AZ 4Q25 – Farxiga sales total $2.1 billion (+2% CER), with LOE expected in 2026; Farxiga + baxdrostat combination therapy to launch in 2026; oral GLP-1 RA to enter phase 3 –

Executive Highlights

- AstraZeneca reported its 4Q25 and full-year results this morning in a call led by CEO Mr. Pascal Soriot – see the press release, presentation slides, clinical trials appendix, and webcast.

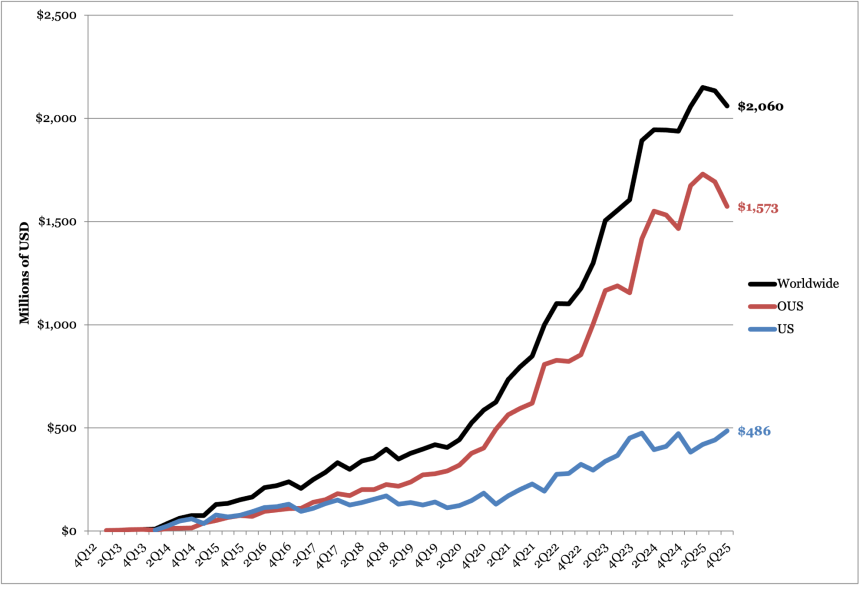

- In 4Q25, sales of AZ’s SGLT-2 inhibitor Farxiga (dapagliflozin) totaled $2.1 billion, up 2% CER from 4Q24 and down 4% sequentially. OUS sales comprised 76% of global revenue and totaled $1.6 billion (up $107 million from 4Q24; +7% CER YoY, -7% Q/Q), while US sales totaled $485 million (up $14 million from 4Q24; +3% CER YoY, +10% Q/Q). In 2025, revenue was $8.4 billion, up 9% from 2024. Management attributed this modest growth to strong demand in Europe and in emerging markets ex‑China, partially offset by loss of exclusivity in the UK and temporary volume-based procurement stocking in China. Farxiga will lose exclusivity in the US in 2026. This projected impact has been incorporated into guidance. We are curious the degree to which just less expensive pricing (ASP = average selling price) in the US would factor into the lower revenue – this seems logical to us.

- Farxiga is being investigated as part of combination therapies in multiple phase 3 trials. Results from the phase 3 MIRO-CKD trial (with nonsteroidal mineralocorticoid receptor modulator balcinrenone[1], now recruiting for phase 3 trials for heart failure with impaired kidney function as part of the BalanceD-HF trial), as well as the Bax24 trial (with aldosterone synthase inhibitor baxdrostat[2], the high-profile drug for difficult-to-treat hypertension), were presented in 4Q25. Baxdrostat’s launch is expected in 2026.

- In incretin therapies, excitingly, the once-daily oral GLP-1 RA elecoglipron (AZD5004), met its primary endpoints in both the phase 2b VISTA (n=310; for obesity) and SOLSTICE trials (n=406; for T2D). The company will advance the candidate into phase 3 development this year. In addition, phase 2 results of multiple obesity candidates are expected in 2026:

- AZD6234 (a long-acting amylin analog). The company reaffirmed that data from the phase 2b APRICUS trial (n=262; for obesity) and the phase 2 ARAY trial (n=64; for overweight or obesity and T2D taking GLP-1 RA) are expected in 1H26 and 2H26, respectively.

- AZD9550 (a dual GLP-1/glucagon RA). Data from the phase 2b ASCEND trial (n=360) of the combination therapy of AZD9550 and AZD6234 is expected in 2H26. The trial was initiated in 1Q25 for adults with obesity or overweight with at least one weight-related comorbidity.

- In MASH, data for the phase 1 CONTEMPO (n=118) trial investigating AZD9550 (dual GLP-1/glucagon RA) in adults with overweight or obesity is now anticipated in 2027, slightly delayed from 2H26.

- In PCSK9 inhibitors, namely laroprovstat (AZD0780), phase 3 trials are ongoing with data expected in 2027.

[1] As a mineralocorticoid receptor modulator, balcinrenone binds to mineralocorticoid receptors and aims to reduce inflammation and fibrosis in the heart and kidneys without the high risk of potassium elevation (hyperkalemia) associated with traditional mineralocorticoid receptor antagonists.

[2] Baxdrostat is a highly selective aldosterone synthase inhibitor designed to lower blood pressure by reducing the production of aldosterone, a hormone that causes salt and water retention.

Table of Contents

- Financial Highlights

-

Pipeline Highlights

- 1. Oral GLP-1 RA elecoglipron to enter phase 3 development in 2026 for obesity and T2D; multiple data readouts for obesity candidates expected in 2026

- 2. Farxiga + baxdrostat combination to launch in 2026, following positive phase 3 results

- 3. Multiple MASH candidates in phase 1 and 2 development

- 4. Oral PCSK9 inhibitor laroprovstat (AZD0780) phase 3 trials ongoing with data expected in 2027

- 5. Full speed ahead on manufacturing plans in the US!

- Close Concerns’ Questions

- Analyst Q&A

Financial Highlights

1. Farxiga sales total $2.1 billion (+2% CER) in 4Q25 and $8.4 billion (+9%) in 2025; loss of exclusivity in the US expected in 2026

SGLT-2 inhibitor Farxiga (dapagliflozin) revenue totaled over $2 billion for the fourth consecutive quarter, up 2% CER from 4Q24 and down 4% sequentially. US sales totaled $485 million, up 3% CER from 4Q24 and up 10% sequentially. OUS sales, which comprised 76% of global revenue, totaled $1.6 billion, up 7% CER from 4Q24 and down 7% sequentially. In 2025, Farxiga totaled $8.4 billion, up 9% from 2024. In the US, annual revenue totaled $1.7 billion (-1%), and OUS revenue totaled $6.7 billion (+12%). Management attributed this modest growth to strong demand in Europe and in emerging markets ex‑China, partially offset by loss of exclusivity in the UK and temporary volume-based procurement stocking in China. While revenues in the US, Japan, and China are expected to decline in 2026, AZ anticipates strong demand growth to continue in Europe and in emerging markets. Farxiga captured 46% of the SGLT-2 inhibitor market, following BI/Lilly’s Jardiance (empagliflozin) which captured 51% in 4Q25.

- In the US, the company will lose exclusivity for Farxiga in April 2026. Management flagged that the Most Favored Nation deal will be a headwind for AZ in 2026 and emphasized that it is already embedded in guidance and is manageable given the franchise’s scale. In addition, the first round of the Medicare Drug Price Negotiation Program (MDPNP), which lowered AZ’s SGLT-2 Farxiga’s price by 68%, took effect in January 2026.

Farxiga Worldwide Financial Results

| Farxiga | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue (Millions) | $1,938 | $2,057 | $2,150 | $2,134 | $2,060 | $8,401 |

| YOY Reported Growth (CER) | +21% (+22%) | +9% (+17%) | +11% (+24%) | +10% (+8%) | +6% (+2%) | +9% (+9%) |

| Sequential Reported Growth | Flat | +6% | +5% | -1% | +10% | -- |

Farxiga 4Q25 Geographic Financial Results

| Farxiga | Revenue (Millions) | YOY Reported Growth | Sequential Reported Growth |

| US | $486 | +3% | +10% |

| OUS | $1,573 | +7% | -7% |

| Total | $2,060 | +6% | +10% |

Pipeline Highlights

1. Oral GLP-1 RA elecoglipron to enter phase 3 development in 2026 for obesity and T2D; multiple data readouts for obesity candidates expected in 2026

On today’s call, management discussed various clinical trial updates:

- Elecoglipron (AZD5004, oral GLP-1 RA). Dr. Sharon Barr (EVP, Biopharmaceuticals R&D) shared that once-daily oral GLP-1 RA elecoglipron met its primary endpoints in both the phase 2b VISTA (n=310; obesity) and SOLSTICE (n=406; T2D) trials. The full data readout for the phase 2 trial is expected in 1Q26. The company will advance the candidate into phase 3 trials this year.

- AZD6234 (long-acting amylin analog). Management reaffirmed that data from the phase 2b APRICUS trial (n=262; for obesity) and the phase 2 ARAY trial (n=64; for people with overweight or obesity and T2D taking GLP-1 RA) are expected in 1H26 and 2H26, respectively.

- AZD9550 (dual GLP-1/glucagon RA). Data from the phase 2b ASCEND trial (n=360) of the combination therapy of AZD9550 and AZD6234 is expected in 2H26. The trial was initiated in 1Q25 for adults with obesity or overweight with at least one of the following weight-related comorbidities: (i) hypertension; (ii) dyslipidemia; or (iii) obstructive sleep apnea. In 3Q25, Dr. Barr said that there is a potential for market segmentation within the company’s obesity portfolio, including AZD5004, AZD6234, and AZD9550.

2. Farxiga + baxdrostat combination to launch in 2026, following positive phase 3 results

Farxiga is being investigated as a combination therapy in multiple phase 3 trials with baxdrostat (an aldosterone synthase inhibitor), balcinrenone (a non-steroidal selective mineralocorticoid receptor modulator), and zibotentan (a selective endothelin A receptor agonist). In 4Q24, Mr. Soriot highlighted the need for combination therapies given that many patients have kidney disease due to hypertension (40%), diabetes (40%), and other causes (20%).

- Farxiga + baxdrostat: Three trials are ongoing to evaluate the combination of baxdrostat and Farxiga versus Farxiga monotherapy:

- (i) BaxDuo-Arctic trial (n=2,554). In March 2024, AZ initiated the phase 3 BaxDuo-Arctic trial (n=2,554), examining Farxiga in combination with baxdrostat versus Farxiga monotherapy in people with CKD and high blood pressure. The study is now expected to be completed in February 2028, delayed from December 2027. The primary outcome will be a change in eGFR from baseline to two years.

- (ii) BaxDuo-Pacific trial (n=5,000). AZ initiated this trial in 1Q25, investigating Farxiga with baxdrostat versus Farxiga monotherapy in people with CKD and high blood pressure. The primary outcome is the time to first renal composite event, and results are expected in 2027.

- (iii) PREVENT-HF trial (n=11,300). AZ added the phase 3 PREVENT-HF trial (n=11,300) in 1Q25, examining Farxiga in combination with baxdrostat versus Farxiga monotherapy in people with T2D, a history of hypertension, established CVD, and CV risk factors. The primary endpoint will be time to CV death or first heart failure event, with results expected in 2027.

- As background, Baxdrostat was added to AZ’s pipeline following the company’s February 2023 acquisition of CinCor Pharma. Results from the BaxHTN trial were presented at ESC 2025 and simultaneously published in NEJM, demonstrating significant reduction in systolic blood pressure in people with uncontrolled hypertension. The Bax24trial, presented at AHA 2025, showed that baxdrostat significantly lowered 24-hour systolic blood pressure by 14 mmHg at Week 12 in people with difficult-to-manage hypertension. On today’s call, Mr. Ruud Dobber (EVP, Biopharmaceuticals) stated that the company is preparing an NME launch of baxdrostat in 2026 for difficult-to-treat hypertension.

- Farxiga + zibotentan: This combination therapy is being investigated in a phase 3 trial for CKD and high proteinuria. Initiated in 4Q23, the phase 3 ZENITH High Proteinuria trial (n=1,835) is evaluating Farxiga in combination with zibotentan versus monotherapy in adults with CKD and high proteinuria. The primary outcome is the change in eGFR from baseline to two years. Adults with T1D are excluded from the trial. The trial is expected to be completed in January 2027.

- In 2Q23, the phase 2 ZENITH-CKD study showed significant and clinically meaningful reductions in UACR at 12 weeks compared with dapagliflozin alone. After 12 weeks of treatment, the UACR difference of zibotentan/dapagliflozin versus dapagliflozin alone was 34%.

- Farxiga + balcinrenone: AZ is investigating this combination in the phase 2b MIRO-CKD trial (n=324) for CKD and a phase 3 BalanceD-HF trial (n=4,800) for HF and impaired renal function.

- Completed in 2Q25, the phase 2b MIRO-CKD trial (n=324) investigated Farxiga in combination with balcinrenone in adults with CKD and albuminuria. The primary endpoint is the change in UACR values from baseline to 12 weeks. People with T1D or uncontrolled T2D are excluded from the trial. The trial found that at Week 12, the reduction in UACR versus dapagliflozin alone was 22.8% for balcinrenone 15 mg plus dapagliflozin 10 mg, and 32.8% balcinrenone 40 mg plus dapagliflozin 10 mg.

- The phase 3 BalanceD-HF trial (n=4,800) for Farxiga in combination with balcinrenone in adults with heart failure and impaired renal function is currently recruiting. Completion is expected in June 2027, with initial data anticipated in 2027, delayed from 2026. The primary outcome will be a composite of CV death, HF hospitalization, and HF event without hospitalization at 38 months. People with T1D are excluded from the trial.

3. Multiple MASH candidates in phase 1 and 2 development

AZ’s pipeline features multiple candidates in phase 1 or 2 for MASH, including for liver cirrhosis, the most severe stage of fibrosis. There are currently no therapies available for liver cirrhosis. See the table below for a summary.

Drug (mechanism) | Trial | Study population | Primary endpoint | Trial status |

AZD9550 (dual GLP-1/glucagon RA) | Phase 1 CONTEMPO(n=118) | Adults with overweight or obesity with or without T2D | Safety, tolerability, and PK parameters | Data anticipated in 2027 |

AZD2389 (anti-fibrotic mechanism) | Phase 2 BORANA(n=40) | Adults with liver fibrosis and compensated cirrhosis | Safety and tolerability | Data anticipated in 2H25 |

zibotentan/dapagliflozin (endothelin A receptor antagonist/SGLT-2 inhibitor) | Phase 2 ZEAL(n=195) | Adults with cirrhosis with features of portal hypertension | Change in hepatic venous pressure gradient (HVPG) | Trial discontinued due to efficacy as of 2Q25. Data readout in 2Q25. |

AZD2693 (PNPLA3 ASO) | Phase 2b FORTUNA(n=220) | Adults with MASH and who are carriers of the PNPLA3 148M risk allele | Efficacy, safety, and tolerability | Trial discontinued due to efficacy in 3Q25. |

Mitiperstat (MPO inhibitor) | Phase 2 COSMOS(n=90) | Adults with MASH | Safety, tolerability, PD parameters | Trial discontinued as of 4Q24 due to “strategic portfolio prioritization” |

Source: AstraZeneca

4. Oral PCSK9 inhibitor laroprovstat (AZD0780) phase 3 trials ongoing with data expected in 2027

As of 2Q25, AZ has initiated three phase 3 clinical trials for laroprovstat (AZD0780). At JPM 2026, Dr. Aradhana Sarin (CFO) said that laroprovstat holds great potential because it is a once-daily, small molecule therapy with no fasting or food restrictions.

- AZURE-LDL (n=2,800) will evaluate LDL-C reduction in patients with dyslipidemia and a history of clinical ASCVD or who are at risk of a first ASCVD event. Data is anticipated in 2027.

- AZURE-Outcomes (n=15,100) will evaluate the time to first event of any component of MACE-Plus, a composite endpoint that includes death, myocardial infarction, stroke, revascularization, heart failure, and thromboembolic events. Patients included will either have dyslipidemia and established ASCVD or will be at high risk of a first ASCVD event. Data is anticipated in 2027.

- AZURE-China (n=360) will evaluate pharmacokinetic parameters of AZD0780 in Chinese adults with dyslipidemia. Data is anticipated in 2027.

No further updates on this clinical trial program were offered in today’s remarks.

5. Full speed ahead on manufacturing plans in the US!

On the manufacturing front, in 2Q25 AZ said that its planned multi-billion-dollar US manufacturing facility will produce therapeutics such as its oral GLP-1 RA, its PCSK-9 in development, laroprovstat, and combination small molecule products. This facility is part of AZ’s $50 billion US investment plan announced in July 2025.

Close Concerns’ Questions

1. How does AZ envision segmenting its obesity portfolio across elecoglipron, AZD6234, and AZD9550, particularly given differing mechanisms and the various expected readouts in 2026?

2. While some may see a landscape dominated by incretin-based therapies, others see enormous value in SGLT-2 inhibitors, especially given their impact on both heart failure and chronic kidney disease. How does AZ envision the role of SGLT‑2 inhibitors in a future diabetes algorithm once SGLT-2 inhibitors are even more accessible and affordable? How does it think about combination therapy and related accessibility for people most in need who can benefit?

3. How does AstraZeneca feel about the “staging type 2 diabetes” future, as written recently about by Dr. Rich Bergenstal (IDC) and Dr. Viral Shah (Indiana University) et al.?

4. How is AZ preparing for potential most favored nation[1] (MFN) expansion to other cardiometabolic classes, including future oral incretins?

Analyst Q&A

On Farxiga

Q (Rajan Sharma, Goldman Sachs): I just wanted to focus on the growth drivers in 2026 outside of Oncology. Do you think the BioPharma business can grow through the Farxiga LOE? Just thinking about the guidance for 2026 at the group level, what has to go right to get to the upper-end of that guidance and when do we get visibility on those factors?

A (Ruud Dobber, EVP, BioPharmaceuticals): First of all, the Respiratory & Immunology portfolio is growing very fast. It was already $9 billion in the course of 2025. There's no reason to believe that products like Breztri, potential also with asthma, or as said in my prepared remarks, products like Tezspire, Fasenra are not growing anymore at double-digit moving forward. So that is a very important growth driver, not only in the United States and Europe, but also clearly in the international markets. So that's one big ticket item.

The other one is clearly that hopefully, we will see the approval of baxdrostat in the course of this year as an approval. That of course will not immediately generate substantial sales in the course of 2026. It's a highly dominated Part D population, but based on all the market research, we truly believe that this product has a multibillion-dollar opportunity as well.

If you see our internal forecasts, yes, we will have a blip for sure regarding the Farxiga LOE, but there are enough other growth drivers in order to compensate and potentially to exceed the growth moving forward. So we are quite bullish in our internal forecasts regarding the forecast for the BioPharma business.

On oral GLP-1 RA elecoglipron

Q (Matthew Weston, UBS AG): On elecoglipron, you've made the announcement that you're moving to phase 3, which I assume indicates confidence in the phase 2 profile that you've seen. But I could read that two ways because you also have a unique target product profile because you're looking about weight management in combination with other parts of your cardiovascular portfolio. So can you make some comments as to whether or not being confident to drive that move to phase 3 means that you think you have efficacy at least as good or better than the competition? Or whether or not you think that it meets your target product profile of at least achieving modest weight loss, which you can then use in combination with other agents?

A (Pascal Soriot, CEO): Let me just answer this one because it's easy to answer actually is we would never move a product in phase 3 and unleash the kind of spend we have – we are committing to if we didn't think we have a product with a competitive profile. So the short answer to your question is we believe we have a very competitive profile, and it doesn't rely on combinations. It actually relies on the monotherapy itself, and of course, combination comes on top. But if monotherapy was not competitive, it would be hard to move it into phase 3 and unlock so much investment.

On obesity

Q (Stephen Michael Scala, TD Cowen): A general question: a hellaciously competitive market of undifferentiated products, which isn't growing very much despite huge awareness, doesn't strike me as the type of market AstraZeneca pursues aggressively. Obesity could be described as that, and you are not only involved, but are increasing exposure. What am I missing? Are you assuming that fundamentals improve, that pricing stabilizes and increases, that strong growth will resume? I know that you're pursuing combos, but value-added products launched into a tough market would strike me as a high probability path to success.

A (Ruud Dobber, EVP, BioPharmaceuticals): It's a fair question. First of all, we truly believe that the market in itself is still quite immature. Yes, injectables have their place, and the first oral moving in, but there's still so much improvements possible. Combination therapies for people with obesity or overweight is very crucial in order to help those patients to reduce their risk of cardiovascular events. So that's one big ticket item.

Second part is that those products are still not very much used in, let's say, the international markets. If you look at the success of Farxiga, a big part of the success of Farxiga across the three indications is that we have a very large footprint in the international markets. So, there's clearly room to maneuver.

The third piece is that we are doing a lot of research and development work regarding the quality of weight loss. Yes, it's not only about the percentage of weight loss, but also are you able to preserve lean muscle, yes or no? Are you able to attach or attack the bad fat, the visceral fat? So I think there are still an enormous amount of possibilities to move to the next generation of anti-obese medicines.

I truly believe that AstraZeneca is one of those companies well equipped in order to address those questions. We have an excellent development and discovery team. You have seen our excitement of the deal we made last week with CSPC, which gives an opportunity to move in long-acting medicines. There's still so much to win in this marketplace. we are keen to play an important role in that.

Q (Rajesh Kumar, HSBC Bank): You've gone to obesity at a time where almost no one is sure whether this market has the same kind of growth and every player is going in. So, if you keep going organically into different segments, you might run out of ideas. So how are you thinking about that problem in terms of reallocation of capital, share buyback or future investments?

A (Pascal Soriot, CEO): So let me make a general comment, and then Aradhana can make more specific comments about capital allocation. One thing I would add to what Ruud said about oral GLP-1 and others is cardiometabolism is going to be – is today the biggest issue mankind is facing. We are in the early phase of this transformation, and the way we can actually tackle this disease, if you want. Beyond GLP-1, you also have SGLT2, and I really believe in the oral segment. Combining those two is going to make a huge difference to how people are treated. The foundation treatment of many of these people should be GLP-1 and SGLT-2; protect the kidneys, the heart, reduce weight, improve metabolic status. Beyond that, we have other mechanisms, of course. So, this is going to remain – I mean it is looking very crowded, but it is also a huge issue for medicine. Over time, things will settle down because not everybody will succeed in this market. We have the pipeline, we have the R&D strengths, in particular development strengths, and we have the commercial network and the manufacturing network to manufacture those products and commercialize them around the world. So, it will continue to be an important issue to tackle from a medical viewpoint. It will be a driving growth for us, a driver of growth, and will become profitable as soon as we can get to scale. In term of general question about capital allocation…

A (Aradhana Sarin, CFO): The $80 billion ambition was on an organic basis. That does not assume any M&A of any size and scale. We're on track to achieve that. We do have substantial firepower. We're very comfortable at 1.2 times leverage. But we have plenty of capacity. That being said, we remain very disciplined in terms of what type of assets we bring in because it's not about just buying assets. It's about actually creating value for shareholders from those assets that we acquire. And that requires substantial investments in R&D once we acquire those assets or license those assets, et cetera. So, again, we are very disciplined in how we do that and we need to continue to add value. On your question of beyond 2030, that's why Pascal highlighted all – I mean, if you look at our R&D expense, a substantial portion of that, I wouldn't say the majority, but a substantial portion is going actually in assets which won't have any substantial revenue in 2030. So, that's all the investment for beyond 2030 to continue the growth rates, because we know in that timeframe, there are going to be substantial LOEs.

A (Pascal Soriot, CEO): If you look at it, we are in a good position. We don't have to go after phase 3 assets that are proven and cost a fortune and you pay upfront, which you're going to get later. We really try to focus our BD activities on earlier assets, where we can add value and create shareholder value because we don't need products immediately. We need to invest for the future. So our strategy really has been to build our pipeline, of course, and add to it, but through earlier BD investments and then add value over time. So, that's really our strategy. As you said, we have a good capacity in term of raising debt, if we wanted to. But we also have to absorb all these products in our P&L, right. So, it's not only a question of cash; a question of P&L, too, and a question of focus. We have a very broad portfolio, but within this, we need to stay focused on what our key priorities are.

On guidance and growth strategy beyond 2030

Q (Luisa Hector): On growth beyond 2030, it does connect to the readouts in 2026. You talked about the $10 billion risk adjusted peak sales potential. Can you give us any more color on that, the mix of the $10 billion, the risk adjustments you've assumed, any assets in particular dominating the $10 billion? Should we assume higher success rates now for AstraZeneca after last year's strong performance? So that's the readouts this year and the link to the growth beyond 2030.

A (Pascal Soriot, CEO): [On the second question,] I wish that we continue experiencing the same success rate, but I don't think we can promise this because, as you know, the risk is part of our industry really, and we have to embrace and brace for the fact that we actually will experience failures. Now, having said that, we are working together with Tempus on and using AI and multimodal model to actually help improve the probability of success in our studies and better shape them [for oncology].

A (Ruud Dobber, EVP, BioPharmaceuticals): A few highlights from a BioPharma perspective. For laroprovstat, our oral PCSK9, we're going to expect the first data set in the course of 2027 is, in our view, a very high potential, with $5 billion+ potential. Clearly, baxdrostat. I'm sure there are many more questions about baxdrostat. It's not only the mono component, but also the combination with SGLT-2 inhibitor dapagliflozin is a very important one. And then the other two combinations, balcinrenone (mineralocorticoid receptor modulator) and dapagliflozin in kidney disease and heart failure is where there's high medical needs. And the combination of zibotentan with dapagliflozin has a sales potential between $3 billion and $5 billion. So there are a couple of big products.

On China

Q (Mattias Häggblom, Svenska Handelsbanken AB): I'm curious to hear how you think about AstraZeneca's competitive advantage from an in-licensing or M&A point of view, given you have two sites in China when committing for assets with a competitor who does not have R&D on-site in China.

A (Pascal Soriot, CEO): I'm absolutely convinced we need to be in China to partner with Chinese companies, but also to compete and learn. Learn to compete with them and how they compete, not only commercially, but mostly from an R&D perspective. Because the world has changed and they are increasingly becoming a fundamental part of innovation in our industry. Some of them, at some point, will become global companies. So it's fundamental for us to be there.

We have quite a good position to do this. We have two R&D centers. We have a strong position, strong profile in China. A few of the deals we've made, we were able to make because people wanted to work with us. With the recent deal we made, I know that someone else wanted to pay more money. But the company wanted to work with us. So that relationship we build with local Chinese companies over time and our reputation and our focus and the focus they know that we have on a few limited diseases have really helped us secure a number of deals over the last few years.

Now, what happens, though, is the cost, the price. The price of these is going up, right? That's why after COVID and when the country reopened, we quickly went there. We've done quite a number of deals over the last few years at reasonable prices and it's becoming more difficult because everybody is going there. But yes, I continue to think we have a good position. We can leverage our position in China, but we will have to remain disciplined because there's competition for deals and the price – prices are going up, and of course, we have to stay focused on what we are doing.

-- by Kayla Mathieu, Kat Moon, Nour Khachemoune, and Kelly Close

[1] President Trump’s MFN rule refers to his push to mandate pharmaceutical companies sell prescription drugs in the US at prices no higher than the lowest prices offered in other developed nations.