Lilly 3Q25 – D+O sales total $13.1 billion (+77%), driven by Mounjaro and Zepbound; 2025 revenue guidance raised by over $2B; pipeline updates on orforglipron and retatrutide –

Executive Highlights

- Lilly presented its 3Q25 update today in a call led by CEO Mr. Dave Ricks and CFO Mr. Lucas Montarce – see press release, webcast, presentation slides, 10-Q, and financial workbook.

- Overall sales for diabetes and obesity portfolio totaled $13.1 billion, up 77% from 3Q24 and up 16% sequentially. US revenue accounted for 67% of global revenue, slightly down from 75% in 3Q24 and 74% in 2Q25 – reflecting significant increase in OUS revenue. Specifically, US sales totaled $8.9 billion, up 61% from 3Q24 and up 6% sequentially, while OUS sales totaled $4.1 billion, up over 2.3x from 3Q24 and 45% sequentially. Growth was mainly driven by strong Zepbound and Mounjaro performance.

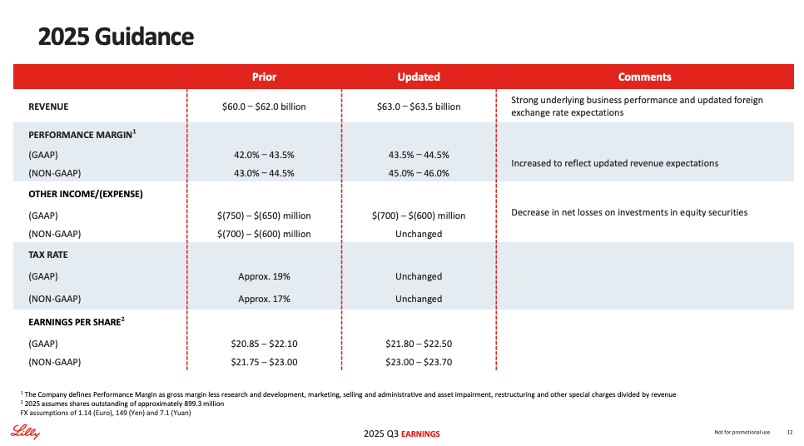

- Lilly raised 2025 revenue guidance by over $2 billion by mid-point from $60-$62 billion to $63-$63.5 billion, given strong business performance and favorable impact of foreign exchange rates. This increase follows the updated expectations in 2Q25, when Lilly increased the revenue guidance from $58-$61 billion to $60-$62 billion.

- Mounjaro (tirzepatide for T2D in the US; tirzepatide for T2D and/or obesity OUS) sales totaled $6.5 billion, up over 2x from 3Q24 and up 25% sequentially. Mounjaro maintained its leadership in the incretin-based therapy market for T2D in the US, where revenue was $3.6 billion, up 49% from 3Q24 and up 8% sequentially. OUS sales totaled $3.0 billion, up over 4x from 3Q24 and up 56% sequentially, with growth driven by strong uptake, especially in China, Brazil, Mexico, and India. Mounjaro is now launched in 55 countries in all major markets. Reimbursement for obesity drugs remains limited in OUS markets. Currently, ~75% of OUS revenue is from people with obesity paying out of pocket, while 25% is from T2D.

- Zepbound (tirzepatide for obesity) sales totaled $3.6 billion, up nearly 3x from 3Q24 and up 6% sequentially. As Zepbound is only commercialized in the US, Canada, and Japan, US sales comprised over 99% of global sales with $3.6 billion in revenue. Management attributed US sales growth to higher demand, partially offset by lower realized prices. For the third consecutive quarter, Zepbound led the obesity market, capturing 63% of total prescriptions (TRx) and 71% of new-to-brand prescriptions (NBRx) at the end of 3Q25. Zepbound vials comprised nearly 30% of TRx and over 45% of new prescriptions in 3Q25. On the clinical development, tirzepatide is evaluated for weight maintenance, adolescents with obesityor overweight, T1D, and chronic kidney disease.

- In the pipeline, CSO Dr. Daniel Skovronsky reviewed clinical updates on orforglipron, a once-daily oral GLP-1 RA, and retatrutide, triple GLP-1/GIP/glucagon RA.

- Several phase 3 data for orforglipron were presented in 3Q25, including full results of ATTAIN-1 and topline results of ATTAIN-2, ACHIEVE-2, ACHIEVE-3, and ACHIEVE-5 trials. With the completion of ATTAIN-2, filings for obesity are set to begin imminently, with a launch expected in the coming year. For T2D, regulatory submission is expected by 1H26, pending ACHIEVE-4 trial results.

- For retatrutide, management updated that up to six phase 3 results will be available by 2026. Dr. Skovronsky shared that retatrutide will deliver greater and more rapid weight loss compared to existing obesity medicines, and will likely be suitable for patients with a very high BMI or those with obesity-related complications that require a high degree of weight loss, suggesting market segmentation.

- As well, Lilly launched several phase 2 and 3 trials evaluating brenipatide, an injectable dual GLP-1/GIP RA, for asthma in phase 2 and alcohol use disorder in phase 3.

- R&D expenses increased 27% to $3.5 billion, or 20% of revenue. To bolster drug discovery efforts, Lilly has also announced in October 2025 a collaboration with NVIDIA to build a supercomputer that would power its “artificial intelligence (AI) factory,” a computing infrastructure that manages data processing, storing, and training. In September, Lilly announced plans to invest $5 billion in Goochland County, Virginia, for antibody-drug conjugate platform and monoclonal antibody portfolio for cancer and autoimmune diseases and $6.5 billion in Houston, Texas, to manufacture small-molecule therapeutics, including orforglipron. Lilly will also invest $1.2 billion in Puerto Rico facility to boost oral medicine manufacturing.

3Q25 Financial Results for Lilly’s Major Diabetes and Obesity Products

Product 3Q25 Revenue (millions) YOY Reported Growth Sequential Reported Growth Mounjaro $6,515 +109% +25% Trulicity $1,052 -19% -4% Jardiance/Glyxambi (royalty for Lilly) $959 +40% +39% Humalog $599 +12% +19% Humulin $177 -15% +1% Basaglar $162 flat +12% Zepbound $3,588 +185% +6% Tradjenta (royalty for Lilly) $71 -22% +22% Total Diabetes $13,118 +77% +16%

Table of Contents

-

Financial Highlights

- 1. D+O portfolio sales total $13.1 billion (+77%), driven by Mounjaro and Zepbound; 2025 revenue guidance raised again to ~$63 billion

- 2. Zepbound (tirzepatide for obesity) sales total $3.6 billion, up nearly 3x; new-to-brand prescriptions rebounds after CVS formulary exclusion

- 3. Mounjaro sales total $6.5 billion (+2x); 75% of OUS revenue from self-pay patients with obesity

- 4. Trulicity (dulaglutide) revenue totaled $1.1 billion (-19%), continuing a downward trend

- 5. Jardiance (empagliflozin) sales totals $959 million (+40%), including a $200 million milestone payment

- 6. Humalog revenue totals $599 million (+12%); biosimilar competition expected to increase

- 7. Basaglar sales totals $162 million, consistent with previous quarters

- 8. DPP-4 inhibitor Tradjenta revenue totals $71 million (-22%)

-

Pipeline Highlights

- 1. Topline results of phase 3 ATTAIN-2, ACHIEVE-3, and ACHIEVE-5 trials of orforglipron; new ATTAIN-OA PAIN and RESTRAIN-SUI trials initiated

- 2. First phase 3 results on retatrutide expected by the end of 2025; retatrutide to fill a distinct clinical segment with very high BMI or obesity-related complications

- 3. Lilly Diabetes-Related Pipeline Summary

- Close Concerns’ Questions

- Analyst Q&A

Financial Highlights

1. D+O portfolio sales total $13.1 billion (+77%), driven by Mounjaro and Zepbound; 2025 revenue guidance raised again to ~$63 billion

Sales for the diabetes and obesity portfolio totaled $13.1 billion in 3Q25, up 77% from 3Q24 and up 16% sequentially. US revenue accounted for 67% of global revenue, slightly down from 75% in 3Q24 and 74% in 2Q25 – reflecting significant OUS revenue growth.

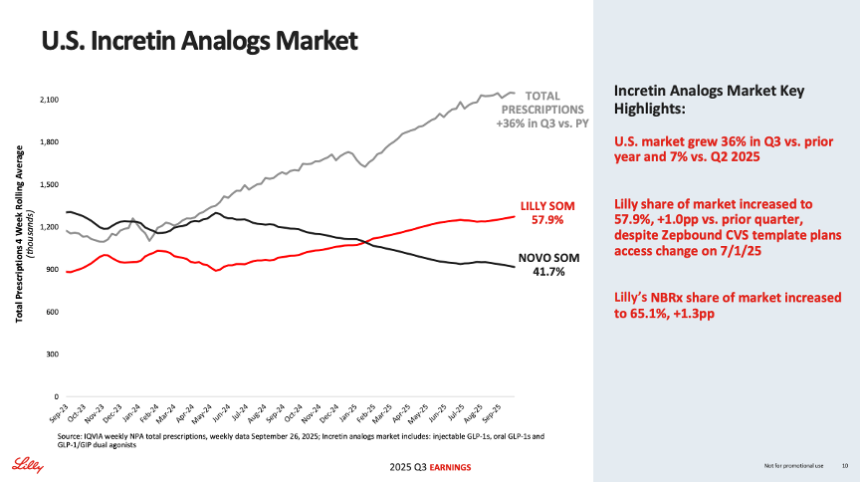

US sales totaled $8.9 billion, up 61% from 3Q24 and up 6% sequentially. Growth was attributed to 60% increase in volume, partially offset by a 15% decrease due to lower realized prices by high single digits compared to 3Q24. Mounjaro and Zepbound were primary growth drivers in the US. For the third consecutive quarter, Lilly led the incretin-based therapy market (slide 10), with Lilly’s medicine capturing 58% of total prescriptions (TRx) – up from 34% in 3Q24 and 57% in 2Q25. Lilly captured 61% of new-to-brand prescriptions (NBRx) share, up one percentage point from the previous quarter.

OUS sales totaled $4.1 billion, up over 2.3x from 3Q24 and 45% sequentially. Growth was mainly driven by 66% increase in Mounjaro’s sales volume and, to a lesser extent, a 6% favorable impact on foreign exchange rates. Of note, Mounjaro is indicated for both T2D and chronic weight management in most OUS countries, except Canada and Japan.

Source: Lilly 3Q25 presentation slides, page 10

Given the strong business performance and favorable impact of foreign exchange rates, Lilly raised 2025 revenue guidance for the second time this year to $63-$63.5 billion, up ~4% from $60-62 billion. This follows guidance update in 2Q25, when Lilly increased the expected full-year revenue from $58-$61 billion to $60-62 billion. Altogether, the new guidance reflects a ~$3.8 billion increase since 1Q25. This update comes at a stark contrast to Novo Nordisk’s guidance, which has been reduced by ~10 percentage points over recent quarters.

Source: Lilly 3Q25 presentation slides, page 12

Lilly Diabetes Worldwide Financial Results – Past Five Quarters

| Overall Diabetes | 3Q24 | 4Q23 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $7,407 | $9,106 | $9,208 | $11,343 | $13,118 |

| YOY Reported Growth | +57% | +59% | +68% | +51% | +77 |

| Sequential Reported Growth | -1% | +23% | +1% | +23% | +16% |

Lilly Diabetes – 3Q25 Geographic Results

| Overall Diabetes | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $8,867 | +61% | +6% |

| OUS | $4,311 | +128% | +45% |

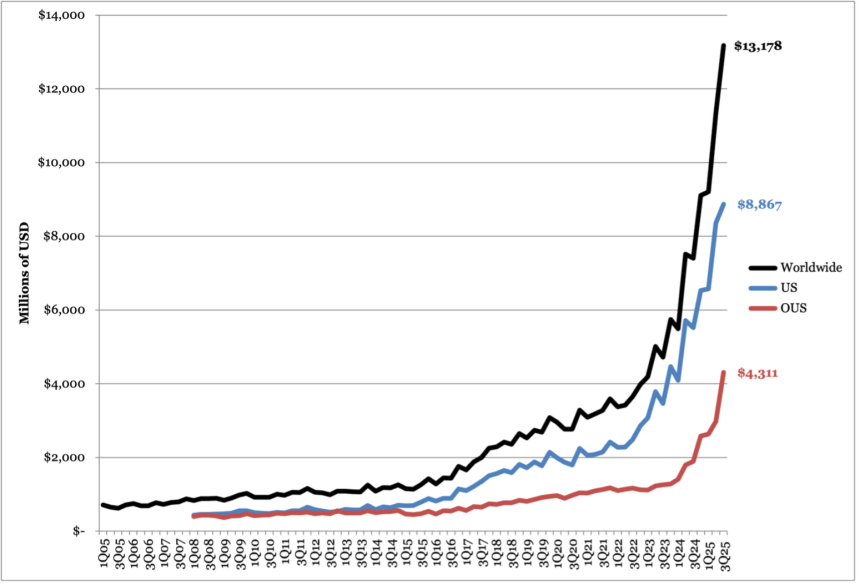

Lilly’s Overall Diabetes Sales (1Q05 - 3Q25)

Source: Close Concerns Knowledge Base

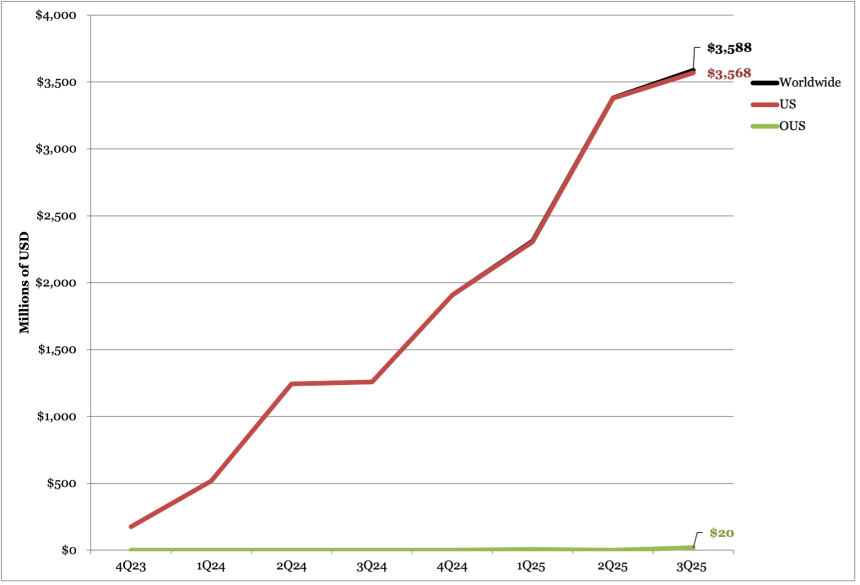

2. Zepbound (tirzepatide for obesity) sales total $3.6 billion, up nearly 3x; new-to-brand prescriptions rebounds after CVS formulary exclusion

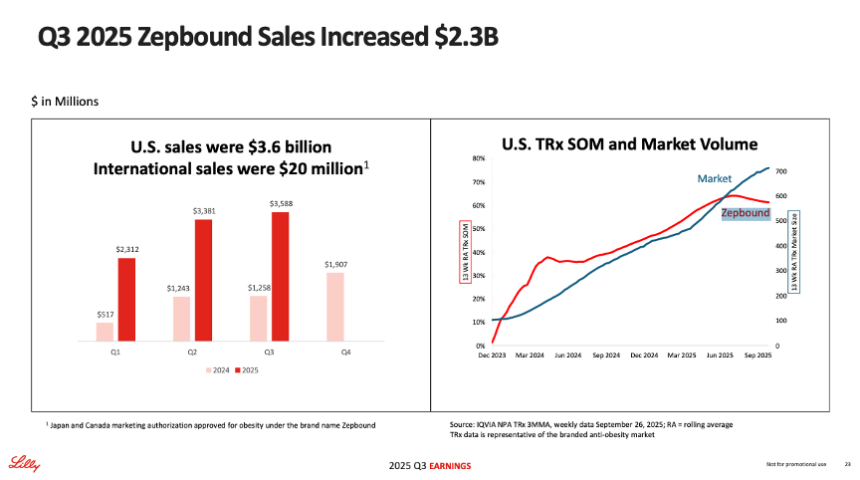

In 3Q25, Zepbound (tirzepatide for obesity) sales totaled $3.6 billion, up nearly 3x from 3Q24 and up 6% sequentially. As Zepbound is only commercialized in the US, Canada, and Japan, US sales comprised over 99% of global sales with $3.6 billion in revenue. Management attributed US sales growth to higher demand, partially offset by lower realized prices. As a reminder, in other OUS markets, such as India, Mounjaro is indicated for both T2D and/or obesity.

For the third consecutive quarter, Zepbound led the obesity market, capturing 63% of total prescriptions (TRx) and 71% of new-to-brand prescriptions (NBRx) at the end of 3Q25. In comparison, Zepbound captured 66% of TRx and 68% of NBRx at the end of 2Q25. Management attributed the slight decrease in TRx share to the July 1 loss of access on CVS Caremark’s national template formulary, which selected Novo Nordisk’s Wegovy as preferred. However, new patient starts rebounded after the formulary change, reflecting continued robust demand for Zepbound.

- In the cash channel, Zepbound vials comprised nearly 30% of TRx and over 45% of new prescriptions in 3Q25. As background, LillyDirect was launched in the US in January 2024, providing direct home delivery service of prescription medications for diabetes, obesity, and migraines. Since June 2025, all doses of Zepbound vials were made available through LillyDirect’s Self Pay Pharmacy Solutions and the Zepbound Self Pay Journey Program. For patients who refill within 45 days after the first fill, Zepbound costs $349/month for 2.5 mg and $499/month for subsequent doses (5 mg, 7.5 mg, 10 mg, 12.5 mg, and 15 mg). Notably, in October 2025, Lilly entered its first retail collaboration with Walmart Pharmacyto launch a pick-up option for people with valid prescriptions to single-dose Zepbound vials. In today’s call, Mr. Ilya Yuffa (EVP and President, Lilly USA and Global Customer Capabilities) said that LillyDirect has significantly increased access for patients and expects retail pick up availability to expand it further.

On the regulatory front, tirzepatide continues to be under review for HFpEF in the EU based on the phase 3 SUMMIT trial (n=731), in which tirzepatide demonstrated a 38% risk reduction in cardiovascular death or worsening heart failure at 52 weeks. Of note, in the US, Lilly announced in 1Q25 that it has withdrawn its application for HFpEF, following the FDA’s request for additional data. On the clinical development, tirzepatide is evaluated for weight maintenance, adolescents with obesity or overweight, T1D, and chronic kidney disease. In 3Q25, Lilly added two more phase 3 trials evaluating the combination of tirzepatide and a monoclonal antibody Omvoh (mirikizumab) for Crohn’s disease and ulcerative colitis with comorbid obesity or overweight.

Source: Lilly 3Q25 presentation slides, page 23

Zepbound Financial Results – Past Five Quarters

| Zepbound | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $1,258 | $1,907 | $2,312 | $3,381 | $3,588 |

| YOY Reported Growth | n/a | n/a | +347% | +172% | +185% |

| Sequential Reported Growth | +1% | +52% | +21% | +46% | +6% |

Zepbound – 3Q25 Geographic Results

| Zepbound | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $3,568 | 184% | +6% |

| International | $20 | N/A | +1220% |

Zepbound Sales (4Q23-3Q25)

Source: Close Concerns Knowledge Base

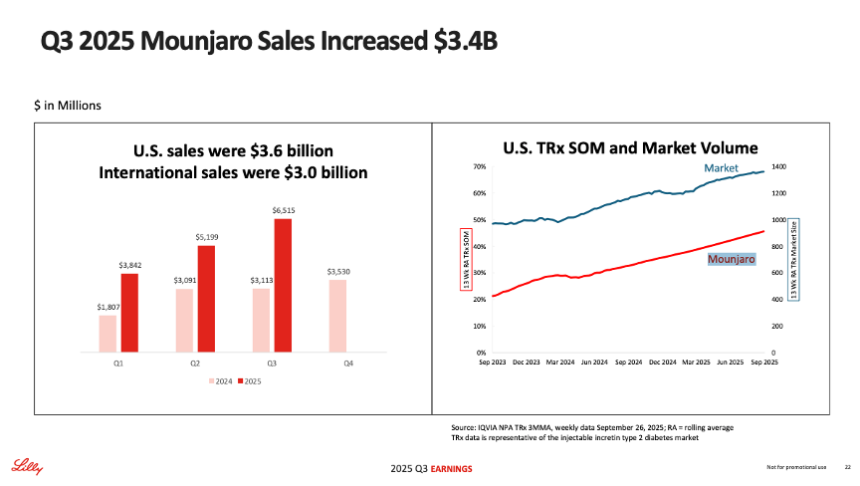

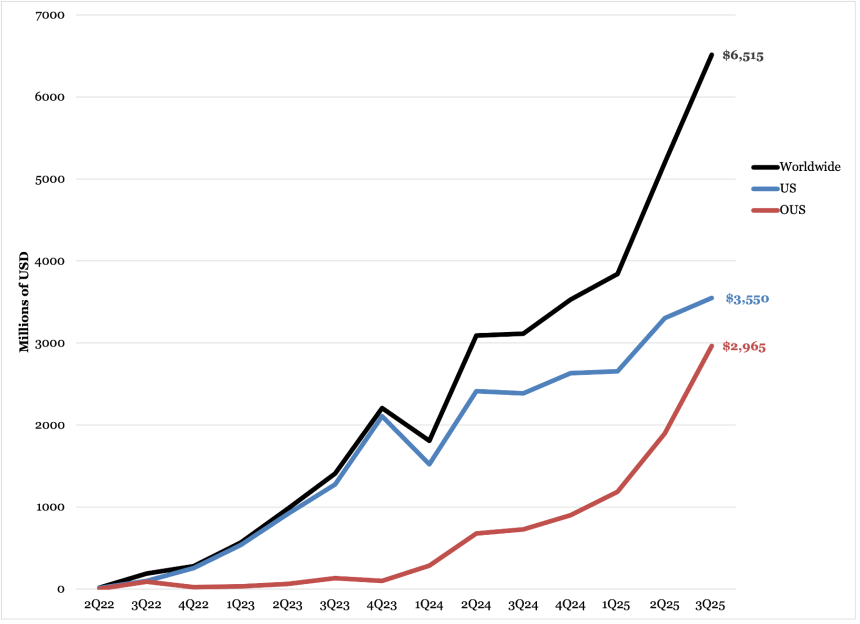

3. Mounjaro sales total $6.5 billion (+2x); 75% of OUS revenue from self-pay patients with obesity

In 3Q25, Mounjaro (tirzepatide for T2D) sales totaled $6.5 billion, up over 2x from 3Q24 and up 25% sequentially. US revenue was $3.6 billion, up 49% from 3Q24 and up 8% sequentially. Growth in the US was driven by strong demand, partially offset by lower realized prices. Notably, Mounjaro remained its leadership in the incretin-based therapy market for T2D, capturing 45% of TRx and 54% of NBRx at the end of 3Q25. This reflects nearly four percentage point increase from 2Q25, when Mounjaro captured 42% of TRx and 50% of NBRx.

Source: Lilly 3Q25 presentation slides, page 22

OUS sales totaled $3.0 billion, up over 4x from 3Q24 and up 56% sequentially. The impressive growth was driven by strong uptake, especially in China, Brazil, Mexico, and India.

Mounjaro is now launched in 55 countries in all major markets. This includes India, where tirzepatide vials were approved in March 2025 and Mounjaro KwikPen was approved in June 2025 and launched in August 2025. Lilly is exploring various commercialization strategies; for example, in October 2025, Lilly partnered with Mumbai-based Cipla to distribute and promote Mounjaro KwikPen in India under a second brand name, Yurpeak. Management acknowledged that reimbursement for obesity drugs remains limited in OUS markets, including India, where all patients must self-pay for the therapy. Currently, approximately 75% of OUS revenue is from people with obesity paying out of pocket, while the remaining 25% is from T2D.

- In the UK in September, Lilly raised the list price of Mounjaro from £92-£122 to £133-£330 ($125-$165 to $180-$446) for people on private insurance but not National Health Service (NHS). The new pricing translates to an increase of 45% to 170%, depending on the dosage. Lilly explained that UK list prices had been significantly lower than other European countries to support early NHS access. This increase is said to better align pricing with other European markets, where Mounjaro costs €410 per month ($477) in the Netherlands and DKK 2,237 per month ($349) in Denmark, as two examples. During Q&A, Mr. Patrik Jonsson (President, Lilly International) said that matching the price in the UK to those in the EU “probably stopped” exports of medicines out of the UK. He also acknowledged that as expected, there is price elasticity in OUS markets; indeed, Avalere reported that prescriptions for its competitor medicine, likely referring to Novo Nordisk’s Ozempic, increased following Lilly’s announcement.

On clinical development, full results of the phase 3 SURPASS-CVOT trial (n=13,299) were presented at EASD 2025. In this head-to-head CVOT comparing Mounjaro to Trulicity in people with T2D and established CVD, Mounjaro numerically reduced major adverse cardiovascular events (MACE) risk by 8 percentage points compared to Trulicity. While there were no mentions during the call, in 2Q25, Lilly shared plans to file for a MACE indication by the end of this year.

Mounjaro Worldwide Financial Results – Past Five Quarters

| Mounjaro | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD Millions | $3,113 | $3,530 | $3,842 | $5,198 | $6,515 |

| YOY Reported Growth | +121% | +60% | +113% | +68% | +109% |

| Sequential Reported Growth | +1% | +13% | +9% | +35% | +25% |

Mounjaro – 3Q25 Geographic Results

| Mounjaro | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $3,550 | +49% | +8% |

| International | $2,965 | +307% | +56% |

Mounjaro Sales (2Q22-3Q25)

Source: Close Concerns Knowledge Base

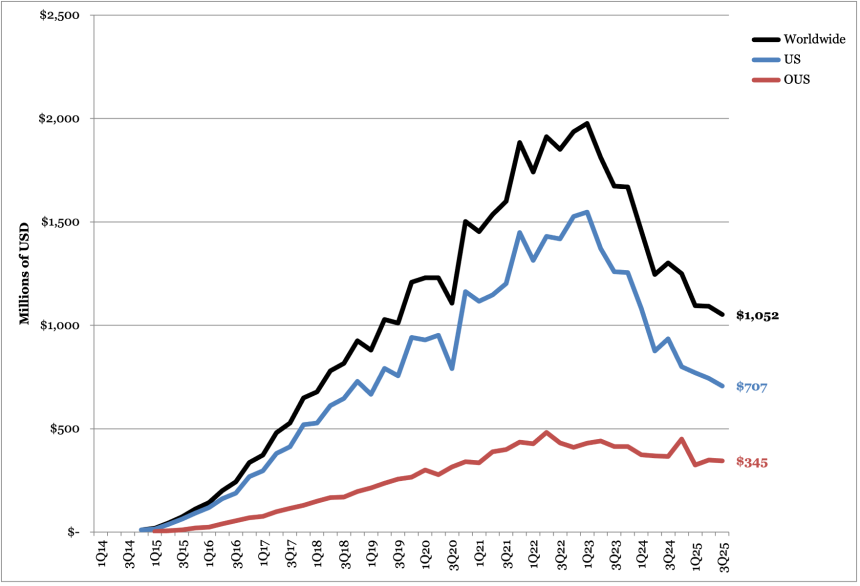

4. Trulicity (dulaglutide) revenue totaled $1.1 billion (-19%), continuing a downward trend

Trulicity (dulaglutide) sales totaled $1.1 billion globally, down 19% from 3Q24 and down 4% sequentially. By geography, US sales totaled $707 million, down 24% from 3Q24 and down 5% sequentially. OUS sales totaled $345 million, down 6% from 3Q24 and down 1% sequentially. While today’s call did not mention the factors contributing to the decline in Trulicity sales, in 4Q24, Lilly attributed the decline to competitive dynamics with newer medicines like Mounjaro. As of 2Q25, Trulicity was no longer on the FDA Drug Shortage list, with the shortage marked as resolved in June 2025.

Full results of the SURPASS-CVOT (n=13,165) were presented at EASD 2025. The phase 3 trial was a head-to-head cardiovascular outcomes trial (CVOT) comparing Mounjaro to Trulicity in people with T2D and established cardiovascular disease (CVD). At four years, tirzepatide reduced MACE‑3 risk by 8% versus dulaglutide (CI 0.83–1.01; p=0.086), demonstrating noninferiority.

Trulicity Worldwide Financial Results – Past Five Quarters

| Trulicity | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $1,301 | $1,250 | $1,095 | $1,092 | $1,052 |

| YOY Reported Growth | -22% | -25% | -25% | -12% | -19% |

| Sequential Reported Growth | flat | -4% | -12% | flat | -4% |

Trulicity – 3Q25 Geographic Results

| Trulicity | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $707 | -24% | -5% |

| International | $345 | -6% | -1% |

Trulicity Sales (4Q14-3Q25)

Source: Close Concerns Knowledge Base

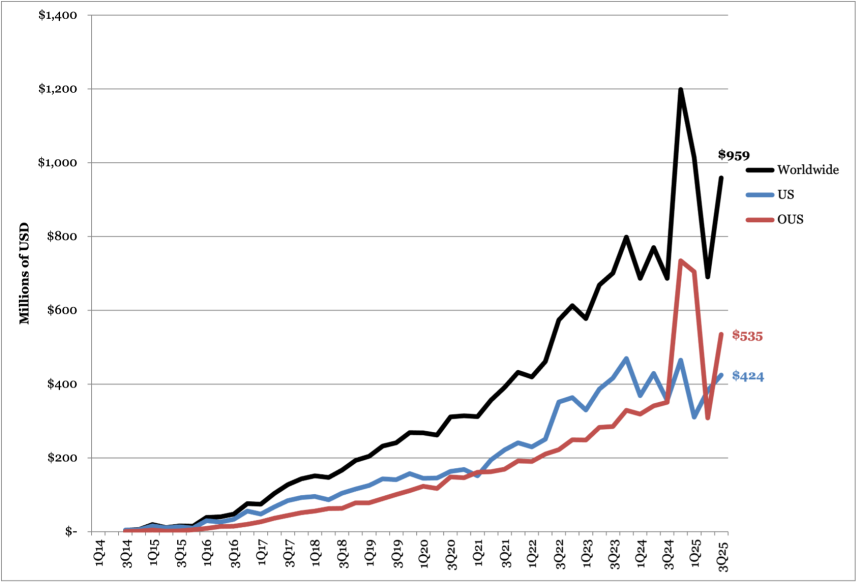

5. Jardiance (empagliflozin) sales totals $959 million (+40%), including a $200 million milestone payment

Sales for SGLT-2 inhibitor Jardiance (empagliflozin) totaled $959 million, up 40% from 3Q24 and 39% sequentially. US sales totaled $424 million, up 26% from 3Q24 and 11% sequentially. OUS sales totaled $535 million, up 53% from 3Q24 and 74% sequentially. OUS sales include a $200 million sales-based milestone payment in 3Q25 from Boehringer Ingelheim. When excluding the milestone payment, Jardiance revenue totaled $759 million, up 10% from 3Q24 and 10% sequentially, and OUS sales totaled $335 million, down 5% from 3Q24 and up 8% sequentially.

- At the end of 2024, Lilly stopped reporting Jardiance’s share of prescriptions in the US. In 4Q24, Jardiance led the SGLT-2 inhibitor market with over 65% in total prescriptions. In 2Q25, Jardiance captured 48% market share, slightly behind AZ’s Farxiga (49%).

SGLT-2 inhibitors will begin to go generic over the next few years. Jardiance’s compound patent is set to expire in 2029 in the US, 2029 in Europe, and 2030 in Japan. Jardiance has won multiple indications, however, including glycemic, heart, and kidney health, Jardiance (10 mg or 25 mg) will remain protected under patent for the treatment of people with T2D and renal impairment until April 2034.

Lilly’s Worldwide Jardiance Revenue – Past Five Quarters

| Jardiance | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Lilly Revenue (Lilly+BI est.) – USD Millions | $686 ($2,059) | $1,198 ($2,694) | $1,014 ($1,933) | $690 ($2,070) | $959 ($2,877) |

| YOY Reported Growth | -2% | +50% | +48% | -10% | +40% |

| Sequential Reported Growth | -11% | +75% | -15% | -32% | +39% |

Lilly’s Jardiance – 3Q25 Geographic Results

| Jardiance | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $424 | +26% | +11% |

| OUS | $535 | +53% | +74% |

Lilly’s Jardiance Sales (3Q14-3Q25)

Source: Close Concerns Knowledge Base

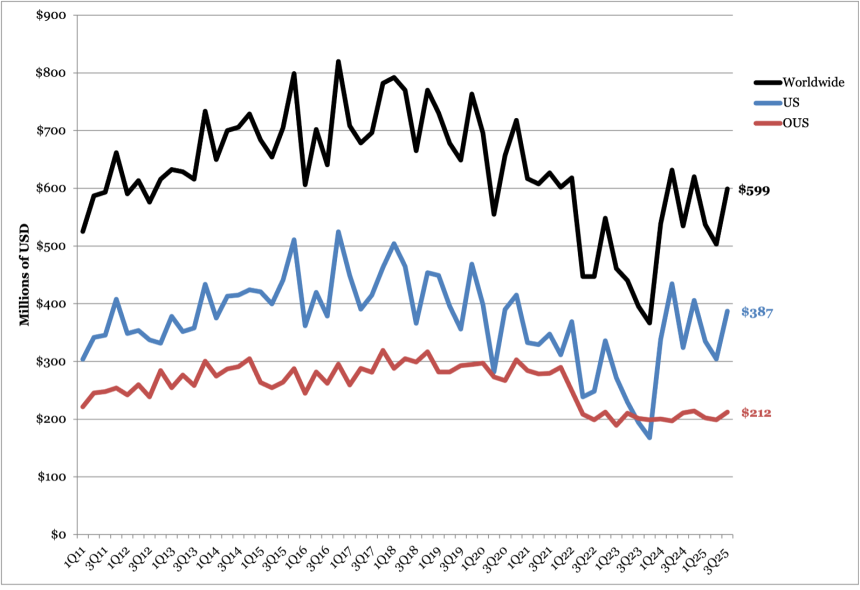

6. Humalog revenue totals $599 million (+12%); biosimilar competition expected to increase

Combined revenue for Humalog and generic insulin lispro totaled $599 million in 3Q25, up 12% from 3Q24 and 19% sequentially. US sales totaled $387 million, up 20% from 3Q25 and 27% sequentially. OUS sales totaled $212 million, up 1% from 3Q24 and 7% sequentially. Lilly did not disclose factors contributing to the rise in revenue in today’s press release or the call.

- While the revenue increased last quarter, we imagine that increased generic and biosimilar competition will continue to affect sales. Biocon Biologic’s Kirsty received FDA approval in July 2025, marking the first and only interchangeable biosimilar to Novo Nordisk’s rapid acting insulin NovoLog (insulin aspart). In February 2025, the FDA approved Sanofi’s Merilog (insulin aspart-szjj) as the first biosimilar to NovoLog.

- While not approved yet, Adocia and Tonghua Dongbao’s BioChaperone Lispro (ultra-rapid insulin) demonstrated noninferior A1c reduction and significant reduction in postprandial glucose levels compared to Humalog in a phase 3 trial for people with T1D (n=509). In topline results announced during Adocia’s 3Q25 call, adverse events and hypoglycemia were similar between the two therapies.

Lilly reduced the price of generic insulin lispro from $82 per vial to $25 per vial and the price of Humalog to $82 per vial in March 2023 and September 2023, respectively. For both lispro and Humalog, the price reduction included 10 mL and 3 mL vials, cartridges, KwikPens, and Junior KwikPens, but did not include the Tempo Pen – a smart, Bluetooth-compatible version of KwikPen. Moreover, in April 2020, Lilly announced an Insulin Value Program to grant monthly prescriptions of Lilly insulins for $35 per month to patients in the US with and without commercial insurance.

Humalog Worldwide Financial Results – Past Five Quarters

| Humalog | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $534 | $620 | $537 | $503 | $599 |

| YOY Reported Growth | +35% | +69% | flat | -20% | +12% |

| Sequential Reported Growth | -15% | +16% | -13% | -6% | +19% |

Humalog – 3Q25 Geographic Results

| Humalog | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $387 | +20% | +27% |

| International | $212 | +1% | +7% |

Humalog Sales (1Q11-3Q25)

Source: Close Concerns Knowledge Base

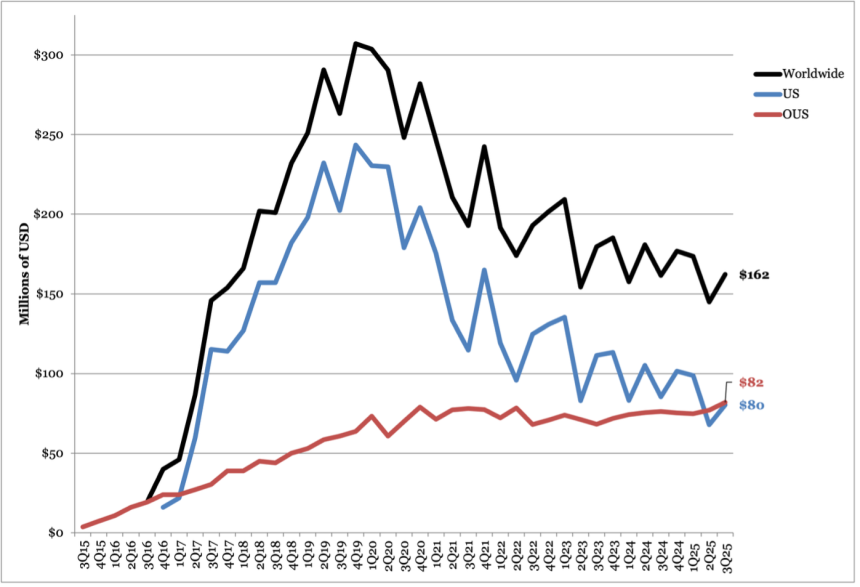

7. Basaglar sales totals $162 million, consistent with previous quarters

Sales for BI/Lilly’s insulin glargine Basaglar totaled $162 in 3Q25, flat from 3Q24 and up 12% sequentially. US sales totaled $80 million, down 6% from 3Q24 and up 18% sequentially. OUS sales totaled $82, up 8% from 3Q24 and 6% sequentially. While Lilly did not mention Basaglar in the press release or the call, as shown in the graph below, 3Q25 sales is relatively consistent with overall decline in revenue seen in the last four years. We imagine the continued decline likely stems from competitive pressures on pricing and volume in the Medicaid segment, which began in August 2021.

Basaglar Worldwide Financial Results – Past Five Quarters

| Basaglar | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $162 | $177 | $174 | $145 | $162 |

| YOY Reported Growth | -10% | -5% | +10% | -20% | flat |

| Sequential Reported Growth | -11% | +10% | -2% | -17% | +12% |

Basaglar – 3Q25 Geographic Results

| Basaglar | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $80 | -6% | +18% |

| International | $82 | +8% | +6% |

Basaglar Sales (3Q15-3Q25)

Source: Close Concerns Knowledge Base

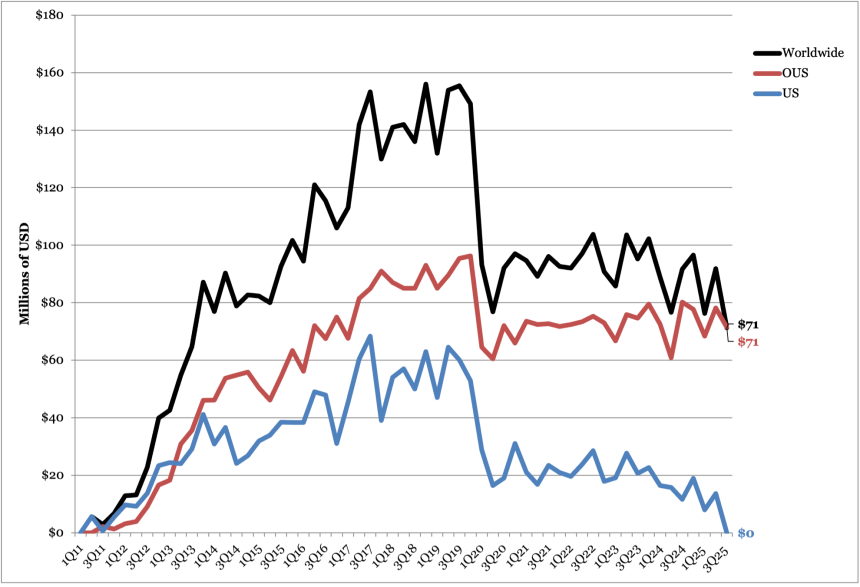

8. DPP-4 inhibitor Tradjenta revenue totals $71 million (-22%)

DPP-4 inhibitor Tradjenta revenue totaled $71 million in 3Q25, down 22% from 3Q24 and down 22% sequentially. OUS sales totaled $71 million, down 11% from 3Q24 and down 9% sequentially. No US sales were reported this quarter by Lilly. Lilly’s partner BI, who is responsible for US sales, is private and has not publicly reported sales for Tradjenta.

- Tradjenta’s sales trajectory is consistent with a broader decline in the DPP-4 inhibitor market. In 2Q25, the DPP-4 class generated $1 billion in sales, essentially flat versus 2Q24 and down 12% from the prior quarter. The decline likely reflects switches by some patients from DPP-4 inhibitors to other therapies, like SGLT-2 inhibitors and GLP-1 RAs given their benefits beyond glycemic management.

Tradjenta Worldwide Financial Results – Past Five Quarters

| Tradjenta | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions | $92 | $97 | $76 | $92 | $71 |

| YOY Reported Growth | -4% | -5% | -14% | +20% | -22% |

| Sequential Reported Growth | +20% | +5% | -21% | +20% | -22% |

Tradjenta – 3Q25 Geographic Results

| Tradjenta | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | -- | -- | -- |

| International | $71 | -11% | -9% |

Tradjenta Sales (2Q11-3Q25)

Source: Close Concerns Knowledge Base

Pipeline Highlights

1. Topline results of phase 3 ATTAIN-2, ACHIEVE-3, and ACHIEVE-5 trials of orforglipron; new ATTAIN-OA PAIN and RESTRAIN-SUI trials initiated

In 3Q25, Lilly announced several phase 3 trial data for orforglipron, a once-daily oral small molecule GLP-1 RA, in adults with overweight or obesity without (ATTAIN) or with T2D (ACHIEVE).

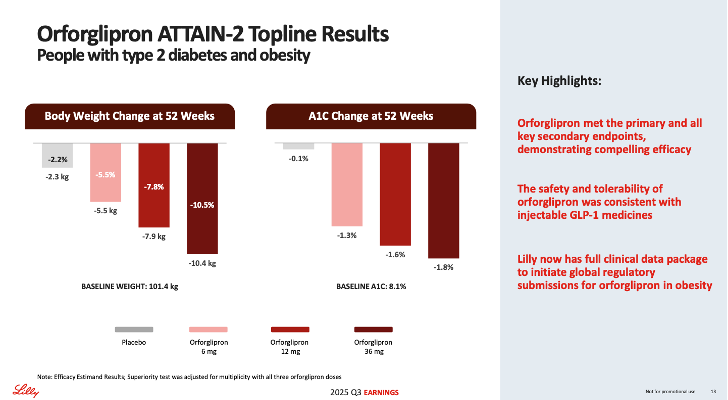

The phase 3 ATTAIN program investigates the safety and efficacy of orforglipron across obesity, diabetes, and comorbidities. Dr. Skovronsky noted that the company has completed the necessary steps to initiate global regulatory filings for the obesity indication with the completion of the ATTAIN-2 trial. Filings are set to begin imminently, with a launch expected in the coming year.

- ATTAIN-1 (n=3,127) trial assessed orforglipron on weight management in adults with obesity or overweight with related conditions but not T2D. In 2Q25, Lilly shared topline results, showing that orforglipron conferred a 12% weight loss, with ~60% achieving ≥10% weight reduction and 40% achieving ≥15%. Full results were presented at EASD 2025.

- ATTAIN-2 (n=1,613) trial assessed orforglipron in people with obesity or overweight with T2D. Topline results reported in August 2025 showed that orforglipron 36 mg confers 11% weight loss (vs. 2% in placebo) and A1c reduction by 1.8% (vs. 0.1%) in adults with obesity and T2D.

Source: Lilly’s 3Q25 earnings presentation (slide 13)

Dr. Skovronsky also highlighted results from the ACHIEVE program, where results from the ACHIEVE-2, ACHIEVE-3, and ACHIEVE-5 trials were announced in 3Q25. He highlighted that across six completed phase 3 orforglipron trials, there were consistent cardiometabolic benefits alongside a stable safety and tolerability profile. Overall, the data support the development of an oral, scalable small-molecule GLP-1 RA with efficacy, safety, and tolerability comparable to those of injectable GLP-1 RA monotherapies for obesity and T2D. Dr. Skovronsky said Lilly views orforglipron as a potential foundational therapy for T2D.

- ACHIEVE-1 compared orforglipron to dapagliflozin in adults with T2D with inadequate glycemic management using metformin. Results were previously presented at ADA 2025 and published simultaneously in NEJM. In the trial, orforglipron demonstrated an A1c reduction of 1.3%-1.6% from a baseline of 8.0%, for the efficacy estimand. Additionally, up to 76% of participants on orforglipron achieved the A1c target of <7.0%, 66% achieved an A1c of ≤6.5%, and 26% achieved <5.7%. At the highest dose of orforglipron (36 mg), participants experienced a mean weight loss of 8% (approximately 16 lbs).

- ACHIEVE-2 compared once-daily orforglipron (3 mg, 12 mg, 36 mg) to a maximum dose of dapagliflozin (10 mg) in adults with inadequately managed T2D on metformin. Orforglipron achieved the primary endpoint, demonstrating a superior A1c reduction from 1.3% to 1.7% across doses, compared to 0.8% with dapagliflozin.

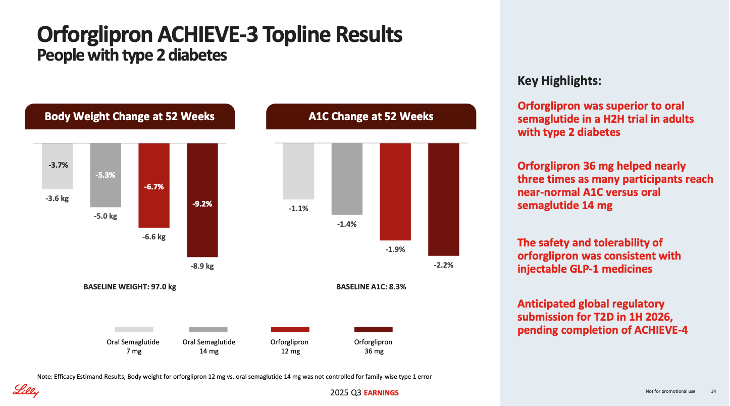

- ACHIEVE-3 compared orforglipron (12 mg and 36 mg) to Rybelsus (oral semaglutide 7 mg and 14 mg) on glycemic reduction and weight loss. Orforglipron demonstrated a 74% relative improvement in weight loss for patients taking orforglipron (9.2%) compared to oral semaglutide (5.3%).

- ACHIEVE-5 was a phase 3 add-on trial for adults with inadequately managed T2D on titrated insulin glargine, with or without metformin and/or SGLT-2 inhibitors. Orforglipron was tested at the three doses (3 mg, 12 mg, 36 mg) against placebo. Orforglipron achieved A1c reduction from 1.5% to 1.9% across doses, compared to 0.8% on placebo.

The ACHIEVE-4 trial (n=2,749) is the last remaining trial in the ACHIEVE program awaiting results. Upcoming results are expected to lead to a regulatory submission of orforglipron for T2D by 1H26.

Source: Lilly’s 3Q25 earnings presentation (slide 13)

Beyond the ATTAIN and ACHIEVE programs, Lilly is also conducting several additional phase 3 orforglipron trials. In today’s call, Lilly announced new phase 3 trials for: (i) osteoarthritis pain; and (ii) stress urinary incontinence (SUI), which may benefit from the weight loss effects of orforglipron. See below for ongoing orforglipron trials.

- ATTAIN-MAINTAIN: An extension of the SURMOUNT-5 trial, aims to test orforglipron as a potential maintenance therapy for patients who have lost weight on injectable incretin therapies, such as Zepbound (tirzepatide). Excitingly, the study is expected to be completed in January 2026.

- This study is the first of its kind, as participants were previously escalated to a maximal tolerable dose of semaglutide or tirzepatide after 72 weeks of treatment. Dr. Skovronsky labeled this a “very ambitious trial.”Topline results are expected late this year or early next year.

- ATTAIN-OSA: Evaluates orforglipron in people with moderate-to-severe sleep apnea and obesity or overweight. The study is expected to be completed in January 2027.

- ATTAIN-HYPERTENSION: Evaluates orforglipron for managing high blood pressure in adults with overweight or obesity. Launched in April 2025, the study is currently recruiting participants and is expected to be completed in September 2027.

- ATTAIN-OA PAIN: Evaluates efficacy and safety of orforglipron in people with obesity or overweight who have osteoarthritis of the knee with pain. The study launched in September 2025 and is expected to be completed in May 2028.

- RESTRAIN-SUI: Evaluates efficacy and safety of orforglipron in females with obesity or overweight who have SUI. The study launched in September 2025 and is expected to complete in March 2028.

During Q&A, Mr. David Ricks emphasized Lilly’s goal of getting orforglipron out to as many patients as possible, as quickly as possible. He also noted that orforglipron is likely a strong candidate for the FDA’s Priority Review Voucher program, with hopes of accelerating launch.

- When asked about a potential segmented approach – positioning orforglipron as a scalable oral maintenance option for lower-severity patients while retatrutide targets heavier or more comorbid populations – Dr. Skovronsky responded that Lilly has long pursued the obesity opportunity with a deep R&D focus and a broad portfolio aimed at multiple targets. He said the company believes it has leading therapies across the portfolio and is closely watching competitors but has not seen anything that changes its view of Lilly’s competitive position. Lilly intends to protect and extend its lead through continued investment in R&D, multiple phase 3 programs, and additional indications.

- Mr. Jonsson added an OUS perspective, highlighting the UK price increase of tirzepatide in September 2025. He stated that for patients with BMI<35 kg/m², for whom tirzepatide may not be as effective, orforglipron becomes more relevant. Overall, he positioned orforglipron as a complementary treatment to some of Lilly’s other incretin therapies.

2. First phase 3 results on retatrutide expected by the end of 2025; retatrutide to fill a distinct clinical segment with very high BMI or obesity-related complications

Retratrutide (triple GLP-1/GIP/glucagon RA candidate) was a major focus of today’s call. Currently, retatrutide is investigated in two phase 3 programs: TRIUMPH and TRANSCEND. Excitingly, Lilly updated that results from six phase 3 studies are expected by the end of 2026.

The TRIUMPH program is evaluating retatrutide in people with obesity or overweight and comorbidities. Specifically,

- TRIUMPH-1 (n=2,300) assesses retatrutide in people with obesity or overweight, and is expected to complete in May 2026.

- TRIUMPH-2 (n=1,000) investigates retatrutide in people with T2D and overweight or obesity, and is expected to complete in May 2026.

- TRIUMPH-3 (n=1,800) evaluates retatrutide in people with obesity and established CVD, with study completion expected in May 2026.

- TRIUMPH-4 (n=405) is investigating retatrutide in people with obesity or overweight and osteoarthritis (OA). The study is expected to complete in December 2025.

- TRIUMPH-4 will be the first phase 3 trial readout on retatrutide and is expected later this year. During the call, Dr. Skovronsky cautioned against extrapolating data from one trial, as more study results are needed to gain a comprehensive understanding of the drug.

- TRIUMPH-6 (n=643) evaluates retatrutide for weight maintenance in people with T2D and obesity or overweight, with study completion expected in May 2026.

- TRIUMPH-7 (n=586) evaluates retatrutide for people with overweight or obesity and chronic low back pain, with study expected to complete in September 2027.

- TRIUMPH-Outcomes (n=10,000) trial will evaluate cardiorenal benefits, and is expected to complete in February 2029.

The TRANSCEND program is actively investigating retatrutide in people with T2D:

- TRANSCEND-T2D-1 (n=480) assesses retatrutide in people with T2D and inadequate glycemic control with diet and exercise alone. The study is expected to complete in February 2026.

- TRANSCEND-T2D-2 (n=1,250) evaluates retatrutide compared to semaglutide in people with T2D and inadequate glycemic control with metformin and with or without SGLT-2 inhibitors. The study is expected to complete in January 2027.

- TRANSCEND-T2D (n=320) investigates retatrutide in people with T2D and renal impairment with inadequate glycemic control on basal insulin with or without metformin and SGLT-2 inhibitor therapy. The study is expected to complete in October 2026.

Finally, phase 3 SYNERGY-Outcomes trial (n=4,500) evaluates retatrutide for MASLD and is expected to complete in August 2032.

During the call, management shared expectations that retatrutide will deliver greater and more rapid weight loss compared to existing obesity medicines, including tirzepatide, due to its “first-of-a-kind triple acting mechanism.” Dr. Skovronsky further added that the therapy will likely be suitable for patients with a very high BMI or those with obesity-related complications that require a high degree of weight loss, suggesting market segmentation.

3. Lilly Diabetes-Related Pipeline Summary

The table below reflects the latest updates to Lilly’s diabetes pipeline products. Items highlighted in yellow indicate changes to the pipeline in 3Q25.

| Candidate | Phase | Timeline/Notes |

| Automated Insulin Delivery System/Smart Pens | Not applicable/Approved | Connected Care Prefilled Insulin Pen under regulatory review as a new indication or line extension; Lilly signs international agreement with Roche, Glooko, Dexcom, and myDiabby to integrate its connected pen products so that users have flexibility in their analysis platform in May 2021; Lilly signs collaboration and licensing agreement with Welldoc in February 2021; Lilly gains non-exclusive global and exclusive US commercialization rights to Ypsomed’s YpsoPump and future mylife AID system in November 2020; US connected pen approved by FDA in 1Q19 (type 1 and 2); AID system advanced to “phase 2” on 4Q18 call; Feasibility study with Dexcom CGM and in-house pump/closed loop algorithm completed February 2018, initiated December 2017 |

| Jardiance (empagliflozin) in post-myocardial infarction | Phase 3 | EMPACT-MI results presented at ACC 2024, failed to meet primary composite endpoint; Fast Track designation granted by FDA in September 2020 |

| Jardiance (empagliflozin) in heart failure | Approved | EU approval in HF regardless of ejection fraction in March 2022; FDA approval for adults with HFpEF with or without diabetes in February 2022; Submitted for HFpEF indication in US and EU; received Breakthrough Therapy designation for HFpEF September 2021; Full results from EMPEROR-Preserved read out at ESC 2021; Approved in US for HFrEF in August 2021;Primary endpoint of EMPEROR-Preserved met; Approved in EU for HFrEF in June 2021; HFrEF sNDA submitted to FDA in January 2021; Positive full results for EMPEROR-REDUCED presented at ESC 2020; Positive topline results for EMPEROR-REDUCED announced in 2Q20; Fast Track designation granted by FDA in June 2019; EMPEROR-Preserved and EMPEROR-Reduced initiated March 2017, expected to complete October 2020 and June 2020, respectively; Two EMPERIAL studies initiated March 2018 to investigate effect of Jardiance on exercise capacity in heart failure patients, expected to complete December 2019 with topline data this year |

| Jardiance (empagliflozin) in chronic kidney disease | Regulatory submission | FDA approval in CKD in September 2023; EU approval in CKD in July 2023; Submitted to FDA and EMA for approval in CKD in 4Q22; Results presented at ASN 2022; Early stop for EMPA-KIDNEY in March 2022due to “clear positive efficacy”; study completed July 2022; Fast Track designation granted by FDA in March 2020; EMPA-KIDNEY announced June 2017and initiated 1Q19 (delayed from November 15, 2018 start), expected completion December 2022; Collaboration with University of Oxford and Duke Clinical Research Institute |

| Jardiance (empagliflozin) in pediatric T2D | Regulatory submission | Pediatric T2D approval in the US in June 2023; In March 2023, FDA accepts sNDA for Jardiance in youth ages 10 and older with type 2 diabetes; phase 3 DINAMO trial presented at IDF in December 2022 |

| Tirzepatide (GIP/GLP-1 dual agonist) | Approval for T2D, obesity, obstructive sleep apnea and obesity, and pediatric/adolescent T2D Phase 3 for diabetes/obesity/T1D + obesity, MALSD, Crohn’s Disease, and ulcerative colitis phase 2 for MASH and CKD | Phase 3 COMMIT-CD and COMMIT-UC trials initiated to evaluate of mirikizumab and tirzepatide combination in adult with Chron’s Disease or ulcerative colitis and obesity or overweight Full SURPASS-CVOT and SURPASS-PEDS results presented at EASD 2025; Approved for pediatric and adolescent T2D in 2Q25; announced positive topline results from SURPASS-CVOT in July 2025; SURPASS-T1D-1initiated for phase 3 trial for adults with T1D and obesity or overweight; phase 3 initiated for MASLD in 2Q25; post-hoc analysis of SURMOUNT-5shared at ADA 2025; Full results of SURMOUNT-5 announced at ECO 2025; Announced in 1Q25 that tirzepatide is no longer being pursued for HFpEF indication in the US; topline results of SURMOUNT-5released in December 2024; FDA-approved for OSA in December 2024; Regulatory submission for HFpEF in 4Q24; Positive topline results of 176-week SURMOUNT-1 trial in August 2024; SUMMIT topline results released in August 2024; Approved in China for chronic weight management in July 2024; phase 3 SURMOUNT-OSA presented at ADA 2024; phase 2 SYNERGY-NASH full results presented at EASL 2024; Phase 2 trial investigating high-dose tirzepatide in participants with T2D and obesity; SURMOUNT-3 and SURMOUNT-4 full results presented at Obesity Week 2023and EASD 2023, respectively; SURMOUNT-3 and SURMOUNT-4 topline results released in July 2023, and full SURMOUNT-2 results presented at ADA 2023. Obesity submission completed in the US in 2Q23; Obesity submission accepted in EU in 1Q23; SURMOUNT-2 topline results released April 2023; Phase 1 bioequivalence study testing new tirzepatide autoinjector device initiated April 2023 with expected completion July 2023; SURPAS-SWITCH-2 studyinitiated March 2023; SURMOUNT-5 trial initiated April 2023; Fast track designation in sleep apnea granted in 4Q22; Initiation of SURMOUNT-MMO trial in 3Q22; FDA approval in type 2 diabetes in May 2022; SURPASS J-mono and SURPASS J-combo results published in The Lancet in August 2022; Phase 3 SURMOUNT-OSA, SURPASS-EARLY, and SURPASS-PEDStrials initiated 2Q22; Phase 3 SURMOUNT-MMO and phase 2 CKD trial announced in December 2021; Submitted for type 2 diabetes indication in US and EU; SURPASS-3 CGM, SURPASS-4, and SURPASS-5 PRO presented at EASD 2021; SURPASS-1, SURPASS-2,SURPASS-3, and SURPASS-5presented at ADA 2021; SURPASS-4 read out in May 2021; Phase 3 study in HFpEF (SUMMIT) initiated in April 2021; SURMOUNT-2,SURMOUNT-3, and SURMOUNT-4 initiated in 1Q21 (all three started March 29, 2021); Positive SURPASS-2 topline results released March 2021; Positive SURPASS-3 and -5 topline results released February 2021; Positive SURPASS-1 topline data released in December 2020;Investor webinar presented November 2020; Phase 3 study in HFpEF (SUMMIT) to initiate in 2021; First patient dosed in SURPASS-CVOT head-to-head against Trulicity in June 2020; Phase 3 SURPASS programunderway – five studies to be underway in 2019; Phase 2 in NASH (SYNERGY-NASH) initiated in 2019; Phase 3 for obesity (SURMOUNT-1) initiated in 4Q19; Dose escalation data presented ADA 2019; Phase 2b data presented at EASD 2018; Phase 1 trial completed June 2017 |

| Insulin efsitora alpha (Basal insulin-FC, f.k.a. “BIF”) (LY3209590) | Phase 3 (T1D and T2D) | Submitted for regulatory approval for T2D in the US in 3Q25; Full results of QWINT-1, 2, and 4 presented at ADA 2025; submitted for regulatory approval for T2D in EU in 2Q25; Full results of QWINT-2 and QWINT-5 presented at EASD 2024; positive topline results of QWINT-1 and QWINT-3 in September 2024; Phase 3 QWINT-2 and QWINT-4 topline results released in May 2024; Initiation of QWINT-1 in 4Q22; Initiation of QWINT-4 and QWINT-5 trials in 3Q22; Phase 3 QWINT-3 trial in T2D initiated March 2022 with expected completion in 2024; Phase 2 data in type 2 diabetes presented at ADA 2022; 5 phase 3 QWINT trials announced in 4Q21; Phase 2 trial in type 1 diabetes completed October 2021; Phase 2 trial in type 2 diabetes completed October 2021; Phase 2 data presented at ENDO 2021 and ADA 2021; Movement into phase 2announced during 2019 Investor Day; Topline phase 1 data expected in 2020 |

| Lepodisiran (siRNA) | Phase 3 | Phase 3 ACCLAIM-Lp(a) trial for reduction of major cardiovascular events in people with high Lp(a) and CVD or at risk of a heart attack or stroke initiated in March 2024; phase 1 results presented at AHA 2023 |

Orforglipron (f.k.a. LY3502970) Oral GLP-1 non-peptidic agonist (NPA) | Phase 3 for T2D, OSA, hypertension, and osteoarthritis knee pain, and urinary incontinence | Positive topline results from phase 3 ATTAIN-2 (August 2025), ACHIEVE-2 (October 2025), ACHIEVE-3 (September 2025), and ACHIEVE-5 (October 2025) trials. Phase 3 trials initiated for osteoarthritis with pain and urinary incontinence. Full ATTAIN-1 results presented at EASD 2025; Positive topline results from phase 3 ATTAIN-1 announced in August 2025; Full results of ACHIEVE-1 results announced at ADA 2025; phase 3 initiated for hypertension in 2Q25; phase 3 initiated for osteoarthritis pain of knee with overweight or obesity; Positive topline phase 2 ACHIEVE-1 results announced in April 2025; announced plans for phase 3 trials for hypertension; phase 3 ATTAIN-OSA trial initiated for OSA in 4Q24; phase 2 results in obesity presented at ADA 2023; phase 3 ACHIEVE-4 trial in T2D and obesity/overweight initiated April 2023; topline phase 2 results in T2D and projected phase 2 results in obesity released December 2022; named orforglipron in 3Q22; phase 2 trial and additional phase 2 trial in Japanese patients completed in September 2022; phase 2 trial initiated September 2021; phase 1 trial ongoing, expected completion March 2022; Moved to phase 1 as of 2Q19; Licensed from Chugai in September 2018;Management reaffirms Lilly’s commitment at JPM 2018 and during 4Q18 call |

| Retatrutide (GLP-1/GIP/glucagon tri-agonist) | Phase 3 for T2D, CV, renal outcomes, sleep apnea, knee osteoarthritis, obesity and low back pain, and MASH | Phase 3 of TRIUMPH-7 initiated for retatrutide in obesity or overweight and chronic lower back pain; Phase 3 initiated for MASLD in 2Q25; Phase 3 trials for obesity include TRIUMPH 1, 2, 3, 4, 5, and 6; Announced plans in 1Q25 to initiate phase 3 trials for obesity and chronic low back pain; Initiated phase 3 TRIUMPH outcomes for CV and renal function in 2Q24; Phase 3 TRANSCEND program initiated in February 2024; TRIUMPH phase 3 trials for triple-G retatrutide are actively enrolling for obesity, sleep apnea, and knee osteoarthritis; Phase 2 results in T2D, obesity, and NASH presented at ADA 2023; phase 3 TRIUMPH program initiated in 2Q23; projected phase 2 results in T2D and phase 2 results in obesity released December 2022; Phase 2 trial in type 2 diabetes and phase 2 trial in obesity/overweight began May 2021 with expected completion October 2022; Phase 1 completed in December 2020; Highlighted in 3Q19 earnings – internal readout to inform potential phase 2 start in 2020; Entered Lilly’s clinical pipelinein 1Q19 |

| Muvalaplin (Lp(a) inhibitor) | Phase 3 | Phase 3 initiated in 3Q25;Announced plans in 1Q25 to initiate phase 3 trial later in 2025; phase 2 trial initiated in November 2022 |

| Bimagrumab (monoclonal antibody against ACVR2B) | Discontinued phase 2 trial in obesity/overweight without T2D | Phase 2 trial discontinued in September 2025; Full results of phase 2 presented at ADA 2025; Phase 2 study initiated in October 2024 for bimagrumab/tirzepatide combination therapy in obesity or overweight without T2D. |

| Brenipatide (injectable dual GLP-1/GIP RA) | Phase 3 (Alcohol use disorder) and phase 2 (asthma) | In 3Q25, Lilly launched a phase 2 trial for asthma in phase 3 trials for alcohol use disorder(AUD) and AUD with hazardous alcohol use. |

| GLP-1/glucagon dual agonist (once-weekly oxyntomodulin, mazdutide) | Phase 2 (T2D), Phase 2/3 (obesity) | Positive results for phase 3 GLORY-1 study of dual GLP-1/glucagon receptor agonist mazdutide in Chinese adults with obesity on January 2024; advanced into phase 2 for obesity in 4Q23; Phase 1 trialinitiated November 2022, expected completion December 2023; Phase 1b results announced in obesity in October 2022; Positive topline phase 2 results announced July 2022; phase 2 study initiated August 2021 with estimated completion 3Q22; Phase 1 completed in July 2021; China-based Innovent Biologics licensed mazdutide from Lilly in 2019; Advanced into phase 1 in 4Q16; Oxyntomodulin analog under development for type 2 diabetes and NASH; First announced in May 2016 R&D update |

| ANGPTL3 siRNA in CVD | Phase 2 | Entered phase 2 development in 3Q22; Phase 1 study completed May 2022; Licensed by Kyttaro Therapeutics in April 2022 to treat ASCVD; Added to pipeline in 4Q20 |

| Glucose-sensing insulin receptor agonist | Phase 2 | Phase 2 initiated in 2Q24; Phase 1 initiated in 4Q23 |

| Nisotirostide | Phase 2 | Phase 2 announced 2Q25; Phase 1 completed in June 2023 for overweight or obese patients studying tolerability of LY3457263 when used with tirzepatide |

| Oral dual GLP-1/GIP agonist (LY3493269) | Phase 1 | Phase 1 trial initiated March 2023, with expected completion September 2023; Phase 1 trialinitiated May 2021, completed in November 2021; Announced in 3Q19 update; Moved to phase 1 in 4Q19 |

| PYY (peptide YY) analog in diabetes | Phase 1 | Phase 1 in obesity initiated November 2022, exp. completion May 2023; Phase 1 study in diabetes initiated June 2022, expected completion September 2023; Added to pipeline in 4Q20 |

| Long-acting GIPR agonists in diabetes | Phase 1 | Phase 1 initiated June 2022, expected completion October 2023; Phase 1 completions October 2021, November 2021and December 2021; Added to pipeline in 4Q20 |

| Eloralintide (amylin agonist long acting) | Phase 2 in obesity; Phase 2 in T2D | Phase 2 study on combination therapy with tirzepatide in T2D 3Q24; Phase 2 initiated in February 2024; phase 1 initiated March 2022, expected completion January 2024 |

| PNPL3 siRNA | Phase 1 (MASH) | Added to pipeline 2Q22; phase 1 study in NAFLD initiated June 2022 with expected completion November 2024 |

| Relaxin-LA in heart failure | Phase 1 | Phase 2 in HFpEF initiated February 2023, with expected primary completion in November 2023; Phase 1 study completed in May 2022; Added to pipeline in 1Q21 |

Lp(a) siRNA in cardiovascular disease (LY 3819469) | Phase 1 | Phase 2 trial initiated October 2022, exp. Primary completion October 2023; Phase 1completed November 2022 |

GLP-1 receptor non-peptide agonist 2 (GLP-1/NPA 2) (LY3549492) | Phase 2 | Phase 2 trial initiated in 4Q24; Added to pipeline in 2Q24 |

| GIP/GLP-1 co-agonist 3 | Phase 1 | Added to pipeline in 2Q24 |

| PCSK9 Editor | Phase 1 | Phase 1 VERVE-102 trial announced 2Q25 for patients with familial hypercholesterolemia |

| ANGPTL3 Editor | Phase 1 | Phase 1 VERVE-201 trial announced in 2Q25 for patients with refractory hyperlipidemia |

| Beta cell encapsulation therapy for type 1 diabetes | Preclinical | Lilly entered partnership with Sigilon in April 2018; Sigilon will file IND; Afterward, Lilly will lead in-human trials |

| Volenrelaxin (long-acting relaxin molecule) | Phase 2 in CKD - discontinued | Discontinued for heart failure and CKD in 4Q24; Phase 2initiated 3Q24 |

| Amylin calcitonin receptor agonist (DACRA QW II) | Phase 1 in obesity – discontinued | Discontinued in 4Q24; Phase 1initiated May 2022, exp. completion in September 2023; Added to pipeline 2Q22 |

| APOC3 siRNA | Phase 1 - discontinued | Removed in 3Q24 |

| NRG4 agonist (neuregulin 4 agonist) in HF and diabetes | Phase 1 – discontinued | Removed in 2Q24; Expected phase 1 completion March 2024 (pushed back from July 2023); Added to pipeline in 2Q20 |

Close Concerns’ Questions

1. What strategies is Lilly exploring to expand coverage for Mounjaro as a treatment for obesity or overweight in OUS markets?

2. How does Lilly anticipate the cardiometabolic outcomes benefits to differ across injectable semaglutide, tirzepatide, orforglipron, and retatrutide?

3. Given that small molecules are cheaper to manufacture, what is the price range that Lilly is considering for orforglipron?

4. Will Lilly evaluate orforglipron and/or retatrutide in people with T1D and overweight or obesity?

5. How does brenipatide differ from tirzepatide, given that both are GLP-1/GIP RA? Is Lilly interested in exploring brenipatide’s potential efficacy in cardiometabolic diseases?

6. How does Lilly expect biosimilar competitions to affect Humalog sales?

Analyst Q&A

On orforglipron

Q (Terence Flynn, Morgan Stanley): A lot of focus is obviously on orforglipron and path-to-market. I was surprised that it wasn't on the first list of the Commissioner's National Priority Review Voucher program. Could you just comment on kind of you guys are seeking that voucher? Then if not, why not? Additionally, how to think about timelines for launch and some of the puts and takes as we think about consensus expectations for 2026?

A (Mr. David A. Ricks, Chair and CEO): As we've said before, we're interested in getting orforglipron to as many patients around the world as fast as we can, including those in the US. Without commenting on specific vehicles, investors can expect us to be pursuing in all the above strategy to get the medicine out more quickly.

Also, I'd point out that if you look at this new voucher program, orforglipron checks, at least three or four of the boxes laid out. So, we'll see. It's obviously a government decision about which pathway they choose and the review time itself. We're focused on speed here and we're ready to launch. The package will go in the quarter, and we hope to get approval as soon as we can after that.

Q (Seamus Fernandez, Guggenheim): I’m curious about some of the behaviors that we're seeing in the market around M&A and how the competitors' dynamics are playing out and how you, Dave and Dan see the market evolving from here. You've commented on retatrutide, perhaps segmenting the heavier patient population with greater comorbidities.

Orforglipron is potentially targeting a maintenance and lower end portion of the market that's massively scalable and you also have tirzepatide blowing the numbers out and potentially cornering the competitor to some degree in other markets.

Just wanted to get a sense of if that behavior would be concerning to you if you don't really spend much time thinking about it because you're so focused on your own business or if there are other considerations as you work to further segment the market and take a deeper leadership position?

A (Dr. Daniel Skovronsky, CSMO): Lilly's been focused on the obesity opportunity for quite some time. We have a very strong R&D engine behind it. When you look at where the science leads us and sort of every kind of reasonable or logical target to pursue, we have robust programs against those targets. In nearly every case we have either a best molecule or first for both.

Clearly, the late-stage clinical molecules that the Street is paying attention to, we like where they are. Behind it, I can assure you there's a robust pipeline that we like. No surprise then that every other company in this industry looks at that and wants to improve their own position. We watch that and of course pay attention but we haven't seen anything that changes our view about the competitiveness of our portfolio or the lead that we have in this space, which we intend to maintain through robust investments, not just in research and development, but as you've seen today, in multiple phase 3 trials and new indications.

A (Mr. Ricks): For a long time, we've all been saying we're focused on every logical target and pursuing the full extent of what these medicines can do for various conditions. Today's call highlights that with some of the new studies Dan highlighted. It's also important to note, in addition to innovation, you need to execute. This is a highly scaled business and reaching potentially tens or even hundreds of millions of people. Lilly has really done well. It's a combination of those two things that built the lead we have. We are very focused on both innovation, which Dan talked about, but also executing with manufacturing build-out in market performance new ways to reach consumers.

Of course, everybody would like to be in our position, but we're focused on defending it and mostly just executing the play we have. We'll probably see more dynamics and noise from other pharmaceutical manufacturers, that's normal. What we need to do is run the strategy out that we've outlined.

Q (Geoff Meacham, Citi): Just had another one on orforglipron. When you think about commercial strategy, would you characterize it as more consumer-centric through Lilly Direct, or should we think about it as a more typical pharma launch with PBM and payer negotiations being really critical on day one. I guess the puts and takes of both of those.

A (Mr. Ilya Yuffa, President of Lilly US): Obviously, we're excited about the profile of orforglipron and how to commercialize it in the US and outside the US as well. Obviously, we understand this similarly to how we've viewed Zepbound, where we need to drive great commercial and overall access for patients for accessibility, but we also recognize that there is significant demand in the consumer segment related to finding ways to get outside some of the frictions in the health care system.

So, we see both looking at broad coverage as well as looking at expanding how we do our direct-to-consumer platform and ensuring that every patient has the ability to access medicines across the portfolio.

Q (Asad Heider, Goldman Sachs): The cash pay channel is where you're continuing to see the most rapid growth in the obesity market, the bond vials are now almost 40% of new scripts. With US price elasticity, you saw a shift in volumes in the UK when Mounjaro prices increase.

What are the learnings from this for the Orforglipron ramp-up next year as it relates to the elasticity of demand across different price points? I guess my question is specifically related to how you're thinking about US versus OUS volume unlocks for Orforglipron as it launches in a world of potential MFN equilibrium prices?

A (Mr. Yuffa): We have experienced significant growth overall in the total market. We've seen sequential growth in the covered overall, the sequential growth is 15%, but we're seeing significant more volume go through a direct-to-consumer platform with Lilly Direct, which says a lot about, one, what consumers and patients as well as providers see as the benefit of Zepbound in particular and also the ability to remove some of the friction and the ability to have accessibility to medicine. We see this channel as a significant channel now and into the future.

Then as part of that, obviously, having more offerings, whether you include being able to pick up your Zepbound vial at a local Walmart, which we announced yesterday or expanding the offering on having another treatment like orforglipron, that's an important element for us to expand the ability for patients to get treated. That is the main goal that we have is to improve overall health outcomes, and we have multiple medicines and different platforms to achieve that.

A (Mr. Patrick Jonsson, President of Lilly International): Maybe just a few additions from an OUS perspective; first and foremost, in the U.K. with a raise in price that was effective September 1st, we learned pretty much what we expected to learn.

What we did was just to take the U.K. price rated to the level of a European price, and even if they have regulations in the U.K., we saw export of medicines out of U.K. to other markets.

Secondly, we're also learning something about consumer pricing elasticity, that exists. Most importantly, orforglipron will meet a slightly different need of the marketplace. We know that obesity is a heterogeneous disease. For people with a BMI below 35 that might not need tirzepatide, we believe that it's a significant opportunity in OUS and also driven by the other teachers that Ken referred to earlier, the opportunity to scale here and to reach up a patient populations and with no need of free duration, et cetera. Receivables as being very complementary in the OUS business setting as well.

Q (Dr. Alex Hammond, Wolfe Research): Can you walk us through the importance of the upcoming ATTAIN-MAINTAIN trial to orforglipron's commercial opportunity? Is there an outcome that might meaningfully change your view on how quickly orforglipron's launch may scale.

A (Dr. Kenneth Custer, President of Cardiometabolic health): This is a really first of its kind study, and we're looking forward to these data this year, we took advantage of the opportunity to rerandomize patients for the sema 5 study who were maximally tolerated on either semaglutide or tirzepatide, we randomized them to orforglipron or placebo, and we're going to measure the percentage of the weight that they lost over the course of 72 weeks that they keep off while taking orforglipron.

We don't know exactly what the results will be, but we're hopeful that that orforglipron will provide a simple once-daily oral option lets patients keep most of their weight off. This is really an opportunity to expand the market even further for orforglipron. Of course, we have very bullish expectations for it as a first-line starter incretin, but also this is an opportunity to you to grow that.

In terms of government, we don't see cannibalization in that way. This is an opportunity to grow the market at a very different rate, and the data from ATTAIN-MAINTAIN could be just an exciting boost and allow us to have some medical information to disseminate the physicians about how their patients switch from drugs like Wegovy and Zepbound. We also know that all management drugs are, of course, indicated for men. These are just data to help HCPs and patients who guide between these assets.

Q (Courtney Breen, AllianceBernstein): You’re preparing for a very large scale launch and by our calculations on the basis of some of the comments you made, you couldn't have enough doses to support five million patients for a full year based on the inventory sales. Dave, you mentioned this could be the GLP-1 for all. Can you help us understand kind of the potential for expansion to market with orforglipron and should we expect to see a slowdown and get on new starts during the initial period of that orforglipron.

A (Dr. Custer): Now with six Phase 3 studies in hand, we really understand the profile of this emerging medicine continues to recapitulate the efficacy and safety of injectable GLP-1s. In fact, Anne recapped some of that during the early part of the call, recapping the ATN2 data, which seemed very consistent with step two as well as the ACHIEVE-2 data showing superiority versus oral semaglutide.

This was a great profile. You're getting glucose benefits, waste benefits, improvements in blood pressure, lipids inflammatory markers all that in a simple once-daily pill with no restrictions on food and water and of course, which we can manufacture and distribute it at scale.

A different magnitude about the opportunity here than historically what we've with incretins. In the United States, there's probably 8 million or 8.5 million people on incretins out of maybe 170 million might benefit. Globally, that's a much bigger number, probably measured in the hundreds of millions or even billions. This is a generational opportunity to figure out how get to incretin to a much larger group of people.

We can do that through the simplicity of the profile, which is also easier to manufacture and distribute. Our plan will be about accomplishing that at international level, getting it out there as quickly as possible, of course, we're also developing with orforglipron in a lot of other settings beyond obesity and diabetes, can recap some of those new that we've announced, and of course, just to recap as well. We see an opportunity not just as a starter incretin here with Orforglipron, but also something that could potentially have been used for patients to continue the success they've had with the drug like Wegovy or Zepbound assessing that now in the ATTAIN-MAINTAIN study and look forward to sharing those data later this year.

Q (Akash Tewari, Jefferies): It was noted if orfoglipron was priced at $100 a month, there'd be no incentive for new medicines in that category to kind of create the next best thing. It was later noted that Lilly's already made billings of doses for orforglipron and it could have an impact on human health at a global level. Can Lilly achieve both goals of kind of preserving continuous innovation in obesity and having ortho be a drug for hundreds of millions of patients with the parity pricing model between the US and the rest of world.

A (Mr. Ricks): Yes, our strategy is to bridge both. Flatter pricing between the US and other developed countries is important, and there's three ways that that this works. One important thing here is just to point out on all these pricing questions that is different in this GLP-1 category is the consumer self-pay channel.

We haven't really seen that at scale in other categories, and it certainly is a channel here, partly because of underinsurance but partly because the benefits of these medicines manifest so consistently. There really aren't that many non-responders at all, and produce a very desirable short-term effect, in addition to enhancing long-term health benefits, it really is a unique situation. We have seen price elasticity, as was mentioned, and that it's, on the one hand, in our interest to offer consumers a compelling price where they can afford to self-pay.

It's also in our interest to continue to build out indications for chronic disease as Ken and Dan were outlining earlier, and we are committed to doing both, having a strong consumer offering, but also proving the health benefit and that should not compete for consumer dollars but for healthcare dollars, either government or from private payers. It's both and these can bridge because we have so much evidence coming of long-term benefit.

We should compete with other classes of medicines in chronic diseases or even create whole new classes, and at the same time, we'll probably continue to see consumer self-pay demand, whether it be for prevention or there are other needs. It is entirely possible to do both. Ken mentioned earlier some of the numbers, we are literally just scratching the surface of global treatment here. There really is a tremendous opportunity to reach tens or even hundreds of millions and more people in the coming years, and that’s our goal.

On Pricing

Q (Umer Raffat, Evercore): On the one hand, there's a lot of commentary on some of the expectations you've laid out on orforglipron pricing framework. If you could expand on that. On the other hand, there's a lot of actions and changes at your main competitor over the last few months, and I almost wonder, do you think they will stay a mature player from a pricing front, or will that no longer be a base case for us?

A (Mr. Lucas Montarce, CFO): Thinking about the pricing dynamics when you unpack our Q3 performance, you see that our pricing continued to perform as what we expected, so it's a good data going after the CVS move that we didn't see again, a significant price erosion, but was very much in line to what we said early in the year for the full year as well. It potentially just had a good data point that you can take from that perspective.

Thinking more broadly about the competition in the marketplace. Again, we always pay close attention on the competition in the marketplace, how we differentiate both commercially, but also on the level of the product. Ilya, Dan, and Ken mentioned the differentiation. And you see that in marketplace. If you take, for example, a good proxy that for me is really direct we have been priced over the last maybe six months already at that starting point at 349 going to 499 and maintain that price and you see the penetration and the competition is placed at the same level as well. We don't see materially change in the dynamics that we see from that perspective and as we continue to penetrate the market and mobilize patients to seek more treatment.

Q (Tim Anderson, Bank of America): With Novo's sema, we get IRA negotiated price within the next month. My sense from talking to some industry folks is that negotiated price may be more favorable in the investment community is expecting, meaning less degradation to the current net price. That would be good for everyone in the space.

What is Lilly picking up on this, and whatever that level of discounting, do you agree that it quite likely has a direct impact on pricing of Lilly's owned products in 2027, or do you think some has negotiated price just won't translate across?

A (Mr. Yuffa): Obviously, we don't know the price has been negotiated. At the same time, there are several things that are important to note. One, that it only applies to sema in Part D beginning in 2027. Overall, if you look at our volumes, Medicare Part D is a small proportion of our overall volume.

Obviously, predominantly in type 2 diabetes and there's lack of coverage in obesity. The most important element to the good here is that tirzepatide has demonstrated superior efficacy versus sema in head-to-head trials, which is a strong foundation for any value-based discussions that we have with payers, not only in our data, but you see that as well in provider preference as well as patient preference that you see in the market.

A (Mr. Ricks): Maybe just one thing because we've been talking about orforglipron and its upcoming launch. We see single-acting GLP-1s as one category in double and triple acting as well as others, but both weight loss and clinical value will be quite different between these medicines, and of course, we're paying close attention to the sema price. As Ilya said, it's a Part D only channel. We’re in a good position because we have so many options.

On Mounjaro

Q (Chris Schott from JPMorgan): In terms of the Mounjaro international ramp, it's obviously had an impressive step up in sales these past two quarters. Can you just elaborate a little bit more on how some of these new country launches are trending relative to your expectations? How to think about growth off this new higher base, and is there any meaningful stocking as we appreciate to kind of look at these numbers? Just a little bit more color on what's been driving this big step-up.

Q (Mr. Patrick Jonsson, President of Lilly International): We are very encouraged by what we're seeing outside of the US, and the business that we shared earlier is 75% out-of-pocket and 25% type 2 diabetes.

What we have seen is an initial stocking in both markets where we launched, and we refer to the big ones being in Q2 in China, Brazil, Mexico, and India. We have seen at least in the performance also in those markets in Q3 and continued very strong performance globally.

Looking forward, the major opportunity is number one in T2D. We have reimbursed on care in the P&A market and we'll continue those efforts across all US markets, but that's going to take some time.

Secondly, the big opportunity when it comes to obesity, it's about patient activation, and we will lean in on all of those efforts also in 2026.

When you look at international, it's important to understand that in reference to the income statement, we are referring to more than 55 countries and our different market dynamics, different buying patterns. As we have seen over the last several quarters, it's not going to be a straight line, but there are significant opportunities outside of the U.S. also moving forward across type 2 and chronic weight management.

On Cigna’s new toward rebate-free pharmacy benefit model

Q (James Shin, Deutsche Bank): David, you previously mentioned narrowing the gap between list and net pricing. Cigna recently announced drug rebates would be replaced with GPO fees, and it sounds like that leads to greater discounts as well as more employers opt-ins. Does that suggest greater GTN pressure than we normally have with the rebates and just make clinical profile is more relevant to format positioning or access? Like what kind of changes should we expect?

A (Mr. Ricks): Yes, and I'd also point out, increasing share in large employer market from kind of non-traditional PBMs, I guess we call them I applaud this. It’s a good move for innovators. It's a good move for patients. It's a good move for payers, for the commercial payers and probably smart of Cigna to make this first move to recoup market share or gain market share.

Everyone wants more transparency and lower out-of-pocket for patients. This kind of model will produce both of those. What we want is to make the basis of competition, one of clinical differentiation that doctors and patients both appreciate in a way, the non-transparent rebates and other behind the scenes activities that determine which medicine a patient gets is not in our interest.

As an innovator, probably the leading spender on innovation in the sector coming up, we're for this. David and his team at Cigna did a good thing here, and we hope others follow in the market in the US can rapidly transition to such a system.

What we hope is that more valuable medicines will have value recognized in pricing and less valuable medicines will have a harder time competing now because you can't just rebate away some number and find formulary position ahead of a better medicine. We are in support of this, and again, it's a good move; hats off to David Cordani and the team. Hopefully, others rapidly follow.

--by Kayla Mathieu, Elizabeth Rose, Kat Moon, Esther Min, Monica Oxenreiter, and Kelly Close