Novo Nordisk 3Q25 – Diabetes/Obesity portfolio totals $11B (+4% YoY, +5% Q/Q), led by Ozempic ($4.8B) and Wegovy sales ($3.2B); highlights restructuring and active M&A efforts for renewed focus –

Executive Highlights

- Novo Nordisk presented its 3Q25 quarterly update today in the first quarterly conference call led by CEO Mr. Maziar Mike Doustdar - see the press release, presentation, finance detail, and webcast.

- Novo Nordisk’s diabetes and obesity portfolio totaled $11.0 billion in 3Q25, up 11% CER from 3Q24 and down 2% sequentially. US sales totaled $6.1 billion, up 10% CER and down 4% sequentially. OUS sales totaled $4.9 billion, up 11% CER from 3Q24 and flat sequentially. Obesity care sales totaled $3.3 billion, up 18% CER from 3Q25 and up 4% sequentially. Novo Nordisk’s medications treated over 42 million people with diabetes and three million people with obesity.

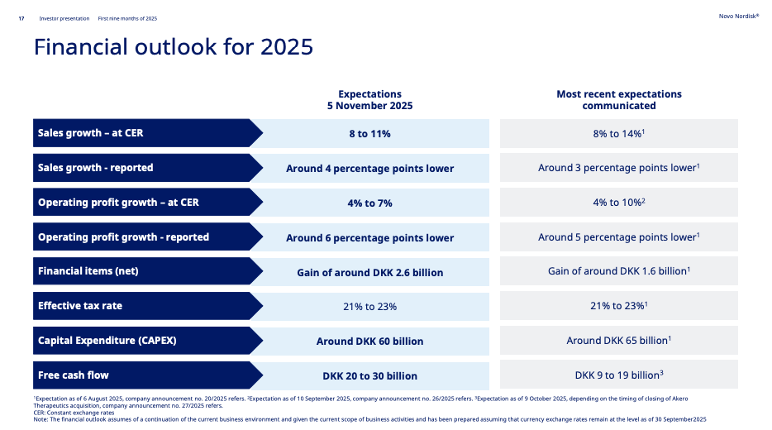

- Given the lower-than-expected sales and business developments, Novo Nordisk revised the 2025 guidance for the fourth time in the last year. Sales growth is now expected to be 8-11%, a lower “high-end” of former expectation of 8-14% announced in 2Q25. We think a lower “high end” makes sense given what is presumably some pricing pressure.

- Mr. Doustdar highlighted several restructuring efforts to redirect resources to new “growth opportunities” in diabetes and obesity.

- In September, the company announced its plans to cut ~9,000 jobs globally (~12% of its workforce).

- In October, the company terminated several stem cell research, including its search for T1D cure.

- At the same time, Novo Nordisk has pursued multiple partnerships and acquisitions in the cardiometabolic field, such as its unsolicited proposal to acquire Metsera that has reached up to $10 billion, a $5.2 billion acquisition of MASH-focused Akero Therapeutics, and collaborations for drug development.

- GLP-1 RA sales across diabetes and obesity continued to drive growth globally. In 3Q25, sales totaled $9.3 billion, up 15% and down 2% sequentially. Novo Nordisk’s share for the global GLP-1 RA market is 49% (down from 52%).

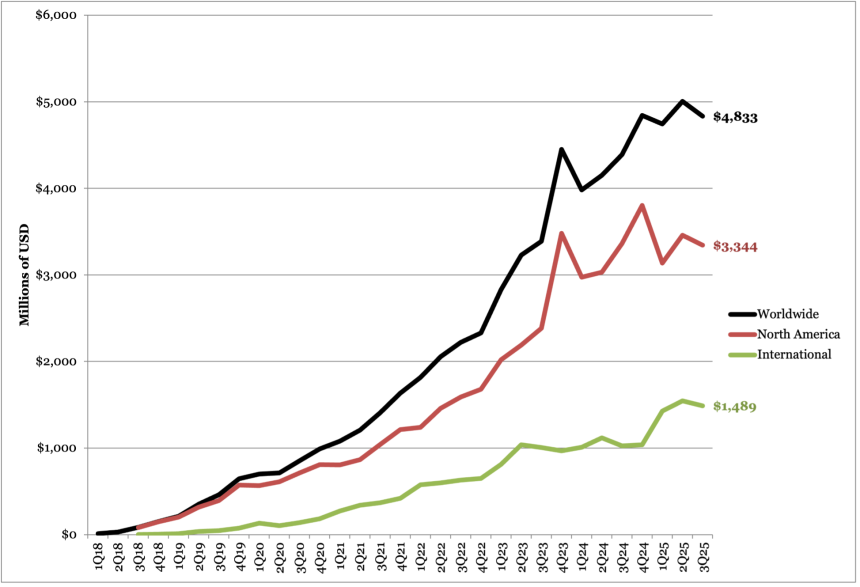

- Ozempic: Global sales totaled $4.8 billion in 3Q25, up 9% CER from 3Q24 and down 3% sequentially. US sales totaled $3.3 billion (+7% CER, -3% Q/Q), and OUS sales totaled $1.5 billion (+13% CER, -4% Q/Q). In the US, Ozempic’s weekly prescriptions total ~670,000 units for the quarter, down from 690,000 in 2Q25. In August, Novo Nordisk launched Ozempic for $499 per month on NovoCare.

- Wegovy: Global sales totaled $3.2 billion in 3Q25, up 23% CER from 3Q24 and up 4% sequentially. Growth was driven by increased volumes, partially offset by lower realized prices. US sales totaled $2.0 billion (+6% CER, -3% Q/Q). OUS sales totaled $1.2 billion (+67% CER, -17% Q/Q). Wegovy is now launched in over 45 countries (up from 35 in 2Q25), with more expected. Wegovy uptake via cash channel totaled ~26,000 weekly prescription (flat from 2Q25), accounting for ~10% of total prescriptions. In August, the FDA approved Wegovy for MASH in adults with moderate to advanced liver fibrosis, based on the ESSENCE trial.

- Rybelsus: Global sales for GLP-1 RA Rybelsus (oral semaglutide) totaled $855 million in 3Q25, down 4% from 3Q24 and flat sequentially. US sales totaled $312 million (-18% CER, -3% Q/Q), and OUS sales totaled $543 million (-15% CER, +2% Q/Q). Rybelsus has been launched in more than 40 countries and continues to expand. On the regulatory side, Novo Nordisk obtained approval for CV indications in the US and the EU for oral semaglutide (14 mg). FDA decision for high dose oral semaglutide (25 mg) is expected in 4Q25.

- As a significant policy update, Novo Nordisk has agreed to the “maximum fair prices” (MFPs) set by the US Inflation Reduction Act for three of its semaglutide medicines – Ozempic, Rybelsus, and Wegovy. Notably, MFPs will take effect under Medicare Part D in 2027. Management shared that if the price caps had begun in 2025, it would have incurred a single-digit sales decline in global sales growth for the year.

- Insulin sales totaled $1.9 billion in 3Q25, up 1% CER and down 7% sequentially. Growth was largely driven by sales in the US, which totaled $497 million (+20% CER, -6% Q/Q). OUS sales totaled $1.4 billion (-4% CER, -6% Q/Q). Novo Nordisk’s insulin market share was largely flat from recent years. In the US, where the company has a market share of 29%, management attributed increase in US sales to positive channel and payer mix, partially offset by decline in volume. OUS, where Novo Nordisk holds 47% of market share, revenue was negatively impacted by periodic supply constraints and lower sales in the EU and Canada.

- Novo Nordisk is facing major impending changes to its Board of Directors. In October, several board members, including the Chair Mr. Helge Lund, resigned due to an unresolvable dispute with Novo Nordisk Foundation about the future composition of the board and the control of the company. The former sought for more conservative approach, while the latter wanted more radical changes to the board configuration. In response, the Novo Nordisk Foundation proposed a slate of new candidates for election to Novo Nordisk’s board of directors, including Former CEO Mr. Lars Rebien Sørensen as the new Chair. An Extraordinary General Meeting will convene next Friday, November 14, to elect new board members.

[1] Year-Over-Year reported growth is in CER unless marked with an asterisk (*).

3Q25 Financial Results for Novo Nordisk’s Major Diabetes Products

| Product | 3Q25 Revenue – USD millions | Year-Over-Year Reported Growth[1]for 3Q25 | Sequential Reported Growth |

| GLP-1 (excluding Xultophy) | $9,269 | +15%* | -2% |

| Ozempic | $4,833 | +9% | -3% |

| Wegovy | $3,200 | +23% | +4% |

| Rybelsus | $855 | +4% | -4% |

| Victoza | $86 | Flat | -40% |

| Saxenda | $118 | -47% | -11% |

| Total Insulin | $1,885 | +1% | -7% |

| Basal Insulin | $637 | +9% | -8% |

| Tresiba | $412 | +31% | -6% |

| Levemir | $49 | -63% | -34% |

| Xultophy | $176 | +12% | -1% |

| Awiqli | $22 | n/a | +141% |

| Rapid-Acting Insulin | $646 | +5% | -10% |

| NovoLog | $547 | -2% | -14% |

| Fiasp | $99 | +67% | +22% |

| Premix Insulin | $371 | -1% | -11% |

| NovoMix | $168 | -17% | -16% |

| Ryzodeg | $203 | +18% | -5% |

| Human Insulin | $209 | -23% | +20% |

| Other | $66 | -11% | -7% |

| Total Diabetes and Obesity Portfolio | $11,044 | +5% | -2% |

Table of Contents

-

Financial Highlights

- 1. D/O portfolio totals $11 billion (+11% CER), driven by GLP-1 RAs; revised guidance expects 8-11% growth amid continued restructuring efforts

- 2. Ozempic totals $4.8 billion (+9% CER); Novo Nordisk reaches agreement with the US on Medicare pricing for semaglutide products

- 3. Oral GLP-1 RA Rybelsus revenue totals $855 million (+4% CER); US and EU approval for CV risk reduction

- 4. Obesity revenue (Wegovy and Saxenda) totals $3.3 billion (+18% CER); FDA-approved for MASH

- 5. Victoza (liraglutide) sales total $86 million (-40% Q/Q); declines driven by movement of GLP-1 RA market to once-weekly treatment options

- 6. Tresiba sales total $412 million, up 31% CER and down 6% sequentially

- 7. Fiasp sales total $99 million (+67% CER); NovoLog sales total $547 million (-2% CER)

- 8. Xultophy sales total $176 million (+12% CER)

- Pipeline Highlights

- Close Concerns’ Questions

- Analysts’ Q&A

Financial Highlights

1. D/O portfolio totals $11 billion (+11% CER), driven by GLP-1 RAs; revised guidance expects 8-11% growth amid continued restructuring efforts

Novo Nordisk’s diabetes and obesity portfolio totaled $11.0 billion in 3Q25, up 11% CER from 3Q24 and down 2% sequentially. Robust growth was seen across both the US and OUS markets. US sales totaled $6.1 billion, up 10% CER and down 4% sequentially. OUS sales totaled $4.9 billion, up 11% CER from 3Q24 and flat sequentially.

Growth was largely driven by Obesity sales (Wegovy and Saxenda), which totaled $3.3 billion, up 18% CER from 3Q25 and up 4% sequentially. GLP-1 RA sales for diabetes also remained robust, totaling $5.8 billion, up 11% CER and down 4% sequentially. By number of patients reached, Novo Nordisk’s medications treated over 42 million people with diabetes and 3 million people with obesity.

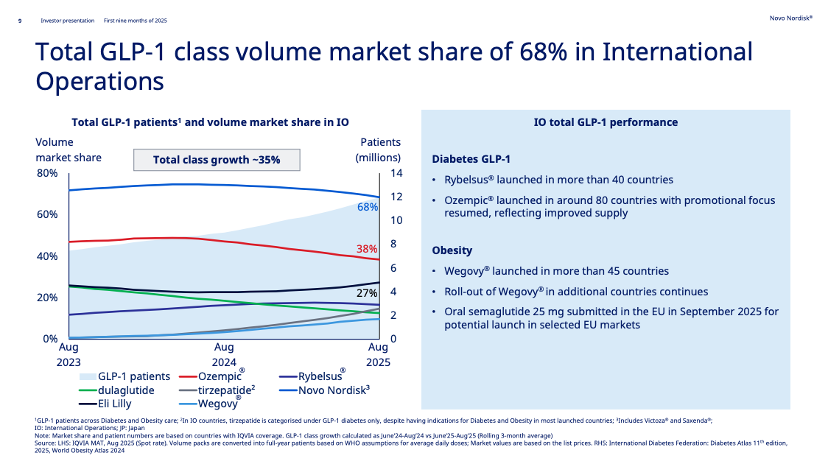

- Novo Nordisk’s market share in diabetes and obesity care declined over the past year. Compared to 3Q24, its share in diabetes value market decreased by 2 percentage points to 32% in 3Q25, which was consistent across US and OUS markets (see slides below). Moreover, the company captured 49% of global market share of GLP-1 RAs for diabetes, down from 56% in 3Q25. Geographically, Novo Nordisk captured 47% of the US market and 68% of the OUS market. Outside the US, Management noted that the numbers may be slightly inaccurate given that IQVIA data categorizes Mounjaro (tirzepatide) as a drug for diabetes in OUS markets when it is indicated for both diabetes and obesity.

- During Q&A, Mr. Doustdar commented, “I don’t like losing market share, but our job right now is to focus the company’s strategy around diabetes and obesity, predominantly because we see a huge expansion potential as we go forward.” Novo Nordisk continues to pursue this field by advancing candidates in the pipeline, conducting mergers and acquisitions (M&A), and exploring other commercial avenues, such as partnerships with retail pharmacies and telehealth companies. He reminded that “it’s a marathon…not a sprint,” and it takes time for these measures to take effect.

Source: Novo Nordisk 3Q25 slides, page 9-10

Given the lower-than-expected sales and business developments, Novo Nordisk revised the 2025 guidance for the fourth time. Sales growth is now expected to be 8-11%, a lower end of former expectation of 8-14% announced in 2Q25 and a nearly 11 percentage point reduction from the original guidance of 16-24% from January 2025. Likewise, operating profit growth is now expected at 4-7% (down from 4-10%).

Source: Novo Nordisk 3Q25 slides, page 17

In prepared remarks, Mr. Doustdar reiterated diabetes and obesity as Novo Nordisk’s core focus areas, given the high unmet needs. Over a billion people are affected by diabetes or obesity globally, yet only 7% of those with diabetes are treated with GLP-1 RAs, and 1% of those with obesity are treated with medications. Moreover, many individuals have comorbidities affecting kidneys, the heart, and the liver.

- To achieve this, Novo Nordisk led several restructuring efforts over the past quarter. In September, the company announced its plans to simplify operations and reallocate resources toward diabetes and obesity – including cutting ~9,000 jobs globally (~12% of its workforce), with 5,000 reductions expected in Denmark. In October, the company terminated its partnership with Heartseed to develop stem cell-based therapy for heart failure. In the same month, the company discontinued its work in cell therapy that previously focused on T1D, Parkinson’s disease, and chronic heart failure – laying off 250 employees. At the same time, Novo Nordisk has pursued multiple partnerships and acquisitions in the cardiometabolic field, reflecting its renewed focus on new “growth opportunities.” This includes its unsolicited proposal to acquire Metsera for up to $10 billion, a $5.2 billion acquisition of MASH-focused Akero Therapeutics, and collaborations for drug development.

- Novo Nordisk is facing major impending changes to its Board of Directors. In October, several board members, including the Chair Mr. Helge Lund, resigned due to an unresolvable dispute with Novo Nordisk Foundation about the future composition of the board and the control of the company. The former sought for more conservative approach, while the latter wanted more radical changes to the board configuration. In response, the Novo Nordisk Foundation proposed a slate of new candidates for election to Novo Nordisk’s board of directors, including Former CEO Mr. Lars Rebien Sørensen as the new Chair. An Extraordinary General Meeting will convene next Friday, November 14, to elect new board members.

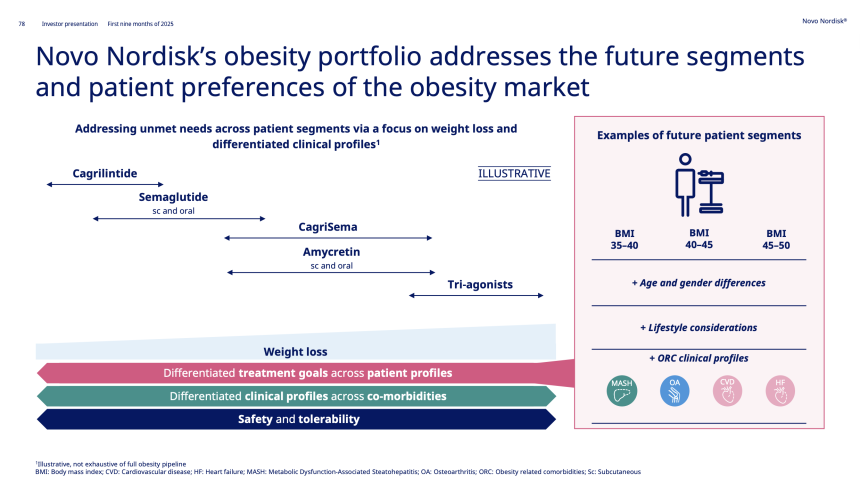

- Novo Nordisk shared significantly about its strategies. See the figure below for what segments of obesity market Novo Nordisk's cardiometabolic pipeline aims to fill.

Novo Nordisk D/O Worldwide Financial Results – Past Five Quarters

Diabetes/ Obesity | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD billions (DKK billions) | $9.8 (DKK 67) | $11.4 (DKK 80) | $10.7 (DKK 73) | $11.3 (DKK 72) | $11.0 (DKK 70) |

| YOY Growth (CER) | +22% (+23%) | +31% (+30%) | +21% (+19%) | +12% (+17%) | +5% (+11%) |

| Sequential Reported Growth | +4% | +20% | -8% | -2% | -2% |

Novo Nordisk D/O Sales – 3Q25 Geographic Results

| Revenue – USD billions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth | |

| US | $6.1 (DKK 41.1) | +3% (+10%) | -4% |

| OUS | $4.9 (DKK 33.8) | +8% (+12%) | flat |

2. Ozempic totals $4.8 billion (+9% CER); Novo Nordisk reaches agreement with the US on Medicare pricing for semaglutide products

Ozempic (once-weekly injectable semaglutide 0.5 mg, 1 mg, or 2 mg) revenue totaled $4.8 billion in 3Q25, up 9% CER from 3Q24 and down 3% sequentially. US sales totaled $3.3 billion, up 7% CER from 3Q24 but down 3% sequentially, and were positively impacted by gross-to-net sales adjustments and volume growth, partially countered by lower realized prices. OUS sales totaled $1.5 billion, up 13% CER from 3Q24 but down 4% sequentially.

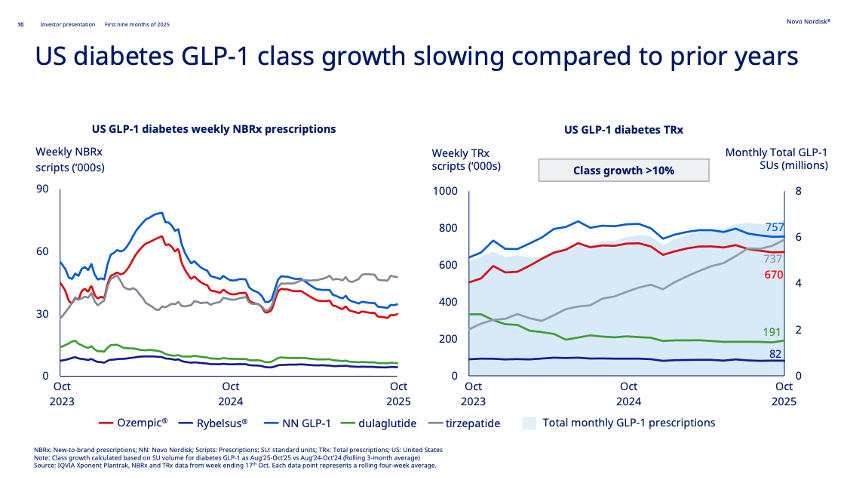

In the US, Ozempic’s weekly prescriptions totaled ~670,000 units in the quarter, down from 690,000 in 2Q25. Since 2Q25, Mounjaro has exceeded semaglutide in both new-to-brand and total prescriptions (737,000 for tirzepatide vs. 670,000 for semaglutide). We wonder how the expanding indications and the cash channel will affect the uptake.

- In August, Novo Nordisk launched a cash option for Ozempic at $499 per month for eligible self-paying patients. This reflects a 50% reduction from the list price of ~$1,000/month and applies to all three doses (0.5 mg, 1 mg, and 2 mg) of Ozempic auto-injectors. Moreover, Novo Nordisk has continued to expand partnerships to increase patient access, including retail pharmacies like Costco, CVS, and Walmart. The company did not share further details about the uptake of Ozempic through NovoCare.

- In a major policy update, Novo Nordisk has agreed to the “maximum fair prices” (MFPs) set by the US Inflation Reduction Act for three of its semaglutide medicines – Ozempic, Rybelsus, and Wegovy. Notably, MFPs will take effect under Medicare Part D in 2027. Management shared that if the price caps had begun in 2025, it would have incurred a single-digit sales decline in global sales growth for the year.

OUS, Ozempic has been launched in ~80 countries and remains a global market leader for GLP-1 RAs in diabetes.

Ozempic Worldwide Financial Results – Past Five Quarters

| Ozempic | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $4,390 (DKK 29.8) | $4,841 (DKK 33.9) | $4,745 (DKK 32.7) | $5,005 (DKK 31.8) | $4,833 (DKK 30.7) |

| YOY CER Growth | +25% (+26%) | +13% (+12%) | +18% (+15%) | +10% (+15%) | +3% (+9%) |

| Sequential Reported Growth | +3% | +14% | -3% | -3% | -3% |

Ozempic Sales – 3Q25 Geographic Results

| Ozempic | Revenue – USD millions (DKK billions) | YOY CER Growth | Sequential Reported Growth |

| US | $3,344 (DKK 21.3) | +1% (+7%) | -3% |

| OUS | $1,489 (DKK 9.5) | +9% (+13%) | -4% |

Ozempic Sales (1Q18-3Q25)

3. Oral GLP-1 RA Rybelsus revenue totals $855 million (+4% CER); US and EU approval for CV risk reduction

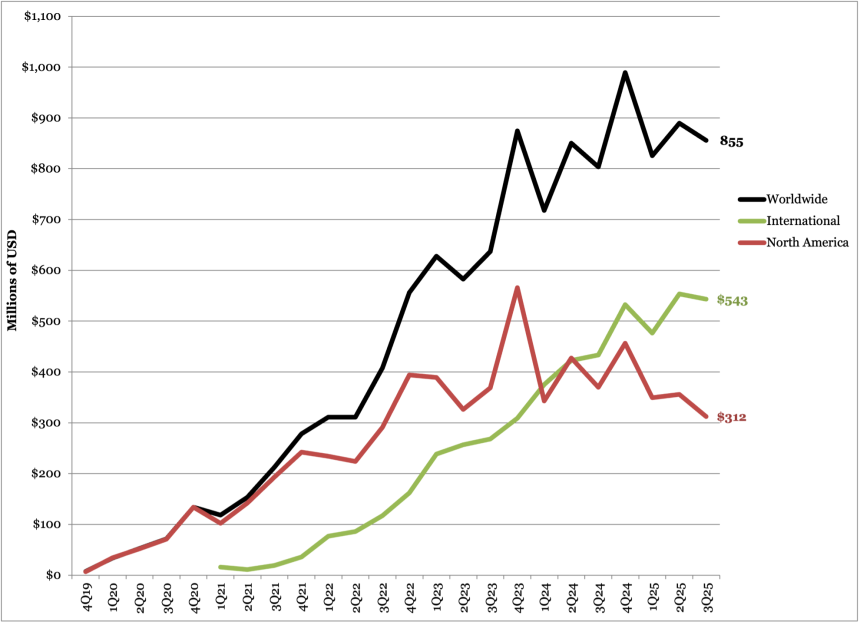

Sales for GLP-1 RA Rybelsus (oral semaglutide) totaled $855 million in 3Q25, down 4% from 3Q24 and flat sequentially. By geography, US sales totaled $312 million, down 18% from 3Q24 and 3% sequentially. OUS sales totaled $543 million, down 15% from 3Q24 and up 2% sequentially. Sales growth was driven by OUS operations, primarily in Europe, Canada, Asia-Pacific Region, and China. As of 3Q25, Rybelsus has been launched in more than 40 countries and continues to expand.

In the US, Novo Nordisk announced several reductions to its Patient Assistance Program (PAP). Starting January 1, 2026, Rybelsus will be removed from the PAP for all patients.

On the regulatory side, Novo Nordisk obtained approval for CV indications in the US and the EU for oral semaglutide (14 mg):

- In October, the FDA approved Rybelsus as the only oral GLP-1 RA for reducing the risk of major adverse cardiovascular events (MACE) in adults with T2D who have a high risk of cardiovascular (CV) death, heart attack, or stroke – regardless of a prior CV event. The approval is based on the phase 3 SOUL trial (n=9,650), in which Rybelsus (oral semaglutide 14 mg) led to a statistically significant and superior 14% MACE reduction in adults with T2D and established CVD and/or CKD.

- In September, the European Commission expanded its approval of Rybelsus’s indication to include cardiovascular benefit. In July, the European Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) issued a positive recommendation of Rybelsus for reducing the risk of cardiovascular events based on the SOUL trial.

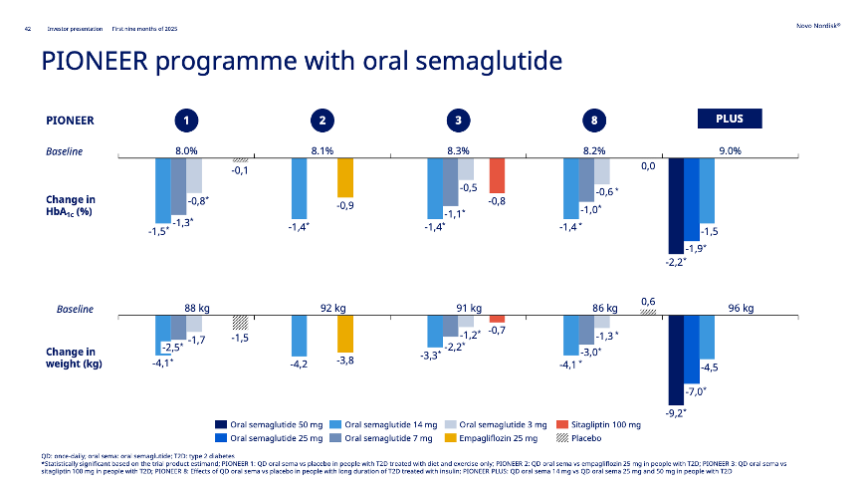

The company continues to advance high doses of Rybelsus for obesity and T2D:

- High-dose oral semaglutide (25 mg) for obesity. Based on the phase 3 OASIS-4 trial (n=307) presented at ObesityWeek 2024, Novo Nordisk submitted oral semaglutide 25 mg for obesity in the US and the EU in April 2025 and September 2025, respectively. As announced in 2Q25, Novo Nordisk expects an FDA decision in 4Q25, though no expected timeline was offered for EU approval. As background, the 64-week OASIS-4 trial demonstrated 14% weight loss compared to 2% with placebo, from a baseline of 106 kg (233 lbs). 71% of participants with prediabetes at baseline reverted to normoglycemia, compared to 33% in the placebo group.

- High-dose oral semaglutide (25 mg and 50 mg) for T2D and obesity. Novo Nordisk submitted high-dose oral semaglutide 25 mg and 50 mg for approval in the EU in 3Q24 based on positive results from the phase 3b OASIS-1 trial and PIONEER PLUS trial. In 4Q24, however, we noticed that Novo Nordisk is no longer pursuing the 50 mg dose in the US.

Source: Novo Nordisk 3Q25 slides, page 42

Novo Nordisk Rybelsus Worldwide Financial Results – Past Five Quarters

| Diabetes/Obesity | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $803 (DKK 5.5) | $989 (DKK (6.9) | $826 (DKK 5.7) | $890 (DKK 5.7) | $855 (5.4 DKK) |

| YOY Reported (CER) Growth | +23% | +18% | +13% | -5% (-1%) | flat (+4%) |

| Sequential Reported Growth | -8% | +27% | -18% | -1% | -4% |

Novo Nordisk Rybelsus Sales – 3Q25 Geographic Results

| Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth | |

| US | $312 (DKK 2.0) | -18% (-13%) | -3% |

| OUS | $543 (DKK 3.5) | +15% (+18%) | +2% |

Rybelsus Sales (4Q19-3Q25)

4. Obesity revenue (Wegovy and Saxenda) totals $3.3 billion (+18% CER); FDA-approved for MASH

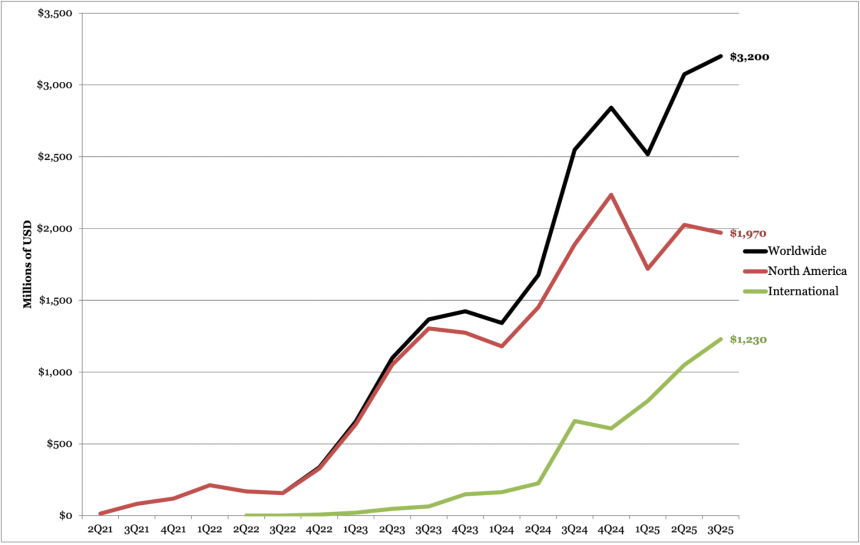

Obesity care sales, which include Wegovy (semaglutide 2.4 mg) and Saxenda (liraglutide), totaled $3.2 billion, up 18% from 3Q24 and up 4% sequentially. Overall growth was driven by both US (+6% CER) and OUS sales (+41%). Novo Nordisk captured 68% of total GLP-1 RA market.

Wegovy sales totaled $3.2 billion in 3Q25, up 23% CER from 3Q24 and up 4% sequentially. Growth was driven by increased volumes, partially countered by lower realized prices. By geography, US sales totaled $2.0 billion, up 6% CER from 3Q24 and down 3% sequentially. OUS sales totaled $1.2 billion, up 67% from 3Q24 and up 17% sequentially. In the US, Wegovy has around 270,000 weekly prescriptions (down from 280,000 in 2Q25), and there was 2.5x volume growth of the branded obesity market in the US.

OUS, Wegovy is now launched in over 45 countries, with more expected. This number compares to 35 countries in 2Q25 and 25 countries in 1Q25.

Novo Nordisk has made several efforts to increase patient access, both through insured and cash channels.

- Wegovy prescriptions via NovoCare Pharmacy, including telehealth collaborations, total ~10,000 weekly prescription (flat from 2Q25), in addition to 16,000 weekly prescriptions (slightly lower from 17,000 in 2Q25) in retail cash channel. Management shared that the cash market accounts for ~10% of total Wegovy prescriptions. Novo Nordisk partnered with GoodRx and Costco to further expand access.

- Within the insured channel, Wegovv has coverage for around 55 million people with obesity in the US. This number aligns with the coverage reported in the past four quarters. Moreover, over 10 million people are estimated to have coverage through Medicaid, which covers people with obesity and weight-related comorbidities like cardiovascular disease. However, due to increased healthcare expenditures, several states, including California, North Carolina, Pennsylvania, Connecticut, and Michigan, announced to end or scale back coverage of Wegovy. In October, Novo Nordisk announced that it lobbied to maintain Medicaid reimbursement for Wegovy across 14 US states. We are curious how the newly negotiated maximum fair price with the US government will affect the coverage and future uptake.

- For commercial payers, in May 2025, CVS Caremark selected Wegovy as its preferred on its commercial template formularies, effective in July 2025. During Q&A, management said that it expects Wegovy to be an exclusive branded obesity medication at CVS in 2026, as well.

- Generic semaglutide is expected early next year. Novo Nordisk’s semaglutide will lose its data exclusivity in Canada in January 2026. Given that its patent, which granted Novo Nordisk exclusive rights to manufacture and sell semaglutide in Canada, lapsed in 2020, generic companies like Sandoz and Hims & Hers can file for regulatory approval for generics starting next year.

Novo Nordisk continues to expand indications of Wegovy.

- In August, the FDA approved Wegovy (semaglutide 2.4 mg) for MASH in adults with moderate to advanced liver fibrosis (stages F2 to F3 fibrosis), and Novo Nordisk launched Wegovy for MASH in 3Q25. This approval is based on Part 1 of the phase 3 ESSENCE trial (n=1,200), in which Wegovy conferred a statistically significant and superior improvement in liver fibrosis, as well as resolution of steatohepatitis with no worsening of liver fibrosis compared to placebo. In 1Q25 and 2Q25, Novo Nordisk filed for regulatory approval in the EU and Japan, respectively, as well.

- High-dose semaglutide (7.2 mg) and its single-dose-device formulation for obesity has been submitted to the EU regulatory authorities. In July, Novo Nordisk submitted semaglutide 7.2 mg to the EMA to expand Wegovy’s label. In October, Novo Nordisk further submitted a variant application for semaglutide 7.2 mg in a single-dose pen. This submission is based on the results of the STEP UP (n=1,407) and STEP UP T2D (n=512) program presented at ADA 2025, in which semaglutide 7.2 mg achieved up to 21% weight loss across several trials. Novo Nordisk expects a regulatory decision for semaglutide 7.2 mg in early 2026 and approval of semaglutide 7.2 mg in a single-dose pen in 2H26. Regulatory submission in the US is expected in 4Q25.

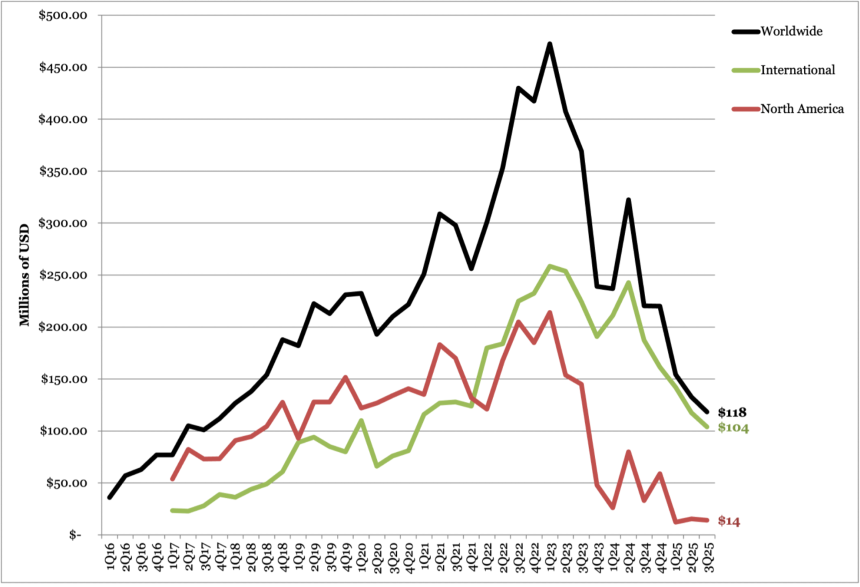

Saxenda sales totaled $118 million, down 47% CER from 3Q24 and down 11% sequentially. US sales totaled $14 million, up 8% CER from 3Q24 and down 8% sequentially. OUS sales totaled $104 million, down 51% CER from 3Q24 and down 11% sequentially.

Wegovy Worldwide Financial Results – Past Five Quarters

| Wegovy | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $2,549 (DKK 17.3) | $2,841 (DKK 19.9) | $2,517 (DKK 17.4) | $3,074 (DKK 19.5) | $3,200 (DKK 20.4) |

| YOY Reported (CER) Growth | +81% | +107% | +83% | +68% (+75%) | +18% (+23%) |

| Sequential Reported Growth | +48% | +15% | -13% | +13% | +4% |

Wegovy Sales – 3Q25 Geographic Results

| Wegovy | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | $1,970 (DKK 12.5) | flat (+6%) | -3% |

| OUS | $1,230 (DKK 7.9) | +62% (+67%) | +17% |

Wegovy Sales (2Q21-3Q25)

Saxenda Worldwide Financial Results – Past Five Quarters

| Saxenda | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $221 (DKK 1.5) | $220 (DKK 1.5) | $154 (DKK 1.1) | $133 (DKK 0.8) | $118 (DKK 0.8) |

| YOY Reported (CER) Growth | -41% | -3% | -35% | -62% (-61%) | -50% (-47%) |

| Sequential Reported Growth | -33% | +3% | -31% | -21% | -11% |

Saxenda Sales – 3Q25 Geographic Results

| Saxenda | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | $14 (DKK 0.1) | +1% (+8%) | -8% |

| OUS | $104 (DKK 0.7) | -53% (-51%) | -11% |

Saxenda Sales (1Q16-3Q25)

5. Victoza (liraglutide) sales total $86 million (-40% Q/Q); declines driven by movement of GLP-1 RA market to once-weekly treatment options

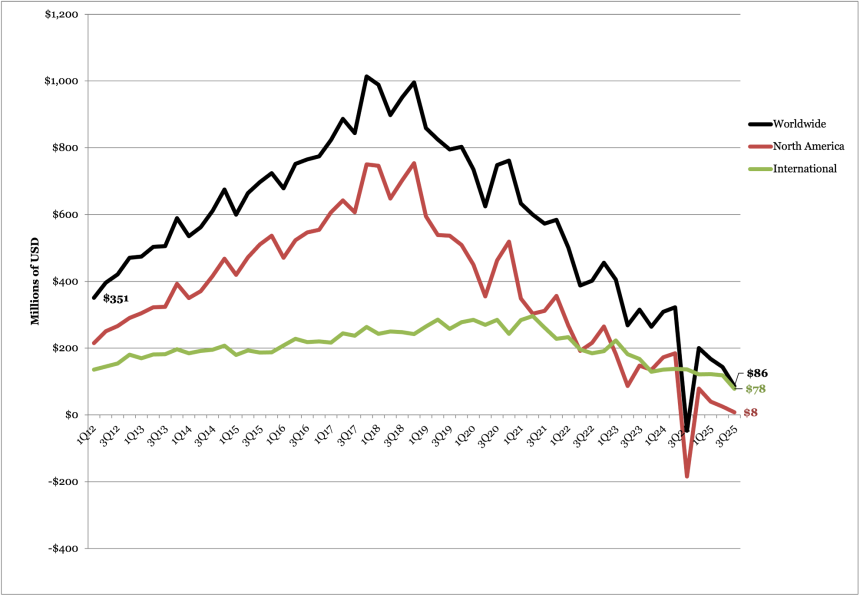

Victoza (liraglutide) sales totaled $86 million, flat CER from 3Q25 and down 40% sequentially. US sales totaled $8 million, flat CER and down 68% sequentially. OUS sales totaled $78 million, down 45% CER and 34% sequentially. Note that year-to-year sales growth was marked as flat in the company’s report because Victoza sales totaled $47 million in 3Q24, due to negative adjustments in prior years from higher Medicaid exposure in the US.

Victoza sales in both the US and OUS markets have experienced marked decline in recent years due to competition with second generation GLP-1 RAs, such as tirzepatide and semaglutide. Further, as the number of generic competitors for Victoza entering the market continues to grow, we imagine Victoza sales will continue to decline in future quarters. Since 2023, Victoza’s patents have expired in China, Japan, the US, and the EU. Moreover, Novo Nordisk has settled multiple patent infringement lawsuits for Victoza, enabling several companies to launch biosimilar versions in 2024 and 2025:

- In July 2025, Mumbai-based Lupin’s generic liraglutide received FDA approval;

- In June 2025, Bengaluru-based Biocon’s generic liraglutide was approved in India;

- In April 2025, Meitheal Pharmaceuticals launched generic Victoza in a three-pack and announced plans to introduce additional pack sizes later this year;

- In December 2025, Hikma Pharmaceuticals launched generic Victoza;

- In June 2024, Teva launched the first generic Victoza in the US at a 13% lower retail price ($470/two pens, $700/three pens) than Novo Nordisk's;

- In March 2024, Biocon’s generic liraglutide was approved in the UK; and

- In January 2024, Mumbai-based Glenmark Pharmaceuticals launched India’s first biosimilar of Victoza.

Victoza Worldwide Financial Results – Past Five Quarters

| Victoza | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | -$47 (-DKK 0.3) | $201 (DKK 1.4) | $168 (DKK 1.2) | $144 (DKK (0.9) | $86 (DKK 0.5) |

| YOY (CER) Growth | -115% (-114%) | -21% (-22%) | -46% (-46%) | -59% (-57%) | N/A (flat) |

| Sequential Reported Growth | -114% | +536% | -18% | -21% | -40% |

Victoza Sales – 3Q25 Geographic Results

| Victoza | Revenue – USD millions (DKK billions) | YOY (CER) Growth | Sequential Reported Growth |

| US | $8 (DKK 0.05) | N/A (flat) | -68% |

| OUS | $78 (DKK 0.5) | -48% (-45%) | -34% |

Victoza Sales (1Q12-3Q25)

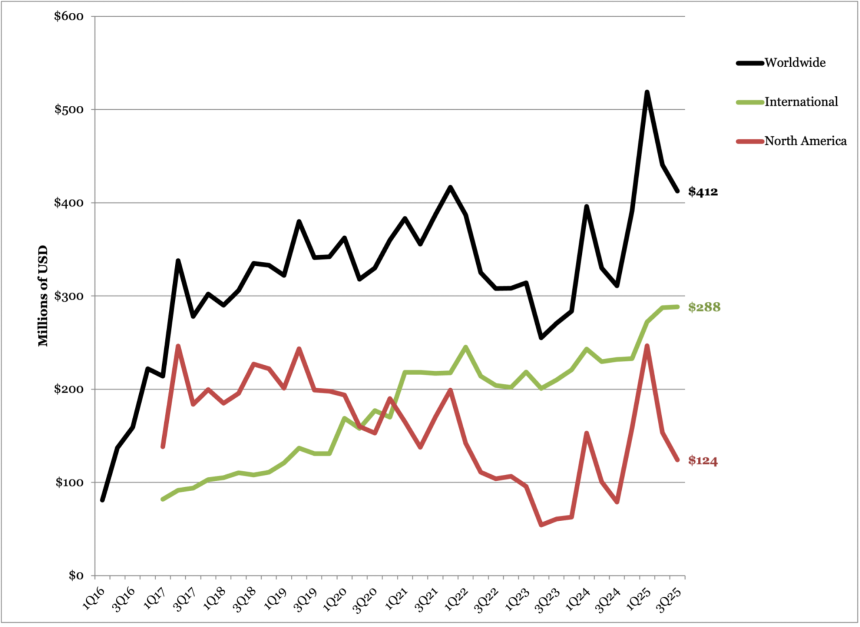

6. Tresiba sales total $412 million, up 31% CER and down 6% sequentially

Revenue for next-generation basal insulin Tresiba totaled $412 million, up 31% CER and down 6% sequentially. US sales totaled $24 million, up 2.2x CER and down 43% sequentially. OUS sales totaled $288 million, up 11% CER and down 3% sequentially.

While Tresiba revenue in 3Q25 is down compared to 2Q25 and 1Q25, the quarter that marked the first break in Tresiba’s overall growth trend since 1Q24, there continues to be strong growth following Levemir’s discontinuation in the US in December 2024. Along with this discontinuation, Novo Nordisk also announced plans in December 2024 to reduce US list prices for Fiasp and Tresiba by over 70%, also effective in 2026.

Tresiba Worldwide Financial Results – Past Five Quarters

| Tresiba | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $311 (DKK 2.1) | $391 (DKK 2.7) | $519 (DKK 3.6) | $441 (DKK 2.8) | $412 (DKK 2.6) |

| YOY (CER) Growth | +11% (+42%) | +43% (+45%) | +30% (+27%) | +22% (+27%) | +24% (+31%) |

| Sequential Reported Growth | -8% | +30% | +31% | -22% | -6% |

Tresiba Sales – 3Q25 Geographic Results

| Tresiba | Revenue – USD millions (DKK billions) | YOY (CER) Growth | Sequential Reported Growth |

| US | $124 (DKK 0.8) | +106% (+124%) | -43% |

| OUS | $288 (DKK 1.8) | +6% (+11%) | -3% |

Tresiba Sales (1Q16-3Q25)

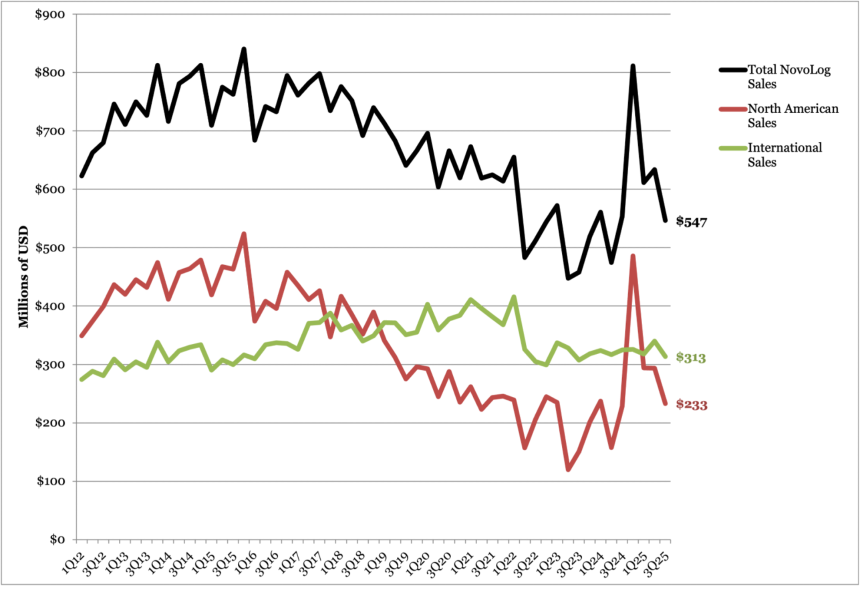

7. Fiasp sales total $99 million (+67% CER); NovoLog sales total $547 million (-2% CER)

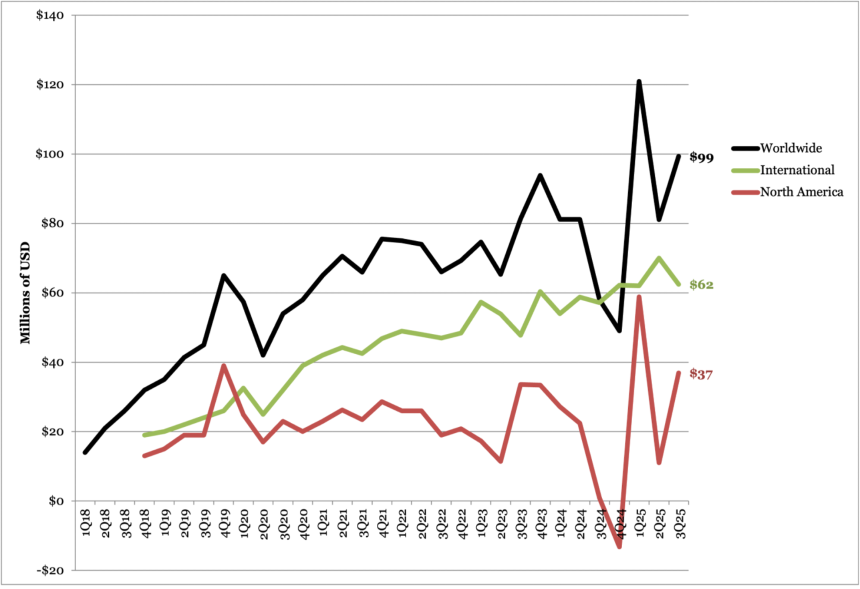

Fast-acting insulin Fiasp sales totaled $99 million, up 67% CER and up 22% sequentially. US sales totaled $36 million, flat CER and up 3.4x sequentially. OUS sales totaled $62 million, up 3% CER and down 11% sequentially. While today’s call did not mention Fiasp, we imagine that the sequential increase in US sales is due to a lower base in 2Q25, when sales decreased ($11 million) due to gross-to-net sales adjustments.

Novolog sales totaled $547 million, down 2% CER and down 5% sequentially. By geography, US sales totaled $233 million, up 5% CER and down 21% sequentially. OUS sales totaled $313 million, down 7% CER and down 8% sequentially. According to the 2Q25 Industry Roundup, Novolog captured 39% of the fast-acting insulin market by volume, while Fiasp accounted for only 5%.

- In the US, Fiasp’s Pumpcart (a pre-filled insulin cartridge) received FDA 510(k) clearance in June 2023 for use with Beta Bionics’ iLet Bionic Pancreas, adding to its compatibility with NovoLog and Humalog.

- Looking ahead, competition is expected to increase following the FDA approval of Biocon’s Kirsty, a rapid-acting biosimilar to NovoLog, in July 2025. Additionally, both Fiasp and NovoLog were selected for the first cycle of the US Medicare Drug Price Negotiation Program (MDPNP), with discounted prices (down 75% to $199/month), which will take effect on January 1, 2026. We are curious to see how this pricing may affect Novo Nordisk’s market share.

Fiasp Worldwide Financial Results – Past Five Quarters

| Fiasp | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $58 (DKK 0.4) | $49 (DKK 0.3) | $121 (DKK 0.8) | $81 (DKK 0.5) | $99 (DKK 0.6) |

| YOY Growth | -31% (-32%) | -46% (-45%) | +47% (+44%) | -9% (-5%) | +60% (+67%) |

| Sequential Reported Growth | -30% | -13% | +143% | -38% | +22% |

Fiasp Sales – 3Q25 Geographic Results

| Fiasp | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | $36 (DKK 0.2) | -4,800% (flat) | +235% |

| OUS | $62 (DKK 0.4) | -1% (+3%) | -11% |

Fiasp Sales (1Q18-2Q25)

NovoLog Sales (1Q12-3Q25)

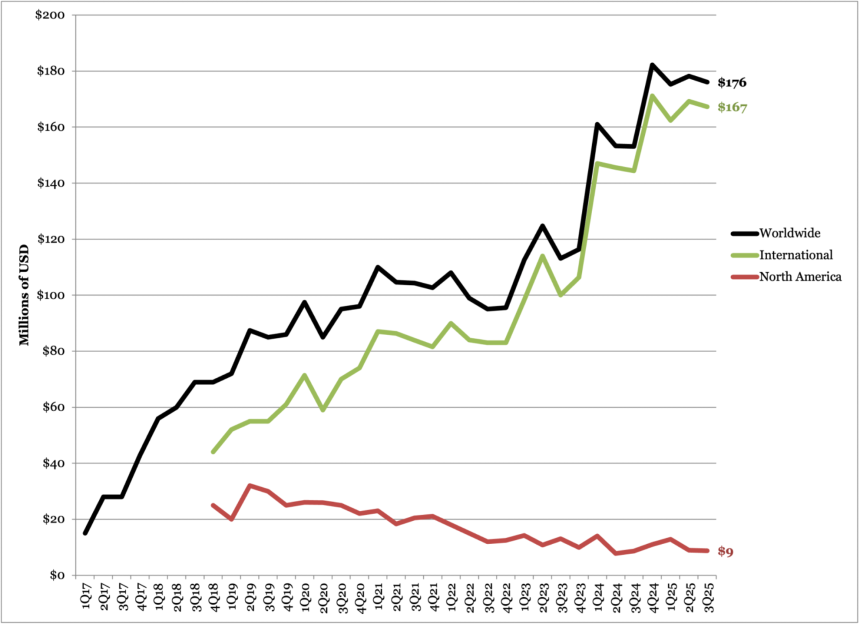

8. Xultophy sales total $176 million (+12% CER)

Revenue for fixed-ratio basal insulin/GLP-1 RA combination Xultophy totaled $176 million, up 12% CER and down 1% sequentially. US sales totaled $8 million, up 5% CER and flat sequentially. OUS sales totaled $167 million, up 12% CER and down 1% sequentially. Following the trends of past quarters, Xultophy demonstrated strong growth in China with a revenue of $61 million, up 54% CER.

- While semaglutide and other incretin-based therapies have demonstrated overwhelming success as monotherapies, many patients can benefit from combination therapies like Xultophy, which include improved A1c levels, reduced insulin-related weight gain, and easier treatment intensification. Studies have shown the combination of basal insulin and GLP-1 RA may also help minimize side effects (e.g., weight gain) seen with insulin therapy alone.

Xultophy Worldwide Financial Results – Past Five Quarters

| Xultophy | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 |

| Revenue – USD millions (DKK billions) | $153 (DKK 1.0) | $182 (DKK 1.3) | $175 (DKK 1.3) | $178 (DKK 1.1) | $176 (DKK 1.1) |

| YOY (CER) Growth | +30% (+35%) | +62% (+64%) | +8% (+7%) | +6% (+10%) | +8% (+12%) |

| Sequential Reported Growth | -3% | +23% | -5% | -6% | -1% |

Xultophy Sales – 3Q25 Geographic Results

| Xultophy | Revenue – USD millions (DKK billions) | YOY Growth | Sequential Reported Growth |

| US | $8 (DKK 0.1) | -2% (+5%) | flat |

| OUS | $167 (DKK 1.1) | +8% (+12%) | -1% |

Xultophy Sales (1Q17-3Q25)

Pipeline Highlights

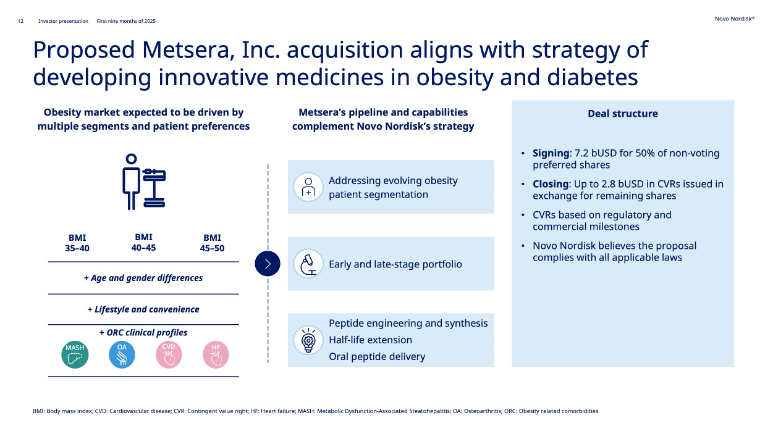

1. Novo Nordisk proposes unsolicited bid of up to $10 billion for Metsera, aimed to complement its own obesity medicines portfolio

In an effort to expand its extensive obesity and diabetes medication portfolio, Novo Nordisk has submitted an unsolicited offer for up to $10 billion to acquire New York-based Metsera, prompting a “Superior Company Proposal” to Metsera’s existing merger agreement with Pfizer. Management shared an interest in acquiring Metsera’s institutional knowledge and capabilities for peptide engineering, half-life extension technologies, and oral peptide delivery, which would be complementary to Novo Nordisk’s current research. Pfizer has alleged that the company is “capturing and killing a nascent American competitor before it gains Pfizer’s support.”

The timeline below details key events surrounding Metsera’s acquisition, following its initial agreement with Pfizer:

- On September 22, Pfizer announced it had signed an agreement to acquire Metsera in a $4.9 billion deal.

- On October 30, Novo Nordisk announced an unsolicited $9 billion offer to acquire Metsera. Following Novo Nordisk’s offer, Metsera notified Pfizer that it considers the proposal to be a “Superior Company Proposal,” triggering a four-business-day period for negotiations.

- On October 31, Pfizer filed a breach of merger agreement lawsuit against Metsera, its Board of Directors, and Novo Nordisk, alleging that Novo Nordisk’s offer cannot qualify as a “Superior Company Proposal” due to significant regulatory risk. Pfizer alleges such risk is identical to a previously rejected proposal from Novo Nordisk to acquire Metsera.

- On November 3, Pfizer filed an antitrust lawsuit against Metsera, its controlling stockholders, and Novo Nordisk alleging that the Danish company’s unsolicited, nearly $9 billion bid to acquire Metsera constitutes an “anticompetitive action” by Novo Nordisk to protect its “dominant” GLP-1 RA market position. Pfizer also submitted a revised proposal for up to $8.1 billion.

- On November 4, Novo Nordisk submitted an updated $10 billion proposal in response to Pfizer’s updated bid. Metsera determined Novo Nordisk’s revised proposal again constitutes a Superior Company Proposal, triggering a two-business-day period during which Pfizer can negotiate with Metsera.

While management did not offer further information on Novo Nordisk’s revised proposal during today’s call, Mr. Ludovic Helfgott (EVP, Product & Portfolio Strategy) expressed confidence in Q&A that proposed deal is in line with legal conditions.

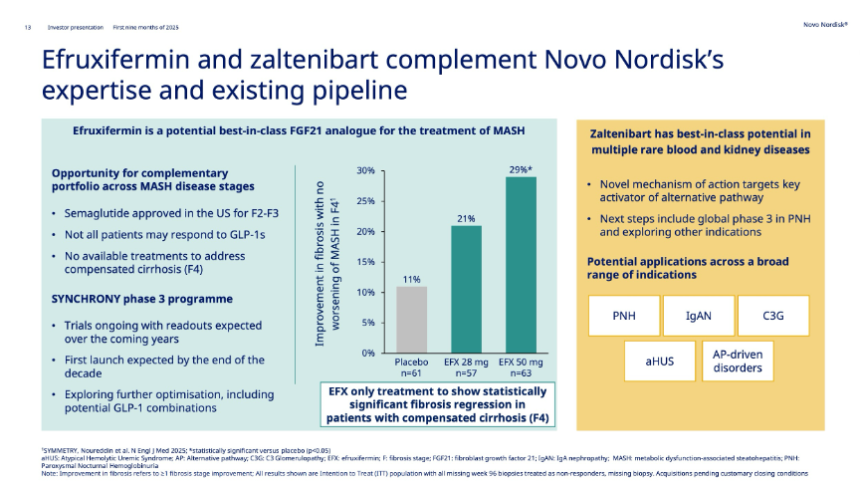

2. Novo Nordisk to acquire Akero Therapeutics and its FGF21 analog for $5.2 billion, expanding its MASH pipeline

In October, Novo Nordisk announced it would acquire Akero Therapeutics and its FGF21 (fibroblast growth factor 21) analog efruxifermin for MASH in a $5.2 billion deal. Efruxifermin is Akero’s lead therapy currently being investigated in multiple phase 3 trials for compensated cirrhosis (fibrosis score F4) and pre-cirrhosis (F2-F3) in people with MASH. Novo Nordisk’s Wegovy (semaglutide 2.4 mg) received approval for moderate-to-advanced liver fibrosis (F2-F3) in MASH in August, joining Madrigal’s Rezdiffra (resmetirom) as the second FDA approved therapy for the treatment of MASH. There are currently no FDA-approved treatments for compensated cirrhosis, where the liver is significantly scarred but still functional.

- Efruxifermin demonstrated therapeutic potential in both pre-cirrhotic (F2-F3) and cirrhotic (F4) stages in phase 2b HARMONY (n=128) and SYMMETRY (n=181) trials, respectively, and is currently being studied in three phase 3 SYNCHRONY trials. Results for the safety and efficacy of efruxifermin in the SYNCHRONY program are expected within the next five years.

Close Concerns’ Questions

1. How does Novo Nordisk expect the new negotiated pricing to affect Medicaid and Medicare coverage?

2. To what extent does Novo Nordisk expect collaboration with retail pharmacies to affect the uptake of Wegovy and Ozempic?

3. How will self-pay pricing of GLP-1 RAs evolve over the next 12 months? Will they continue to decline, and how will this impact prescriptions?

4. Will Lilly’s lower prices of Zepbound’s starting dose ($349 per month) prompt Novo Nordisk to lower the price for Ozempic/Wegovy’s starting doses ($499 per month)?

5. What will the concentration of semaglutide be for Novo Nordisk’s submission of once-daily oral Wegovy, given that a different formulation with an increased bioavailability has been launched in the UK?

6. How does Novo Nordisk assess investment for the future versus current cost-cutting? From the perspective of Novo Nordisk management, what is the balance between expanding the R&D portfolio and continued company-wide restructuring?

Analysts’ Q&A

On overall market share

Q (Carsten Lonborg Madsen, Danske Bank): I'll start out with a sort of a relatively basic question for Mike now that it's the first time you have a quarterly conference call here. If we look at your road show presentation, we can see that in the combined obesity and diabetes market, specifically the GLP-1 market, you lost 9 percentage points of global market share over the last 12 months. That's a significant loss of market share. We obviously knew about this trend. But still, when you look at what you can actually do in terms of strategic initiatives to turn this around, what are the tangible initiatives that you are thinking about implementing? Your drug pricing in the US in Q3 doesn't seem to have a significant delta effect on your momentum in the US market. So, could you provide some examples?

A (Mr. Mike Doustdar, CEO): As someone who has been part of the commercial organization for so long, I would not lie and say I don't like losing market share. However, our current task is to focus the company's strategy on diabetes and obesity, primarily because we see significant expansion potential as we move forward. We are expanding our pipeline through our own activities, as well as, of course, acquisitions. We are getting our costs under control to invest and ensure that no stone is left unturned, and we're putting most of our efforts at this point into expanding the markets.

There are millions and millions of diabetes and obesity patients out there, including in the US, who are not getting their treatments. Launching new products like our Wevogy pill is one way to get there. Other ways is through increasing our commercial partnerships. You have seen Costco, Walmart, GoodRx, LifeMD, Ro, all of those are ways for us to expand the market and really make sure that through that, we succeed and have a successful future. But it does take time for those measures to take effect. It's a marathon, as I have said a number of times now, not a sprint.

Q (Martin Parkhoi, SEB): Mike, with respect to market share loss, because if you look at your old area IO and look at reported sales, then Lilly has actually done a sprint. Two years ago, you had a margin of 80% on sales on reported numbers, and today, you are at 50%. So, can you talk a little bit about, you know, what has not gone wrong for you, but what they have done right in IO to basically capture so much more share than you? Is it commercial execution in IO across the countries, or is it just due to product superiority? Why can they sprint, and you cannot?

A (Mr. Mike Doustdar, President and CEO): So, a couple of different ways to answer your question, Martin. There are markets where we are clearly competing well and gaining market share within IO, and there are markets where we are losing. So, it is market dynamics that dictates IO, and averages sometimes cloud the picture. In certain markets, such as China, the market is not growing as much as we had anticipated. We have said it in the past. It's predominantly because we have never launched a previous version of obesity drugs in that market. At the same time, we have seen in the same market that we're losing the online battle to our competitor, predominantly because of the obesity drug. Wegovy is not allowed to be sold online, whereas if you have a mega brand, then it's a very different picture.

If you take a look at some of the European markets, such as the UK, we have seen growth over a period of one quarter, which has now surpassed our competitors' numbers. So, this is a dynamic market that changes, and it is really to be seen on a longer horizon and not quarter by quarter. We still have a patient base more than two times more than our competitor in international operations. The volume strategy and the future potential of international markets is still incredibly attractive for us. But we came to this market with a very high level of market share, 100% on our own. So, losing market share is something that we had anticipated. And as our competitor comes in and we also enter the next year, it will not just be Lilly, but also in some of the markets, other players will emerge as we lose. So, we have to look at this longer-term. And when we do look at it longer term, I am incredibly optimistic for the volumes and the level of unmet need that exist in international operations.

On acquisitions

Q (Carsten Lonborg Madsen, Danske Bank): The acquisitions you have done or are planning to do will lead to a sort of quite significant cash outflow, especially if you get the Metsera. So, if you have Akero, Metsera, you have CapEx. You also need to pay dividends next year, I assume. Is there anything you could discuss regarding capital planning, capital allocation, and also how high in the hierarchy the dividend payout ratio is in terms of being extremely important for our investors, of course?

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): We have a clearly articulated capital allocation framework, which says invest in the business provided an attractive return; pay our dividend in a consistent manner to pipeline additions through BD and M&A. Finally, if excess cash, do a share buyback. So, that's our framework, which has remained unchanged for quite a while. And, with that, I'm saying that we do have a consistent approach – an approach to dividends and have no intention of changing that.

The starting point is clearly to convert our earnings into cash flow, which we focus on each and every day. And then looking at value-generating opportunities, both organically and inorganically, as in the case with Akero, for example. So, I hope that's clear.

Q (Pete Verdult, BNP Paribas): Mike, don't shoot the messenger, but there are many people who view your pursuit of Metsera as an implicit signal that your confidence in the internal pipeline has waned over the past 12 months. My question is, where do you see the critical differentiation between the assets you're looking to acquire versus the CagriSema and amycretin? Is it just the multi-dosing angle or other factors at play? And then, secondly, and it's a very simple question, but we've heard overnight from our network that neither has been contacted by the FTC for information relating to Metsera. I know you're not going to go into any details, but can you at least confirm if this is actually the case?

A (Mr. Mike Doustdar, President and CEO): I would say, Pete, that I very excited about our own pipeline. I think we have a fantastic pipeline. But when you have an ambition to go to hundreds of millions of people and treat them, then no pipeline is broad enough. So, we have been looking at Metsera for a long time. We are very excited about these assets.

The proposal to acquire Metsera strongly supports our long-term strategy, primarily because these assets are differentiated and complement our products and portfolio. That's why we're doing it. I'll pass it on to Martin, who can more easily explain the differentiation of our own assets to you. But I would say it works very well in complement to what we have.

A (Mr. Martin Holst Lange, Executive Vice President of Development): I can only echo that what we are looking for is complementary to our pipeline. You've heard us speak many times; obesity is not just one disease. It's many different diseases with many different presentations, different patients coming in with different ages, different BMIs, different behaviors, different needs, different body compositions, and different comorbidities. They have different focus areas. And for us to really serve the full palette of suffering from obesity and its comorbidities, we need a diversified pipeline. What we have achieved is differentiation and complementarity. And when we see that, then if we can progress that with diligence

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): Yeah. So, the short answer is that, at this point, we don't want to get into any details around the process. It's still to be determined where everything is going. We know that Mestera was thought superior. And that's what we can relate to. And then I can say, as part of this due diligence, that we conduct a comprehensive review to ensure compliance with all laws and regulations, which is standard practice for any due diligence. We always do that, and we did that here also with the assistance of external experts. We are confident that this deal can close in accordance with the regulations.

Q (Sachin Jain, Bank of America): I'm sure you're expecting the question, but the last couple of years, you've given some high-level color. Would you be willing to just share moving parts as we think about 2026, a lot of factors there, of course, in the base and IO patent, Akero, consensus sitting at roughly 7% sales. So, just any high-level thoughts? Thank you.

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): I think you actually already captured some of the key elements going into your own question. So, the starting point is we do not guide for next year today. We revisit guidance for next year at a later point in time, as we normally do. What I can say is, as always, current momentum is the foundation for future trends in the business. Not saying everything continues, but if a current momentum is where we start, then we have a few specific items worth calling out in relation to next year's growth rates. One is, this year, we have some gross-to-net favorability. I would estimate it to be around 2 percentage points on group sales growth this year. That will not repeat into next year. So, that needs to be factored into our growth rates.

Then, the loss of exclusivity in certain IO markets, we've been calling that out for quite some time, including in our release. This is expected to have a low single-digit negative impact on next year’s sales growth for the group. Then, on sales. Dave was covering the Wegovy pill, which, of course, is our main launch for next year, pending regulatory approval by the FDA. And then the final discretionary factor to call out is Akero and the step-up in R&D cost associated with that transaction, pending closing expected late this year. That will have a 3% negative impact on operating profit growth in 2026.

Q (Mike Nedelcovych, TD): Martin, can you articulate what specifically about the Metsera agents is differentiated from Novo's own pipeline candidates other than the potential for once-monthly dosing? In response to the previous question, you restated that Metsera is different and complementary, but I'm wondering what public data lead you to that conclusion or, if those data are not public, can you confirm that? That's my first question.

A (Mr. Martin Holst Lange, Executive Vice President of Development): I don't want to go into specifics, but maybe just iterate on what we are looking at, where we look for complementarity to our pipeline. It's data on efficacy, and those can be differentiated at many levels. If data on safety and tolerability, a little bit of the same consideration, it's scalability and then, obviously, in this case, the dosing frequency. On more than one parameter, we see complementarity to our pipeline, and therefore, this is an attractive proposition for us.

Q (Emmanuel Papadakis, Deutsche Bank): Maybe follow up on Metsera, the deal structure, and the risk associated with that. Can you just help us understand your comfort with the risk around the way you are structuring? Your offer seems there's a reasonable chance you could end up with 50% of the company you don't control ultimate benefit, preventing someone else from owning them. So, why are you comfortable with that possibility or how do you expect to avoid it? And then just a quick clarification on the Medicare access discussions. What would the upper limit of discount you're contemplating be? Would that be in line with the MSP, or would this be something in addition to that?

A (Mr. Ludovic Helfgott, Executive Vice President of Product & Portfolio Strategy): Well, I think everything stems from, I guess, what you feel as an excitement for the portfolio of Metsera. We really believe in the assets. We believe in the team. And we believe that the deal structure that we have now, which, by the way, as Karsten said, has been vetted and discussed with external counsels and experts and believe that it's in line with all legal standards, boils down to the quality of the asset and the data that we have the confidence in.

So, of course, we know when you get into such an acquisition that this deal will be reviewed, but we're comfortable that even 50% of the shares that we would have in our pocket would be actually worth a lot if the product pans out to be the way we think it is. So, in all cases, as it boils down to science, we believe that we have a good value proposition. Of course, we would prefer at the end to have that in our portfolio from an operational perspective. But the value there, we believe, is really, really high.

On the EVOKE trial

Q (Mike Nedelcovych, TD): We are now less than a month away from the CTAD presentation, so I'm assuming that Novo has the data in-house and is simply cleaning them up before topline release ahead of the presentation. So, my question is, if it is an unequivocally negative result, would Novo cancel its CTAD presentation? Thank you.

A (Mr. Martin Holst Lange, Executive Vice President of Development): On EVOKE, I do want to reiterate, we do not know the data in-house in this room. If we did, we would actually have to issue a corporate announcement immediately. Our starting point is to disclose data, good or bad. We currently aim to present all the data we have.

On the REDEFINE 4 trial

Q (James Quigley, Goldman Sachs): So, firstly, on REDEFINE 4, how important is this in demonstrating differentiation from a physician and a marketing perspective? Have you thought any more about how could behave in a flexible dosing scenario versus other trials in real-world data and can you confirm that you still look to launch CagriSema if REDEFINE 4 shows no statistically significant difference?

A (Mr. Martin Holst Lange, Executive Vice President of Development): Yes, REDEFINE 4, as you well know, we've taken some learnings from REDEFINE 1, more specifically that we needed to do a study. So, we amended the REDEFINE 4 study. That being said, our base case has always been noninferiority with an upside of superiority. In the case of noninferiority on weight loss, we still see a potential for upside on gastrointestinal side effects and tolerability. However, we also believe that the CV benefits we know from semaglutide could potentially pan out, and what we read from REDEFINE 3 clearly differentiates. But I do want to iterate there is still the potential for superiority upside, but obviously in an amended study that should be taken with a little bit of a risk.

On Medicare and IRA

Q (Florent Cespedes, Bernstein): About Medicare, could you share with us your view on Medicare, on one hand, the opportunity if there is a broader coverage of people with obesity on this channel; and the second, about the potential risk or the IRA, the next step on IRA. Could you provide some details about the press release regarding that? Any comments about this opportunity and the associated risk with Medicare would be greatly appreciated. Thank you.

A (Mr. David Moore, Executive Vice President of US Operations): The Medicare opportunity is very important to us and something we've been pursuing since we launched into obesity over a decade ago. We know that there are roughly 30 million people of Medicare age who are suffering from obesity, and that is something that we feel is really important, that those individuals have access to anti-obesity medicines. We can't speculate on what the potential is and how many of those patients will be able to reach. However, we view this as a very important development for us.

Regarding your second question about the IRA, it's not something that we are able to comment on. We are under strict confidentiality with CMS, and CMS will be making the announcement of what those prices are at some point in the near future.

Q (Harry Sephton, UBS): So, just in light of the agreed IRA direct negotiation discounts on semaglutide and also some of the press reports yesterday on potential obesity Medicaid coverage, I don't want you to comment directly, but it appears you'll end up with significantly different prices for your products across different channels. So, I wanted to get your thoughts of how you expect that you're able to maintain the segmented pricing by channel or should we assume that all prices gradually trend towards the lowest level?

Second, just on the current US market trends, can you discuss how you're currently thinking about the levers to improve access and commercial insurance coverage on Wegovy and Ozempic going into next year or do you expect that the majority of 2026 US growth is really going to come from the launch of the Wegovy pill? Thank you.

A (Mr. David Moore, Executive Vice President of US Operations): As we mentioned, we can't discuss any of the specifics around IRA, but we do appreciate the question and the fact that, historically, we have been able to maintain different prices in different channels, given that be Medicaid, Medicare or commercial and, now, you know, our increasingly expanding cash channel. Of course, we can't speculate what that will mean in the future. But, historically, we have been able to maintain the differentiation between those markets and the access that comes with it.

To your second question around the trends, in terms of the quality of access, it's something that continues to be really important for us as sometimes receiving an obesity medication can be a challenge because of the friction that exists in the marketplace. We continue to push for and invest in improved access. It's a clear priority for us. This includes both our cash offerings. It's also what we do with payers. But, you know, we haven't seen a large uptake yet in terms of that opportunity, but it's something that we're going to continue to push for in 2026 access. We don't really expect the access to be largely changed in 2026, but we do know that each of the payers or Medicaid, as we mentioned earlier, you know, have budget constraints and there could potentially be some loss of coverage as well.

Q (Richard Vosser, JPMorgan): You mentioned a couple of times about coverage maybe even getting a little bit worse in Medicaid and maybe even the commercial payers, the barriers staying high. Well, in that case, you know, how should we think about the pricing? Normally, we think about increased rebate levels and increased pricing should remove barriers to get more reimbursement. So how should we think about that going into 2026? Thanks very much.

A (Mr. David Moore, Executive Vice President of US Operations): We continue to have dynamics that we've discussed in the past, continued pressure both in GLP-1, as well as in obesity, with respect to price as we look to unlock more volumes. However, I want to reiterate that the quality of access is a clear priority for. We're working with payers to ensure that the experience is one where patients can receive their medicine more seamlessly. You know, that means lower utilization management, right? That means less of a prior authorization criteria. When we say we're investing in quality of access, that's really what we mean. And that's the focus of our conversation with payers.

In 2026, we don't expect a significant difference in terms of access in the commercial channel. As we mentioned, there may be some in Medicaid. But when we look at the commercial opportunity, you know, I think it is important to note that we have been making progress in terms of access. We continue to believe that the CVS opportunity remains there and that we will see Wegovy as the exclusive branded AOM at CVS in 2026 as well.

On Wegovy FlexTouch

Q (Martin Parkhoi, SEB): On device strategy, a bit of a setback for Wegovy FlexTouch in the US. You had argued that it should be an important part of flexibility in the consumer channel. Is your device strategy also with respect to the launch of products in vials, and in which market would that be relevant?

A (Mr. David Moore, Executive Vice President of US Operations): As you mentioned, it's a setback to receive the CRL and Wegovy FlexTouch. Looking into 2026, we are looking at other presentations. This includes vials. It includes other devices that we're thinking about entering into the market, which would lead to more optionality, especially as we continue to grow in the cash channel as well. On the FlexTouch specifically, we are in active dialogue with the FDA and working through the CRL, but can't comment on any specific timelines yet at this point.

On Wegovy pill

Q (Sachin Jain, Bank of America): On Wegovy pill, just wondered if you could talk about how you're scenario planning around pricing, given some news overnight, and given your API restriction and ability to compete on price, and any further color you can give on launch cadence as we think about that launch.

A (Mr. David Moore, Executive Vice President of US Operations): We're incredibly excited as we move closer to the approval date of the Wegovy pill. I think this is a big step forward in terms of expanding the market and for those individuals that align better with taking a pill for their obesity.

We can't comment on specific pricing, of course. However, I would like to confirm that we will have the Wegovy pill available in all channels. And this is different from previous launches because we will have the ability to focus on Medicaid, Medicare, and commercial, while also offering a cash option through all our various telehealth partnerships, as well as our own NovoCare Pharmacy and the retail partnerships we've aligned with. This is a new approach for us. We're also considering competitiveness. This is a competitive profile in terms of efficacy and tolerability, and we're looking forward to bringing it to people living with obesity in the US.

Q (Mr. Michael Nedelcovych, TD Cowen): On Wegovy's formulary position with CVS, the deal looks to already be having an impact on prescription volumes in the US, Lilly has suggested that the sum total of lives covered that might be affected by the formulary update is roughly 200,000. Does that align with your thinking as well? And how many of those people do you expect will actually make the switch to Wegovy?

A (Mr. David Moore, Executive Vice President of US Operations): We are pleased with what we're seeing so far on the CVS formulary conversion. That conversion is going according to plan at this point. We won't comment on the specific number of lives and what the actual percentage of conversion is. But to tell you that we are seeing things that are largely in line with what we expected and what was in the plans.

Q (James Quigley, Goldman Sachs): Can you talk through the launch preparations for oral Wegovy in ex-US? In the release and in the comments, that you might look to launch in select IO countries versus previously, when is it likely to be mainly focused on the US? So, what's happened such that you consider also launching in the ex-US and how do you balance this with the US launch processes and pricing?

A (Mr. Ludovic Helfgott, Executive Vice President of Product & Portfolio Strategy): So, let's take a step back. The real focus and the priority of our Wgovy pill launch is the US and will remain the US in 2026. As you rightly read, we are, indeed, opening the option to launch in selected markets in the course of 2026, of course, depending on how things are ramping up. And we are definitely ready to launch in these markets to be able to make the best and the most of the Wegovy pill. And by the way, we are also very quickly transferring some knowledge from the telehealth channels, for instance, in the US into some IO markets. We are very active right now as we speak in many markets across the world, not just in Europe but also in Australia, for instance, or in other part of the world where we believe that we really are gaining progress on the telehealth side.

So, again, we are accelerating our overall experience curve on the telehealth and that would be proven very helpful at the time we launch the Wegovy pill. it's also noteworthy to say that the IO markets are also markets where we have some of the nicest experience and Rybelsus in Europe and elsewhere, which means that we can also leverage our experience in the oral markets for Rybelsus with the Wegovy pill. So, priority to the US, but fully ready to take on some selected markets in IO when the time comes.

On telehealth

Q (Richard Vosser, JPMorgan): Mike, you alluded to more telehealth involvement, particularly in the US. I think prior arrangements have faced challenges, given that they continued to bulk compound. There has been some discussion about continuing or new agreements, as well as the wider involvement of telehealth. So, I wondered what was different this time and whether there was any evidence of any increased pressure around from the FDA or legal pressure to remove the compounders, and what could change on that front.

A (Mr. Mike Doustdar, President and CEO): No increased pressure, to answer your question directly. However, we have been quite consistent regarding the illicit API that is coming from China and being used by compounders. We find that, since these are not FDA-approved, their safety is questionable. And as a pharma company, we don't basically like that. That hasn't changed at all. We also have been saying that we need to increase our access and we need to find ways to get to many more patients. The cash channel and telehealth is definitely an attractive way to go about it. In that context, we're having dialogue and discussions with multiple players on how we could actually increase our access. And then we will see with who we should go into partnership. We've made a number of those partnerships available. So, we talked about Costco. We have talked about Walmart and ongoing dialogues with many, many more are ongoing in pursuit of our market expansion that I spoke to earlier on.

--by Kayla Mathieu, Elizabeth Rose, Kat Moon, Esther Min, Monica Oxenreiter, and Kelly Close