Dexcom 4Q25 – Record global revenue of $1.3 billion (+13%) in 4Q25, driven by coverage expansions for T2D internationally; userbase exceeds 3.5 million; full-year revenue of $4.7 billion –

Executive Highlights

- Dexcom reported its 4Q25 and full-year 2025 financial results today on a call led by CEO Mr. Jake Leach and CFO Mr. Jereme Sylvain – see the press release, webcast, presentation, and Form 10-K.

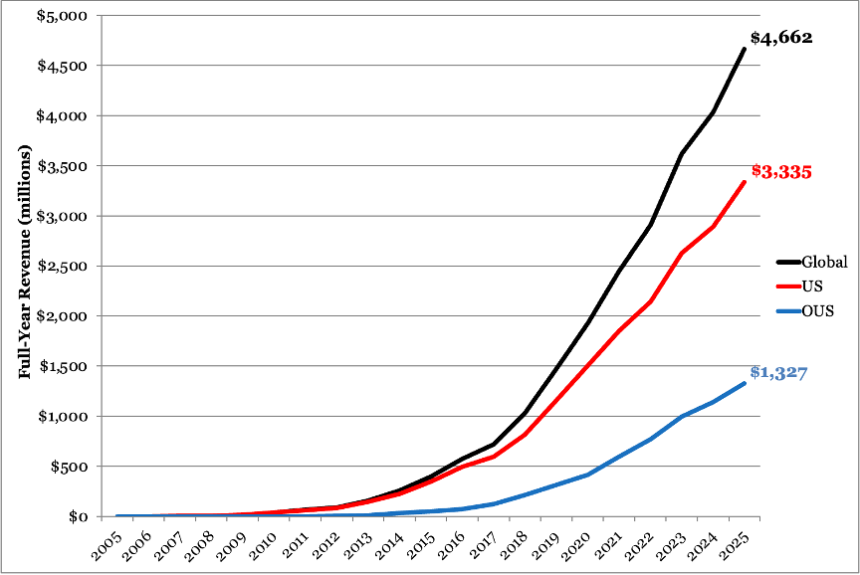

- Global Dexcom revenue totaled $4.66 billion in 2025, up 16% from 2024. Full-year US revenue totaled $3.3 billion, up 15% from 2024, while full-year 2025 international revenue was $1.3 billion, up 16% from 2024. 4Q25 revenue totaled $1.26 billion, up 13% from 4Q24 and 4% sequentially. US revenue totaled $892 million, up 11% from $803 million 4Q24 and 5% sequentially from $852 million in 3Q25, accounting for 71% of global revenue. International revenue totaled $368 million, up 18% from $310 million in 4Q24 and 3% sequentially from $357 million in 3Q25.

- Management particularly highlighted strength in several international markets that have recently seen coverage expansions for its T2D populations, including Germany, the UK, and France – with France being among Dexcom’s fastest-growing markets. Mr. Leach also remarked that Dexcom is “just getting started” in the Asia-Pacific region, with recent coverage wins in Japan. We’d like to see far more focus on Asia ourselves, as well as many parts of the EU that are not yet focus areas.

- Dexcom reiterated full-year 2026 revenue guidance of $5.16-$5.25 billion, representing approximately 11-13% growth. Mr. Sylvain said guidance assumes: (i) continued category growth; (ii) incremental growth contribution from Stelo and new product advancements; and (iii) a predominantly unchanged coverage landscape in the near-term, while still pushing for broader CGM access globally. This arena seems full of change from our view …

- In pipeline updates, management discussed the broad rollout of the Dexcom G7 15 Day system in the US, which began in December 2025. Mr. Leach also reviewed several new products and features that Dexcom has received clearance for in recent months. This includes My Dexcom Account, Dexcom’s newly launched digital support system to streamline the customer support experience, and Dexcom Smart Basal (a CGM-integrated basal insulin dosing feature for adults with T2D) that will see an early access launch in select US clinics this month (we look forward to learning about which ones). Dexcom continues to work on launching Stelo and a new CGM in Dexcom’s ONE+ category internationally in 2026.

- With the two largest CGM manufacturers reporting their 4Q25 updates, we have a sense of the CGM Market. In 4Q25, Abbott and Dexcom’s combined CGM revenue totaled approximately $3.3 billion, up 12% from $2.9 billion in 4Q24 and up over 30% from $2.4 billion in 4Q23. Sequentially, the combined revenue increased by 2% from $3.2 billion. Growth in 4Q25 reflects continued expansion of CGM adoption in new populations, with both companies highlighting sustained momentum in T2D. It also reflected strong growth, if not “in every geography,” in many geographies for sure!

- Mr. Leach also confirmed that Dexcom will host its Investor Day in May 2026 at its manufacturing site in Mesa, Arizona. We look forward to hearing additional updates on its innovation pipeline, including more details on Dexcom G8, there! It’s brave and smart to plan an investor day in the hot, hot, hot sunshine of May in Mesa – we know they are getting a great deal on this financially!

See below for our top highlights.

Table of Contents

-

Financial Highlights

- 1. Worldwide 4Q25 revenue of $1.3 billion, up 13%; full-year 2025 totals $4.7 billion, up 16%

- 2. GAAP gross margin of 64%; GAAP net income decreases 6% sequentially to $267 million; cash flat from a year earlier

- 3. JPM 2026 guidance reiterated for full-year 2026 revenue of $5.16-$5.25 billion (+11-13% growth)

- Business Highlights

-

Pipeline Highlights

- 1. Hardware pipeline: G7 15 Day now available for US adults with diabetes in all channels in the US; no commentary on Dexcom G8

- 2. Software innovation: Progress in My Dexcom Account, Smart Basal launches

- 3. New CGM in Dexcom ONE+ category to launch OUS in 2026

- 4. Integration with Epic EHR grows to over 160 healthcare systems

- Analyst Q&A

- Close Concerns’ Questions

Dexcom Full-Year Revenue (2005 – 2025)

Financial Highlights

1. Worldwide 4Q25 revenue of $1.3 billion, up 13%; full-year 2025 totals $4.7 billion, up 16%

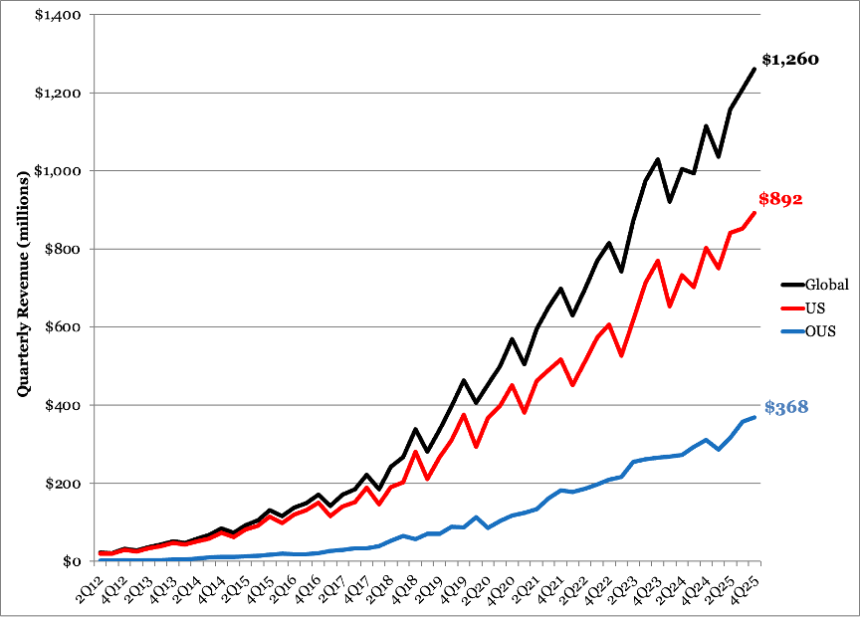

Dexcom Quarterly Revenue (3Q12 – 4Q25)

In line with its preliminary 4Q25 announcement ahead of JPM 2026, Dexcom reported a record global revenue of $1.26 billion in 4Q25, up 13% from 4Q24 and 4% sequentially. Absolute YOY revenue growth in 4Q25 was $629 million, reflecting strength both in the US and internationally. Mr. Sylvain attributed the momentum to Dexcom’s ongoing G7 15 Day rollout in the US and improvements to its product experience with new hardware and software innovation.

- US revenue totaled $892 million in 4Q25, up 11% from 4Q24 and 5% sequentially. The US continues to represent the majority of Dexcom’s business, accounting for 71% of total revenue this quarter, nearly flat from 72% in 4Q24. This is mostly consistent across previous quarters, which fluctuated from a low of 71% in 1Q23 and 2Q23 to a high of 75% in 3Q22. In 3Q25, US sales represented nearly 70% of global sales. Full-year 2025 US revenue totaled $3.3 billion, up 15% from 2024.

- In Q&A, management attributed growth to a combination of fewer sensor deployment disruptions and the early adoption wave following G7 15 Day availability. He also referred to positive impacts of better prescriber education, as clinicians better understand the shifting T2D coverage landscape and become more comfortable with CGMs.

- International sales totaled $368 million in 4Q25, up 18% from 4Q24 and 3% sequentially. Management called out particular strength in Germany, the UK, and France, the latter of which is one of Dexcom’s fastest-growing markets following T2D access expansion. Full-year 2025 international revenue was $1.3 billion, up 16% from 2024.

- In Q&A, Mr. Leach framed future international growth as a two-part opportunity: (i) by deepening penetration in markets where Dexcom is already established as coverage expands from intensive insulin into basal and beyond; and (ii) by expanding geographically, including recent expansions in the Asia-Pacific regions.

- Global revenue totaled $4.66 billion in 2025, up 16% from 2024. Revenue in 2025 came in slightly above the high end of Dexcom’s 2025 guidance of $4.63-$4.65 billion.

2. GAAP gross margin of 64%; GAAP net income decreases 6% sequentially to $267 million; cash flat from a year earlier

Dexcom reported a GAAP gross margin of 64% in 4Q25, up from 59% in 4Q24 and from 61% in 3Q25. Mr. Sylvain attributed margin expansion to lower freight expenses as Dexcom reestablished ocean shipping during the quarter and improving scrap rates as supply chain performance continued to normalize following manufacturing and sensor quality work in 2025.

- GAAP net income totaled $267 million, up significantly from $152 million in 4Q24 but down from $284 million in 3Q25.

- Dexcom ended the quarter with $2.6 billion in cash and cash equivalents, flat from 4Q24 and down from $3.3 billion in 3Q25. Mr. Sylvain also emphasized that Dexcom surpassed $1 billion in free cash flow for the first time in 4Q25.

3. JPM 2026 guidance reiterated for full-year 2026 revenue of $5.16-$5.25 billion (+11-13% growth)

Management reiterated full-year 2026 revenue guidance of $5.16-$5.25 billion, representing 11-13% growth from 2025. Mr. Sylvain said this guidance assumes: (i) continued category growth; (ii) incremental growth contribution from Stelo and new product advancements; and (iii) a predominantly unchanged coverage landscape in the near-term, while Dexcom continues to push for broader CGM access globally.

- Non-GAAP gross margin is guided to 63-64%, with expansion expected as Dexcom benefits from lower freight expenses and manufacturing expenses, as well as increasing contribution from the G7 15 Day.

- Dexcom expects operating margin of ~22-23% and adjusted EBITDA margin of ~30-31%, while planning for incremental hiring and spending to support launches. Mr. Sylvain also discussed the Ireland manufacturing facility ramp in late 2026. These investments were explicitly linked to readiness for broader global coverage, including its expectation for Medicare coverage expansion to T2D non-insulin populations, over time.

Business Highlights

1. Record new user starts in 2025 driven by global T2D population as Dexcom pushes for broader global coverage

Dexcom reported record new patient starts in 2025, with its global CGM user base exceeding 3.5 million, up more than 20% from roughly 2.8-2.9 million at the end of 2024. New starts in 4Q25 were at near-record levels, as some patients who had delayed initiation while waiting for the G7 15 Day began on the sensor. Management cited strong sell-through and utilization trends across both US and international markets.

- Management highlighted strength in several international markets that have recently seen coverage expansions for its T2D populations: Germany, the UK, and France. France was among Dexcom’s fastest-growing markets. Mr. Leach also remarked that Dexcom is “just getting started” in the Asia-Pacific region, with recent coverage wins in Japan. Management suggested that, long-term, the international opportunity could ultimately surpass the core US market given the size of the global T2D population. Dexcom also highlighted its plans to launch a new CGM product in its Dexcom ONE+ category to reach new international populations currently without coverage. Moreover, the non-insulin T2D population remains another significant untapped opportunity, and Dexcom eventually hopes to enter prediabetes and other populations.

- In the US, commercial coverage for T2D non-insulin users began expanding last year, and Dexcom is awaiting a potential Medicare decision that could extend access to nearly 12 million additional patients. Dexcom is building CGM capacity in anticipation of this expansion.

- Evidence generation remains central to these coverage expansion efforts. Dexcom anticipates a readout of its randomized controlled trial in people with T2D not on insulin mid-year. Moreover, Dexcom’s internal registry data in reimbursed non-insulin users shows strong health outcomes and utilization rates comparable to basal insulin users, reinforcing that reimbursement drives sustained engagement. In the meantime, the ADA has strengthened its Standards of Care further supporting CGM use in this population. For reference, the 2026 guidance expanded CGM eligibility to include individuals on non-insulin therapies that may cause hypoglycemia and for any diabetes treatment where CGM helps in management.

2. Stelo use grows in the US as Dexcom prepares to launch OTC CGM internationally

Stelo adoption accelerated in 2025 following its late-2024 launch. At JPM 2026, Dexcom reported $130 million in full-year 2025 Stelo revenue with more than 500,000 users and a “strong majority share” of the OTC CGM market. This represents the high end of the previously guided 2-3% contribution to total company revenue.

- Management reiterated that a nutrition database and AI-enabled enhancements will launch “shortly” within Stelo’s Smart Food Logging feature. This builds on broader product enhancements, including the initial rollout of this AI-based meal logging tool to Stelo in July 2025 (previously available only on G7). The enhanced feature provides macronutrient tracking and detailed meal breakdowns, helping users better understand how food choices affect glucose trends. These updates precede a fully redesigned app expected in the “coming months,” which aims to offer a more consumer friendly experience.

- Dexcom also plans to expand Stelo availability internationally in 2026, though specific geographies were not disclosed. Mr. Leach noted that Stelo is attracting a broader user base, including people with T2D not on insulin therapy – a population that currently lacks CGM coverage. He positioned Stelo as an entry point into the CGM ecosystem, with the potential to transition users to G7 as reimbursement coverage expands.

3. Management touts progress in manufacturing and logistics

Dexcom emphasized meaningful operational progress in manufacturing and logistics. During 4Q25, the company rebuilt its finished goods inventory to its preferred levels, reestablished more efficient ocean freight shipping routes, and strengthened its overall supply chain performance. These improvements continued to reduce the sensor deployment issues identified earlier last year, which were a focus of Dexcom’s 3Q25 call. Management also expects these improvements, as well as growth of the G7 15 Day adoption, to support gross margin improvement by 200-300 basis points in 2026. Dexcom continues to make meaningful progress on its new Ireland manufacturing facility, which is projected to begin production in 4Q26.

Pipeline Highlights

1. Hardware pipeline: G7 15 Day now available for US adults with diabetes in all channels in the US; no commentary on Dexcom G8

Management highlighted the broad rollout of the Dexcom G7 15 Day system in the US in December 2025. The sensor first launched in the DME channel and became available through the pharmacy channel as well in early January. Mr. Leach said that initial patient feedback has been “excellent,” with patients and physicians particularly thrilled by the longer wear time necessitating fewer monthly sensor changes. He also highlighted its new algorithm, which offers improved accuracy compared to the 10-day G7 (8.0% MARD vs. 8.2% MARD). G7 15 Day is already integrated with Insulet’s Omnipod 5 and Beta Bionics’ iLet, and he said at JPM 2026 that Tandem integration “will come very soon.” Dexcom’s near-term focus includes building greater of this product’s availability in the market.

- There was no commentary on Dexcom G8 in today’s call. Mr. Leach has previously described Dexcom G8 – which will feature a 50% smaller wearable, a next-generation chipset, and support for multi-analyte sensing (with ketone measurement among the first publicly disclosed analytes in development) – as a cornerstone of the company’s innovation strategy. Dexcom has not disclosed a timeline for regulatory submission or launch, though Mr. Leach teased that further details will be shared at an investor event in May at Dexcom’s Mesa, Arizona manufacturing facility.

- However, Mr. Leach highlighted clearance for a new patch technology Dexcom received last week. The technology has demonstrated in clinical trials the ability to strengthen sensor survival on its G7 system, including the G7 15 Day. It will also later be brought to Stelo and Dexcom ONE+.

2. Software innovation: Progress in My Dexcom Account, Smart Basal launches

Mr. Leach highlighted several new products and features that Dexcom has received clearance for in recent months. This includes My Dexcom Account, Dexcom’s newly launched digital support system to streamline the customer support experience. He also teased future additional offerings planned that integrates AI into this customer experience.

- Dexcom will initiate the early access launch for Dexcom Smart Basal this month. Dexcom received FDA clearance for the CGM-integrated basal insulin dosing feature for adults with T2D in November 2025. Management highlighted Smart Basal’s potential to become the “new standard” for any person managing T2D with basal insulin, as it aims to enable more accurate basal insulin titration, accelerate the time to reach optimal dose, significantly simplify workflows for the prescriber, and improve outcomes for those using our products. Dexcom has already selected several clinics around the US to pilot this technology, informing Dexcom about optimizing clinical workflows and patient outcomes ahead of a broader national launch.

3. New CGM in Dexcom ONE+ category to launch OUS in 2026

Dexcom plans to expand its international portfolio in 2026 with the launch of Stelo and an additional CGM system positioned within its lower-cost Dexcom ONE+ category. This reinforces management’s strategy to broaden access across diverse reimbursement and pricing environments globally. Mr. Leach emphasized that Dexcom’s international growth focuses on expanding coverage and tailoring its product portfolio to meet different market structures. The addition of another CGM platform is intended to reach into new patient segments and price-sensitive markets that the current portfolio does not fully address. Mr. Leach reiterated that Dexcom’s tiered product strategy has already led to meaningful international coverage and share gains, particularly where reimbursement structures differ from the US.

4. Integration with Epic EHR grows to over 160 healthcare systems

Dexcom reported that its Dexcom Direct EHR integration is now live or onboarding at over 160 healthcare systems, representing a meaningful expansion from ~100 systems in 2Q25. Mr. Leach framed EHR integration as a key component of Dexcom’s strategy to elevate the customer experience for users and clinicians alike. The integration enables seamless transmission of CGM data into multiple EHR platforms including Epic, reducing workflow barriers and making it easier for clinicians to access glucose data without requiring separate portals.

Analyst Q&A

On coverage expansions

Q (Matt Taylor, Jefferies): Jake, I wanted to ask you on your first call as CEO to talk a little bit more about some big picture items that you mentioned in your comments that feel like the company is early on the glucose sensing journey. I'd imagine a lot of that has to do with the potential coverage to come here in the future. I wanted to have you talk a little bit more about where the existing legacy and core markets could go in the coming years, but also with an eye to non-intensive type 2 coverage that we could see coming over the next 12 months to 24 months. Thanks.

Mr. Jake Leach, CEO: Thanks, Matt. You know I really do think we're in the early innings of a game here with when you think about the size of the problem out there with metabolic health and the growth of diabetes globally. And then you look at the solutions that we provide with our technology and the outcomes that we can drive. If you look across every segment of patients that we serve, whether it's type 1, type 2, insulin users or type 2 non-insulin users, we drive significant outcomes, both health outcomes for the user and their prescribing physician, but also financial outcomes for the health systems. And so, the awareness of those outcomes continues to grow.

We've been generating evidence for years to help unlock the access for millions of users. And so, as you mentioned, you know, as we look at the landscape of coverage we've started, towards last year, seeing coverage unlocked commercially for type 2 non-insulin users. And we are on the verge of, of expansion into the broader group of type 2 that are covered by Medicare. And so, when that expansion happens it's almost 12 million people that would then suddenly get access to CGM. And so that's why when I think about the road ahead and the durable years of growth we've got, there's just this tremendous opportunity to have an impact on the lives of many people.

As you think internationally, too, the opportunity there is pretty significant. And as I mentioned in my comments, we see it as being larger than the US over time now internationally. Typically, the coverage trails a bit from the US, but with the evidence we continue to generate and the awareness we continue to generate, we're confident that over time this access is going to continue to open and provide opportunity for us to impact more lives.

Q (Larry Biegelsen, Wells Fargo): I'll follow up on type 2 non-insulin treated patients. Jake, based on your response there, it sounds like you think it's coming soon – the CMS proposal. You know, your main competitor is expecting [a CMS proposal in the] first half of 2026. Are you in agreement with that? When should we expect to see the RCT data? Lastly, how do you want us to think about the kind of potential impact from CMS coverage of type 2 non-insulin? Thanks for taking the question.

Mr. Leach: Thanks, Larry. You know as we continue to work with CMS and you know, actually as we've been sitting here waiting for the coverage decision from them, we've actually had the ADA update their guidelines for type 2 non-insulin had really, further moving towards recommending the product for that group and recommending that they have the choice. And so, I think that's clearly based on the real-world outcomes that we've been generating.

So, we mentioned, at JPMorgan around the registry that we've started for non-insulin users. And that's basically people that have coverage today that are type 2 non-insulin users. We're seeing great sustained outcome in terms of health improvement and high sensor utilization. And so that gives us confidence that we know that we can make an impact in this population. And clearly, the private payers have seen that and have started moving the direction of coverage.

And so, we're going to continue to do everything we can do to support a coverage decision here with Medicare, which one of the things you mentioned is our randomized control trial in type 2 non-insulin users that that trial. We're very excited to read that trial out here towards the middle of this year. And you know it's a trial consisting of about 300 people across two arms: those who weren't using CGM and those using standard care methods. And we are fairly excited to share the results of that as we get towards the end of the study.

Q (Marie Thibault, BTIG): Good evening. Thanks for taking the questions. Jereme, I wanted to discuss pricing. You mentioned a couple points of pricing. One of the factors was some of the commercial unlock of the type 2 non-insulin patient population. How would you have us thinking about any potential pricing headwinds as we think about the Medicare unlock that could be coming here in the next 12 months or so? Of course, volume will be an offset. The amount of volume mix will make a difference. But how would you have us thinking about that in regard to the couple points that you referenced with the commercial unlock?

Mr. Jereme Sylvain, CFO: Every year when we go through negotiations, it's interesting. You know, we're always asking for more coverage. And for good reason. Right? There's a lot of folks who ultimately need it. And we know that we can deliver value really to all pathologies. But every year there's it's the classic, you know, volume, price conversations and everybody goes through it. And it's been pretty stable for some time.

As you're so, so nothing new this year, but, you know, in the context of how you're thinking about, you know, CMS and, you know, coverage and how that unlocks, you know, I think the way CMS at least has done work around this space is they've done the work around competitive bidding. Really. That's where the rubber hits the road in terms of how they're thinking about it from that perspective. If you think about how the approvals work, you know, there's, there's an LCD code ultimately that is approved. And, and, and that coding applies to where the coverage ultimately sits. That typically does is the approval the pathology approval. It's the guidelines. The rules pricing is typically handled separately from that.

And so, I think what you've got is you've already got a natural mechanism in place for what is a fair value is through the competitive bidding process, which I will obviously work through. And we'd expect that to kick in really here more in 2028. So, I think that's at least how we're thinking about it in terms of how that unlock would play out – “statutorily”, is, maybe, the best way to put it. Should something change will certainly keep you posted, but at least that's our read on kind of how the that would play out. And we'll know a lot more [going forward] - right.

Obviously, we're excited about CMS coverage. We talked about it. We're building for it as we speak. I mean, as we start to build capacity today, we're building to be ready for it as if it came tomorrow. So, I mean, that's how bullish we are on, on it coming. And so, you know we'll certainly give you more and more feedback as we go because we obviously expect it to be a key part of everything we do this year, including obviously in RCT readout, which again, we'll have here in the first half in the middle of the year. Obviously, it's going to be in the first half. We committed to that. But as we kind of move here over the next few months.

Q (Zachary for Bill Plovanic, Canaccord Genuity): Thank you for taking the questions. Back to the G7, non-intensive type 2 market. So, in the past, you say, you know, right now we have 6 million covered lives and we can get to 25 million. You said Medicare would be 12 million. So just where do we stand today? And then, you know, and just [can you] explain what I guess the cadence of covered labs could look like? Thank you.

Mr. Sylvain: So, you are really thinking about the commercial side of the house? Obviously, the Medicare side of the House will start with fee for service and then you move into advantage. So, you know, it'll go Part B, then into Part C, and we can talk about that as it comes. But that should happen pretty quickly. On the commercial side, the side I think you're more alluding to in progress we've made, you know, we talked about 6 million lives. It was the three big PBMs, and we talked about knocking down, you know, some additional plans, et cetera. I think the expectation is we've knocked down, you know, another five-ish 5-ish% percent of that market over the course of renewals this year. But that will continue to take place. We keep working that it doesn't have to happen just annually. It's something that we'll continue to do over the course.

So that would be, you know, individual plans kind of smaller. PBMs, PBMs on custom formularies. So, we got another good chunk of it, I think. But you know we'll keep chipping away at that. So, it puts you at maybe 6.5 million of the 12.5, maybe a little bit higher than that even. But we'll keep chipping away. But that's at least the updates. We have a few more in there that continue. And you know, I would expect to give you updates over the course of the year as we keep chipping away and try to get that to, to full coverage over time.

On Dexcom’s innovation pipeline

Q (Jayson Bedford, Raymond James): Good afternoon. I had a question on basal, which seems to be the segment of the market that's taking a little longer to evolve. What's been the hurdle to deeper adoption into this segment? And do you view Smart Basal as a tool to kind of reintroduce G7 to this population and drive better growth?

Mr. Sylvain: Thanks for the question. You know, to your point, we do feel like Smart Basal is a great opportunity for us to meet the needs of the patients. I think we've seen good growth in basal given the population and the coverage. And as we continue to want to expand that across the globe, we're going to use this new tool. And it's really designed to improve the user experience, both for the patient and the prescribers, so that when they think about a patient who's going to go on to basal insulin therapy, this is the product they should get. They should get a G7 paired up with Smart Basal and the system. We're very excited to start piloting that that technology this month.

So, we've got a number of clinics across the United States already selected. They'll come on, and we intend to learn from the workflows and how this product fits in seamlessly to their workflow

and drives the outcomes that both the patients and the physicians are after getting to the right dose faster so that they can really see the benefit of that insulin therapy. I think as we do more of that and we get the experiences around it, it's going to drive more and more share of that patient population feel better.

Q (Brandon Vasquez, William Blair): Thanks for taking the question. I wanted to focus, you know, a little bit on the innovation pipeline, but I know there's a lot to be done on the hardware. So, we're talking about a G8 and things like that. But there's a lot of software you guys are coming out with, like Smart Basal. We were just talking about Stelo and Neo tracking things like that. It has just been a minute. Talk to us a little bit about what is left in the pipe pipeline on the software side. Like, what else can you do here? What else can you leverage the software side for? And then maybe the kind of follow up to that is, do you think at some point you need to start to validate these features in clinical trials for them to make more meaningful impacts and drive kind of large-scale adoption?

Mr. Sylvain: Yeah. Thanks, Brandon. Fantastic question. No, we are nowhere near done. There's so much more we can do on both. As you mentioned, the hardware, but also on the software. You know, our goal is to be the premier glucose sensing solution for all people, which what that really means is that it takes into account all the different journeys that a patient has from becoming aware of our product to a physician prescribing it, to the patient onboarding to them using it and driving the outcomes that are so important.

And then of course service in all of those aspects. If you think about that whole journey, there's many things that we can continue to enhance digitally through software, whether it's for the physician or for the patient themselves, to help them onboard faster. So really our goal is to remove friction, to remove any kind of speed bumps so that they get the experience that is the highest caliber. And so, we're trying to develop the best solution plus the best experience. And we do feel like over time, that's going to be the winning formula, because you've got folks that are not only seeing the outcomes, but they're also sticky and staying and retained and having a wonderful experience for many years to come. Basically, increasing the lifetime value, you know, driving those outcomes, as you mentioned, is very important for us to run clinicals and or generate real world evidence that shows the outcome of how those new features do actually drive outcomes.

And we've done that, you know, basically through all the different patient segments. We've done some recent work with real world evidence in type 2. But even things like our delayed high alert, which is an innovative feature that is built into the product that basically delays the high alert and it has clinical outcomes associated with it. And so that's something that, as our sales force gets out there and talks to physicians, they can talk about the difference, the competitive difference that we provide in the outcomes that we drive. And there's one thing I wanted to mention is our sales force is so fired up right now, based on the 15-day and all the enhancements we have coming, we're really looking forward to spending some time with them at the national sales meeting in a couple of weeks, but there's so much more we can do, and I can't wait to show you guys over time all the innovation that we're going to bring.

And to your question, the whole clinical, you know, validation of features, you know, I think the, for example, I mean, most of these that's exactly what you do, right? I mean, you think about Dexcom Smart Basal that goes through obviously a 510(k) clearance. So just think about all these features. They're all going through the appropriate clinical pathways where appropriate and where we're meaningful. So, expect us to continue to do that, but also expect us to look at new and novel ways to navigate technical features into the hands of users over time and work with the administration on how we do that. And there's obviously a lot of guidance coming out now about how to bring innovation quicker. And the R&D team is teed up to do just that. Just to do that is to bring innovation quicker and quicker and put it in the hands of users.

On G7 15 Day

Q (Travis Steed, Bank of America): I wanted to ask about the 15-day sensor. How we should think about the rollout of that, the impact on margins, and the use of that to open up new markets? I heard you mention new products launching internationally and talking about international getting to be bigger than the US, which is only 30% of your company today, so, a lot of international growth there. I wanted to touch on those two topics.

Mr. Sylvain: I can certainly start on the margin side and then I can turn it over to Jake in terms of, talking about long-term opportunities outside the US. So, you know, as we think about the 15-day product, clearly in the US, it's launched. And we'd expect that to certainly start to contribute to margins over the course of this year. The reality is it starts to contribute to margins even more in future years, because this is a year about getting folks interested, making sure they understand the benefits and really converting a base over time. We'll start with new patients and we'll convert the base. So, the contributions, yes, there will certainly be some help this year. And you can see that in our gross margin guidance.

But the real opportunity starts as you get further out. Obviously, Stelo is on a 15-day platform. G7 has moved to that platform. You can imagine most of our products move to that platform over time. And as we launch out new product platforms, that's obviously the focus. So, you can see where that becomes kind of the basis for launching and that cost. Ultimately, it becomes a bit of an advantage, right? In terms of going into new markets. It's really hard to get into this space. There's a few companies that can really produce it and Stelo is how you're able to build the product at a cost that as you move into, say, some emerging markets where you can take advantage of those opportunities both where length and cost and ultimately delivering the highest quality product within those confines.

I do think it does provide us an opportunity, not only from a margin perspective, but also from the opportunity of expanding and driving new opportunities where there's a fit for need purpose for our product. You've already seen us move to fit for need, where you start to see our product portfolio strategy outside the US. This just helps us continue to drive down that pathway. Jake, I want to give some just thoughts longer term on international and what we can do with that.

Mr. Leach: The 15-day product where time will be extending that to the portfolio globally. So, we've launched it on Stelo. We've launched in the G7 here in the US. We're going to extend it globally. And the feedback from users has been pretty incredible. One note that's important is that, over the time frame that we've had G7 in the market, we've made a lot of enhancements to the product and to the technology, to the processes. Everything about how we build that sensor and provide it to users has been enhanced. And so, the 15-day product got all of that from day one.

So, as we launched this new version of G7, we're seeing great feedback about both the longevity, the sensor, the reliability, but also the accuracy. This is the most accurate sensor we've ever produced and users are noticing it. You can see it out there in the blogs. You can see it in customer feedback. They really are seeing that this algorithm enhancement we've made is playing through in their experience, which is important as we are striving to continue to be the premier glucose sensing solution for all, and so excited about the ability to continue to expand 15-day across the portfolio.

Q (Josh Jennings, TD Cowen): Good afternoon. Thanks for taking the questions. I wanted to ask a two-part question on G7 15 day. Sounds like the early patient experience has been strong. Great durability with such lasting out to 15 days. I just wanted to see if there's any more color on any or any data you have, just on that durability of wear. And does the patch that you just got approved the new adhesive technology maybe improve the percentage of sensors that get out to 15-day out into the 90% range? And then I guess it's a three parter, but just any rebate dynamics that we should be thinking about in 2026 as G7 15-day enters the pharmacy channel? Thanks for taking all the questions.

Mr. Leach: Thanks, Josh. Yeah. Sensor survival longevity, as we call it, is a super important and super important part of the CGM portfolio. And as we extend sensor, where it's obviously something we look closely at, it's actually our goal is to ensure a good user experience. So, we don't unlock that extended life until we're confident in its performance. And so, in the field, what we're seeing is very consistent across the patient spectrum with what we saw in our clinical studies.

Now we recognize that, from the very early days of CGM when our first CGM only lasted three days, not all sensors last. And often it's as, as you mentioned, related to adhesive. And so, we have been driving adhesive innovation for several decades. And with the new version of the patch for G7, we are excited that it does drive a pretty meaningful improvement in survival. And we will put it across the whole portfolio of Dexcom ONE+ and Stelo so that all of our patients get the benefit. So, it'll continue to drive that performance for any sensor that doesn't.

For any sensor that doesn't last the period of time, we have a very robust program that we continue to enhance around how to ensure patients always have the sensors they need, because we know how important this technology is to all of our users and the benefits they get from it. So that goes back to that. The idea of setting the bar for service and being the gold star there. We are making investments there. We're continuing to enhance the way that we handle those types of situations to ensure our users get the best experience.

Mr. Sylvain: Then just your question on rebates. The, there's two ways to think about rebates. One is what is the rebate rate and what is the net price. And then the second piece is how many folks select, you know, essentially the rebate rate in those plans. The rebate rates in terms of, you know, the pricing flooded right into the G7 10-day. So effectively G7 15-day, G7 10-day are effectively the same price. So that for a month supply I think that's important. So, effectively same revenue per month. On the flip side, in terms of utilization, you know, our expectation or realization of selection or inclusion into that rebate catalog, our expectation is 100% of all those sensors. So, you know, sometimes you start at 96, 97, 98. You know, you move up those areas. Someone folks, you know, some say not preferred or not covered. 15-day essentially is slotting in right where G7 is. So, we're at 100%. We shouldn't see any changes essentially in rebate trends as a result of moving over 15-day.

On 2026 guidance

Q (Robbie Marcus, JP Morgan): Thanks for taking the question. Jereme, I wanted to ask on the OpEx guide, you have 63% to 64% gross margin. When I do the math, it looks like you're getting about 100 basis points of de-leverage on OpEx to get to the range. What are you spending it on after such a great year of expense control? Where are you kind of loosening the flow a little bit in 2026? Thanks.

Mr. Sylvain: Yeah, it's a fair question, Robert. Look, we had a really great year this year in terms of OpEx control. In fact, I think Q4, you look at the spend profile sequentially from Q3 to Q4, our spend is essentially flat. And so, you know, really great job done by the team there as you roll forward the math. I mean, if you kind of use it in round numbers, the goal isn't necessarily to deliver. I think you have to play within the ranges a bit to get there, but the goal isn't necessarily to deliver. The point is, is the leverage in the P&L next year predominantly will flow through gross margin, and the goal is to keep the off-Op margin or the Op expenses as a percent flat. Now, what's running through that P&L is the launch of our Ireland manufacturing facility.

So, we have a facility in Ireland that you guys are all aware of it. We're going to be hiring in staffing. Up will obviously be turning on depreciation. There'll be a lot of folks there in training. We'll be running, you know, validation, validation samples across those lines. We expense those that happen. So, there's a big investment in that in that manufacturing facility. We'll turn that on here likely in the fourth quarter of this year. At which point those costs will come out of OpEx and up into Cogs. But as we ramp up those expenses over the course of the year, you'll see those playing through. That's what really soaks it up.

So obviously that's a bit of a one-time thing when you're opening up a facility. Those will dissipate as we move, obviously to turn that facility on into 2027. So, underneath all of that, Robbie, I think it's important to note that because you are still getting leverage, it's just there's an investment we're making into a facility, though obviously, that that investment in leverage will obviously be in play through 2027 and beyond. So, we're still getting leverage there. We're still getting leverage, obviously in gross margin, the work continues. It's just this year; gross margin is going to do a little bit of the work. While there's some, I would say, temporal things running through OpEx.

Q (David Roman, Goldman Sachs): Thank you. Good afternoon, everybody. I want to just maybe dig a little bit more into the 2026 revenue and maybe specifically around the new patient dynamic. I think sometimes we get wrapped around the axle on this record of the new patient dynamic. That may or may not be significant as we look forward here but maybe give us some broader perspective on what is assumed from sort of underlying volume growth at different ends of the guidance range. What are some of the factors operationally that need to play out that would put you at the 13% level, and what would put you at the 11% level?

Mr. Sylvain: Yeah, thanks. It's a fair question. And at the end of the day, I know we do spend a lot of time talking about new patients. At the end of the day, what drives revenue is your patient base. And obviously a key component to that is how many new patients you add. But it's also what you do around retention utilization and then of course price. And so and so you know, as you think about the puts and takes into next year, you know, think about it this way. We start, we start, we exit a year. We actually are talking about patient base growing at about 20% to 20%. And so that's your starting point for what you'd expect in terms of starting point for volumes as you move into the year.

Over the course of the year, our expectation, is we have a couple points of price and that's been consistent, in that the remainder in the delta between, what I would say is any anticipations around unit volumes would be around mix. And the reason mix is still there. It's much smaller than it used to be. But we do still have a lot of new coverage coming on, specifically in the PBM space for, for type 2 non-insulin. And then outside the US, we are winning a lot of tenders in Dexcom ONE+. And it comes at a different price point. So that mix is still there. And it will come down from 2025. That makes an impact. So that puts your unit volume growth there. Just south of that 20% puts you in the, you know, the mid to upper teens. And that gives you kind of presumptions around unit volume.

You know from there in terms of if you're thinking about the inputs, we talked a little bit about this at JPMorgan. So, we're happy to reiterate it. We don't necessarily need record new patients to hit the low end of our guidance. And you'd want to hit a record new patient to certainly hit the top end of the range and beyond. And so that's the way we're going to run the business. Obviously, we had a record new patient year in 2025. We'll obviously focus on setting high targets internally and achieving those targets internally. But that gives you some of the inputs and puts and takes in the guidance. The other piece of the guidance, I think it's just important to note this assumes coverage stays predominantly the same.

And so obviously if things change around coverage that would change our new patient outlook. Certainly. And then we'd have to kind of give you guys an update as that moves to the year. Hopefully that gives you some puts and takes. You're right though, David. At the end of the day, these are all puts and takes around a user base and how that user base grows and moves over time. And that's why it's really important. We always acclimate everybody with what how did our user base grow year-over-year? And you guys have the most recent update based on our last touch point. So, they usually, puts and takes and any other questions be happy to follow up with.

Q (Richard Newitter, Truist): Thanks for taking the questions. Just a simple one for me. I just wonder if you can comment on revenue cadence at all, specifically the Q1 but anything else? Throughout the year, I think the street's said about a 6% sequential sequentially lower Q1 versus Q4, is that, you know, is that a reasonable place and way to think about it or anything else you'd call out? Thanks.

Mr. Leach: Yeah, it's a good, good question. A fair question. I think cadence wise for the full year, you know, our expectation is continuing to see a little less into Q4 and a little more into Q1. And just it's a slow evolution over time. But as more and more goes to the pharmacy and less and less goes through the DME commercial part of the business in terms of at least the total patients still. Still both good businesses. You don't have that stocking dynamic you typically see in houses in the fourth quarter where someone tries to maximize benefits. You still have that. You still have a decent sized business, but it's just less of a percentage of the business.

So, the expectation is obviously Q1 is a little bit higher than typically in Q4. I would say last year we talked about, you know, Q1 being, you know, a 7% to 8% decline, and we came in closer to seven in that range. I would say this year we've been talking about we talked about this at JPMorgan. On stage, we think it's a 6% to 7% decline. So, I think the street's a bit, little bit is within the range or probably at the higher end of that range, but not far out of it. It's a pretty it's a pretty safe place to be. So, 6% to 7% sequential is about what we would think. This is a little bit less seasonality this year than last year.

On sensor uptake and utilization rates

Q (Danielle Antallfy, UBS): I had a question on how you guys are thinking about utilization. Obviously, as basal ramps, I suspect utilization is coming down a bit. As we do get coverage for non-insulin, using [patients with] type 2, utilization will also look different there. I'm curious as you guys are sort of thinking about not only 2026, but beyond. Even qualitatively, how should we think about utilization based on what you know today?

Mr. Leach: Thanks, Danielle. You know, as we look at the spectrum of users with our, you know, the highest utilization we see in those aged users, type 1 on automated insulin delivery systems. You know, they're well north of 90% utilization, which makes sense because those aid systems don't operate without a sensor connected to them. And they are, the ease of use and the outcomes that they drive are so powerful that that's what we see there. Type 2 IIT and non-IIT, type 1. It's very similar. It's kind of in that 90% to 85% range. And those utilization rates have remained fairly consistent over time. And so, we're not seeing much change there.

So, your question is around basal and also the non-insulin users. For basal-only users, we've had a longer time frame with those users as coverage opened up a number of years ago. And so that that group has about an 85% to 80% utilization rate. That's actually what we saw in our studies, you know, and we've seen it play out in the real world, which is always great when you see the clinical trial actually reflect real world use. And so, 80% to 85% in that type 2 baseline. Some of the more recent learnings is from our registry where, you know, we always anticipated that type 2 non-insulin users might not have the same rate of utilization as those type 2 basal users just because of the difference in the insulin. They're not taking a dose of insulin. There's not the risk of hypoglycemia a number of those things. So, we've kind of assumed there might be slightly less utilization in that group. But in the registry, which is this new group of patients that have coverage for CGM that are type 2 non-insulin users. That registry is about 12 months old, and we are seeing high utilization rates in that group, very similar to those basal users. When you're in a reimbursed environment, I think that's a key. We see the best utilization when our patients have coverage. And so, we're seeing good utilization there and we'll continue to track it. But so far, those rates have remained pretty stable. And it's an important aspect as we think about our expansion globally. And as we continue to see more customers come on to the products. And it's important also because type 2 is our largest opportunity as we think about the long term. And so, we'll keep those in mind. But we're feeling good about what we're seeing. You know, as we look at user experience too, there's really an opportunity to drive further utilization as we get more engagement with the product. And so, as we make the software updates, we start adding more AI insights to the technology. The idea is can we drive utilization even higher?

So, I think that's the question to be to be out there, but I'd like to see it improve even further. I think the best way to take it, Danielle, is at least back to the models, is to think about it as the utilization. The trends have remained the same. In fact, there's work we're doing, obviously, to make them better. It's just really more about the mix. And as you guys are modeling by cohort, think about it that way versus utilization by cohort going down. Just make sure you have the mix right and that should help out.

Q (Jeff Johnson, Baird): Thank you. Good afternoon. Jereme or Jake, I think you pointed out in your prepared remarks about strengthening US sensor uptake trends in the fourth quarter and said that those continued into the first quarter. Maybe you could just flesh that out a little bit for us – what was some of the recovery from the sensor deployment issues kind of mid-year? Was that continued strength in maybe to AID uptake? Anything you can point to there and just talk about maybe Jereme; you also mentioned your installed base being an important driver of growth. Just how stable has that T1 and T2 user base been as Libre 3 is starting to launch in the US?

Mr. Sylvain: Yeah, thanks for the question. You know, I think as you look at what's called sell through trends and that's, that's our way of looking at who's ultimately, you know, going to the pharmacy or going to the DME picking up product. That becomes really important. You know, you can look at other things. There are various other data points we use, but we certainly use those as well, because that's people actually physically picking up and using the product. And we saw that improve over the course of the fourth quarter and continue.

Now there's a couple different reasons, out there and certainly, you know, part of it is going to be. Certainly, some work we've done around, you know, certainly sensor deployments. Jake alluded to it earlier. We've done some really nice work around that. We've seen our warranty rates coming down and certainly our complaint rates coming down moving into the year. That's exciting to see. It also helps to have launched our 15-day product. We only launched it in the DME in the fourth quarter. So that's not necessarily a large piece of it, but certainly we expect having that new product out there to be a really good opportunity.

And then, you know, naturally, as you would expect, as we get out in front of physicians one, two, three, four times and they can see the coverage landscape changing for those non-insulin users, you know, that certainly starts to play out a little bit as well. So, I think what you're seeing is a little bit of all that I mean all of these things are intertwined at the end of the day, you know, providing a 15-day product and all the features and the accuracy associated with is great. Having less sensor deployment challenges is great. And certainly, having our sales force out calling on folks, all those things really coming together.

So, we're seeing that play through in terms of stability of the user base, retention, utilization. You know, you’re kind of alluding more to the retention side. It's been stable. I mean, we haven't seen many changes at all over that time frame. Certainly, there was a lot of there was some noise over the course of the summer. But I think we've been very focused on making sure that we've got in front of those and that the experience that folks have when using the product is an excellent one. Jake alluded to it earlier. Spend a ton of time really focused on this, speaking to patients, speaking to physicians, speaking to advocacy groups over the course of time, and making sure we're listening. And to the extent that we do need to make changes, make those changes.

All in all, at the end of the day, I think what it proves is Dexcom has built an incredible product, built on amazing accuracy, and I think people are passionate about one, using the product and making sure they're getting all the benefit out of it. I think you're seeing that as we're getting out into the field. So, we've seen that stable, and I would expect to see that stable moving forward even with, you know, other even competitive product launches out there.

On international growth

Q (Matthew O’Brien, Piper Sandler): Good afternoon. Thanks for taking the questions. Jacob and Jereme, I would love to double click on that commentary saying that you're going to basically make up about a $2 billion delta between your US and your OUS business. I know it's going to take time, but can you talk about if you've got a big competitor out there, they've got a huge international business. How do you do that – how do you close that $2 billion delta? I'm assuming we're talking revenues and not just volume. How do you do that over what time frame – is it 15 years, is it five years? And then, Jereme, what kind of impact does it have? Do we have any pockets of weakness on the margin side as you're scaling that business and it's becoming a bigger portion of the overall revenue base? Thanks so much.

Mr. Sylvain: Thanks, Matt. You know, when I look at the international opportunity, there's two big pieces, right? There's the opportunity to continue to expand within the markets we're already present in. If you think about, we've established pretty strong businesses throughout Europe and we're just getting started in the Asia Pacific region. And so, when you think about just going deeper into patient populations, you know, coverage across the international markets, as I mentioned earlier, trails the US. So, there's really a lot of coverage to still unlock. When we think about the international patients. You know, type 2 basal is only starting to see coverage wins. We got a win in France. We've seen Japan move there. And you know we're looking towards Germany to start. We've got some coverage there for basal insulin users. But I mean there's still the opportunity for it around the globe. If you just look at the sheer volume of patients and the impact that we know that our technology can make. The opportunity is there. The key and the unlock is for us to generate the evidence, make sure there's awareness of the evidence, the advocacy from both the clinicians and the patients, and basically drive that through each of these markets.

We've been very successful. We've basically we've been the leader in driving evidence generation for the unlock for millions of lives. And so, we're going to keep doing that around the globe. It takes work. Every healthcare system is slightly different. It's actually a reflection of that is in the fact that we have a pretty substantial product portfolio outside the US to really meet the needs of both different segments of users, but also the different tiered structures of pricing that we see outside the United States.

And so, we're going to continue, as we mentioned, by adding another product to that portfolio, which will help us expand to access to customers we don't have today. And so, we're going to be very focused on driving access and also making sure we have a product portfolio that takes advantage of that access when it comes and we'll be ready. I think previously with our focus in the United States, we there, was more opportunity outside of the United States that we didn't take advantage of, as you mentioned, that our competitor did. But we're going to be ready this time is more access opens. We're going to be there to be the one for taking the share there.

In terms of time frame, it will take a little while. You know, it's not going to be in the next five years. And the reason is, is we have a lot of bullish expectations still here in the US. And so that's why I think it's really important. We'll talk about obviously we're going to be talking about it until we see the coverage with the CMS expansion obviously, and we won't stop there. We'll be looking to try to expand into prediabetes and beyond. And so, you know, the US has a long runway ahead of it. As you think about the international markets, though, you know, we're still not in tons of markets around the world.

And so, Jake alluded to the markets we're already in. There's an opportunity to go deeper. There's certainly an opportunity to work on taking share. And we'll do that. And you know, I think we've done a really nice job over the years. But boy, there's a lot of markets we're going to need to go into over the years. And we have plans to do that. And we'll talk a little bit more about it in May at our Investor Day. But a lot of opportunity that's not even in our P&L or in our revenue today that that we can see ahead of us. And so and so, yes, it's a longer-term vision. Absolutely.

But when you start to sit down and think about the countries we're not in today, and you think about, you know, how many folks around the world are impacted with diabetes and the coverage that's starting to kick up when we show up in countries, you can see the opportunity is immense and it's really on us to get out there. Make sure we get into those countries and we're in those countries. Take share. So, it's more than five years. It's fair point and we'll have a little bit more color as we get into May.

On 2025 financials

Q (Michael Polark, Wolfe Research): Good afternoon. I have a gross margin question. In 2025, I think there were 325 basis points of one timers called out, scrap freight and small receiver recall. If I look at the 2026 guide, the midpoint calls for 270 bps dips of expansion. So not even getting all of that one time or stuff back. And also, not considering credit for 15-day, which is starting. So, the question is why is this the right gross margin guide. And do you agree? Or where are we on the scrap and freight kind of overhangs? And if I could sneak in one related item just on hardware mix in the US, excluding yellow in 2025, what was the G6 versus G7 10-day and by the end of 2026? What will G6 next be versus G7 10-day G7 15-day?

Mr. Leach: So, I'll answer the first one. You know, the I think you have a little bit too much math in what I call the COGS associated with that. It's a little bit less than that. And so, what you should see is you think about the year if you were rolling it forward is you'll see, improvements across certainly a little bit, a little bit that'll spill here into Q1 just because you cap and roll certain variances and obviously freight and scrap stay in. But there's certain variances as you're getting up to speed. So, you just have to be mindful of that. It doesn't go away immediately overnight because you do roll those in. But it’s a little bit less than the number you have. But a little bit of roll into the year, you'll see the improvements play through. You'll also see the 15 day.

And so, you'll, you'll see those numbers. And likely what you'll do is you'll pop out of the top end of our guidance range. But this just remember in the fourth quarter we turn on Ireland. And so, all of those fixed costs, we talked earlier with Robbie about that way down the P&L in the first three quarters, in the top margin side or the OpEx side flipped to Cogs. And so, we had actually expected decline in our gross margin into the fourth quarter, as you have a full facility turning on all those costs, but the production levels will be much lower. And so, there's a lot of fixed overhead that you won't pick up and cap and roll that. So, I think that that at least helps to understand, you know, that's That at least helps to understand. That's why there's some geography. That might help there a little bit.

And obviously the converse of that, as you'd expect to see up expenses come down in the fourth quarter. It's all a moot point across the board when you look at top margin, because it's all geography. But hopefully that helps you at least as you're kind of penciling out the year, and then you're thinking about the sequencing over the course of the year, just a little bit too, about customer base and the products they're using. So, we've seen, you know, rapid obviously declines of G6 users as they've switched over to G7. And so, the vast majority of our base here in the US is on G7. And as we have launched the 15-day, actually in December, we started seeing quite a few upgrades from G6 to G7 15-day. And so, we anticipate that that will continue. And our intent is, towards the middle of this year is when she said she will really start phasing out. And so, we'll start building in more capacity for G7.

On Stelo

Q (Joanne Wuensch, Citi): Good evening and thank you for taking the question. Could you tease out what the Stelo contribution was to the 2025 results and what is embedded in your 2026 guidance, and any color you can give on how that's going? That would be wonderful. Thank you so much.

Mr. Leach: Sure. Yeah. So, we talked about $130 million of stellar revenue in 2025. So, you know, kind of at the top end of our 2% to 3%, number. So that's certainly we're happy to see that and a lot of great progress over the course of the year channel wise. And, you know, really excited about the new. And we shared a little bit of some of the pictures at JPMorgan on our presentation. So, you'll see it up on our website. We've got some new, new, uh, a new app coming for Stelo, here in the coming months. So, we're really excited about that. In terms of 2026. You know, we had talked about contributing about a point to growth in 2026. So, you guys can do the math on that. Obviously, those are big round numbers just given how big the organization is. But again, we still expect it to be a nice contributor to growth, albeit the base you'll actually have a base this year versus obviously in 2025, you didn't have a base to compare it to.

And Joanne, it's just when you think about how it's going with Stelo, you know, as Jereme mentioned, we're really excited about the new innovation that we're bringing. We have a whole new redesigned app. We're launching a new smart, basically enhancing the smart food logging that we already had that now will capture macronutrients and things. But what we're seeing is, you know, a whole spectrum of different types of users. Start using Stelo, and particularly one of the groups that we've got our eye on is, is type 2 non-insulin users. These are the folks that that don't have coverage for CGM. And so, they're using this little product over the counter. But over time what we're seeing is there's a real opportunity for those folks for us to transition them from Stelo over to G7 as coverage emerges. And so Stelo becomes a very important part of our portfolio, not just for, you know, pre-diabetes and health and wellness, but also to get type 2 access to the technology early and then transition them to a covered product as coverage continues to unlock.

Close Concerns’ Questions

- What international markets does Dexcom expect to strengthen or expand coverage for T2D on basal-only insulin in 2026 or beyond and match the growth strength in France?

- What features will the new CGM in Dexcom’s ONE+ category offer?

- When does Dexcom anticipate a national rollout of Smart Basal? How will Dexcom decide on “select US cities”?

- How has Dexcom seen the mix of Stelo users (wellness vs. T2D not on insulin) evolve as coverage of anyone with T2D expand in the US?

- What international markets is Dexcom prioritizing for future launch of Stelo?

-- by Jeremy Alkire, Riya Chatterjee, Katherine Moon, and Kelly Close