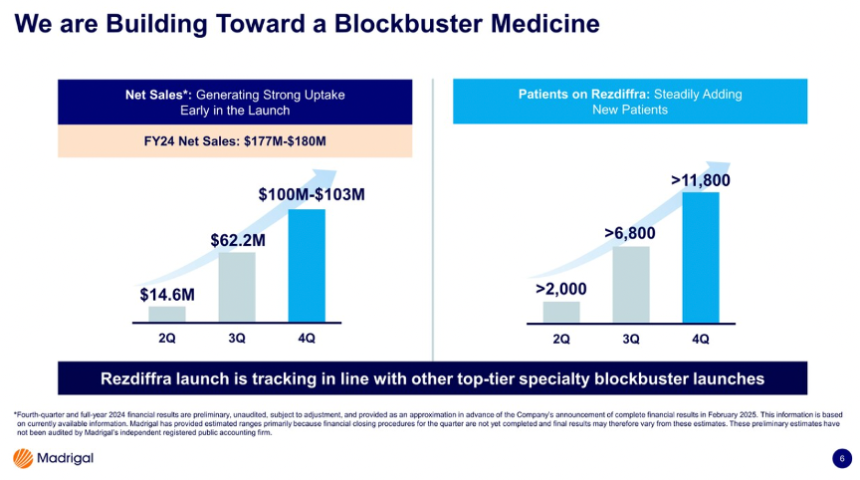

11. Madrigal: “Foundational MASH treatment” Rezdiffra sales total $180 million in the first nine months, with over 11,800 patients treated

CEO Mr. Bill Sibold highlighted Madrigal’s Rezdiffra (resmetirom), the first FDA-approved treatment for MASH, as a highly competitive and successful therapy for continual growth. Overall, this was one of the strongest presentations we saw at JP Morgan, and we look forward to seeing the company expand. Compared to where the company stood at JPM 2024, Madrigal has achieved multiple milestones in just one year.

- In March 2024, Rezdiffra received FDA approval for people with MASH with moderate to advanced liver fibrosis (F2 and F3), based on results from the phase 3 MAESTRO-NASH trial (n=966). Mr. Sibold emphasized that this approval has helped Rezdiffra secure the position as the “foundational” MASH treatment. According to Madrigal’s preliminary financial published on Monday, Rezdiffra totaled $100-103 million in 4Q24 and $166-180 million in 2024 – of note, the full-year result only includes nine months of Rezdiffra’s launch. Previously, Rezdiffra sales totaled $62.2 million in 3Q24 and $14.6 million in 2Q24.

- Furthermore, Mr. Sibold shared that more than 11,800 patients are on Rezdiffra, a significant growth from over 6,800 patients in 3Q24. Madrigal ended 2024 with $931 million in cash, which is expected to support continual launch in the US and upcoming commercialization in the EU.

- Mr. Sibold emphasized that Rezdiffra’s substantial growth reflects the critical need for MASH treatments. He called MASH a serious liver disease, which is expected to become the leading cause of liver transplants in the US. In fact, MASH represents the leading cause of liver-related death and liver transplants. Mr. Sibold shared alarmingly data that once people pass F2 and F3, they have a 10 to 17-fold higher chance of liver mortality. While MASH was previously seen as a “graveyard of drug development,” Mr. Sibold shared excitement that Rezdiffra has demonstrated the potential to address this disease with high unmet needs. We will know more about how broad the Rezdiffra application is when data emerges for patients with stage 4 fibrosis in several years (see more below).

- Rezdiffra’s foundational MASH treatment is attractive from multiple perspectives. Mr. Sibold highlighted Rezdiffra’s differentiated profile as a thyroid hormone receptor-β agonist that directly targets the liver. With this unique mechanism of action, Rezdiffra targets the underlying causes of MASH. Additionally, Rezdiffra provides highly effective treatment, as it improves liver stiffness in 91% of patients at three years. Finally, as a once-daily oral pill, Rezdiffra offers patients ease of administration, along with a well-tolerable profile.

- The market opportunity is very large, regardless of competitors entering the landscape. Mr. Sibold emphasized that given Rezdiffra is the first and only MASH treatment, and that it provides an attractive market of 315,000 people diagnosed with F2 and F3 who are seeing a specialist that Madrigal could call on. Mr. Sibold estimated that Rezdiffra has treated <4% of the target population to date, and therefore, there’s plenty of market opportunity ahead.

- During Q&A, Mr. Sibold expressed confidence in Madrigal’s success and leadership position, even with (some may say especially with) the potential approval of GLP-1 RAs in MASH. While we aren’t sure of the market that they will target, we imagine it will include those with stage 1 fibrosis. In fact, Mr. Sibold said GLP-1 RAs entering this landscape will help expand the market and further increase awareness, screening, diagnosis, and treatment. Furthermore, he noted high discontinuation rates of GLP-1 RAs pose a challenge compared to Rezdiffra, which has high tolerability. Mr. Sibold also pointed to opportunities for combination therapies, as 25% of patients of Rezdiffra are on GLP-1 RAs, and 50% have been previously exposed to GLP-1 RAs.

- F4 indication has the potential to double Rezdiffra’s opportunity. Mr. Sibold reminded that the ongoing MAESTRO-NASH-OUTCOMES trial (n=845) of Rezdiffra in patients with cirrhosis (F4) has completed enrollment in October 2024, as shared in 3Q24. This trial is of great interest, as positive outcomes could lead to expanded indications for Rezdiffra, potentially doubling its target patient population. This trial was initiated in August 2022 and is expected to complete in January 2027. Alarmingly, Mr. Sibold said that people with F4 have a 42-fold increased risk of liver mortality.

- During Q&A, Mr. Sibold addressed a question regarding the potential of Rezdiffra in delaying or preventing MASH. Given the efficacy of Rezdiffra in F2 and F3, Mr. Sibold said that this is the population Madrigal is focused on. He said, “That’s where the benefit lies … where the values are with the highest unmet need.” He suggested that perhaps GLP-1 RAs could be indicated for prevention.

- Madrigal awaits Rezdiffra’s approval and commercial launch in the EU in 2025, country by country. As emphasized in 3Q24, Madrigal plans to commercialize Rezdiffra in the EU pending EMA regulatory approval, expected in mid-2025. In the discussion, Mr. Sibold announced plans to start commercialization in the EU one country at a time, starting with Germany. Overall, Mr. Sibold expressed high optimism, as Rezdiffra has already been recommended as a first-line treatment for MASH in the joint EASL-EASD-EASO clinical practice guidelines for MASH, presented at EASL 2024. With 125 trial sites across the EU, Mr. Sibold said several countries are familiar with Rezdiffra and have expressed significant interest.

- Mr. Sibold hopes to build a pipeline to secure long-term growth. He emphasized the high efficacy and quality of Rezdiffra, explaining that now, the company aims to build a pipeline over the next several years to fortify Madrigal’s leadership market position in MASH. When asked about the specifics of a potential pipeline during Q&A, Mr. Sibold suggested exploring the next best mechanism of action or combination treatments that enhance Rezdiffra’s efficacy. In the meantime, of course, Madrigal plans to continue positioning Rezdiffra as a foundational treatment. We imagine this will continue to be quite effective given the major needs in the field and no competition now.

- Diagnosing and screening MASH as an emerging field. As the field is moving away from using liver biopsies to diagnose MASH (at least later stage MASH, meaning stage 2 or stage 3), Mr. Sibold expects several developments in this arena. He said, for example, that more interest has emerged in non-invasive tests (NITs), especially with the approval of Rezdiffra. He said it would be important to figure out the best sequence and combination of NITs to improve diagnoses. Additionally, he referred to the FIB-4 score, which the ADA called the “most cost-effective” strategy for identifying people at risk for MASH in the 2025 Standards of Care.

12. Merck: Diversifying portfolio in diabetic macular edema; upcoming key readouts with PCSK9 and GLP-1 RA

Reflecting on the past three years since his appointment as CEO, Mr. Robert Davis said Merck has delivered impressive “breadth and depth” to the field beyond oncology. Alongside consistent revenue growth, Merck has expanded its portfolio to increase focus on other therapeutic areas – compared to nine assets in 2021, Merck had 26 candidates in 2024. With a growing pipeline, Mr. Davis affirmed Merck’s ability to continually grow and impact patient outcomes into the next decade and beyond.

- As a testament to a diversifying portfolio, Mr. Davis recalled Merck’s acquisition of London-based EyeBio in May 2024. Following this acquisition, Merck announced the initiation of the phase 2b/3 BRUNELLO trial (960), evaluating Restoret (MK-3000) for diabetic macular edema (DME) in September 2024. The BRUNELLO trial will enroll people with T1D or T2D and DME, and it is expected to complete in December 2027. With Restoret, Merck aims to address current shortcomings with DME with anti-VEGF injections (Eylea or Vabysmo).

- On key readouts, Mr. Davis noted several upcoming results in the cardiometabolic portfolio that will be shared in 2025. Oral PCSK9 enlicitide decanoate (previously called MK-0616) is in a phase 2b trial that is expected to complete in December 2025; this timeline is a bit delayed from the projected date of October 2025. Additionally, GLP-1/glucagon RA, MK-6024 (efinopegdutide) is in multiple phase 3 trials with hypercholesterolemia: (i) CORALreef Lipids (n=2,760), expected to complete in August 2025; (ii) CORALreef HeFH (n=270), expected to complete in April 2025; and (iii) CORALreef Outcomes (n=14,550), expected to complete in November 2029.

- While Mr. Davis did not share in today’s presentation, in December 2024, Merck announced a partnership with Hansoh Pharma for HS-10535, an investigational preclinical oral small molecule GLP-1 RA. This announcement reinforces Merck’s expanding portfolio into the obesity arena, in which Dr. Davis shared significant interest in recent earnings calls (1Q24, 2Q24, 3Q24).

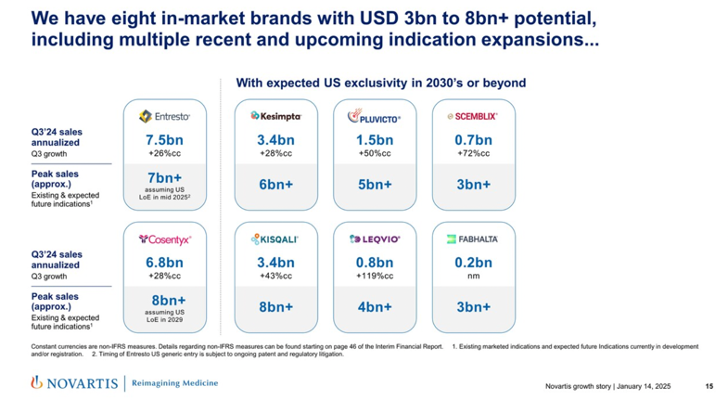

13. Novartis: Innovation across four therapeutic areas, with significant progression of Entresto and Leqvio for heart failure and CVD

CEO Dr. Vas Narasimhan highlighted Novartis’ innovation across four therapeutic areas: (i) cardiovascular-renal-metabolic disease; (ii) immunology; (iii) neuroscience; and (iv) oncology. Dr. Narasimhan affirmed that Novartis continues to progress significantly, combining core therapeutic areas and technology platforms in four priority regions, including the US, China, Germany, and Japan. Over the past few years, Novartis has streamlined the pipeline by nearly 40% (155 projects in 3Q21 compared to 94 in 3Q24). With a more focused R&D, Dr. Narasimhan said the company has increased research resources by nearly 50% per project and 5% of developmental spending. Novartis also continues to leverage technology platforms to enhance the scalability of the pipeline and integrate a diverse, broad application.

- Novartis has eight in-market brands in the US with up to $8 billion peak potential. These products include Entresto (sacubitril/valsartan), an angiotensin receptor-neprilysin inhibitor (ARNI), for heart failure, which totaled $7.5 billion in annualized 3Q24 sales. Dr. Narasimhan emphasized that peak sales will reach more than $7 billion, assuming Novartis files for a loss of exclusivity (LOE) for Entresto in the US in mid-2025. Previously, in 3Q24, US sales grew by 25%, with total prescriptions (TRx) increasing by 20%, around 45,000 new-to-brand prescriptions (NBRx), and around 500,000 TRx per month. Another product that Dr. Narasimhan highlighted included Leqvio (inclisiran), an siRNA PCSK-9 inhibitor, which totaled $800 million in annualized 3Q24 sales, with a potential to reach more than $4 billion in peak sales.

- Novartis continues to build a strong pipeline across cardio-renal-metabolic health to address high needs. In this sector, Novartis focuses on select disease areas, including heart failure and hypertension, atherosclerosis, arrhythmia, and acute kidney injury (AKI). Dr. Narasimhan shared that Entresto and Leqvio contribute to this therapeutic area as anchor assets, and he expressed excitement about advanced platforms like siRNA.

- Novartis has more than 15 submission-enabling readouts in the next two years. Dr. Narasimhan particularly showed excitement about readouts for Leqvio in primary prevention (VICTORION-1-PREVENT, expected April 2029) and secondary prevention (ORION-4 and VICTORION-2-PREVENT, expected in 2026 and 2027, respectively). Additionally, data for the Lp(a)-HORIZON trial (n=8,323) will highlight pelacarsen in major cardiovascular events in people with CVD (expected in May 2025).

14. OPKO Health: Dr. Elias Zerhouni highlights the promising potential of dual GLP-1/glucagon RA in development for oral and injectable formulations

President and Vice Chairman Dr. Elias Zerhouni shared updates on OPKO Health’s business and pipeline development across oncology, immunology, and metabolic diseases (see webcast and presentation slides). Reflecting on 2024, Dr. Zerhouni highlighted the successes of the ModeX proprietary technologies, acquired in May 2022, in advancing several candidates to the clinical stage for oncology and viral diseases. He also celebrated the growing revenue from OPKO Health’s two products, Ngenla (human growth hormone for pediatrics) and Rayaldee (calcifediol for stage 3 or 4 chronic kidney disease and vitamin D insufficiency). He also highlighted the growth of BioReference Health’s laboratories, which has positioned OKPO Health on a stronger financial footing.

- We were particularly excited to hear updates on the company’s incretin-based candidates: (i) GLP-2 RAs; and (ii) oxyntomodulin (OXM) analog, a dual GLP-1/glucagon RA for diabetes, obesity, and MASH. OPKO Health is developing these candidates in both injectable and oral tablet formulations – the latter in collaboration with Entera Bio since September 2023. Dr. Zerhouni noted that GLP-1 receptor mono-agonists are no longer “sufficient” for increasing metabolism and addressing comorbidities, expressing confidence in the potential of dual GLP-1/glucagon RA for obesity and advanced liver diseases (F2, F3, and F4). Dr. Zerhouni emphasized that glucagon RAs act on the liver and complement the limitations of GLP-1 RAs, and the preclinical data are promising. While not mentioned in today’s presentation, preclinical data of oral OXM in rodents and pigs are also favorable, as announced in September 2024. Dr. Zerhouni expects these candidates to advance to clinical trials by late 2025 or early 2026.

15. Pfizer: Dr. Albert Bourla expects phase 3 trial of once-daily oral GLP-1 in 2H25; confidence in capturing oral GLP-1 RA market

In a fireside chat, CEO Dr. Albert Bourla shared Pfizer’s vision for 2025 amid new administrations, product launches, and ongoing clinical trials. See webcast and presentation slides. Dr. Bourla began by reflecting on the successes of 2024. Pfizer secured 13 approvals across generic disorders, vaccines, and cancer treatments; achieved a $4 billion cost reduction; and restructured R&D, including leadership changes and organizational improvements, meeting five key priorities discussed last year at JPM 2024. Looking ahead with the new year, Dr. Bourla highlighted new values: (i) improve R&D productivity and operational efficiency through technologies like AI; (ii) maintain leadership in vaccines, cardiovascular disease, and migraine; and (iii) optimize capital allocation. Dr. Bourla also shared anticipation that the upcoming Trump administration will cause “radical changes” and believes that opportunities will outweigh the risks. Pfizer will engage proactively with the new administration to influence policy to improve innovation and access to medicine, given the intensifying competition with global players in biosciences like China. While much of the fireside chat focused on R&D and commercial updates for COVID-19 and cancer treatments, Dr. Bourla presented insights on Pfizer’s once-daily, oral GLP-1 RA, danuglipron.