Abbott 3Q25 – Diabetes Care revenue exceeds $2 billion (+19%; +16% operationally); focus turns to non-insulin intensive T2D population in the US; DGK launch expected in 2026 –

Executive Highlights

- CEO Mr. Robert Ford and CFO Mr. Phil Boudreau led Abbott’s 3Q25 financial results this morning (see press release, webcast, infographic).

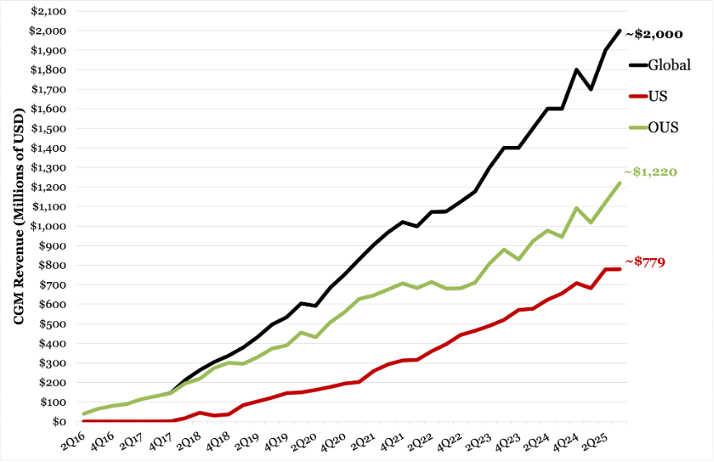

- 3Q25 was another impressive quarter for Abbott’s CGM business across its full and growing portfolio, in key international markets in particular. FreeStyle Libre revenue totaled $2 billion for the first time in 3Q25, growing 25% from 3Q24 and 5% sequentially. Growth was led internationally, with 29% FreeStyle Libre growth OUS and 19% growth in the US. FreeStyle Libre and Lingo represented an estimated 97% in 3Q25 revenue, similar to previous quarters[1].

- Today’s call highlighted the opportunity Abbott has in working with people with T2D not only on basal insulin but also those on less-intensive medicines like GLP-1 and SGLT-2 inhibitors. Indeed, these are broader opportunities in the CGM landscape, particularly within the non-intensive and non-insulin T2D populations in the US and internationally.

- In the basal-only segment, Mr. Ford remained bullish on Abbott’s competitive position. He estimated market penetration at roughly 20% in the US and just 5% internationally. Despite regional variability in adoption rates, Mr. Ford noted that US basal-only growth has lagged behind key European markets that have full basal coverage, where uptake has reached about 75% of the rate seen among intensive insulin users.

- Mr. Ford pointed to the importance of reaching more PCPs, where awareness of the clinical value of CGM is high but usage remains limited.

- Mr. Ford also highlighted significant opportunity in the broader non-insulin T2D population, citing early positive signals from the CMS and strong support from the ADA for expanding CGM coverage to this group. He said CMS policy changes could begin to take shape as early as the first half of 2026[2].

- 3Q25 was another impressive quarter for Abbott’s CGM portfolio, particularly in key international markets. FreeStyle Libre revenue totaled $2 billion for the first time in 3Q25, growing 25% from 3Q24 and 5% sequentially. Growth was led internationally, with 29% FreeStyle Libre growth OUS and 19% growth in the US. FreeStyle Libre and Lingo represented an estimated 97% in 3Q25 revenue, similar to previous quarters.

- The rest of Abbott’s CGM portfolio is exciting, indeed, ranging from the Medtronic CGM partnership to the multi-analyte sensors, a very exciting program. Mr. Ford reiterated Abbott’s anticipated launch of its dual glucose-ketone (DGK) sensor sometime next year, as shared in 2Q25, and announced for the first time that it would initiate a continuous lactate monitor sensor Investigational Device Exemption (IDE) trial in 2026.

Table of Contents

-

Financial Highlights

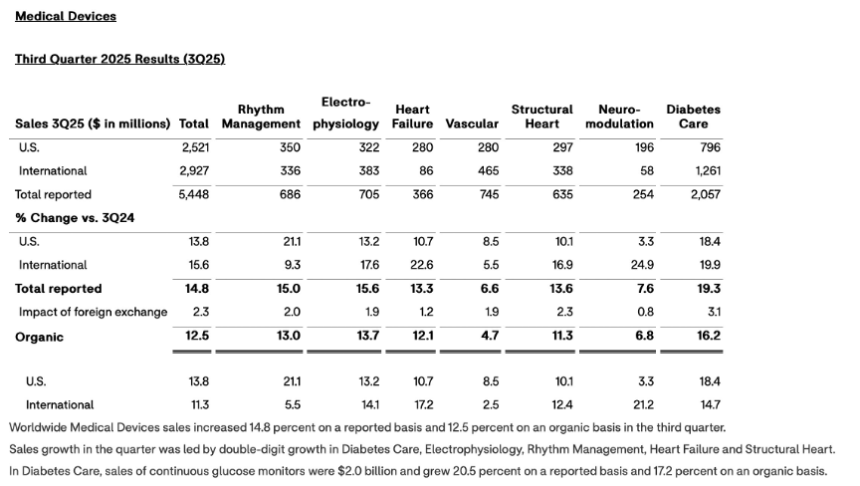

- 1. Diabetes Care revenue surpasses $2.1 billion (+19%; +16% operationally); CGM revenue totals $2 billion (+25%; +17% operationally)

- 2. International Diabetes Care revenue totals $1.3 billion (+20%; +15% operationally)

- 3. US Diabetes Care revenue totals $796 million (+18%); US CGM revenue grows 19% – quarterly results reflect multiple drivers

- 4. “Adapting and delivering” to global tariff pressures

-

CGM Franchise Highlights

- 1. An area of new note: Mr. Ford reports just 20% US and 5% OUS market penetration in T2D non-intensive insulin population

- 2. Multi-analyte sensors in 2026: DGK launch and pivotal trial for lactate sensor anticipated next year

- 3. Abbott-partnered CGM Instinct launched by Medtronic in the US

- 4. At one year anniversary of Lingo, focus remains squarely on Libre franchise

- 5. New Ensure and Glucerna offerings in nutrition, though PROTALITY unmentioned

- Diabetes-Related Analyst Q&A

- Close Concerns’ Questions

Financial Highlights

1. Diabetes Care revenue surpasses $2.1 billion (+19%; +16% operationally); CGM revenue totals $2 billion (+25%; +17% operationally)

Abbott Diabetes Care recorded $2.1 billion in sales in 3Q25, up 19% (+16% operationally) from 3Q24 and 4% sequentially. Growth was driven by: (i) continued expansion across both basal-bolus and basal-only insulin users; (ii) rising CGM adoption among non-insulin users; and (iii) sustained international strength.

- CGM revenue totaled $2 billion, up 25% (+17% operationally) from 3Q24 and up 5% sequentially. As in previous quarters, 3Q25 FreeStyle Libre and Lingo accounted for over 95% of revenue. FreeStyle Libre’s sales have been bolstered by expanded reimbursement for basal-only users in the US and select international markets, as well as broader commercial coverage among non-insulin using populations.

Source: Abbott 3Q25

- Volume growth in Diabetes Care is increasingly international. Diabetes Care business grew $332 million from 3Q24 (from $1.7 billion) and $76 million sequentially (from $2 billion).

- International Diabetes Care totaled $1.26 billion, up $209 million from 3Q24 and up $74 million sequentially.

- US Diabetes Care totaled $796 million, up $123 million from 3Q24 and steady (+2 million) sequentially.

- Management acknowledged the impact of tariffs and foreign exchange on gross margin and emphasized that the Diabetes Care remains a core growth driver, supported by FreeStyle Libre’s global affordability positioning and expanding global manufacturing scale. In Q&A, Mr. Ford characterized tariff pressures as unexpected, relative to what might have been expected some time back, and emphasizing Abbott’s longtime and in our view extremely impressive ability to “adapt and deliver.” His comments underscored the company’s confidence in being able to offset tariff-related cost pressures through its global scale, manufacturing efficiency, and operational presence – we were quite impressed in hearing about the company’s tariff mitigation program, discussed briefly by CFO Mr. Phil Boudreau. Mr. Ford reiterated that, despite these headwinds, Abbott remains on track to expand gross margins over time, reaffirming full-year 2025 guidance.

2. International Diabetes Care revenue totals $1.3 billion (+20%; +15% operationally)

International Diabetes Care revenue reached $1.3 billion in 3Q25, up 20% (+15% operationally) from 3Q24 and 6% sequentially. We estimate that OUS CGM revenue totaled $1.2 billion, up 29% from 3Q24 and up 9% sequentially. OUS growth accounted for nearly two-thirds (63%) of year-over-year growth in Diabetes Care and nearly all of the quarter’s sequential growth. Mr. Ford cited Abbott’s scale, cost position, and geographic breadth as major bigger factors to its strength outside the US.

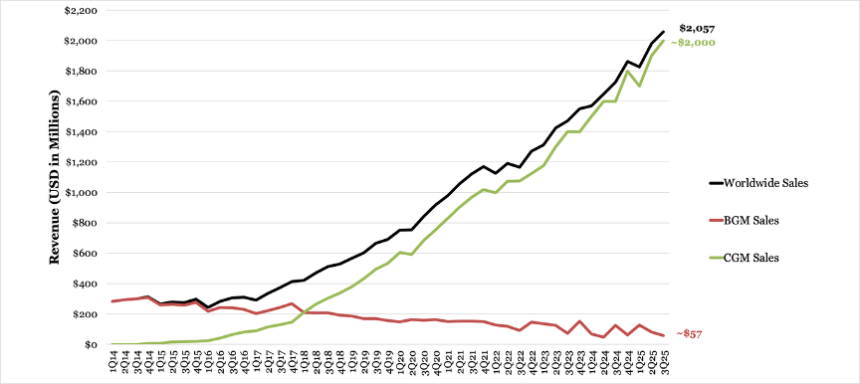

While it is quite challenging to estimate BGM sales[3], we imagine they may have totaled as little as ~$60 million in 3Q25, down quite substantially (perhaps on the order of 50% but it could be much less) from 3Q24, and down as much as 30% sequentially. OUS BGM revenue may have totaled ~$40 million in 3Q25, down as much as 60% from 3Q24 (against a tough comparison of 1.2x growth) and down 38% sequentially.

3. US Diabetes Care revenue totals $796 million (+18%); US CGM revenue grows 19% – quarterly results reflect multiple drivers

US Diabetes Care sales totaled $796 million, up 18% from 3Q24 and flat sequentially. This represents 39% of Abbott’s total Diabetes Care revenue, roughly on par with previous quarters.

- During Q&A, Mr. Ford noted that US CGM revenue grew 19% from 3Q24, implying sales of $780 million, flat sequentially. He attributed much of the lack of sequential growth primarily to stocking dynamics – while this is can “sound” challenging to understand, the growth expected for the year remains as strong as ever. Specifically, Mr. Ford said that a new manufacturing site outperformed expectations in 1H25, enabling early fulfillment of FreeStyle Libre 3 Plus sensor backorders across multiple US channels present since the sensor’s US launch. This led to greater pull-forward in revenue than anticipated, some of which was originally expected to come in 3Q25. Despite these timing effects, Mr. Ford said that Abbott sees multiple avenues of growth in the US, particularly through expansion into the non-insulin intensive T2D market – a priority for the company (see more below). As well, he confirmed that US revenue is up 25% year-to-date, keeping Abbott on track to meet its full-year growth target of over 20%. Potential key drivers of this growth include:

- Further increased adoption among basal-only insulin users in the US (penetration was said to stand at 20%);

- Increased ease of use for providers following Libre data integration with Epic EHR in April, a feature Mr. Ford highlighted in his prepared remarks as particularly valuable for busy PCPs – hopefully this is also helping their interpretation abilities;

- Presumed growth in Lingo adoption, particularly after its launch on Amazon in February; and

- Expanding AID compatibility with FreeStyle Libre sensors:

- Insulet launched Omnipod 5 with FreeStyle Libre 2 Plus compatibility in November 2024;

- Beta Bionics launched iLet with FreeStyle Libre 3 Plus integration in October 2024;

- Sequel also initiated a phased launch of twiist with FreeStyle Libre 3 Plus in the US in July; and

- Medtronic initiated the launch of the Medtronic-Abbott sensor integrated with MiniMed 780G last month.

- While it is difficult to assess, we estimate that US BGM revenue may have been in the range of $16 million, down 8% from an easy comparison of 26% decline in 3Q24. Estimated sales grew approximately 7% sequentially – unfortunately, due to rounding of large numbers, this could easily be growth that is meaningfully higher or lower, and we’ll return to look at this market again.

More integrations are still expected this year, including:

- a full launch of FreeStyle Libre 3 Plus with Tandem’s t:slim X2 in the US following the June launch of an early access program;

- the international launch of FreeStyle Libre 3 Plus and t:slim X2 integration; and

- Tandem’s Mobi and FreeStyle Libre 3 Plus compatibility for US and international users.

While these partnerships weren’t discussed at length, Q&A today was so fascinating – we include a fragment of a particularly striking part of the discussion below (see our Appendix for the full Q&A).

Q (Robbie Marcus, JP Morgan): Good morning, and thanks for taking the questions. Robert, could you give more color on what’s happening in the US and outside the US and how you're thinking about the market developing, particularly in the US with the ketone sensor on its way hopefully next year and what seems like increasing commentary on CMS coverage of non-intensive type 2?

A Mr. Ford: Yes, US grew 19%. We didn't really have any kind of comps on that. So – and year-to-date, the US is up 25%. I think growth – I think what you're referring to a little bit there is growth in the first half of the year was a little bit higher really due to some shelf restocking dynamics that we saw. If you remember, last year, Robbie, we launched Libre 3 Plus and had a pretty significant drive in demand here, higher than what we had anticipated. And the new manufacturing facility we made investment wasn't fully up and running. So, that caused backorders with customers [and] backorders with the wholesalers at the pharmacy channel.

The way we had planned this year was our manufacturing site would come up and running, and it would be more of a linear kind of recovery. But the factory actually did really well in the first half. So, that led to customers doing some restocking earlier than what we had thought and a little bit higher, quite frankly, just given the demand that they were seeing in Libre 3. So, that resulted in a little bit of a pull-forward of a couple percentage points of growth. So … it's just a little bit of a timing dynamic. I think most importantly, we remain on track with the original US full year growth assumption of over 20%. So, demand is still very – very strong …

To your question on kind of next year, yes, I expect to see another real strong year of growth in the US with additional demand coming from the new sensor, the new dual-analyte sensor … That's going to help drive increasing penetration in that intensive insulin user segment. So, I'd say there's still room for penetration internationally … in that segment. In the US, there's still some room also. But I'd say that's going to really help us drive share gains, whether it's in the pumper segment or just in general intensive insulin user segments.

There's still a lot of penetration in the basal segment. I know because of the dual-analyte sensor, we get a lot of attention on this insulin – intensive insulin segment. But I'm still very bullish on the basal segment. In the US, it's only about 20% penetrated today. Internationally, it's only 5% – it's less than 5%. So, I think there's still a lot of opportunity for growth in the US with continued basal penetration, and then not to mention the potential for CMS to cover type 2 non-insulin. I think that's an opportunity. I see positive signs of that developing. The ADA has been very supportive of that.

I think you could probably see proposed coverage of that come out sometime next year, maybe in the first half. But then, you've got – and you know this pretty well, Robbie. You've got your normal timing there of comment periods, the final cover decision, when the actual date is going to be [isn’t known]. So, I think there's a scenario where that could happen next year. But – and we'll be ready to execute. But I'm not building that assumption of that segment coming in or having any significant contributions in 2026. It's not in my base forecast for 2026 … But I think if it becomes a reality, I think this will be a real nice win for CMS patients.

So, I think we got a lot of growth opportunities between the patient segments, between the technology being launched across geographies. I know your question was focusing a lot on the US. I think we've got a great portfolio and a great lineup as we go into the US next year. But I also think there's just tremendous opportunity internationally, and that's an area of particular strength for us that we've built the scale, that we've built the technology and the cost positions there. So, yeah, I feel good about Libre. I feel good about our US position and the momentum that we're going to have US and internationally.

4. “Adapting and delivering” to global tariff pressures

Management acknowledged the impact of tariffs and foreign exchange on gross margin and emphasized that the Diabetes Care remains a core growth driver, supported by FreeStyle Libre’s global affordability positioning and expanding global manufacturing scale. In Q&A, Mr. Ford characterized tariff pressures as “unexpected, but not excuses,” emphasizing Abbott’s ability to “adapt and deliver.” His comments underscored the company’s confidence in being able to offset tariff-related cost pressures through its global scale, manufacturing efficiency, and operational presence. Mr. Ford reiterated that, despite these headwinds, Abbott remains on track to expand gross margins over time, reaffirming full-year 2025 guidance.

CGM Franchise Highlights

1. An area of new note: Mr. Ford reports just 20% US and 5% OUS market penetration in T2D non-intensive insulin population

Today’s call highlighted Abbott’s interest in broader opportunities in the CGM landscape, particularly within the non-intensive and non-insulin T2D populations. Overall, Mr. Ford expressed optimism about long-term market expansion, citing strong clinical value, growing awareness, and potential policy shifts. He also urged the US Abbott team to broaden its engagement with clinicians to help catalyze adoption in an area he considered underpenetrated: people with T2D who are managed with only basal insulin.

- In the US basal-only segment, Mr. Ford remained bullish on Abbott’s competitive position and room for growth. He estimated market penetration at roughly 20% in the US and just 5% internationally. Despite regional variability in adoption rates, Mr. Ford noted that US basal-only growth has lagged behind key European markets with full basal coverage, where uptake has reached about 75% of the rate seen among intensive insulin users. Regardless, Mr. Ford emphasized strong underlying momentum in areas in the US where CGM adoption is low and pointed to the importance of reaching more primary care physicians (PCPs). While awareness of CGM and its clinical value for the population is high, actual experience among PCPs remains limited. Mr. Ford noted that growth is “probably more dependent on [Abbott’s investment to reach more physicians] than concerns on whether or not there is value – the clinical data is pretty resounded.” He also emphasized the importance of sustained investment in US regions where penetration is already high, aiming to ensure continued expansion.

- Mr. Ford highlighted the April integration of FreeStyle Libre data with EHR Epic as a key step in simplifying CGM use for busy PCPs. This “turnkey solution” allows providers to more easily manage patients and leverage ambulatory glucose profiles to identify issues and adjust care more efficiently.

- While Mr. Ford focused on the opportunities presented by the US basal-only population, we are also intrigued to see how Abbott can harness the significant opportunity posed by this population internationally, particularly given the low 5% penetration rate among basal-only T2D users outside the US. We acknowledge that reimbursement remains a key barrier in many countries. While some European markets — like France and parts of Italy — already cover FreeStyle Libre for basal-only users, many limit reimbursement to those with T1D or T2D on basal-bolus regimens. Further penetration will likely rely on robust real-world evidence that prompts government into faster action.

- Mr. Ford also cited early positive signals from the CMS. While CMS policy changes could begin to take shape as early as the first half of 2026, he was cautious about projecting immediate financial impact – especially as the proposed change would require additional time for public comment periods and final CMS review. He emphasized that revenue forecasts will not assume material contributions from this potential policy shift next year, but noted it could serve as a key driver of long-term adoption and growth.

2. Multi-analyte sensors in 2026: DGK launch and pivotal trial for lactate sensor anticipated next year

Mr. Ford indicated that Abbott’s DGK sensor is expected to launch next year. He characterized this as a potential tailwind for the company, with revenue growth from new products across MedTech overall expected to ramp throughout the year. Addressing lower US growth compared to international, Mr. Ford said that the DGK sensor is expected to drive increasing penetration among intensive insulin users with the opportunity for Abbott to increase market share. Additionally, Mr. Ford identified insulin pump users as a target population for the sensor upon launch, a reflection of the focus of panelists at conferences and scientific gatherings around the world on its potential to detect early ketone rise following an undetected insulin pump suspension. No further details on launch timing or pricing were shared in today’s call.

- In advance of the launch, key insulin pump manufacturers have shared their intentions to integrate with the DGK sensor. Sequel first shared its intention to integrate its AID system (twiist) with the upcoming sensor in May, and Tandem, Beta Bionics, and Ypsomed and CamDiab followed with respective announcements in the days leading up to ADA 2025. Insulet has also spoken publicly about its agreement with Abbott for Omnipod 5-DGK integration. Surprisingly, there was no commentary in today’s call about these integrations.

Abbott also announced plans to initiate a continuous lactate monitor sensor Investigational Device Exemption (IDE) trial in 2026. This will be part of nearly 200 clinical trials planned across various geographies and areas of research. This announcement provides concrete detail on the development of sensors for this analyte, which Abbott has previously said could offer new metabolic insight for patients. Elevated lactate can indicate metabolic disturbance due to factors like septic shock and heart failure.

3. Abbott-partnered CGM Instinct launched by Medtronic in the US

While unmentioned on today’s call, the Instinct sensor developed by Abbott reached a key milestone in 3Q25, with Medtronic beginning to roll out the sensor in September and initial shipments expected in November. The sensor will launch integrated with MiniMed 780G following FDA clearance earlier this month of Medtronic’s SmartGuard algorithm as an interoperable automated glycemic controller (iAGC), alongside the previously cleared MiniMed™ 780G insulin pump as an alternate controller enabled (ACE) pump. While financial terms of the Abbott-Medtronic partnership have not been disclosed, we remain interested in understanding the material upside Abbott may realize as Instinct adoption scales.

4. At one year anniversary of Lingo, focus remains squarely on Libre franchise

Lingo was also not mentioned in today’s prepared remarks or in Q&A. The OTC CGM was launched in the US in September 2024. The sensor is designed for individuals 18 years or older not on insulin therapy. As of 4Q24, Mr. Ford discussed plans to eventually expand the launch of Lingo in the US and explore additional international markets beyond the United Kingdom. Abbott has not provided any userbase updates in past quarters or today.

5. New Ensure and Glucerna offerings in nutrition, though PROTALITY unmentioned

In nutrition, sales increased 4% in 3Q25. This was led by Abbott’s adult nutrition business, particularly by the nutrition shake Ensure. Mr. Ford highlighted a 10% growth in international markets with high demand for Ensure and Glucerna. The company plans to continue to invest in these brands: recently, Abbott launched a version of Glucerna with one gram of sugar, and plans to launch a version of Ensure with 42 grams of protein later this month. There were no updates on Abbott’s PROTALITY nutritional brand, which intends to support muscle mass preservation during weight loss. Given the worry about this generally, we are surprised Abbott is not highlighting this more on the call.

Diabetes-Related Analyst Q&A

On 2026 outlook, margins, and tariffs

Q (Larry Biegelsen, Wells Fargo): Robert, back in July, you sounded comfortable with consensus sales and EPS for 2026. What are your high-level thoughts on next year, if you're still comfortable with consensus? It seems like you have some nice tailwinds next year.

Mr. Robert Ford, CEO: Yeah, I'm very comfortable with consensus. In fact, this is a question that was asked last year in our Q3 earnings call, and consensus for 2025 at that time was 7.5%, EPS growth of 10%. That's the same consensus estimates that we have today. I was comfortable with delivering that type of growth at this time last year, and I'm comfortable again today to forecast and deliver that type of growth next year. These estimates that you referenced, they're pretty much in line with the results that we've delivered year-to-date. We delivered those results in a year where we faced, I'd say, larger-than-expected headwinds in Diagnostics and unexpected impact here from tariff. I think that's just a great example of the culture we have here at Abbott. So, it's just no excuses, just adapt and deliver. The portfolio that we have, we have the ability to do that. But, when I think about our ability to sustain this level of performance that we're seeing in 2025 into 2026, I really see it as kind of three key buckets of growth for us, Larry.

First of all, there's underlying momentum in the current portfolio, whether it's in MedTech, in Established Pharmaceuticals, in a large portion of our Diagnostic business, and I expect that momentum to continue. We've got high-growth products here, whether it's AVEIR, TAVR, Libre, TriClip. I'm sure we'll talk about those. So, that's one big driver of our growth sustaining into next year.

Second one, I'd say, is new product launches. We've got a lot of new product launch cadence into next year, whether it's Volt in the US, TactiFlex Duo, dual-analyte sensor, the new Alinitydiagnostic system, biosimilars. I mean, these are all product launches here that will add to our sales and sales growth, and that will gain momentum over the course of year.

Then, as I said also, we've got some easing of some of the headwinds that we had this year. Pretty significant headwind in Diagnostic. We talked about that in July, over $1 billion of headwind, whether it's the VBP pricing dynamics in China this year or the decline in COVID testing. I think we'll start to see a full lapping of that next year on a full year basis. But we'll start to see some of it quite frankly in Q4. So, I feel very confident and comfortable with that type of top line growth. If you look also why we're in this position, Larry, I mean, we made investments in 2020, 2021. These product launches that I'm highlighting here, those are investments that we made. So, we'll be able to deliver the high single-digit top line growth, double-digit EPS growth, while at the same time, I'm going to remain unwavering here in the commitment to invest in the pipeline and drive growth organically.

We'll have close to 200 clinical trials across all of our businesses across a variety of different geographies next year. And within those, we're going to initiate some really important pivotal trials next year that we're funding for products that we expect are going to be significant contributors in the future, whether it's the mitral valve replacement clinical trial that will go into IDE. Our balloon TAVR trial will go into IDE, AVEIR conduction system pacing, peripheral IVL IDE trial, a continuous lactate monitor sensor IDE trial. So, we can maintain this top and bottom-line growth while at the same time making the investments in the portfolio that we know we need to do. And then, we've got a good track record here of expanding our gross margins and our op margins. We've got great gross margin improvement teams. We've been able to work hard this year to be able to mitigate the impact of tariffs as they have full year effect next year. So, we feel good about being able to drive the top and the bottom line. The portfolio has been pretty resilient over these years. It's got nice offensive and some defensive kind of characteristics. Overall, I feel very good about the momentum we have going into – the momentum that we have in the second half and – of this year carrying into next year and just feel good about the outlook that we've got for next year.

Q (David Roman, Goldman Sachs): A lot of focus this year has been on some of the discrete headwinds that you faced around China VBP and DRG updates, the dynamics with USAID and COVID testing. You made clear in your comments around 2026 an expectation that those headwinds start to moderate. What are some of the underlying drivers of the Diagnostics business and how will it accelerate going forward?

Mr. Ford: I don't think the dynamics that we've been talking about, David, have changed. I don't think that's a bad thing to be quite honest with you, because it just shows that we've got a handle on kind of the headwind that we've been facing, which was really the VBP in the Diagnostic area. I think one of the things I talked about, different from other VBPs that we've seen in China, is that usually if you won a VBP kind of tender, you have a price hit, but then you've got a volume kind of offset.

I think you just raised there, one of the challenges we've seen in this segment specifically is you had the price hit, which was the majority of our headwind, but you also saw some changes in the DRG model that has impacted volume a little bit also. So, I was actually in China last week. I've spent a week there. I was over there over the weekend too. I had an opportunity to really go in-depth with all the different stakeholders. I think the team has done a really good job at navigating this. I think that if you look at some of the dynamics that we're seeing in some of the accounts, we're starting to see a little bit now, some of that volume start to re-pick up. I'm not going to say that it's fully back. But I'm encouraged to see some of the signs start to pick up in terms of volume there. If you look at how that happened to us, it really started happening in Q4 of last year. So, we'll start to see a little bit of that headwind – kind of that comp start to be minimized in Q4 this year in China.

And then, next year – like I said, we've made changes. We've brought in new products, new management teams, et cetera, and I feel good about what I saw there last week, David. So, I don't think that that's changing, and like I said, I think that's not a bad thing. We'll be lapping all of that, and we're seeing nice progress there from the team too. I do think that the aspect that is changing is we are seeing our business outside of China continue to accelerate, and that's going to be the other dynamic here to be able to move our Diagnostic business from being kind of low single-digit growth to now kind of mid single-digit – mid to high single-digit growth next year.

US has done incredibly well. I give a lot of kudos to the team there. They were up 10% this quarter, and that's driven by a lot of new business capture. So, again, the portfolio is very competitive. We got a large number of new business that we acquired last year and continue to see new business converting to Abbott this year. So, I think share gains in the US is really what's driving that. European region did very well too. This quarter, I think they were up 6% – 6% to 7%, and they're doing very well also. And then, Latin America for us is growing mid-teens – consistently growing mid-teens here also.

So, I think the dynamic is not changing. So, we're not seeing the situation get worse in China, and I think the teams are doing really well there and we'll be out of that next year. And outside of China, I think the dynamics are going exactly how we've expected them to go, which is Alinity is being rolled out. It's a very competitive system. The teams are hitting their stride here in various important geographies, and like I said, I expect that to continue. So, you put that combination together, David, of passing the headwinds of the VBP in China and continue acceleration in the – on all the other geographies, I think Diagnostics is set up for a nice recovery year next year.

Q (David Roman, Goldman Sachs): In the gross margin line, there are a lot of moving parts this quarter and some foreign exchange-related dynamic. Can you talk about the operational performance in the P&L from some of those other factors and how we should think about margin trajectory on a go-forward basis?

Mr. Philip Boudreau, CFO: You touched on the right elements there. Gross margin continues to be a key area of focus for us. We've spoken in the past of the dedicated teams that we have in each of our business that drive the constant ideation and execution throughout our supply chains and operations, even our affiliates. And that's progress that we continue to make good traction on here. The step back that you referred to here in Q3 sequentially certainly reflects a normal pattern that we have more of our plant operational maintenance shutdowns that occur in the third quarter. And so, that's a normal sort of phenomenon. Also, as you touched on, the first meaningful impact of tariffs that we're feeling in gross margin is in the third quarter there as well. I would say we've done a really nice job in terms of the team that I chartered to work on tariff mitigation. And so, we continue to make good progress there and implement ideation not only on how to improve that impact going forward. But also the team is generating ideas to pass over to the gross margin expansion teams. And so, continue to feed that funnel. And I think we are kind of on track with year-to-date 60 basis points of gross margin expansion and comfortable that that pattern will continue here and kind of maintain that sort of 57% outlook in the profile going forward.

On international market, future outlook, Volt

Q (Robbie Marcus, JP Morgan): What early feedback in Europe have you received on Volt, and how people should think about the ramp in cadence of Volt and overall EP as we move into next year?

Mr. Ford: Sure. Well, we're seeing acceleration on our growth rate in EP, obviously, in the second half. We knew that was going to be the case. Second half was going to be better than the first half and 2026 will be better than 2025. I think that you've seen here double-digit growth across the board, more specifically also in our ablation catheter portfolio. So, yeah, I feel good about what we've done here, Robbie.

I mean, this idea that we've been playing defense over the last couple of years, it's actually been a [ph] quiet (00:23:36) offensive strategy, where we've used the adoption of PFA on other system – other competitive systems to increase our capital footprint. And now, we'll be in a position to bring in the catheter – the PFA catheter. It's doing very well. I just got some feedback yesterday and been following the roll-out. It's going very well. I'd say, efficacy and efficiency, those seem to be table stakes right now. PFA has proven to work and get the job done more quickly.

So, I think what I'm seeing now is longer term durability of results, safety, these are becoming quickly, I think, the point of competitive differentiation, and I think Volt is going to offer a couple areas there. I'm not the expert on all of this. But what I've heard so far has been that – two advantages that come across loud and clear for Volt is it delivers energy in a very kind of focused direction. The lesions are broader, they're deeper, seem to be more durable and minimizes the risk of hemolysis. And then, the second thing I continue to hear resounding positive feedback is the integration with EnSite is a game-changer, right.

That real-time contact visualization that we always talked about, we thought that that was going to be an important differentiation, and we're seeing that. It reduces – because you've got that real-time, we're seeing that it's reducing the amount of applications, and as a result of that, minimizing muscle contraction. And that minimization of muscle contraction allows us to then run these procedures with conscious sedation rather than exclusively with general anesthesia.

I think that's a hugely important aspect, if you look at what's going on with healthcare systems and the difficulties with general anesthesia and having that specialty ready to go at any given time. So, that gives us flexibility in a lot of European markets and in a lot of segments here in the US. So, we'll continue to roll it out internationally. And I think your timing for Volt is an okay timing for now. I mean, obviously, we're going to try and target to see an earlier approval. But for now, I think that's not a bad timing to have and – but I think what's been clear for me over these last couple of years is just the importance of the full portfolio.

And I think that Abbott's shown that it does have a full portfolio, not just of the mapping, the capital, the talent and the clinical specialists that are out in the field, but also bringing in a wide variety of different PFA tools, whether it's a one shot, whether it's going to be a focal PFA through our TactiFlex that we expect to get approval in Europe next year. And quite frankly, it's been increasingly clear to me that the companies are going to need more than just PFA. You're going to need to have PFA and you're going to need to have LAA. So – and we've got both of those. So, I don't think it's a question of Abbott being late. We're right on time, and we're complete with the full portfolio that we need. So, I expect EP to do much better in 2026 than what it did this year, and I think this year, it's done pretty well too.

Q (Vijay Kumar, Evercore ISI): When you look at overall China, inclusive of Diagnostics and MedTech and EPD franchise, can you remind us what China has done for you year-to-date, what was it last year? What is your view on normalized growth outlook for China? I'm curious to hear your view on China.

Mr. Ford: China, I was there last week, like I said. It's an important market for us, and it's going to continue to be an important market. But as the company has grown in portfolio and – its participation in our total revenue – as a percent of total revenue has come down a little bit, right. So, if you look at that China, let's say, 10 years ago, Vijay, it was probably close to like 9%, 10% of total Abbott revenue. Today, it's less than 6%. But it doesn't mean that it's not an attractive area of the world for us to continue to invest in and drive to

If you look at our EPD and Nutrition businesses, those two businesses have been up double-digits year-to-date. And the team had done a really good job there about building the portfolio and taking advantage of the growing segments there that we can offer innovation and solutions there. Our cardio neuro business has actually seen sequential growth step-up throughout this year. So, I think if you take out – the real challenge for us has been, obviously, the Diagnostic piece, and that was our – that was one of our larger businesses in China before the VBP.

So, Q3 decline was pretty much in line with what we saw in Q1 and Q2. So – but if you remove that, I'd say our growth rate in China is around 5% to 7% if you take out the Diagnostic piece. And I think that that's probably not a bad place to be in. And as we expand the portfolio there, bring in new innovations, I think that that's probably a good growth target that I look at for 2026. I don't know who you're referring to, who's talking about mid-teens. If you've got – if it's a company that doesn't have a lot of business, then – yeah, then you've got opportunities to grow your position.

We got a lot of business in China, and I think that a growth rate of mid single-digits, at least how we're planning for, is how we built our – how we're looking at our 2026, and quite frankly, as we look kind of going forward. So, I'm placing a lot more emphasis on growth contributions from other geographies. I think we've got a lot more opportunities than over here. But again, like I said, it still remains an important market for us and we're committed to it.

On Electrophysiology and PFA penetration

Q (Josh Jennings, TD Cowen): One, could you help us understand the drivers of the double-digit ablation catheter growth? Second, as the competitive environment in mapping evolves, how do you see the mapping franchise performance in 2026? Third, where does Abbott see PFA penetration in the US and OUS by the time Volt is launched globally?

Mr. Ford: For the first question, that's significantly driven by international, as you probably would have expected, Josh. So, a big driver there has been that. But we've got good growth – good mapping growth in the United States still. So, we still believe that we're – the data shows that we're still market leader in mapping cases. Obviously, with other competitors launching their mapping systems, we've seen an uptake in their mapping, in their – in the amount of cases that they're now mapping tied to their own catheters. So – but even with that, we still feel that we've got a leadership position in the amount of PFA cases that we've mapped. We have added other products also that help drive our growth there. Again, this goes back to this understanding of all the different segments in the EP area. Yes, ablation catheters are important. They're a big segment of the market, and so are Diagnostics.

But we've got other parts of the portfolio also that are driving growth. We recently launched a – our 13 French Agilis Sheath, which is viewed as one of the best introducer sheaths for not only our product, but even for competitive systems also. So, that helps also. We're launching ICE also. So, that's also a driver. So, I think, again, going back to my comment, you got to have a full portfolio here. And I think trying to pin it down to like is it mapping, is it this, yeah, I mean, obviously, we're tracking all those different segments, Josh. But we kind of view it as looking at the amount of cases that we're doing and looking at it on a revenue per case, and our revenue per case is actually going up as we're introducing more and more new products to support those cases.

So, I think your last question was about penetration of PFA. It seems like it is becoming the go-to energy source here. I think the numbers that you threw out there sound reasonable. If you think about 2026, you'll now have all four manufacturers with PFA ablation catheters with mapping systems tied to PFA ablation catheters. So, I think that number sounds reasonable to me. And then, internationally, yeah, it's a little bit less. But we'll see. We'll see what will happen. I think that Volt could actually change that dynamic internationally and maybe it can lead to a much higher penetration rate in international markets, specifically in Europe that mimics the US penetration. But that's not a bad assumption to have for now.

Q (Vijay Kumar, Evercore ISI): CRM is of your fastest-growing product line within MedTech. Can you remind us on how big is this category, the dual-chamber leadless pacemaker? Wwhere are we from a penetration standpoint? What innings are we in?

Mr. Ford: Yeah. I'm going to pick up on it's kind of crazy comment that you made. For us, it's actually taking a vision that we had, like I said in my opening comments, to change the standard of care here, make the investment. That's been done. And I think now we're seeing the benefit. It's fundamentally changed the growth trajectory of our business. I'd say, five years ago, our CRM business was flat – flat business. Then, it moved to mid single-digit, high singledigit, and then this quarter hitting double-digits.

It's pretty remarkable also, I would say, given the fact that this has historically been a low growth market. So, we're obviously taking market share. I give total kudos to the team in terms of how they went about this all the way from R&D, operations, clinical, commercial. I think they've done a really good job. And I think AVEIR is just now really hitting its stride, and we're driving uptake in both single and dual-chamber. I expect this to continue. I expect this type of performance to continue for the next few years. They've established a very large base of US physicians that are now implanting this.

I'd say, on the single-chamber, we're probably about 50% penetrated. And so, there's still room to grow there. But half of our implants so far have been dual-chamber, and we're probably sub-10% penetration over there. And those penetration rates are mostly US. So, I think there's a lot of opportunity here for us to do this and to live up to that vision.

We've got great opportunity international too. We're seeing really nice momentum in Europe and Japan. And I think the long-term aspiration here is to be able to convert a significant portion of this market. We estimate the low-voltage pacing market to be around $4 billion. We want to convert a significant portion of that, and in doing so, become the market leader in this segment. So – and the team's done a really good job, and there's pipeline, there's innovation, there's clinical work, there's investment behind it. So, I've got – it's not crazy to think about it, if you look at all the work that the team has done and put forward, and I think they're ready to capitalize on this. And they've got – they have pretty high aspirations of where they want to take their sales and their market position.

On CGM basal penetration and US adoption barriers

Q (Danielle Antalffy, UBS): We've talked in the past about CGM becoming standard of care. It surprises me that we're still only 20% penetrated in the US in basal. What do you think are still the barriers to this and how long will they persist? I mean, you talk to clinicians, and it feels like the momentum is there. Quiete frankly, we should be inflecting at this point, and I can't tell if we are. So, just curious what you think is maybe preventing that, or maybe you think we're in the inflection, I don't know. I don't want to speak for you, if you could comment on that?

Mr. Ford: Yeah. I think it's difficult to generalize. Every market that we see on the basal has gone at different speeds. If I look at some of the key European markets where we got full basal, it's actually gone, I would say, maybe at threequarters of the speed that the intensive insulin user kind of got picked up. And you're right, the US is a little bit slower. I think there is a large universe of primary care docs that needs to be covered. There's probably more awareness that needs to be built.

I know you might think, well, there's just already a lot of awareness, how come it's not ascended. But there's still a lot of pockets around this country where we're going in with our sales force for the first time, and there's a very high-level understanding of what CGM is, but there hasn't been a lot of experience. So, that's what we're working on, a lot of sampling programs. I think the work that we did – that the team did for Epic integration in a more turnkey versus every different office doing their own integration, so to have it fully integrated into Epic, I think that'll be good.

And I think the other thing that is going to be important for the primary care doc, I mean, these are very fast visits, Danielle. They don't have a lot of time. So, I think they're starting to really understand the benefit of using ambulatory glucose profiles and look at those and be able to find out where the problem is in that basal population. It's 20%. It's – there are probably pockets of the United States where I've seen higher penetration rates. But that's okay.

I think that what's important for us is that we're continuing to see an increased sustained penetration. And I think that if I were to sum it up, it's probably more dependent on us than it is about concerns about whether there's value or not value. I mean, I think the clinical data is pretty resound in terms of the benefit that it has. So, this for me is just more about us doing better, investing more, covering more physicians, and that's what we're doing.

On Nutrition performance and litigation update

Q (Joanne Wuensch, Citi): Could you give us an update on where we're sitting on the NEC litigation? It looks like there were some pockets of Nutrition that were weaker this quarter than we would have expected. And if you could just sort of address that and how you think about that going forward, that would be great

Mr. Ford: On the litigation, as I've done in the past, I'm not going to comment on any – deep into any specific cases. I think you saw – over the last couple of months, you saw some of the federal cases go through the process. In both of those cases, Abbott won on summary judgment. So, we stand behind – I mean, I'll just stand behind the products. I stand behind our label and the importance of these products in the healthcare system. So, we'll see more cases progress this year and then into next year. There's clearly a difference in terms of how the federal cases are being looked at versus maybe some of those earlier cases on the state are being looked at. But we remain committed and we'll commit to defending the product and defending the use of it going forward.

I think your other comment was pockets of softness in Nutrition. I'd say, for me, the – I think if you look at the 4% growth, it's pretty much in line with our kind of historical growth rate. I think the one that was a little bit off where we historically had been was in our – on our US pediatric. And that's – I mean, that's just competitive – a competitive impact. We gave back some share that we had captured last year when a competitor experienced a supply disruption. I knew it was going to be difficult to hold on to it, to hold on to it permanently, but still I'm disappointed that we saw that happen. And then, on top of that, we also saw a large WIC contract – state contract move from Abbott to a competitor in the quarter. So, that had an impact over there.

I expect some of these share losses here that we've seen in the US to impact our growth rate here in the US pediatric for the next couple of quarters. But what I'll say is we faced this during the supply disruption in 2022, and we got our share back. It takes a few quarters. But I'm very confident that the team will be able to do that, first, because we recently won two new WIC contracts. The combination of those two contracts actually are higher than the one that we lost, but those go into effect Q1 and Q2 of next year. And then, we've got several new product launches that we'll be launching here in the US over the next couple of quarters. So, it's going to take a couple of quarters, but I'm confident we'll be able to get our share back.

On MedTech portfolio growth drivers and M&A strategy

Q (Travis Steed, BofA): What are you thinking in terms of procedures and underlying market growth of the device business?

Mr. Ford: Yeah. I mean, I think the way our device portfolio has evolved, if you look back five, six years ago, it was a high single-digit grower, and the combination, it was really – you had double-digit growth in Diabetes, in EP, in Structural Heart, and then you had, say, about – that was about 40% of our revenue in Vascular and CRM that was relatively flat. So, the way we've done this, and I've talked about this also, is okay, how do we ensure that the high-growth areas continue to grow and accelerate, and that's what we're seeing in Structural Heart, in EP and in Diabetes, even in Heart Failure.

And then, how do we reposition what we would characterize as historically slower growth segments of a very large portion of our portfolio, how do we get them from being flat to at least growing mid single-digits. If you get them to grow mid single-digits, then you move up to double-digits. And that's what essentially has happened. If you look at our CRM business, I talked about this, it's gone from being flat to now being double-digit. That has a tremendous impact, and I think that there is a lot of sustainability in that.

In our Vascular business, we started to reposition the portfolio. I would say Vascular is on the same journey that CRM was on, maybe a year or so behind it. But we're already seeing the impact. We've been able to show pretty consistent delivery of 5% to 6% growth in our Vascular business over the last year or so. So, I think they're on their kind of journey to reposition the portfolio to higher growth. So, my expectation is it is very sustainable. We're in these very high-growth markets. We have great portfolios. We've been investing significantly and disproportionately in those programs from product development to clinical trials. And so, I think it's very sustainable.

Q (Travis Steed, BofA): How are you thinking about the portfolio over the medium-term? Do you have the right assets going forward, new markets you want to be in? At some point, are we going to see you guys kind of utilize the balance sheet and the cash?

Mr. Ford: Yeah. Well, we have been using it. We have been using it in terms of dividend and growing our dividend. We have been using it in terms of share buybacks. We've been using it in terms of debt and debt pay-down. We've got $3 billion of debt to pay down next year. And I think I prefer to pay that down when it comes due, but we'll wait to see what interest rates look like. So, we have been using it. We've been making investments – internal investments with manufacturing and some of our digital solutions.

So, yeah, I don't think that we've just been sitting on it. Obviously, we've got businesses that are very strong positive cash flow generators. On the M&A side, yeah, I talked about there being opportunities, very good opportunities out there. We've got a strong organic pipeline, which allows us to be a little bit more selective. But if there are opportunities that fit us strategically, and there are a lot of opportunities that fit us strategically, and make – and can generate an attractive return, we've got capacity to do that too. So, I like the position we're in, but we are putting our cash to use.

On Structural Heart

Q (Danielle Antalffy, UBS): On the Structural Heart piece of the business, and specifically in left atrial appendage closure and could you talk more about how you see left atrial appendage closure evolving for Abbott specifically in 2026 and beyond?

Mr. Ford: Listen, I think it's a really important area of growth. You're right. I don't think that we've taken the right amount of share with the concomitant procedure. I know that the teams are looking at how to do that more effectively as we go into beginning of next year. But this is an area that we continue to invest in.

I think that what I'm seeing right now from the results – or at least feedback that I've heard from physicians on our next-generation Amulet device is significantly positive versus what I've heard from other products that we've put into trial. So, when I get calls and text and things like that from some of the KOLs that are working on the trial, really making sure that we understand of how competitive and how good this next generation is. I think that's going to allow us to do that.

We've actually completed the enrollment of that trial. So, we're going to be filing – we got to do the follow-up, and then we'll be filing in the first half of next year. So, we'll see if this is a 2026 launch or if it's more of a 2027 launch. But I think that's going to be hugely important, and I think it's going to be hugely important as it relates to our full portfolio here. We think that it's going to be a differentiator for us to be able to have not only all the PFA tools and mapping tools and service and support, but now to be able to add a much more competitive device on the LAA side.

We've got a read-out of our trial against NOAC. That'll be in 2027. I understand that there'll be a read-out from a competitive system next year. But I think that this is a high-growth area and one that's got a lot of attention from me and from the management of our device teams on how we can kind of leverage the portfolio better. So, I've got high expectations as we go into next year and especially with the next-generation product.

Q (Suraj Kalia, Oppenheimer & Co.): Structural Heart continues to be an important segment for Abbott, and you talked about some of the new products on the horizon, balloon-expandable valves, Cephea, so on and so forth. Would love to get your thoughts specifically on the mitral and tricuspid US TAM. The landscape seems to be changing with SGLT2 inhibitors, cath lab capacity and so on. What are the puts and takes for realizing this TAM? Thank you for taking my questions.

Mr. Ford: I mean, I think there's a lot of opportunity in those two products that you just referred to. I think on the tricuspid side, I'd say what needs to be done here is continue to invest in data and data generation to be able to strengthen the referral pathways to be able to have broader adoption. I think between repair and replace, it's good to have both those tools. Right now, what I'm seeing is repair is being the preference, just given the safety profile. On the MitraClip side, we've invested in a clinical trial to look at using MitraClip in low and intermediate risk patients.

So, I think for those two products, you're going to have to continue to invest in clinical and clinical evidence. Obviously, you support that with your field-based teams, et cetera. But I think the real big drivers of and continued drivers of that are going to be clinical evidence. But I mean, I take a step back here and maybe just look at how you started your question about Structural Heart. You went quickly into those two products. But this is an area that if – in my view, if you want to be a cardiovascular and MedTech leader, you have to have a strong, robust and differentiated portfolio and strong position in Structural Heart.

If you look at the revenue across the players, we've – last year, I think we crossed over to number two. So, we have a number two position. And I don't think that's by accident. We've invested in that area. We've invested heavily in that area. We've got a portfolio of great products. You have MitraClip, TriClip. You got Navitor. You got Amulet. And you've got several – if I look at over the next couple of years, there are multiple catalysts here to sustain and even accelerate this double-digit growth that we got, whether it's label expansions in Navitor, MitraClip. We launched our fifth-generation MitraClip and TriClip product. That's important.

We've seen guideline changes happen. You saw some of that guideline change happen in the European conference about a month ago. Expanding the product and the technologies to other markets. I think the launch of TriClip in Japan is going to be a real important move for us. We've done some bolt-on M&A in this space also. This quarter, we actually bought an AI-powered imaging software company in Europe that specialize in interventional cardio pre-procedure planning. I think that's going to be hugely important in this space. So, we've added to that and integrating that team into our programs.

And then, the pipeline, like you said, whether it's balloon TAVR, Amulet – our next-generation Amulet and our mitral replacement valve, I think those are all – I've actually been pretty close – I've been closer to the mitral replacement program recently. And the feedback that I've heard from this product is just spectacular, and I think it's got the potential to live up to the expectations that we all had back in 2015 when all of us made significant investments in buying early assets and – with the belief that mitral could be as big as TAVR. I think that this is the product that's going to – it's got the potential to fulfill that promise.

So, I put all that together, I think that wSuree're in a tremendously competitive position in Structural Heart. The portfolio is very complete, and we're going to continue to invest in it and be a leader here. So, I feel good about that part of our MedTech portfolio and be able to kind of sustain that double-digit growth going forward, so.

Close Concerns’ Questions

- How does leadership expect Epic EHR integration and expanded sampling programs to accelerate US basal and primary care adoption of FreeStyle Libre in 2026? What additional investments might be required to close the gap between US and European CGM basal-only penetration rates?

- Are there trends in the characteristics of the US “pockets” that still face significant basal-only T2D underpenetration?

- Given ongoing tariff and foreign exchange headwinds, what operational or manufacturing levers is Abbott prioritizing to uphold full-year organic-sales guidance?

- When in 2026 does Abbott expect the DGK to launch, and what are the company’s expectations for initial uptake?

- Does Abbott have plans to offer a lactate sensor in conjunction with its cardiac device offerings? How might these interact, if at all?

- How has demand for Abbott’s BGMs fluctuated in the US and internationally?

--by Riya Chatterjee, Jeremy Alkire, Nour Khachemoune, Monica Oxenreiter, and Kelly Close

[1] This compares to 96% in 2Q25, 93% in 1Q25, and 97% in 1Q24 and 4Q24 – the “balance” of the revenue was BGM.

[2] We are not sure the degree to which this groups feels they need CGM – while insulin is prompting hypoglycemia and the perceived and real need for CGM, we are not sure how much those on GLP-1 and SGLT-2s feel they need CGM. From our view, they need for CGM to fight hyperglycemia is huge.

[3]This revenue is approximately 3% of the overall Diabetes Care division. We note that this estimation is due to rounding in Abbott’s CGM revenue, as the company reports CGM revenue rounded to two figures ($2.0 billion) in its press release. Therefore, our estimation assumed exactly $2.o billion in CGM revenue; if actual FreeStyle Libre revenue is over $2.0 billion, even slightly, our BGM estimate overestimates Abbott’s “true” BGM revenue in the quarter. The continued decline likely reflects the structural shift away from BGM toward CGM adoption.