Insulet 4Q25 – Full-year revenue reaches $2.7 billion (+30%); record new customer starts with over 40% with T2D; continued R&D investment support pipeline momentum –

Executive Highlights

- Insulet announced its 4Q25 and full-year 2025 financial results on a call today led by CEO Ms. Ashley McEvoy, CFO Ms. Flavia Pease, and COO Mr. Eric Benjamin (see press release, presentation, and webcast).

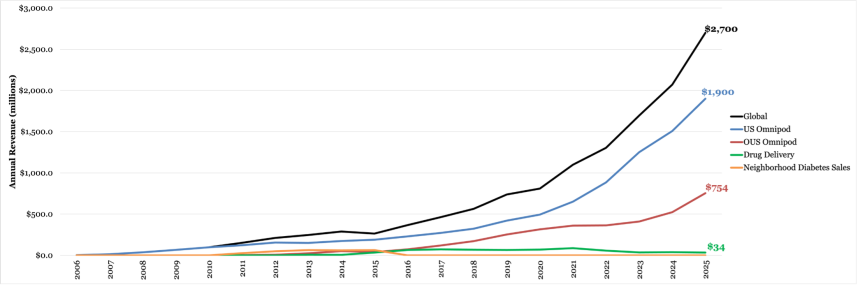

- Insulet’s 4Q25 revenue totaled a record $784 million, up 31% from 4Q24 and up 11% sequentially. Insulet reported $2.7 billion in full-year 2025 Omnipod revenue, up 30% from 2024.

- US Omnipod revenue in 4Q25 totaled a record $568 million, up 28% from 4Q24 and up 14% sequentially. Insulet reported $1.9 billion in full-year 2025 US Omnipod revenue, up 27% from 2024.

- International Omnipod revenue in 4Q25 was $214 million, up a significant 51% from 4Q24 and up 6% sequentially. Insulet reported $754 million in full-year 2025 international Omnipod revenue, up 44% from 2024.

- Insulet reported record new customer starts across both the US and international markets in 4Q25 and full year 2025. In the US, Insulet reported year-over-year growth in new customer starts with T1D in 4Q25 and full-year 2025, with almost all (over 85%) coming from MDI. New customer starts with T2D grew significantly in 4Q25 sequentially and YOY, with T2D representing over 40% of new US patient starts, up from over 25% at the time of FDA clearance. Omnipod 5 saw strong YOY and sequential growth in new customer starts internationally as well.

- As part of Insulet’s broader strategy for the rest of this decade, management highlighted several planned developments:

- The integration of the FreeStyle Libre 3 Plus CGM with Omnipod 5 is planned for the first half of 2026; the company has initiated a limited market release of the integration.

- Key algorithm updates – a 100 mg/dL glucose target, greater time in automated mode, and improved responsiveness to enhance the user experience – will also enter a full launch in 2026, with a limited market release now underway.

- The STRIVE trial evaluating the SmartAdjust 2.0 algorithm against the current SmartAdjust algorithm was completed in November 2025. Insulet plans to publish the pivotal results at ADA 2026.

- Insulet also completed enrollment in the EVOLUTION2 T2D feasibility study for the company’s fully closed-loop system in 2025.

- For full-year 2026, Insulet guided to 20-22% total company revenue growth (~$3.25-$3.3 billion) and 21-23% Omnipod revenue growth. It also aligns with continued expansion following the first full year of US Omnipod 5 for T2D and of recent international launches. For 1Q26, management expects total company growth of 25-27%, including Omnipod revenue growth of 28-30%.

Table of Contents

-

Financial Highlights

- 1. Record 4Q25 revenue of $784M (+29%) and full-year 2025 revenue of $2.7B (+30%); US Omnipod 4Q25 revenue totals $568M (+28%)

- 2. Management issues 2026 guidance of $3.2-$3.3 billion (+20-22%); 1Q26 total company growth of 25-27%

- 3. 4Q25 gross margin expands to 72.5%; annual free cash flow of $378 million

- Omnipod Highlights

-

Pipeline Highlights

- 1. CGM interoperability expands: FreeStyle Libre 3 Plus integration planned; algorithm enhancements in 2026

- 2. SECURE-T2D and RADIANT trials published; STRIVE study for Omnipod 6 complete; pivotal EVOLUTION initiation in 2026 for fully closed-loop

- 3. Omnipod Discover global rollout planned for 2026; Omnipod 6 planned for 2027 with single updatable pod

- Analyst Q&A

- Close Concerns’ Questions

Insulet’s Global Revenue (2006 – 2025)

Financial Highlights

1. Record 4Q25 revenue of $784M (+29%) and full-year 2025 revenue of $2.7B (+30%); US Omnipod 4Q25 revenue totals $568M (+28%)

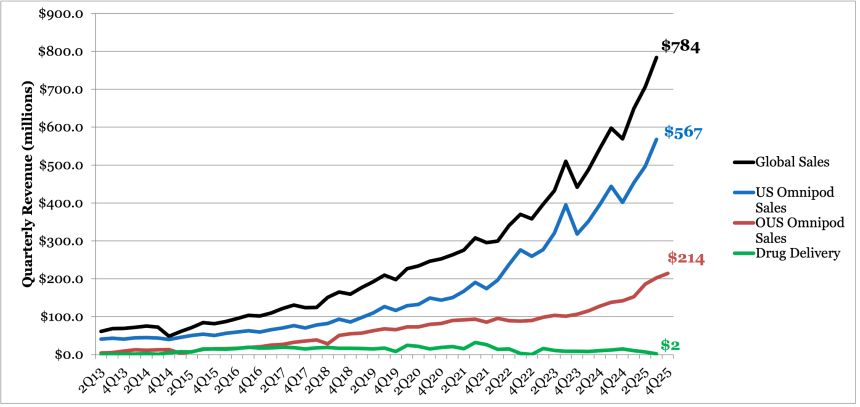

Quarterly Global Revenue (2Q13 – 4Q25)

Insulet’s 4Q25 revenue totaled a record $784 million, up 29% from 4Q24 and 11% sequentially. Insulet reported $2.7 billion in full-year 2025 Omnipod revenue, up 30% from 2024. Growth reflected sustained global demand for Omnipod 5, with over 85% of new customer starts coming from multiple daily injections (MDI) and over 40% from T2D in 4Q25. Ms. McEvoy said strong utilization and retention rates globally also contributed to this growth.

- US Omnipod revenue in 4Q25 totaled a record $568 million, up 28% from 4Q24 and up 14% sequentially. Insulet reported $1.9 billion in full-year 2025 US Omnipod revenue, up 27% from 2024, consistent with its 3Q25 guidance of $1.9-$1.92 billion (+26-27%).

- International Omnipod revenue in 4Q25 totaled $214 million, up a significant 51% from 4Q24 and 6% sequentially. Insulet reported $754 million in full-year 2025 international Omnipod revenue, up 44% from 2024. This exceeded previous Insulet’s previous guidance from 3Q25, which projected revenue of $722-$728 million (+38-39%).

- International growth was attributed primarily to volume and solid performance in core European markets, including the UK, Germany, and France. Ms. McEvoy noted robust uptake following Omnipod 5 launches in Canada and Australia. In Canada, reimbursement expansion to half of all provinces supported over 60% growth in new customer starts, and Australian new customer starts more than tripled post-launch. Geographic expansion also contributed to growth, with Omnipod 5 now available in 19 countries.

- Drug Delivery revenue totaled $2 million in 4Q25, down 83% from 4Q24 and down 72% sequentially.

2. Management issues 2026 guidance of $3.2-$3.3 billion (+20-22%); 1Q26 total company growth of 25-27%

For full-year 2026, Insulet guided to 20-22% total company revenue growth (~$3.25-$3.3 billion) and 21-23% Omnipod revenue growth ($3.24-$3.29 billion). This guidance reflects continued penetration across US T1D and T2D populations, as well as in international markets. It also aligns with expectations of continued expansion following the first full year of Omnipod 5 for adults with T2D in the US and recent international launches.

- For 1Q26, management expects total company growth of 25-27% (representing revenue of ~$711-$723 million), including Omnipod revenue growth of 28-30% (~$709-$720 million). In the US, Omnipod growth is expected to be 24–26% ($498-$506 million) and internationally, growth is expected to be 37–39% (~$209-$212 million), with foreign exchange expected to provide a modest tailwind.

- In full-year 2026 US Omnipod sales, Insulet guided to 20-22% growth (~$2.3-$2.34 billion), which Ms. Pease said was primarily driven by continued new customer starts, increasing penetration among MDI users, and momentum in T2D following strong adoption in 2025.

- For full-year 2026 OUS Omnipod revenue, Insulet guided to 24-26% growth ($935-$950 million). Ms. Pease said this would be supported by new customer starts as Insulet penetrated further into current markets and expanded Omnipod 5 into additional markets. She also noted that international guidance assumes stable utilization and slightly greater retention rates from 2026 compared to 2025.

3. 4Q25 gross margin expands to 72.5%; annual free cash flow of $378 million

Gross margin in 4Q25 reached 72.5%, while full-year 2025 gross margin expanded to 71.6%. This improvement was supported by top-line growth, and Ms. Pease also noted manufacturing productivity gains at Insulet’s Acton and Malaysia facilities.

- Insulet ended 2025 with $716 million in cash, cash equivalents, and short-term investments, down from $953 million in 2024.

- Insulet reported an adjusted net income of $109 million in 4Q25, representing ~14% of revenue, up from $58 million in 3Q25.

- Insulet reported $569 million in net cash from operating activities in 2025, up from $430 million in 2024.

- Insulet reported $378 million in free cash flow in 2025, compared with $305 million in 2024.

- Both Ms. Pease and Ms. McEvoy highlighted increased investing in R&D. R&D spending totaled $91 million in 4Q25, up 50% from 3Q25. This represents ~12% of total revenue, an increase from ~10% of total revenue in 4Q24. Full-year 2025 R&D spending was $301 million, up 37% from 2024 and representing ~11% of total revenue. The higher R&D spending is aligned with Insulet’s aggressive investment in its pipeline, including Omnipod 6, a fully closed-loop system for T2D, and ongoing work with the STRIVE and EVOLUTION trials.

Omnipod Highlights

1. Record new customer starts globally, with growing US T2D contribution

Insulet reported record new customer starts across both the US and international markets in 4Q25 and full year 2025, with the vast majority of people coming from MDI.

- In the US, Insulet reported year-over-year growth in new customer starts with T1D in 4Q25 and full-year 2025, driven by strong patient and prescriber preference for Omnipod. Almost all (over 85%) came from MDI. Ms. McEvoy attributed some of this strength to Omnipod’s broad market access, available in approximately 48,000 pharmacies and covered for more than 90% of insured lives (~300 million of the 317 million insured people in the country). Ms. McEvoy also pointed to positive impact of Insulet’s direct-to-consumer (DTC) campaigns, which are generating record lead volume in new patients and subsequently activating new prescribers aware of Omnipod 5.

- In T2D, new customer starts grew significantly in 4Q25, both sequentially and year-over-year. T2D represented over 40% of all new patient starts in the US, underscoring the significant expansion of this customer segment since Omnipod 5 received FDA clearance for use in the population in August 2024 – at that time, T2D made up over 25% of new starts. Ms. McEvoy pointed to strong clinical and real-world outcomes and the strengthened ADA guidelines in the 2026 Standards of Care now recommending AID as the preferred insulin delivery system for people with T2D who require insulin. Ms. McEvoy suggested the availability of Insulet’s fully closed-loop (FCL) algorithm in 2028 will enable further penetration of the T2D market and those being cared for by primary care providers (see more below).

- Internationally, Omnipod 5 saw strong year-over-year and sequential growth in new customer starts, supported by new sensor integrations such as Insulet’s launch with Dexcom G7 in Germany. The company reported that its Omnipod 5 launches in Canada and Australia already delivered robust growth – new customer starts increased 60% with Omnipod 5 reimbursement in half of Canada’s provinces, and new customer starts more than tripled following the launch of Omnipod 5 in Australia.

- Ms. McEvoy reiterated that all populations – US T1D, US T2D, and OUS T1D – remain underpenetrated and there is still significant room to expand the insulin delivery and AID market. The company’s estimated global utilization and annualized retention rate remained roughly stable for 4Q25 and full-year 2025.

2. Omnipod 5 now available in 19 countries, with Spain planned for late 2026 launch

Omnipod 5 is available in 19 countries as of today, with nine new countries added in 2025 alone. Collectively, the company reported that these nine markets delivered growth in line with the UK and Germany combined – two of its strongest in Europe – in 2025. Ms. McEvoy said that Insulet’s global expansion will continue in 2026, beginning with Omnipod 5 and Omnipod Discover’s recent launches in the Middle East. Spain will soon follow, with an Omnipod 5 launch expected “later this year.”

- Insulet continues to invest in manufacturing capacity to support expand patient bases and broader global availability. This included further expansion of its Malaysia manufacturing facility with additional lines coming online and the start of development of Insulet’s new facility in Costa Rica, which is expected to be operational in 2029.

3. US prescriber base expands to over 30,000 HCPs (+28%); T2D prescriber base grows to over 6,500 clinicians (+62%)

Insulet management highlighted the company’s prescriber base expansion beyond traditional endocrinology ecosystems in the US. Insulet’s US prescriber base now includes more than 30,000 healthcare professionals, up 28% from nearly 24,000 in 2024. This has been driven in part by its prescriber base for T2D, which grew 62% from 2024 to more than 6,500 clinicians. Ms. McEvoy highlighted that its US sales force has focused on reaching high prescribing offices that treat both T1D and T2D, even as most people with T2D are managed in primary care settings. Insulet expanded its sales force by around 25% in 2025 to support these efforts.

Pipeline Highlights

1. CGM interoperability expands: FreeStyle Libre 3 Plus integration planned; algorithm enhancements in 2026

As part of Insulet’s broader strategy for the rest of this decade, management highlighted several developments that are planned for 2026.

- The integration of the FreeStyle Libre 3 Plus CGM with Omnipod 5 is planned for the first half of 2026. The company has initiated a limited market release of the integration. Previously, the company launched FreeStyle Libre 2 Plus integration for users in several markets, including the UK, Netherlands, US, Italy, Belgium, Switzerland, France, Saudi Arabia, Kuwait, UAE, Israel, the Nordic countries, and Australia. Omnipod 5 has also integrated with the Dexcom G7 15 Day sensor upon its launch in December 2025.

- Key algorithm updates will also enter a full launch in 2026, with a limited market release now underway. These updates will enable a 100 mg/dL set point target for tighter glycemic control, increase the time spent in automated mode, and include responsiveness improvements to enhance the user experience and clinical outcomes.

- Omnipod Discover will also continue to roll out in 2026. The new data platform is designed to deliver streamlined insights to support the efficient review of Omnipod 5 data by healthcare professionals and enable confident prescribing. Earlier this month, the platform launched in Saudi Arabia, Kuwait, Qatar, and the United Arab Emirates following a limited release in the US.

2. SECURE-T2D and RADIANT trials published; STRIVE study for Omnipod 6 complete; pivotal EVOLUTION initiation in 2026 for fully closed-loop

Management highlighted Insulet’s progress in clinical research and publications, as well as plans to launch further studies towards a fully closed-loop system.

- SECURE-T2D: Full results from the trial were presented at ATTD 2023 and were published in JAMA Network in 2025. In a first-ever Omnipod 5 real-world dataset (n=31,691), users with a 110 mg/dL target (n=17,339) achieved a Time in Range of 71%. A substantial difference in outcomes was seen based on the aggressivity of target glucose levels.

- RADIANT: Full 26-week RADIANT trial results were presented at ATTD-Asia 2025. Data showed sustained glycemic improvements with the use of Omnipod 5 and FreeStyle Libre 2. A1c remained stable at 7.2% for those continuously on Omnipod 5 from Weeks 13 to 26. Participants who switched from MDI to Omnipod 5 at 13 weeks saw their A1c decrease by 0.7% (from 8.0% to 7.3%) by 26 weeks (p <0.0001).

- STRIVE: The trial (n=132) evaluating the SmartAdjust 2.0 algorithm against the current SmartAdjust algorithm was completed in November 2025. Insulet plans to publish the pivotal results at ADA 2026.

- EVOLUTION: In 2025, Insulet also completed enrollment for the EVOLUTION2 T2D feasibility study for its next-generation fully closed-loop algorithm. Preliminary results from the algorithm were presented at ATTD 2024. The 11-week, 72-participant trial in New Zealand saw an increase of about five hours/day TIR (+20%) in 12 adolescents with T1D and roughly three hours/day (+13%) in eight adults with T1D, without a significant increase in hypoglycemia. Insulet plans to present results from EVOLUTION2 at ATTD 2026.

3. Omnipod Discover global rollout planned for 2026; Omnipod 6 planned for 2027 with single updatable pod

Ms. McEvoy outlined continued progress across Insulet’s digital and next-generation platform strategy, highlighting the global rollout of Omnipod Discover in 2026 and advancement of Omnipod 6 toward a planned 2027 launch. She framed these initiatives as aimed at reducing clinical burden and simplifying onboarding among users.

- Omnipod Discover is a new data platform designed to streamline provider workflows and simplify interpretation of Omnipod 5 data, delivering clear insights to support more efficient decision-making and confident prescribing. Ms. McEvoy noted that Omnipod Discover also improves the onboarding by reducing startup complexity and enabling faster initiation for new users. The platform has already debuted in four recently launched Middle East markets (Saudi Arabia, Kuwait, Qatar, and the UAE) and is expected to rollout globally in 2026.

- Omnipod 6, planned for 2027, is being developed as a next-generation AID system featuring improved connectivity, more personalized automation, and enhanced flexibility in on-body placement. Ms. McEvoy said pivotal STRIVE study data is expected to be presented at ADA 2026, supporting continued development and future regulatory submission ahead of launch.

- Ms. McEvoy reiterated that Omnipod 6 will be a single, updatable pod design compatible across all major CGM systems. This will allow for smoother real-time software updates and faster implementation of new features, without requiring new hardware purchases. This design is intended to simultaneously improve user outcomes and wear experience, but also accelerate Insulet’s innovation cycle.

Analyst Q&A

On Insulet’s competitive positioning

Q (Jeff Johnson, Baird): Ashley, I just want to start from a high level maybe with the first question here. You're couple months away from your one-year anniversary leading Insulet. Stock has had a great run in the first six months of your tenure. It's faced maybe some challenges here the last five or six months. What do you think is the most underappreciated part of the Insulet story at this point, especially from an investor perspective?

Ms. Ashley McEvoy, President & CEO: Thanks for the question, and it's great to see Insulet continue to execute and live into our commitments that we shared in November at our Investor Day. I would highlight four key areas. Number one is our tech lead, which we'll continue to innovate off. I'll come back to that. I would say, number two is our growing commercial prowess, I'll come back to that. Three is our manufacturing at scale, and four is our financial strength.

I'll start with just our tech lead. As we shared, we've invested over $3 billion to get here. Omnipod 5, we're just 3.5 years into the launch, into the US, 2.5 years in places like the UK and Germany. And we continue to post record NCS. This knowledge, this experience, and this tech lead really continue to prove the leadership that's resulted in number one most prescribed and number one most requested. And importantly, in my opening remarks, I really shared how we've built this meaningful pipeline that really addresses the biggest unmet needs in the market. And you heard us touch around really two algorithm improvements. Starting actually this weekend, we launched a limited market release with Omnipod 5 with a lower set point, advanced automated mode. It connects with FreeStyle Libre 3. We're going to be launching our new data platform, so that will be going out into full market release in a couple months. We will also be launching our third-generation algorithm with Omnipod 6. As we mentioned in our opening remarks, we're going to be posting the data and the algorithm at the ADA. This is a meaningful advancement in personal automation as well as over-the-air connectivity, as well as on-the-body placement with a lot of variability, which is important for patients, as well as a 1-pod. And you're going to hear us talk about – there's been a lot of noise, if you will, in the industry, which is really good things for patients – around this fully closed-loop. We believe that we are in a class by ourselves of how we're going to define what fully closed-loop really means. I'll come back to that in inquiry. But it's a very strong pipeline.

And then our commercial prowess I think is really underappreciated. We have the largest sales force in the industry. We're going to evolve that sales force for messaging from selling on simplicity and ease of use and our highly differentiated technology to our strength of clinical performance. I'll come back to that. And then, as Flavia was mentioning in her opening remarks, 30,000 prescribers with Omnipod, which is up 28%. Very strong brand loyalty and we continue to have unparalleled access and affordability.

We manufacture at scale. It's one thing to get regulatory approval, it's different thing to manufacture. We produce tens of millions of pods with high-quality, medical grade quality at consumer electronic scale. And when we say something, we execute on what we're going to say. I'm really pleased the team is building out Malaysia. We're already margin accretive in Malaysia. In Acton, we've improved productivity, and we've already started to break ground on Costa Rica.

And last is just the financial wherewithal, I mean, not only our recurring revenue model, 70% gross margin, expanding operating margin, EPS above revenue, and cash-flow positive. So, those are perhaps underappreciated tenets of the Insulet company.

Q (Danielle Antalffy, UBS): My question is on the competitive moat. Ashley, you touched on this earlier. I do think it's underappreciated. I specifically wanted to see if you could talk a little bit about the sampling at the physician's office and sort of if you could walk through how this works, like who trains the patient to ensure they get the optimal experience and appreciate it's still early, but what are you seeing for capture rates with that program?

Ms. McEvoy: I think the company is best known for just having really differentiated technology and investing ahead of the curve in supply chain and maybe pioneering this pharmacy pay-as-you-go model. What I would like to see at the end of this year is a better appreciation of the commercial prowess that we've been building over the past couple years. So, we have been expanding our sales force. We expanded it around 25% last year. We're continuing to do that. We call on over 17,000, so full coverage of the endos, really 10,000 of the highest prescribers. What we're evolving is our messaging, as I mentioned earlier, in addition to selling what they've come to love, which is really this differentiated technology platform that's simple and easy to use. It's why it's the gateway to the category to new users, it's easy for them to explain. They’re also educating on our really strong clinical performance. We will continue that messaging in 2026.

To make it easier to get people on Omnipod, we're also the only AID offering that can really get people on a sample. Right in the practice, they can go put a pod. It's a very capital efficient way for us to initiate trial. We've gotten a lot of really good feedback both from young children as well as grandparents around that moment of delight. Once they try it on, they get the wow factor, and we have very strong conversion ratios.

In addition to the called-on universe, we also have activate directly to consumer, make them aware of the category, make them aware of Omnipod 5, and people go in and ask for doctors for that and they specifically ask for Omnipod and that's a new category user. Those then become new patients but they also become new prescribers and that's why you heard us talk about – when we ended the year we had 30,000 prescribers writing for Omnipod which is up 28%. And we're going to continue that flywheel of really creating the market and creating demand for Omnipod.

On new patient start trends

Q (Robbie Marcus, JPMorgan): I wanted to ask on new patient start trends, US and outside the US. And we've seen some of your competitors stumble a bit on new patient adds recently. You mentioned record new patient starts, I believe that's US and outside the US, but you could clarify that if I'm wrong. How are you thinking about finding sources of sustainability in the new patient growth? Type 2 is clearly a home run for you in the US. How do you keep that growing and getting larger and larger and continuing to win there? And then same question, outside the US, you've been moving into new geographies. How do you sustain your number one share there and continue to grow that over time?

Ms. McEvoy: As I mentioned before, I think, at Investor Day, we enjoy very balanced growth from the US and OUS. We did enjoy record new customer starts in the US as well as OUS. And our role as a category leader, as we shared, we've generated about 65% of the market growth has come from Insulet. And that really is the primary source of our volume are coming from people not in the category, and those are people on multiple daily injections. And so, we engineer our innovations to bring new customers into the market. About 10% of ours comes from switching, and we are switching from competitive AID, but our primary source is coming from MDI.

And that, we can go into type 1 where we continue to improve new customer starts and post new records, both in the US as well as OUS. In the US, that's backed by strong ADA guidelines. We mentioned that 40% of people are on AID therapy, meaning there's still a lot of room. When CGM has 70% penetration, there's a 30-point spread. So, it’s backed by science, and we’re working to really educate on our very strong clinical performance as well as the unparalleled access and affordability in type 1. Type 2, Robbie, you mentioned we're at the nascent stages, at 5% penetration. We have a very strong value proposition. We have very strong science. You're going to hear us talk more about kind of our strategic pivot taking advantage of the largest channel of the number one sales force in the US of migrating from really sharing our differentiated technology into proven clinical outcomes.

It's something quite frankly we own. There's a bit of a misperception in the marketplace that we have to correct and stand, and set the record straight, which is in addition to our preferred form factor and preferred user experience, we have very robust clinical performance on A1c reduction and improved Time in Range. Not just in our clinical trials, but importantly, in two independent studies just recently that compared AID systems, Omnipod's A1c was unsurpassed and our Time in Range was similar. So, we're going to take that message and that science to the largest channel of our P&L, which is our field force.

Q (David Roman, Goldman Sachs): Can you help us reconcile script trends to what you're seeing in reported revenue? I think this was a dynamic that caused quite a lot of noise intra-quarter. So, can you maybe size up how new patient start trends and volume growth compares to revenue? And if script data is not the right barometer, what should investors be using to track performance?

Ms. Flavia Pease, CFO: Yes, we know there had been a lot of questions around script data during the fourth quarter. As a reminder and we talked a little bit about this in the JPMorgan conference in January. If you were going to use script data, the best would be to use total pods as that's a best reflection of the future revenue outlook. If the total pod data is not available, you can use total scripts. It will not capture potential changes to longer script fills, going from a 30-day to a 60-day to a 90-day, but it's also a good second-best option.

And then finally, you can use NBRx, but there is a little bit of noise on NBRx because of samples and also different channels, specialty channel is not captured there as you use IQVIA data. And then finally in the fourth quarter, there's a little bit of I would say, seasonality where you see higher volume going through wholesale with specialty pharma than in other quarters which is not necessarily captured in script data but affects revenue. So, there are a few items that folks have to take into consideration when they extrapolate from scripts into dollars of revenue.

Q (David Roman, Goldman Sachs): Are you willing to provide the difference between new patient start growth and overall revenue performance?

Ms. Pease: We'll continue to provide qualitative commentary on the strength of our new customer starts. And we talk about them. Ashley just mentioned the strong performance in both US and OUS and the continued growth that we see as we continue to expand penetration of AID. But we're not going to provide specificity on new customer start growth rates.

Q (Richard Newitter, Truist): I think you said you exited the year at about 40% of new patient starts. I guess that would seem to imply that your Type 1 segment maybe saw moderating growth leveling off in the single-digit range. I guess, is that the right way to think of it going forward? And if so, what is that, is that share? Is that just the market kind of – has started to moderate and we're getting near maturity?

Ms. Pease: We had very strong type 2 performance in the fourth quarter and there was a continuation of that strength throughout the year. We had record new customers starts for both US and international both year-over-year and sequentially.

To your point, Richard, type 1, it grew nicely year-over-year and it was comparable to the third quarter, which was a record quarter for us in NCS. The level of penetration obviously in type 1 is higher than type 2. And as we continue to bring AID into those markets, you will see an accelerating growth in Type 2 just given that it's 5% today versus Type 1 at 40% penetration of AID.

But we continue to source a lot of our volume from MDI as we talked about, 85%, and that's really our strategy to drive that penetration in those customer segments and internationally which is also still very underpenetrated.

Mr. Benjamin: I think as Flavia described, type 1 in the US is more penetrated and the level of new customer starts in the market is high and so it continues to be a significant driver of growth. Ashley described it well. We've got a balanced growth portfolio and type 1 is a big part of that.

Type 2, the level of new customer starts in the market has been low and we are accelerating that as we launch Omnipod 5 with type 2 and did so over the course of 2025, which is why you saw that mix grow. You also saw our type 1 new customer starts outside the US grow significantly year-over-year and those three levers, US type 1, US type 2, international type 1 are going to contribute a balanced contribution to our growth over time.

On 2026 guidance and competition

Q (Larry Biegelsen, Wells Fargo): Ashley, you're guiding to 21% to 23% Omnipod growth for 2026. And you gave a three-year LRP of 20% recently. How are you feeling about being able to sustain the 20% growth in light of new competition? And anything new you can offer on why you think investor concerns around competition are overblown? Do you think it's going to be harder for new companies to scale or compete directly with Insulet in the patch pump market or do you think their entries will have a rising tide effect?

Ms. McEvoy: I'm really pleased to see the confidence in the company even increase since our Investor Day that we shared in November. As we come as a company out of stealth mode to the position of market leadership, performance trumps everything. I'll go back to some elements that I think are maybe underappreciated. Getting regulatory approval is not really the definition of impact. And we have this 25-year head start with again $3 billion of investment that's enabled us a lot of knowledge, a lot of tech know-how, a lot of experience on scale.

And I think in this marketplace, if you look at history, there's been a lot of attempts because it is an attractive market. But I will tell you there are a lot of barriers to entry. And those really come down to manufacturing at scale with high quality. It has to go to continuing to innovate with clinical performance and really unlocking the TAM. What's going to enable us to deliver the top-tier performance is by continuing to bring new users into this category. And our pipeline is specifically designed to bring new users from MDI into the category. And I think the biggest unmet need for us is to really start to improve the acumen among the clinical base, particularly in the US, of our strong clinical performance.

So, in addition to being number one prescribed and number one most requested predominantly because of our differentiated form factor and user experience, we also want them to know and be well aware of just the strong proven clinical performance both efficacy and safety and unsurpassed in the category. I think that will be new information for many more clinicians. And then I'm going to come back to just continuing to build on our commercial prowess as we go. Larry, again, I think this company has been known as being really good at technology and really good at the supply chain.

What's perhaps underappreciated is this evolving commercial of having the largest sales force, selling on science – we're bringing new prescribers into the category. We have this beloved brand that we are activating. When we activate DTC, we generate record new leads into the category. We're converting those leads into brand loyalty. They become new Omnipod podders. And then we continue to have unparalleled access and affordability. We've been in the pharmacy channel for nine years and we've built remarkable relationships with the payers and the PBMs because we have very strong clinical and economic evidence and we're going to take that strength and continue because 100% of our portfolio is in pharmacy. So, while others may be at 10% or 30%, Omnipod's been at this for nine years and will continue to have unparalleled access and affordability.

Ms. Pease: One final add is also the financial strength that we have. We have best-in-class gross margin which has built through these investments that Ashley talked about over the years. We are free cash flow positive and that strength allows us to continue investing in the business while at the same time being able to expand margins. And that investment is in innovation. It is in unlocking the market with AID penetration and is also in capacity to invest ahead of demand when you are in a disposable form factor construct.

Ms. McEvoy: As we shared, Larry, we got $1 billion that we're going to invest in R&D in just the next three years and we also are planning new next-generation platforms beyond the three-year window to stay ahead.

Q (Travis Steed, Bank of America): You talked about changing your guidance philosophy, so I just wanted to make sure we had an understanding of how you are going to set this year's guidance versus prior years and kind of what's been kind of baked-in into 2026 versus kind of what's left for upside. And do you expect record new starts in Q1 as well?

Ms. Pease: We continue to set guidance with a full intent to deliver. That has not changed. The guidance that we provided today reflects a balanced view of our outlook at this point. And we will experience normal seasonality in the first quarter which has been the case historically between fourth quarter and first quarter. But outside of that, we are very confident and pleased to be able to provide an outlook of 25% to 27% for the first quarter and 20% to 22% for the full year.

Q (Richard Newitter, Truist): Can you put some assumption bars around the upper and lower ends of your range or maybe said another way, what would have to happen to the biggest needle mover in your assumption set to be at the upper end or above?

Ms. Pease: Well, we provided a guidance range. So, to me, that is the upper and lower end of the bars that you're describing, Richard. And I think we obviously, as I said earlier, we continue to set guidance with the full intent of delivering and this is our best outlook at this point given where we are in the year. Obviously, if we can advance AID penetration even further and faster, that will translate into us being closer to the top end of the range.

On G7 15 Day integration

Q (Michael Polark, Wolfe Research): I have a question on one of your sensor partners. So, G7 is moving to 15-day from 10-day. Is this a different pod for Insulet or is this the same pod? And if it's a different pod, can you comment on the company's readiness to provide integration with the 15-day sensor? I'm remembering back to 2024, it took some time for the G7 Pod to become widely available and I think it suppressed starts for a period of time before it was widely available, so I'd like to understand the dynamics around the move from Dexcom to 15-day.

Mr. Eric Benjamin, COO: As a reminder, we were ready with the 15-day launch day one with Dexcom. So, Omnipod 5 is compatible with the 15-day G7 now. And that's a great experience for customers. It's been one of the key things we've been focused on, as you know, Mike, with accelerating sensor integration for customers. We were ready day one with 15-day. As Ashley mentioned earlier, we began the limited market release of our FreeStyle Libre Plus integration just recently, and we're excited to bring that to market in the first half of 2026.

And then looking ahead to Omnipod 6, recognizing this need to evolve even faster with the market, it's part of why we're designing one pod that can be updated in-market for faster innovation so that with Omnipod 6 we can always push the latest technologies directly to pods that customers have. So, we're accelerating in innovation and sensor integrations now, pleased to be on market with Dexcom 15-day and assuring that we're positioned to do that going forward.

On future data presentations

Q (Joanne Wuensch, Citigroup): Good morning and thank you so much for taking the question. ADA is going to be here before we know it. Is there anything in particular that we should look forward to there and I'm also trying to key in on when are we going to get a line of sight on some of the clinical steps for Omnipod 6?

Ms. McEvoy: I think it's important and I'm going to spend a little bit of time on this quickly and then Eric will cover the others. We are designing as the market leader with our big eyes focused on the underserved type 2 market in the United States where we have 5% penetration and there's 5.5 million people on insulin that we would like to be on AID therapy since the ADA guidelines recommended AID therapy as the standard of care. We have designed our fully closed-loop to address the biggest barriers for those patients with type 2 to get onto AID therapy. It starts with our algorithm which will include no user intervention. It requires no dosing. It has no mealtime interactions, no adjustments while the pod is worn.

Then there are two other areas that are really important to the type 2 user base. One is the clinician, and for the clinicians, this will require no defined settings at start, which is a big barrier right now to the primary care prescribing base that just don't have the time to go input all of those settings. And then third, Joanne, is that patients don't have to do two-hour training. This is something that they can initiate on their own. So, our combination of really modernizing the training so that they can do it at home on their own time without two hours, really unlocking prescriber adoption, not having to put in settings really important for the primary care audience, which is really who's going to be managing patients who have type 2 diabetes.

This will be a very CGM-like experience for people with type 2 diabetes. So, we're going to be sharing our data from our feasibility at the ADA. But in addition to that, we have some – our third-generation algorithm in Omnipod 6 that Eric will touch on.

Mr. Benjamin: Just building on Ashley's comments about what's coming at the upcoming congresses. At ATTD we'll be showing the EVOLUTION data as Ashley just described on our way towards that truly transformative fully closed-loop system to unlock primary care. We'll also be showing some health economic data showing favorable outcomes in ER visits for the unique fully disposable experience that is Omnipod as compared to tube pumps. So really excited for what's coming at ATTD.

Looking ahead to ADA, that's where we'll be publishing the pivotal results from STRIVE. That's the pivotal study that supports Omnipod 6. Excited to be reporting that out. And in addition, Ashley, mentioned this earlier, but there are more independent third-party studies comparing clinical results of on-market AID systems coming out. And in two recent of those, Omnipod has shown unsurpassed A1c and similar Time in Range to those reporting Time in Range using an iCGM sensor.

One of the other things that we're paying attention to is that it's really important to interpret clinical data based on A1c, and it's hard to compare across studies that don't use an iCGM sensor for Time in Range. There’s more of those studies coming out and you'll see us talking about those too.

Close Concerns’ Questions

- With R&D spend now accounting for ~11-12% of revenue, does Insulet expect to continue to grow its investment level as the company advances development of Omnipod 6, fully closed-loop, and its next-generation platform?

- As international growth accelerates, which specific geographic markets are expected to contribute most meaningfully in 2026?

- What role will Omnipod Discover play in increasing prescriber adoption and improving long-term retention?

- Does Insulet expect the share of new US starts with T2D to continue to increase or stabilize close to current levels?

-- by Jeremy Alkire, Riya Chatterjee, Nour Khachemoune, Monica Oxenreiter, and Kelly Close