JPM 2026 Day #1 Highlights –

Executive Highlights

- The 44th Annual JP Morgan (JPM) Healthcare Conference began today at the Westin St. Francis Hotel in San Francisco! This year, the meeting convened 525 companies and over 9,000 attendees across the healthcare industry, from large pharmaceutical and device companies to early clinical-stage biotech firms and non-profit organizations. We appreciate JPM for organizing dynamic conversations on innovation, market changes, and health policy. Take a look at upcoming sessions in our Preview.

- In tech, we heard updates across CGM, AID, and digital health.

- Dexcom: Dexcom announced a total preliminary, unaudited full-year 2025 revenue of $4.66 billion, up 16% from 2024. The company also reported preliminary, unaudited 4Q25 revenue of at least $1.26 billion, up 13% from 4Q24 and 4% sequentially. Mr. Leach announced that Dexcom’s global CGM userbase now exceeds 3.5 million people, up over 20% from 2.8-2.9 million users at the end of 2024. Mr. Leach highlighted significant US coverage expansion in 2025 for all people with diabetes, and he emphasized international expansion as one of Dexcom’s top growth priorities.

- Medtronic: Medtronic CEO Mr. Geoff Martha expressed enthusiasm about the growth trajectory across several of the company’s franchises. Commentary on the diabetes business was limited, as the unit remains on track to separate via IPO by the end of calendar year 2026. While unmentioned in prepared remarks, Medtronic also announced today the FDA clearance of MiniMed Go app, which integrates Medtronic’s InPen with the Abbott-partnered Instinct CGM; interoperability with Simplera and the MiniMed Go app is currently under review by the FDA.

- In therapy, we listened to several updates from companies dedicated to treatments for diabetes, obesity, and complications.

- Amgen: Amgen CEO Mr. Robert Bradway discussed GIP antagonist/GLP-1 RA MariTide was in detail, underscoring its potential as a differentiated long‑acting therapy for both obesity and T2D. Amgen expects to establish the use of MariTide as a long-term maintenance therapy and as potentially the first monthly therapy for T2D. The company is preparing a phase 3 program to evaluate MariTide in T2D. PCSK-9 inhibitor Repatha is one of six major growth drivers for Amgen, and olpasiran, a first-in-class siRNA molecule targeting Lp(a), was also highlighted for its innovative promise in general medicine.

- Madrigal: Madrigal CEO Mr. Bill Sibold said that Madrigal has three areas of growth for the future: (i) delivering on the best-in-industry drug launch of Rezdiffra; (ii) progressing towards an indication for stage F4 fibrosis (cirrhosis, F4c); and (iii) extending leadership through pipeline expansion. The company will focus on combination therapy with Rezdiffra and the phase 2 oral DGAT-2 inhibitor ervogastat (which the company licensed from Pfizer just last Friday), combination therapy with SYH2086 (a small molecule oral GLP-1 RA licensed from CSPC Pharmaceutical Group in July 2025), and the F4c indication in 2026.

- Pfizer: Chairman and CEO Dr. Albert Bourla discussed the company’s visions, key milestones, and growth strategies across metabolic health, immunology, cancer, and more. Dr. Bourla placed a significant focus on Pfizer’s “controversial acquisition” of Metsera and shared that Pfizer views the US government’s Most Favored Nation negotiations as manageable and positive, albeit a bold move.

- Regeneron: CSO Dr. George Yancopoulos highlighted obesity and cardiometabolic disease as major areas of expansion, focusing on the limitations of current GLP‑1 RA therapies and the opportunity to address obesity alongside hyperlipidemia. Regeneron plans to combine its GLP‑1/GIP agonist, olatorepatide, with Praluent (PCSK9 inhibitor), aiming for >50% LDL‑C lowering in addition to weight loss. Phase 3 results for olatorepatide in obesity in China are expected in 1H26.

- Roche: CEO of Roche Pharmaceuticals Ms. Teresa Graham explained that Roche is focusing on six key areas in the management of obesity designed to address continual gaps in the therapeutic landscape: tolerability, suboptimal responses in up to 20% of patients, lean muscle loss, a ceiling effect on weight loss, weight maintenance challenges, and comorbidities. She named petrelintide, CT-388 (a dual GLP-1/GIP RA), CT-996 (a small molecule GLP-1 RA), pegozafermin, and emugrobart (a monoclonal antibody targeting myostatin) as key therapies in development for obesity.

- At a lunch symposium, JPMorgan CEO Mr. Jamie Dimon was part of a compelling fireside chat that touched on a variety of topics, including his perspective on global affairs and the role of corporations and healthcare organizations in this ecosystem. Mr. Dimon said that the US should continue to demonstrate strong military leadership in global affairs yet should not overuse the military, and on young voters questioning capitalism and the free market, Mr. Dimon said that corporations must think of national interests with their actions.

Table of Contents

- Open and Welcome

-

Diabetes Therapy Highlights

- 2. Roche: Targeting a “top three” role in obesity through petrelintide, pegozafermin, and more; anti-VEGF Vabysmo returns to growth after market challenges

- 3. Pfizer: Dr. Albert Bourla shares vision of obesity treatment landscape with Metsera’s assets and reflects on MFN and tariffs

- 4. Amgen: PCSK-9 inhibitor Repatha highlighted as key to Amgen’s growth through 2030; extensive discussion of long-acting T2D and obesity candidate MariTide

- 5. Merck: “Democratizing” PCSK9 therapy and combinations with Lp(a); MK 3000 as a potential new mechanism of action for diabetic macular edema

- 6. Sanofi: Strategies and progress across mid- to late-stage development projects; teplizumab receives approval in the EU for stage 2 T1D

- 7. Regeneron: CEO Dr. Leonard Schleifer and CSO Dr. George Yancopoulos emphasize internal R&D engine, Eylea HD momentum, and obesity strategy

- 8. Viking: Dr. Brian Lian highlights oral and injectable VK2735 (dual GLP-1/GIP RA) and amylin agonist for obesity

- 9. J&J: CEO Mr. Joaquin Duato outlines diversified growth strategy with momentum in cardiovascular portfolio

- 10. Madrigal: “10% of 10%” of global MASH patients treated; detailed approaches to combination therapy including GLP-1 RAs and DGAT-2 inhibitors

- 11. Arrowhead Pharmaceuticals: RNA interference treatments for obesity to advance to phase 2b trial

- 12. Corcept Therapeutics: Dr. Joseph Belanoff highlights broad implications of cortisol modulation, including hypercortisolism, obesity, and diabetes

- 13. Novartis: De-risked pipeline driving post-Entresto growth; Leqvio as the foundational therapy for the company’s cardiorenal metabolic franchise

- 14. Vertex: Journavx (suzetrigine) shows strong growth in the pain sector with potential indication for diabetic peripheral neuropathy

- Diabetes Technology Highlights

- Diabetes Big Picture Highlights

Open and Welcome

1. JPM’s Jeremy Meilman welcomes over 9,000 attendees, reflecting on four decades of global health industry

In a crowded Grand Ballroom, Mr. Jeremy Meilman (Global Co-Head of Healthcare Investment Banking, JP Morgan) delivered welcoming remarks. He began by reflecting on the long history of holding JPM Healthcare Conference in San Francisco and how much the health industry has expanded over those decades. In 1983, when JPM first convened at the same Westin St. Francis hotel, only 21 companies, with an aggregated market cap of $4 billion, participated with fewer than 100 attendees. This year, JPM brought together 525 companies, whose collective market cap sums to over $9.9 trillion, for over 9,000 registered attendees. The US market has changed significantly over the years, as well. The Center of Medicare and Medicaid Services’ (CMS) annual spending in the same time period increased from $355 billion to $5.9 trillion, while federal funds rate decreased from 9.9% to 3.6%.

- Mr. Meilman said that strong momentum of growth is carrying through 2026. Since COVID-19, healthcare industry sector has demonstrated robust performance, with the biotech sector becoming the strongest performing sector for the first time in 2025. 2H25 also marked a period with significant increases in M&A (+44% from 2024), with the number of $5 billion+ deals increasing from four in 2024 to 16 in 2025 – which includes Novo Nordisk’s $5.2 billion acquisition of Akero Therapeutics and Pfizer’s $10 billion acquisition of Metsera. This momentum is continuing this year, Mr. Meilman said, as the past week was the busiest first week of January in decades for equity issuance.

- On the key trends for healthcare sectors in 2026, Mr. Meilman highlighted the uncertainty of policy changes like tariffs and Most Favored Nation deals, the increasing role of AI, and robust M&A activity.

- Pharmaceuticals & Biotech sector faces significant uncertainty with regard to tariffs and Most Favored Nation policy, contributing to a slower start to the year. Partnership and M&A activities was robust in 2025, with total value for M&A being $101 billion, up over 3x from $33 billion in 2024. On the other hand, Initial Public Offering (IPO) volume decreased by half from 2024 to 2025, indicating higher standards expected for early-stage companies. He expects 2026 to be a stronger year for IPOs with high-quality biotech companies.

- Healthcare Services sector is focused on integrating AI technology and increasing security. Mr. Meilman predicts 2026 to be active with M&A.

- The MedTech sector has efficiently dealt with tariff challenges in 2025 and continues to mitigate the impact of geopolitics with China and supply chain. M&A activities, portfolio management and restructuring will remain robust.

- The Life Science Tools, Diagnostics, and Pharma Services sector is navigating changes with academic and government funding. The bioprocessing industry is rebounding.

Diabetes Therapy Highlights

2. Roche: Targeting a “top three” role in obesity through petrelintide, pegozafermin, and more; anti-VEGF Vabysmo returns to growth after market challenges

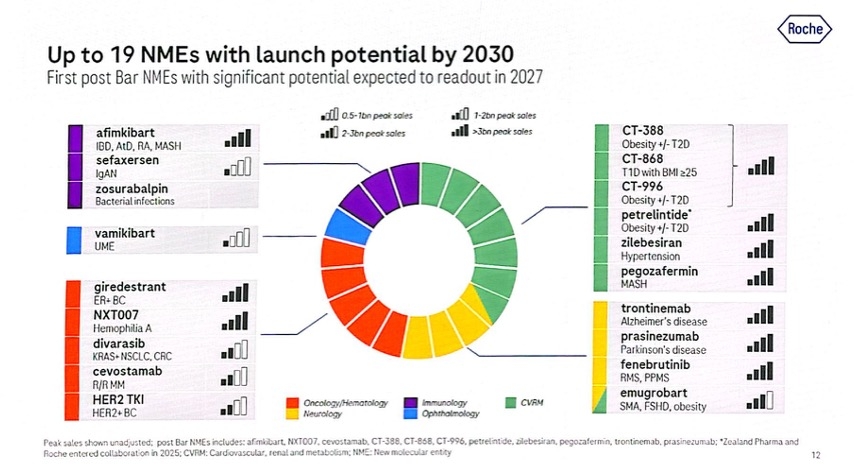

Roche Pharmaceuticals CEO Ms. Teresa Graham characterized Roche’s approach to cardiometabolic care as “delivering the next innovation cycle,” highlighting the company’s obesity portfolio in particular. Ms. Graham said that Roche is entering a new era of innovation in 2026, with early stages of the era taking root in 2025. Key priorities for 2026 include maximizing the current on-market portfolio, which is positioned to deliver growth through 2028, and delivering key launches including vamikibart, an anti-inflammatory antibody for retinal diseases. Roche also plans to prepare for its entry into the Alzheimer’s and obesity markets. Ms. Graham said that 60% of Roche’s R&D pipeline and total pharmaceutical sales involve a partnership, noting its partnership with Zealand on amylin agonist petrelintide and its recent acquisition of 89bio in particular. Roche is on track to achieve full year 2025 guidance, she said. In 2025, the company reported positive phase 3 results for 12 therapies, as well as 10 new molecular entities (NMEs) including pegozafermin, an FGF21 analog. There were no mentions of its diagnostic division, including BGMs and CGMs.

- Ms. Graham reiterated Roche’s commitment to being a top three player in obesity. Data on five NMEs that will enable phase 3 trials for the therapies are expected to be presented in 2026. Roche is focusing on six key areas in the management of obesity designed to address continual gaps in the therapeutic landscape: tolerability, suboptimal responses in up to 20% of patients, lean muscle loss, a ceiling effect on weight loss, weight maintenance challenges, and comorbidities. She named petrelintide, CT-388 (a dual GLP-1/GIP RA), CT-996 (a small molecule GLP-1 RA), pegozafermin, and emugrobart (a monoclonal antibody targeting myostatin) as key therapies in development for obesity. Ms. Graham said that Roche hopes to provide options for patients who prioritize different benefits of GLP-1 RAs, from those seeking moderate weight loss to high weight loss with good tolerability, as well as providing options for combination therapies.

- Roche has up to 19 NMEs with the potential for launch by 2030, including seven candidates in cardiovascular, renal & metabolic disease (CVRM). Ms. Graham said that these candidates provide the greatest potential and greatest level excitement for the company’s future. Roche is developing CT-388 for obesity with or without T2D, CT-868 for T1D with a BMI of 25 kg/m² or greater, petrelintide for obesity with or without T2D, zilbesiran for hypertension, pegozafermin for MASH, and emugrobart for obesity, spinal muscular atrophy, and facioscapulohumeral muscular dystrophy (see figure below). During Q&A, Ms. Graham again said that petrelintide, CT-388, and CT-996 are Roche’s most exciting candidates.

- In ocular health, discussion focused on Vabysmo (faricimab-svoa), the company’s franchise-leading anti-VEGF injection for wet AMD, DME, and RVO. Ms. Graham said that the therapy has had continued strong global growth following challenges in 2025. Recall that in 3Q25, the company revised its global full-year growth guidance for Vabysmo to 15% from 20%, reflecting the approximately 15% contraction of the US branded intravitreal therapy market seen so far in 2025. Roche said that reduced availability of co-pay foundation support has been the primary driver of this decline. Today, Ms. Graham said that the market has leveled and that Vabysmo will now return to accelerating growth.

3. Pfizer: Dr. Albert Bourla shares vision of obesity treatment landscape with Metsera’s assets and reflects on MFN and tariffs

In this standing room-only symposium, Pfizer Chairman and CEO Dr. Albert Bourla discussed the company’s visions, key milestones, and growth strategies across metabolic health, immunology, cancer, and more. Dr. Bourla began by reflecting on 2024 and 2025, when Pfizer cut operating expenses by $5.6 billion. Noting that the company beat earnings for consecutive quarters, he emphasized Pfizer’s strong performance and business execution. He also highlighted several uncertainties that the company faced in 2025: (i) tariffs, which Pfizer has mitigated effectively via the Most Favored Nation deal; (ii) normalization after significant drop in COVID-19-related revenue; and (iii) acquisition of Metsera to strengthen its obesity pipeline. Entering 2026, Pfizer aims prioritize maximizing the value of recent acquisitions (including Metsera), delivering critical R&D milestones, investing for post-2028 growth, and implementing AI across R&D, manufacturing, and operations. Key catalysts for 2026 include delivering data readouts for phase 2b VESPER trial of ultra-long-acting GLP-1 RA (MET-097i, now named PF’3944) and phase 1/2 trial of the combination of PF’3944 and amylin agonist (MET-233i, now named PF’3945). Impressively, it will also launch ten phase 3 pivotal studies for PF’3944.

- Dr. Bourla placed a significant focus on Pfizer’s “controversial acquisition” of Metsera. As a reminder, in September 2025, Pfizer agreed to acquire Metsera for up to $7.3 billion. However, bidding war set off when Novo Nordisk submitting an unsolicited ~$9 billion acquisition offer on October 30. After several days of public discourse and legal action, Pfizer ultimately acquired Metsera with an amended $10 billion offer. Metsera’s pipeline included: (i) once-monthly GLP-1 RA MET-097i; (ii) once-monthly amylin analog MET-233i; and (iii) oral GLP-1 RAs MET-097o and MET-224o, among other candidates.

- Within five weeks of closing of acquisition, Pfizer and Metsera have efficiently integrated and is advancing the candidates. In fact, Pfizer had launched the first phase 3 trial in December 2025, earlier than when Metsera had originally planned in 2026. Dr. Bourla shared that additional data has further increased Pfizer’s confidence in the candidates. Specifically, he believes that once-monthly candidates have the best-in-class potential with favorable tolerability profile. He also expressed excitement about the benefits of combination therapies, such as amylin agonist with GLP-1 RAs or Metsera’s candidates with an oral small molecule GLP-1 RA licensed from China-based YaoPharma in December 2025.

- Looking forward, Pfizer will launch ten phase 3 obesity trials this year and target commercial launch in 2028 – preferably, management said, in early 2028.

- On the broader obesity market, Dr. Bourla commented that the market size is underestimated, as cash-pay channel constitutes ~30% of the market. He further added that obesity market has similar growth potential to that of Viagra years ago.

- When asked about Most Favored Nation (MFN) pricing deal, Dr. Bourla shared that Pfizer views the negotiations as manageable and positive, albeit a bold move. He further explained that MFN deal only affects eight high-income countries outside the US, while the other hundred countries remain unaffected. One of the countries, the UK, has already signed the deal with the US government to significantly increase its spending on innovative medicines, suggesting that countries are adjusting to the policy changes. Pfizer is now in dialogue with other countries like France and Germany. Dr. Bourla noted that these countries acknowledge that they are behind with innovative medicine compared to China and the US and that, with the new system, “products won’t be launched” unless they are paid for.

4. Amgen: PCSK-9 inhibitor Repatha highlighted as key to Amgen’s growth through 2030; extensive discussion of long-acting T2D and obesity candidate MariTide

Amgen CEO Mr. Robert Bradway discussed Amgen’s approach to general medicine in great detail, including MariTide, Repatha (evolocumab), and olpasiran, which are major cardiovascular therapies for the company. Mr. Bradway first highlighted Amgen’s “broad and deep” portfolio across four therapeutic areas: general medicine, rare disease, oncology, and inflammation. He emphasized consistent execution across financial performance, regulatory progress, and late‑stage pipeline advancement. The company had five successful FDA approvals in 2025, with 10% year-over-year revenue growth and 14 products annualizing at $15 billion. In general medicine, Amgen is focusing on heart attacks, stroke, hypercholesterolemia, osteoporosis, chronic weight management, T2D, and obesity-related conditions. Repatha, a PCSK-9 inhibitor that lowers LDL cholesterol levels to prevent strokes and heart attacks, received high attention throughout the presentation, as did GIP antagonist/GLP-1 RA MariTide and Lp(a)-lowering olpasiran. Looking ahead, Amgen is developing a number of key therapies and is further integrating new technology and AI into its research and commercialization processes. Mr. Bradway also discussed the recent acquisition of Dark Blue Therapeutics and Disco Pharmaceuticals as opportunities for further growth.

- GIP antagonist/GLP-1 RA MariTide was discussed in detail, underscoring its potential as a differentiated long‑acting therapy for both obesity and T2D. Looking back at 2025, Mr. Bradway highlighted the six global phase 3 studies of MariTide that Amgen initiated in 2025. The company sees opportunity for MariTide in chronic weight management, atherosclerotic cardiovascular disease, heart failure, obstructive sleep apnea, and T2D. Phase 2 data showed robust reductions in A1c and weight with monthly dosing, alongside favorable cardiometabolic improvements and a tolerability profile consistent with the GLP‑1 class. In chronic weight management, the majority of participants who achieved ≥15% weight loss maintained the loss for a second year on lower monthly or quarterly dosing, with very low rates of nausea and vomiting. He said that the therapy has garnered high interest with its differentiated approach to obesity and related conditions. He highlighted MariTide’s strong treatment efficacy with monthly or even quarterly dosing in development, and that tolerability at initiation improves with multi-step dose escalation. Mr. Bradway also said that the therapy is very well tolerated at target doses and at maintenance doses. Amgen expects to establish the use of MariTide as a long-term maintenance therapy and as potentially the first monthly therapy for T2D. The company is preparing a phase 3 program to evaluate MariTide in T2D.

- The six phase 3 studies are:

- MARITIME-1, which has completed enrollment in adults living with obesity or overweight but without T2D;

- MARITIME-2, which has completed enrollment in adults with obesity or overweight with T2D;

- MARITIME-CV, which is enrolling adults living with established ASCVD and obesity or overweight;

- MARITIME-HF, which is enrolling adults living with heart failure with preserved or mildly reduced ejection fraction and obesity; and

- MARITIME-OSA-1 and MARITIME-OSA-2, which were both initiated in 3Q25 in adults living with obstructive sleep apnea.

- Recall that full results of the 52-week phase 2 trial of once-monthly MariTide in obesity with and without T2D were presented at ADA 2025. Major takeaways included the high GI adverse event rates despite robust weight and A1c reductions. In the treatment efficacy estimand, MariTide conferred up to 20% weight loss vs. 2.6% with placebo at 52 weeks. For the treatment policy estimand, MariTide conferred up to 16% weight loss compared to 2.5% with placebo.

- GI adverse events. Rates of nausea and vomiting were very high across the MariTide arms. In the non-dose escalation arms, nausea was reported by 77-87% of participants, and vomiting was reported by 68-92% of participants. Dose escalation appeared to lower the rates of adverse events; however, nausea, vomiting, and constipation rates still remained high. During today’s presentation, Mr. Bradway characterized the safety and tolerability profile as consistent with the GLP-1 RA class overall and focused on the therapeutic promise of a once-monthly or once-quarterly drug. He said that real-world experience with incretins has always demonstrated challenges such as high discontinuation rates, high treatment burden, and high required dosing frequency. Amgen believes that MariTide is suited to this challenge and that quarterly dosing can still maintain weight loss. In the second year of MariTide treatment, the therapy was very well tolerated including at quarterly doses, with a very low incidence of nausea and vomiting and no new safety signals observed.

- The six phase 3 studies are:

- PCSK-9 inhibitor Repatha is one of six major growth drivers for Amgen, expected to be a key driver of product sales in 2026 and through the end of the decade. Mr. Bradway highlighted the therapy’s strong commercial performance, up 33% from 4Q24 and annualized at approximately $3 billion, and pointed to the October 2025 VESALIUS‑CV results showing a 36% reduction in first heart attack among patients without prior cardiovascular events and 25% reduction in 3-point MACE. Mr. Bradway emphasized that more than 100 million people worldwide are not at LDL‑C targets, and penetration is still in the single digits. Amgen sees a substantial runway for expansion. He highlighted the strong clinical evidence supporting the use of the therapy and its ability to reduce in risk of first myocardial infarction in people who have never had one. During Q&A, Mr. Bradway said that Repatha was the first therapy with such demonstrable preventative effects and that it provides a new therapeutic option for patients who otherwise have optimized care, including with statins. He said that Amgen hopes to “change heart disease’s status as one of the world’s leading killers.”

- In November 2025, full results of the phase 3 VESALIUS-CV study (n=12,257) were presented at AHA, which evaluated the effects of PCSK-9 inhibitor Repatha (evolocumab) in people with high CV risk without prior atherosclerotic CVD (myocardial infarction [MI] or stroke) – including people with diabetes and/or atherosclerosis. Impressively, evolocumab conferred 20% risk reduction in all cause death, 25% risk reduction in MACE-3, and 19% risk reduction in MACE-4 at five years.

- Olpasiran, first-in-class siRNA molecule targeting Lp(a), was also highlighted for its innovative promise in general medicine. Mr. Bradway highlighted olpasiran as one of Amgen’s most important late‑stage cardiometabolic programs, emphasizing its potential to address what he described as the “residual risk” in cardiovascular disease. He noted that one in five people carries genetically elevated Lp(a), a risk factor that cannot be modified by diet or exercise, and reiterated that phase 2 data showed 95–100% reductions in Lp(a). Amgen expects the phase 3 Ocean(a)-Outcomes trial (n= 7,297) to clarify whether lowering Lp(a) can meaningfully reduce cardiac events, and Mr. Bradway stressed that if the trial confirms this, olpasiran could represent a major advance for patients at high cardiovascular risk. Mr. Bradway noted that results are expected sometime in 2027.

- On biosimilars, Mr. Bradway highlighted that through 3Q25, biosimilars grew 42% from 4Q24, and the portfolio has now generated ~$13 billion in cumulative revenue. He framed the business as a demonstration of Amgen’s ability to “reliably and safely supply” complex biologics at scale, with the slides noting that the second wave of launches (including Eylea biosimilar Pavblu) is driving current growth while a third wave advances through phase 3 development.

5. Merck: “Democratizing” PCSK9 therapy and combinations with Lp(a); MK 3000 as a potential new mechanism of action for diabetic macular edema

Merck Chairman and CEO Mr. Robert Davis highlighted a new wave of late-stage assets on Monday afternoon, which extend the company’s reach beyond its historic core of oncology medicines. Enlicitide (oral PCSK9 inhibitor), MK 3000 (tetravalent, tri-specific Wnt antibodies), and the oral Lp(a) small molecule underscore Merck’s expansion into cardiometabolic disease. For a company that developed its Januvia franchise for presumably $1 - $2 billion, that has yielded well over $50 billion in revenue, we are very intrigued by the way that the company discussed Enlicitide – very efficacious, very safe, and very easy to take (our way of describing “tolerable”).

- Overall pipeline and financial portfolio framing. Merck projects over $70 billion in commercial opportunity by mid-2030, representing a $20 billion increase from 2025. Ten key programs, which notably include Enlicitide, account for around 70% of the $70 billion in sales. Nearly all have first-in-class potential with multi-billion peak sales. Four of those ten have already launched or have positive phase 3 data, while the remainder are expected to have major phase 3 readouts in the next 12-18 months. Positively, Mr. Davis shared that half of the $70 billion is expected to be clinically de-risked via phase 3 readouts by the end of 2026, with near-complete de-risking expected by the end of 2027.

- Enlicitide. Mr. Davis characterized Enlicitide as a therapy that was designed to be a potent LDL-lowering pill, with effects that “looked like the antibodies” – functioning as a “biologic in a pill.” In 2025, Enlicitide had three clinical readouts: (i) CORALreef Lipids (n=2,912); (ii) CORALreef HeFH (n=303); and (iii) CORALreef AddOn (n=301). Results demonstrated ~97% adherence and adverse event rates similar to placebo, supporting a broad use profile. Notably, it sounded like Merck hopes to “democratize” PCSK9 with Enlicitide by offering an affordable pill which can be widely accessed in the US and globally – as compared to a more niche, injectable therapy. We were extremely moved by Mr. Davis’ discussion of how good cholesterol scores could look and be. We will be extremely interested in watching how guidelines are discussed in the month and years ahead, particularly given some of the results at AHA.

- MK 3000. Mr. Davis highlighted MK 3000 as a potential new mechanism of action for the treatment of diabetic macular edema (DME). Phase 3 readouts of the BRUNELLO (n=984) and BAROLO (n=1,054) trials are targeted for September 2026. Mr. Davis emphasized that timing is “well ahead” of what was initially expected.

- Lp(a) oral small molecule. Merck acquired the Lp(a) small molecule candidate through a transaction with Longray and hopes to develop it as a combination therapy with Enlicitide – thereby combining a PCKS9-mediated LDL lowering with Lp(a) reduction in patients with a high cardiovascular risk. This combination, notably, was presented as part of a broader cardiometabolic plan which also includes Enlicitide-statin combinations, reflecting a company philosophy of being “first or best” and then planning “what’s next.”

6. Sanofi: Strategies and progress across mid- to late-stage development projects; teplizumab receives approval in the EU for stage 2 T1D

CEO Mr. Paul Hudson, EVP of R&D Dr. Houman Ashrafian, and CFO Mr. François-Xavier Roger discussed Sanofi’s strategic progress throughout 2025, including key mid- and late-stage development projects – see webcast and presentation slides here. With active portfolio management, capital allocation, and the launch of new treatments, Mr. Hudson said 2025 was “an extremely busy” year. Sanofi has generated 8.7% growth in sales through 3Q25, and the company expects double-digit growth continuing into the next decade. Looking forward to the new year, management emphasized confidence in continued profitable growth, with several updates on mid- and late-stage developments across immunology, rare diseases, oncology, neurology, and vaccines.

- New indications and breakthrough therapies. While management mentioned several treatments the company focuses on, they didn’t highlight teplizumab during today’s meeting. Nevertheless, teplizumab continues to make strides in the field, with today’s announcement that the treatment has been approved in the EU to delay the onset of stage 3 T1D in adult and pediatric patients eight years and older with stage 2 T1D. This announcement follows the positive opinion granted by the European Medicines Agency’s Committee for Medicinal Products for Human Use in November 2025 under the brand name Teizeild – of note, teplizumab received FDA approval in the US in November 2022 under the brand name Tzield. The press release states that Sanofi has decided not to progress with a second application of teplizumab in recently diagnosed stage 3 T1D in the EU at the moment, with next steps under evaluation. Beyond the US and EU, teplizumab is approved in the UK, China, Canada, Israel, the Kingdom of Saudi Arabia, the United Arab Emirates, and Kuwait.

- Sanofi’s response to tariffs and the administration’s new policies. Mr. Hudson commented on Sanofi’s agreement with the US government, announced in December 2025, to increase the accessibility of treatments by ensuring state Medicaid programs can distribute Sanofi’s treatments at the same prices available to other high-income countries. This decision reduces treatment prices by an average of 61% for select therapies for diabetes, CVD, neurological conditions, and cancer. Sanofi also agreed to offer products through TrumpRx and other direct-to-patient platforms at an average cost reduction of nearly 70%. With this agreement, Sanofi has secured a three-year tariff-free period on products it imports. Mr. Hudson said these decisions will help Sanofi make a further impact in the field and reach greater patient populations – he stated that the 2026 guidance will reflect these outlooks.

- Additionally, regarding policy changes, management responded to a question about the major changes issued this month regarding the government’s recommendation for vaccinating children. Mr. Hudson explained that more than 50,000 newborns get admitted to the ICU every year, and encouragingly, Sanofi’s vaccines have helped dramatically decrease the numbers by 80-90%. He said it’s clear that the administration has “sensitivity around vaccination policies” and wants to give parents a choice. Yet, Mr. Hudson said there’s a “delicate line” because not everyone is informed about the importance of vaccination, or the consequences of not receiving it, creating significant variability. Therefore, he encouraged the audience that Sanofi will continue “staying objective,” presenting evidence to demonstrate efficacy.

7. Regeneron: CEO Dr. Leonard Schleifer and CSO Dr. George Yancopoulos emphasize internal R&D engine, Eylea HD momentum, and obesity strategy

Regeneron CEO Dr. Leonard Schleifer and CSO Dr. George Yancopoulos described the company’s internally driven innovation model, underscoring the company’s commitment to “following the science” and investing in platforms that deliver long-term value to shareholders (see webcast and presentation slides). The session centered on two areas with significant relevance to diabetes and obesity: cardiometabolic disease and retinal health. Dr. Schleifer and Dr. Yancopoulos gave updates on the company’s GLP‑1/GIP and PCSK9 combination strategy and the accelerating uptake of Eylea HD.

- Dr. Yancopoulos highlighted obesity and cardiometabolic disease as major areas of expansion, focusing on the limitations of current GLP‑1 RA therapies and the opportunity to address obesity alongside hyperlipidemia. He emphasized that approved GLP‑1 RAs lower LDL cholesterol by less than 10%, leaving a substantial unmet need for people with obesity who also have elevated cardiovascular risk. To address this, Regeneron plans to combine its GLP‑1/GIP agonist, olatorepatide, with Praluent (PCSK9 inhibitor), aiming for >50% LDL‑C lowering in addition to weight loss. In China, phase 3 results for olatorepatide in obesity are expected in 1H26, with a global clinical development plan also beginning this year. Presentation slides also emphasized the company’s focus on enhancing the quality of weight loss with GLP-1 RAs, focusing on muscle preservation. The ongoing phase 2 COURAGE trial (n=1,005) showed that trevogrumab (anti‑GDF8/anti‑myostatin), with or without garetosmab (anti‑activin A), significantly preserves 50-80% of lean mass lost with semaglutide alone.

- In ophthalmology, Eylea HD (aflibercept 8 mg) was a major focus. In 4Q25, US net sales reached $506 million, up 66% from 4Q24 and up 18% sequentially. Dr. Schleifer attributed this momentum to a November 2025 label expansion, which added monthly dosing and an indication for macular edema following retinal vein occlusion. Prefilled syringe resubmission is under FDA review, with a decision expected in 2Q26. Dr. Schleifer reiterated the company’s goal of establishing Eylea HD as the preferred anti‑VEGF option across retinal diseases, including diabetic macular edema and diabetic retinopathy.

- During Q&A, Dr. Schleifer emphasized that these three enhancements (monthly dosing, the RVO indication, and the upcoming prefilled syringe) collectively support the rapid shift toward Eylea HD, which has grown from ~30% to ~50% of franchise sales over the past year. They also noted that payer coverage of monthly dosing removes a key barrier to initiating patients on Eylea HD, which they expect will further accelerate adoption.

8. Viking: Dr. Brian Lian highlights oral and injectable VK2735 (dual GLP-1/GIP RA) and amylin agonist for obesity

In an afternoon session, CEO Dr. Brian Lian highlighted multiple clinical programs in development for obesity and other metabolic disease. Viking’s pipeline includes several promising candidates, including injectable and oral VK2375, which are progressing with impressive data.

- Injectable VK2375 (dual GLP-1/GLP RA) for obesity. Dr. Lian described VK2735 as a dual GLP-1/GIP agonist with a pharmacokinetics profile that enables potent, durable weight loss and supports the potential for weekly and monthly dosing. In the phase 2 VENTURE trial (n=4,650) – published today in Obesity – VK2735 conferred up to 14.7% weight loss at 13 weeks with ~90% of treatment effect maintained four weeks after stopping treatment. GI adverse events (AEs) were mostly mild/moderate and concentrated at first exposure and at titration steps. This AE profile inspired Viking’s “start low, go slow” titration mantra that Dr. Lian repeated throughout the session. Two phase 3 VANQUISH trials for stepwise titration up to 17.5 mg and 52-week maintenance are in progress: (i) VANQUISH-1 (n=4,500) for obesity is fully enrolled; and (ii) VANQUISH-2 for obesity and T2D is on track for primary readout in 2027.

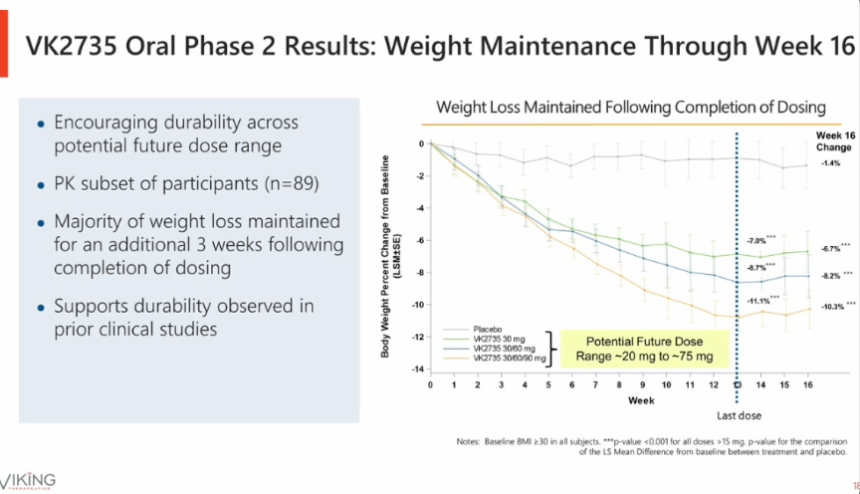

- Oral VK2735 (dual GLP-1/GLP RA) for obesity. In phase 1 (n=92), oral VK2735 (the same GLP-1/GIP molecule as the injectable formula) conferred up to 8.2% weight loss and an “excellent” tolerability profile after 28 days of treatment at the highest dose. Treatment effects were largely maintained through Day 57 (roughly 4 weeks after last dose). In the phase 2 VENTURE-Oral trial (n=280), VK2735 demonstrated dose-dependent weight loss up to 12% at the 120 mg dose with no plateau. Durability analyses and a 90 mg titrated to 30 mg “maintenance” arm support most weight loss being maintained after stopped or lowering the dose. Furthermore, continued modest loss was observed at low doses. Dr. Lian shared Viking will focus on the ~20 mg to ~75 mg range, with lower starting doses and slower titration to optimize the GI profile, once again, following the “start low, go slow” approach.

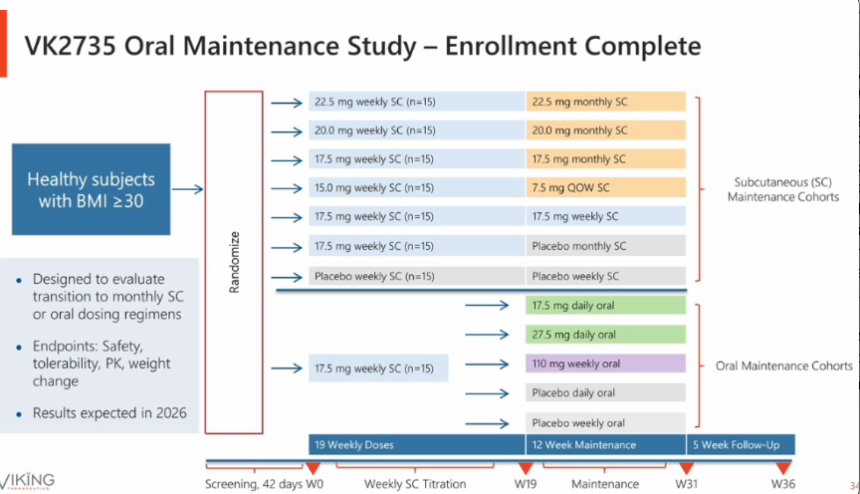

- Injectable and oral VK2735 for weight maintenance. Viking completed enrollment in a dedicated maintenance study for VK2375. The trial will start patients on injectable VK2735. After 19 weekly doses, patients will be randomized to monthly injectable VK2735, every-other-week injectable VK2735, an oral VK2735 regimen (daily or weekly), or a placebo arm. The goal of the trial is to show that after substantial weight loss with injectable VK2735, a lower dose of injectable or oral dosing can maintain weight loss with fewer side effects.

- Amylin agonist for obesity. While not covered in Viking’s prepared presentation, Dr. Lian offered insights into the amylin agonist for obesity during Q&A. Specifically, he noted than an IND filing for a single ascending dose (SAD) trial followed by a 28-day multiple ascending dose (MAD) is planned for 1Q26. Moreover, citing promising preclinical data, Dr. Lian shared that the amylin agonist could act as a standalone therapy, particularly for patients with a lower starting BMI. The company also plans to investigate a combination therapy of amylin analog and a GLP-1-based weight loss therapy like VK2735.

- VK2809 (THR-ß agonist for MASH). While VK2809 delivered a successful phase 2b readout in 2024, Viking does not intend to advance the candidate internally. The therapy is available for out-licensing, and Dr. Lian shared that there is external interest in this candidate.

9. J&J: CEO Mr. Joaquin Duato outlines diversified growth strategy with momentum in cardiovascular portfolio

In this standing-room-only session, CEO Mr. Joaquin Duato discussed J&J’s top priorities in 2026, which include MedTech, cardiovascular business, as well as surgery and ophthalmology sectors. Mr. Duato especially spotlighted J&J’s cardiology franchise, which is approaching $9 billion,anchored by cardiac ablation, heart failure device company Abiomed, and calcified arterial disease with Shockwave Medical. Notably, J&J plans to launch the Shockwave C2 Aero coronary catheter in 2026, reinforcing its leadership in interventional cardiology. While there was no direct mention of diabetes or obesity, we are excited about these advancements given that cardiovascular disease is the leading cause of mortality in this population. Mr. Joaquin also shared insights into how J&J navigates the dynamic business environment with the Trump administration.

- Mr. Duato reiterated the company’s goal to manufacture the majority of its advanced medicines used in the US, with two new plants underway in North Carolina for biologics manufacturing and Pennsylvania for cell therapy manufacturing, part of a $55 billion investment plan. The sites were announced as part of an agreement with the US government that will allow access to medicines at discounted rates for millions of patients. In exchange, the company’s pharmaceutical products are exempt from tariffs. Moreover, as part of the Most Favored Nation deal announced in November 2025, the company will also be participating in the direct-to-consumer platform TrumpRx to offer J&J medicines at discounted rates, joining other companies like Pfizer, Lilly, and Novo Nordisk. Mr. Duato viewed these agreements as a “step in the right direction,” as they expand access to medicines and give companies exception from tariffs, allowing the companies to focus on “what [they] do best” – developing, manufacturing, and commercializing medicines.

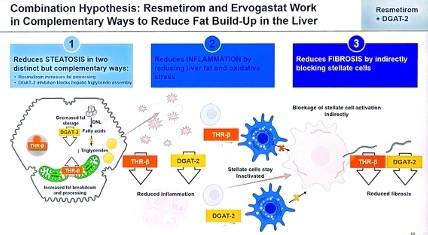

10. Madrigal: “10% of 10%” of global MASH patients treated; detailed approaches to combination therapy including GLP-1 RAs and DGAT-2 inhibitors

Madrigal CEO Mr. Bill Sibold, CMO Dr. Dave Soergel, and CFO Ms. Mardi Dier discussed the company’s approach to growth in 2026 and beyond, highlighting its recent expansion to a three-product portfolio. Mr. Sibold said that Madrigal has three areas of growth for the future: (i) delivering on the best-in-industry drug launch of Rezdiffra; (ii) progressing towards an indication for stage F4 fibrosis (cirrhosis, F4c); and (iii) extending leadership through pipeline expansion. The company will focus on combination therapy with Rezdiffra and the phase 2 oral DGAT-2 inhibitor ervogastat (which the company licensed from Pfizer just last Friday), combination therapy with SYH2086 (a small molecule oral GLP-1 RA licensed from CSPC Pharmaceutical Group in July 2025), and the F4c indication in 2026. With over 29,500 patients on therapy as of 3Q25, Madrigal still has significant potential for expansion – the market of 315,000 patients with diagnosed F2/F3 fibrosis is about 10% penetrated, which represents only 10% of all patients thought to have MASH. Many patients remain undiagnosed. This “10% of 10%” strategy of addressing a greater patient population fuels Madrigal’s optimism for the future. Mr. Sibold also compared the launch of Rezdiffra to the launch of specialty therapeutics for irritable bowel disease, rheumatoid, and psoriasis over the past thirty years. He explained that therapies for these conditions were all once thought to be very niche markets, yet all three have now grown to over $20 billion markets. Madrigal believes that the liver health market is only at the cusp of its future growth.

- Oral DGAT-2 inhibitor ervogastat offers promise for Madrigal’s pipeline. Three days ago, Madrigal announced that it has entered an exclusive global license agreement with Pfizer for ervogastat, as well as and two early-stage candidates for the treatment of MASH. Pfizer received an upfront payment of $50 million and is eligible for milestone payments and royalties on net sales. Madrigal has rights to develop, manufacture, and commercialize ervogastat globally. Dr. Soergel discussed the mechanism of action of the therapeutic class: DGAT-2 inhibitors block the enzyme called diacylglycerol acyltransferase 2 (DGAT-2), which catalyzes the final step of triglyceride synthesis and storage in the liver, lowering lipotoxic fat and inflammation. The therapy will be delivered orally and is expected to be combined with Rezdiffra, as the therapies work in distinct, complementary ways.

- In 2026, Madrigal will conduct a drug-drug interaction study of the two therapies, with a phase 2 combination study anticipated to start in 2027 following regulatory discussions. In previous studies, ervogastat has demonstrated impressive liver fat reduction, with up to 61% percent of patients considered super responders (a 50% reduction of liver fat from baseline over 48 weeks). This represents significant clinical improvement to liver fibrosis.

- Combination therapy with oral GLP-1 RA MGL-2086 was also a focus of discussion. In July 2025, Madrigal entered an exclusive global license agreement with China-based CSPC Pharmaceutical Group for SYH2086, a preclinical oral small molecule and orforglipron derivative. The therapy, now known as MGL-2086, has the potential to improve Rezdiffra’s efficacy in combination therapy. Dr. Soergel explained that weight loss of ≥5% significantly improves Rezdiffra’s efficacy, emphasizing that the company is therefore targeting such modest weight loss as opposed to greater proportions. He said that a MGL-2086 phase 1 single ascending dose study will begin in 2Q26.

- Madrigal seeks an expanded indication for compensated MASH cirrhosis, also known as stage 4 fibrosis (F4c). A significant unmet need remains in this disease stage, with an estimated addressable patient population of 245,000. There is a high urgency to treat these patients as there is a 42-fold greater risk of liver-related mortality. Management said that F4c outcomes trial data are estimated to be delivered in 2027, and that two-year data from MAESTRO-NASH OUTCOMES provides confidence in the future results. With over 10,000 current or past prescribers of Rezdiffra, Mr. Sibold said that adoption of the therapy for F4c is expected to be rapid upon approval with the therapy’s growing familiarity. As the therapeutic landscape continues to change rapidly, Madrigal says it is tracking to be first to market for this indication and more.

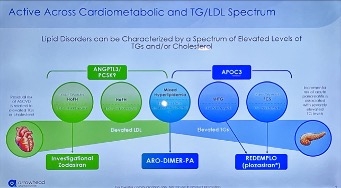

11. Arrowhead Pharmaceuticals: RNA interference treatments for obesity to advance to phase 2b trial

Dr. Chris Anzalone (Arrowhead Pharmaceuticals CEO) highlighted Arrowhead’s RNA interference (RNAi)-based therapy portfolio. Arrowhead is a clinical-stage biopharmaceutical company with a market capitalization of $8.9 billion and cash and investments of $920 million, excluding $200 million each from Sarepta and Novartis and $930 million from recent public offerings. The company is focused on developing RNAi therapies using its targeted RNAi molecule (TRiM) platform for a wide range of diseases. Arrowhead launched its first medicine Redemplo (plozasiran) – an RNAi treatment that targets APOC3 – for familial chylomicronemia syndrome (FCS) in November 2025 and continues to advance 20 early, mid, and late-stage clinical programs across cardiometabolic, pulmonary, liver, and neuromuscular indications. Dr. Anzalone emphasized that the TRiM platform can be applied to seven cell types (i.e., liver, lung, skeletal muscle, central nervous system, adipose tissue, ocular, and cardiomyocyte) with more to come, positioning Arrowhead as a “clear leader” of RNAi therapies.

- Obesity pipeline. Dr. Anzalone established what he envisions as the future of obesity care: (i) recognizing the heterogeneity of obesity; (ii) reducing visceral fat for cardio-kidney-metabolic outcomes; and (iii) combining therapies to further reduce cardiovascular risks. He noted that people with obesity and T2D lose less weight with incretin-based therapies, and therefore, positioned RNAi-based therapies as a potential treatment option to address unmet needs. Arrowhead is advancing ARO-INHBE (n=120) and ARO-ALK7 (n=126) studies in people with obesity with or without diabetes in phase 1/2a trials. ARO-INHBE inhibits Activin E, while ARO-ALK7 reduces the expression of ALK7, both of which are known to regulate energy homeostasis in adipose tissue. According to interim data announced last week, ARO-INHBE significantly reduced serum Activin-E by 85% on average, visceral fat by 9.9% at Week 16, and 16% with two doses at Week 24. In people with obesity and T2D, adding ARO-INHBE to tirzepatide doubled weight loss compared to tirzepatide monotherapy. Meanwhile, ARO-ALK7 decreased ALK7 gene expression by up to 88%, and conferred up to a 13.6% reduction in visceral fat (compared to a 0.5% increase with placebo) at Week 8.

- While remaining cautious about interpreting the early data, Dr. Anzalone expressed excitement about initiating phase 2b studies as soon as possible. Specifically, Arrowhead aims to assess the use of add-on therapies in combination with other GLP-1 RAs or as maintenance therapies following discontinuation of GLP-1 RAs. Beyond these candidates, Arrowhead hopes to expand its obesity pipeline with dimers and new targets for the liver and adipocytes.

- Lipid pipeline. As shown in the slide below, Arrowhead’s portfolio addresses both elevated LDL-C and triglycerides, including homozygous (HoFH) and heterozygous familial hypercholesterolemia (HeFH), severe hypertriglyceridemia (sHTG), FCS, and mixed hyperlipidemia. Redemplo (plozasiran), an RNAi therapy for APOC3, has been approved by the FDA and launched in November 2025. Zodasiran, an RNAi targeting ANGPTL3, has demonstrated a 41% reduction in LDL-C in people with HoFH and a 62% reduction in people taking PCSK9 inhibitors in a phase 2 trial (n=18), suggesting an additive benefit. It is currently being evaluated in a phase 3 trial (n=60). ARO-DIMER-PA is the first dual RNAi therapy targeting APOC3 and PCSK9. Preclinical studies in monkeys showed a significant reduction in non-HDL-C, LDL-C, and triglyceride levels. Arrowhead expects to launch phase 1/2 study for mixed hyperlipidemia in this month, with initial data expected at the end of 3Q26.

12. Corcept Therapeutics: Dr. Joseph Belanoff highlights broad implications of cortisol modulation, including hypercortisolism, obesity, and diabetes

In this afternoon session, CEO Dr. Joseph Belanoff discussed Corcept Therapeutics’ focus on cortisol modulation. He first explained that cortisol regulates metabolism, immune system, apoptosis, and psychiatric health. Excess cortisol is often an underlying driver of the Cushing syndrome (hypercortisolism); cardiometabolic diseases like hypertension, diabetes, obesity, and metabolic dysfunction-associated steatohepatitis (MASH); cancer; and neurological diseases like Alzheimer’s. Hence, cortisol modulation has a potential for broad therapeutic opportunities.

- Dr. Belanoff reviewed the findings of the CATALYST trial, highlighting the higher-than-expected prevalence of hypercortisolism. To many experts’ surprise, Part 1 (n=1,113) found that nearly a quarter of individuals with difficult-to-manage T2D had underlying hypercortisolism. Moreover, in Part 2 (n=252) of the trial, Korlym (mifepristone), a glucocorticoid receptor antagonist and a treatment for hypercortisolism, significantly lowered mean A1c (1.5 percentage points vs. none with placebo), weight, and visceral fat. Given the high prevalence of hypercortisolism, Dr. Belanoff estimates that the drug has potential to reach $2 billion in annual revenue.

- Corcept Therapeutics is developing relacorilant (a highly selective glucocorticoid receptor agonist) for the treatment of hypercortisolism with hypertension and/or hyperglycemia. Relacorilant aimed to address the limitations of Korylm as a non-selective progesterone and glucocorticoid antagonist (which could also be used to induce abortion). In the phase 3 GRACE program, the candidate significantly lowered systolic blood pressure by 12.6 mmHg and A1c by 0.7 percentage points from a baseline of 7.1%. Despite these results, Corcept Therapeutics received a Complete Response Letter from the FDA in December 2025, noting that more evidence of effectiveness is necessary to show favorable benefit-risk assessment. Dr. Belanoff said that the company plans to meet with the agency soon to discuss its concerns, provide additional analyses, or potentially appeal the decision.

- In MASH, miricorilant, a selective glucocorticoid receptor, is currently evaluated in a phase 2 MONARCH (n=175) study among patients with biopsy-confirmed MASH. The trial has completed enrollment, with results expected by year-end 2026. In phase 1b trial, miricorilant demonstrated 30% reduction in liver fat, as well as improvement in liver health and fibrosis, with favorable tolerability profile.

13. Novartis: De-risked pipeline driving post-Entresto growth; Leqvio as the foundational therapy for the company’s cardiorenal metabolic franchise

CEO Dr. Vas Narasimhan’s presented Novartis as a focused “pure‑play medicines” company entering a “catalyst‑rich” period on Monday morning. He detailed a diversified pipeline that expects to compensate for Entresto’s (an angiotensin receptor-neprilysin inhibitor) loss of exclusivity in July 2025 and sustain ~5% annual growth through 2030.

- Overall pipeline and financial portfolio framing. Dr. Narasimhan shared 14 in‑market blockbusters and nine additional brands with multi‑billion‑dollar sales potential in Novartis’s portfolio. Moreover, the company is hosting six active launches and expects 15 submission‑enabling readouts over the next two years. Dr. Narasimhan shared that the company targets ~5% annual growth through 2030, which is supported by a deep portfolio of patent-protected assets.

- Dr. Narasimhan described Novartis’ cardiovascular risk reduction portfolio as being built “on the back of Leqvio” – a foundational lipid‑lowering medicine. The company intends to extend its cardiovascular risk-reduction portfolio with “siRNAs to more infrequently administered medicines,” signaling interest in its RNA‑based programs that designed to improve durability and reduce patient burden of treatment in chronic cardiovascular disease.

- Dr. Narasimhan also shared excitement on Novartis’ “portfolio of assets in the renal space.” While specific candidates were not specifically named today’s presentation or Q&A, Novartis’ renal assets were considered to be in the company’s late-stage plan for a 2026-2030 catalyst and subsequent launch cycle.

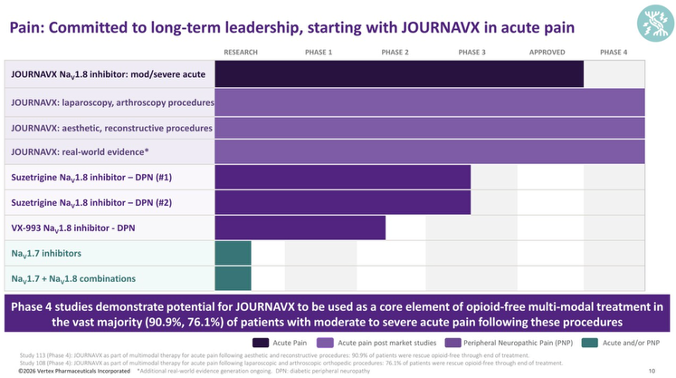

14. Vertex: Journavx (suzetrigine) shows strong growth in the pain sector with potential indication for diabetic peripheral neuropathy

Dr. Reshma Kewalramani (Vertex CEO) took the stage to present Vertex’s differentiated strategy to continue delivering in three established disease areas (cystic fibrosis, heme, and acute pain), with emerging potential in renal health and more to follow. Dr. Kewalramani emphasized that Vertex only pursues diseases that have high unmet needs and develops targeted treatments. With this focus, the company has seen significant growth from established and emerging diseases, including: (i) cystic fibrosis, which continues to expand market leadership with expectations to sustain such position for many years to come; (ii) Casgevy (exagamglogene autotemcel), which is well positioned to become a “blockbuster medicine”; (iii) povetacicept (dual antagonist of the BAFF and APRIL cytokines), which holds the potential for best in class treatment for renal health; and (iv) Journavx (suzetrigine), which builds on the momentum of its first year launch to grow in prescriptions and revenue. In addition to these key sectors, Dr. Kewalramani stated that the company aims to serve patients across 10+ disease areas, each with a multi-billion-dollar market potential. She reinforced Vertex’s commitment to diversifying geographic presence and revenue base to increase the number of patients the company can support.

- Progress of Journavx. Journavx is a twice-daily, oral, selective non-opioid NaV1.8 inhibitor FDA-approved in January 2025 for moderate-to-severe acute pain. From March 2025, when Journavx became available at pharmacies, to now, Journavx has >200 million covered lives with all three national PBMs contracted and approximately 900 hospitals with treatment access. Additionally, >30,000 prescribers have used Journavx across a broad range of specialties, and >500,000 prescriptions have been distributed to patients.

- Future outlook for Journavx. Looking forward to 2026, Dr. Kewalramani hopes to expand the number of covered lives and hospitals that use the treatment. Furthermore, she expects to double the field team to drive HCPs’ adoption and depth and triple the number of prescriptions from 2025. Dr. Kewalramani affirmed that Vertex is building a durable and long-term franchise in pain treatments, seeking a strong leadership position similar to its significant presence in cystic fibrosis. Some long-term goals of Journavx include: (i) transforming the standard of care and shifting the treatment paradigm away from opioid use; (ii) ensuring patients have an informed and positive journey; and (iii) accompanying patients with access and reimbursement.

- Journavx to penetrate other areas of pain. Dr. Kewalramani reminded Vertex’s pursuit of Journavx for other pain indications, including diabetic peripheral neuropathy (DPN). The first phase 3 trial (n=1,100) of Journavx for DPN was launched in 3Q24, and today, Dr. Kewalramani announced that the second phase 3 DPN trial has also been launched – this timeline aligns with management’s announcement in its 3Q25 call that the study would launch in November 2025. As previously shared, enrollment for both phase 3 trials of suzetrigine is expected by the end of 2026, with results available in 2027.

Diabetes Technology Highlights

15. Dexcom: Preliminary full-year 2025 revenue of $4.66 billion (+16%) and 4Q25 revenue of $1.26 billion (+13%); global userbase grows over 25% to 3.5 million

Ahead of CEO Mr. Jake Leach’s presentation at JPM this morning, Dexcom announced a total preliminary, unaudited full-year 2025 revenue of $4.66 billion, up 16% from 2024. Revenue came in slightly above the high end of Dexcom’s 2025 guidance of $4.63-$4.65 billion (updated in 3Q25). The company also reported preliminary, unaudited 4Q25 revenue of at least $1.26 billion, up 13% from 4Q24 and 4% sequentially. 4Q25 US revenue is expected to be approximately $892 million, up 11% from 4Q24 and 5% sequentially, while international revenue is expected to be $368 million, up 18% from 4Q24 and 3% sequentially. Mr. Leach also announced that Dexcom’s global CGM userbase now exceeds 3.5 million people, up over 20% from 2.8-2.9 million users at the end of 2024.

- Mr. Leach reviewed several key product and platform updates for Dexcom in 2025. He highlighted the FDA clearance and December 2025 launch of the G7 15 Day CGM for adults with diabetes as a major milestone. He described the launch as “extremely successful,” with the product now available across both DME and pharmacy channels. G7 15 Day is already integrated with Insulet’s Omnipod 5 and Beta Bionics’ iLet, and he said Tandem integration “will come very soon.” Among users who have switched, 91% reported the system is as easy or easier to use than their prior CGM.

- Dexcom also received FDA clearance for Smart Basal, designed to help basal-only insulin users reach optimal dosing in about one month and improve adherence – an area Mr. Leach described as one of Dexcom’s fastest-growing segments.

- Dexcom Direct EHR integration continues to progress, with more than 160 healthcare systems live or onboarding.

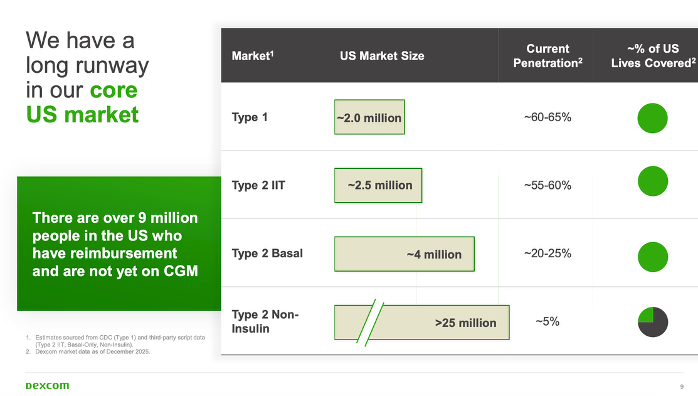

- Mr. Leach highlighted significant US coverage expansion in 2025, noting that Dexcom announced in 2Q25 that the three largest PBMs now cover CGM for all people with diabetes. The company estimates that more than nine million people currently have CGM reimbursement but are not yet using the technology. He also pointed to potential Medicare coverage expansion for people with T2D not using insulin, saying Dexcom is “on the cusp” of progress driven by strong clinical data. Mr. Leach previewed 12-month real-world data from Dexcom’s T2D non-insulin registry showing sustained improvements in A1c, weight, and BMI, building on previously shared six-month results and demonstrating benefits across age groups and medication regimens. In addition, Dexcom’s randomized controlled trial in T2D non-insulin users is expected to read out in 1H26, supporting broader global coverage expansion.

- Gestational diabetes (GDM): Mr. Leach said Dexcom has already established “good coverage” for CGM use in GDM and argued that CGM should be standard of care given strong outcomes, including reductions in C-sections, preterm births, large-for-gestational-age infants, and NICU admissions.

- Inpatient care: He noted that more than 14 million dysglycemic events occur annually in US hospitals, underscoring the need for improved inpatient glucose monitoring.

- Prediabetes: Mr. Leach said CGM can enable earlier diagnosis of prediabetes, prompting behavioral changes that reduce the risk of progression to T2D.

- Dexcom reported record new patient starts in full-year 2025 and described 4Q25 as a “too-close-to-call” race for another record quarter. Mr. Leach said 4Q25 starts were strong, noting that some patients had been delaying initiation while waiting for the G7 15 Day. While he did not provide a regional breakdown, he cited strong sell-through and use patterns in both the US and international markets.

- Mr. Leach expressed confidence in Dexcom’s 2026 financial outlook. The company issued full-year 2026 revenue guidance of $5.16-$5.25 billion, implying 11-13% growth compared to 2025. Mr. Sayer said growth will be driven by increasing CGM adoption across all diabetes populations, the continued rollout of Stelo, and further international coverage expansion. Guidance assumes strong, near-record new patient additions, high patient retention, and a largely unchanged global CGM coverage landscape. Stelo is expected to contribute “nominally.”

- Dexcom also expects a non-GAAP gross margin of 63-64% and a non-GAAP operating margin of 22-23%. Gross margin expansion is projected to be driven in part by momentum from improved manufacturing efficiency in 2H25 and uptake of the G7 15 Day. He also expects operating margin expansion despite incremental investments, including hiring and spending for Dexcom’s new Ireland manufacturing facility (see more below). In response to JP Morgan’s Mr. Robbie Marcus deeming Dexcom’s margin guidance “conservative” in Q&A, Mr. Leach cited flexibility from the G7 15 Day transition and the time required to migrate its current installed base as rationale for Dexcom’s guidance. Dexcom expects to generate more than $1 billion of free cash flow in 2026, with incremental operating expenses allocated to R&D (including software and Dexcom G8), promoting manufacturing efficiency, and expanded global sales and marketing efforts.

- Mr. Leach emphasized international expansion as one of Dexcom’s top growth priorities. He noted that Japan and France now cover CGM for all insulin users, Canada has expanded access for people with T2D, and Dexcom expects additional wins across Western Europe and Australia for insulin-using T2D patients. However, he noted that Dexcom’s guidance does not anticipate major coverage unlocks in 2026, though the company continues to work toward broader global access. Addressing affordability in markets without insurance coverage, Mr. Leach acknowledged varying price sensitivity and said Dexcom aims to keep out-of-pocket costs as low as possible. He added that Dexcom plans to introduce Stelo into international over-the-counter (OTC) markets in 2026, noting that cash-pay access can accelerate eventual reimbursement, as seen previously in Eastern Europe with Dexcom ONE. As international mix increases, he added traditional revenue seasonality may evolve; for example, he said that if Dexcom’s sequential revenue decline from 4Q to 1Q has already evolved from the mid-teens to the low double digits, we could expect to see another one-point improvement to this dynamic in 1Q26.

- Stelo adoption accelerated in 2025 following its late-2024 launch. Dexcom reported $130 million in full-year 2025 Stelo revenue, with more than 500,000 users and a “strong majority share” of the OTC CGM market. Mr. Leach highlighted Stelo’s availability on Amazon and noted that many users have signed up for product subscriptions. Product enhancements continue, including the launch of Dexcom’s AI-based meal-logging feature on Stelo in July 2025 (expanding a previous G7-only feature) that has already seen more than 10 million meals logged to date. Dexcom is also developing more advanced meal-logging tools with macronutrient tracking to better contextualize CGM trends.

- Mr. Leach discussed Dexcom’s hardware pipeline featuring the next-generation Dexcom G8 sensor, which will feature even better accuracy, 50% smaller form factor, and advanced sensing capabilities and error detection. He said Dexcom will also use product as gateway to expand into the additional clinical areas of GDM, inpatient care, and prediabetes. He also announced that Dexcom will introduce new product in its Dexcom ONE+ category.

- Mr. Leach also offered commentary on Dexcom’s pipeline and manufacturing plans. He discussed Dexcom’s next-generation G8 sensor, which is expected to offer improved accuracy, a 50% smaller form factor, and advanced sensing and error-detection capabilities. He said Dexcom will also use product as gateway to expand into GDM, inpatient care, and prediabetes. He also announced that Dexcom will introduce a new product in its international Dexcom ONE+ category in 2026. Finally, Dexcom continues to make progress on its Ireland manufacturing facility, which is expected to come online in 4Q26, alongside broader supply-chain investments to improve resilience and strengthen quality systems.

16. Medtronic: With Diabetes business spinoff expected by the end of 2026, management highlights four new generational growth platforms

Medtronic CEO Mr. Geoff Martha expressed enthusiasm about the growth trajectory across several of the company’s franchises. Commentary on the diabetes business was limited, as the unit remains on track to separate via IPO by the end of calendar year 2026. As previously disclosed, diabetes revenue totaled $2.8 billion in Medtronic’s fiscal year 2025 (+10%). He reiterated that while diabetes remains a strong business with attractive opportunities, Medtronic believes capital can generate higher returns when redeployed across other areas of the portfolio, supporting the rationale for the separation.

- While unmentioned in prepared remarks, Medtronic also announced today the FDA clearance of MiniMed Go Smart MDI app, which integrates Medtronic’s InPen with the Abbott-partnered Instinct CGM; interoperability with Simplera and the MiniMed Go app is currently under review by the FDA.

- Medtronic CFO Mr. Thierry Piéton noted that R&D spending grew to 8.5% of revenue at the end of FY2Q26 (3Q25), outpacing revenue growth, and the company has internally set a long-term target of approximately 10%. He added that diabetes currently represents an above-average R&D investment within the portfolio. Medtronic applies a three-tiered prioritization framework for R&D investment:

- Generational growth platforms such as cardiac ablation and Hugo RAS;

- High-growth businesses including neuromodulation and structural heart; and

- Large, established franchises that generate significant profit and sustain Medtronic’s leadership (e.g., next-generation CRM). Funding decisions are “rack-and-stacked” based on expected return on investment.

- Medtronic established two new management committees in 2Q25 to optimize operations and drive growth. Mr. Martha noted that while the Operations Committee is charged with focusing on margin expansion and execution under the Medtronic Performance System – which he called a driver of improved commercial, operational, and financial rigor – the most significant addition has been the Growth Committee, which is tasked with actively pursuing tuck-in M&A opportunities aligned with Medtronic’s core franchises and long-term portfolio strategy. Mr. Piéton also described itself as “on offense” for strategic M&A, with a focus on tuck-in acquisitions that complement internal innovation.

Diabetes Big Picture Highlights

17. San Francisco Mayor Mr. Daniel Lurie welcomes business, scientific, and medical leaders to San Francisco

For the lunchtime “opening,” San Francisco Mayor Mr. Daniel Lurie returned to welcome leaders to San Francisco and to introduce Mr. Dimon and Ms. Terry-Ann Burrell. We remembered vividly last year Mayor Lurie doing the same and it was terrific to see him again and to see what a difference a year makes! Mr. Lurie reflected on the changes to the city of San Francico that he has overseen in just one year, including improved public safety and economic recovery. He said that 28% of San Francisco residents believed the city was moving in the right direction one year ago, with this figure now standing at 62%! Crime is down 30% in one year and has been reduced by 40% in the city center. Getting specific, he said that car break-ins are at their lowest in 22 years. On a positive note, he said that there were with additional exciting activity in visitors to the city - hotel bookings in San Francisco related to scientific and other conferences have risen a whopping 62% in just one year! Mr. Lurie said he will continue to cultivate a direct line of communication to CEOs and small business owners and he thanked them profusely – as well as the giant group of leaders for continuing to bet on San Francisco!

18. Fireside Chat Fascinates: JPMorgan Chase CEO Mr. Jamie Dimon in conversation with Ms. Terry-Ann Burrell on geopolitics, the free market, leadership suggestions, and healthcare innovation

In an extremely packed lunchtime fireside chat (even the overflow rooms were very packed!), JPMorgan Chase CEO Mr. Jamie Dimon offered his perspective on global affairs and the role of corporations and healthcare organizations in this ecosystem.

- Mr. Dimon asserted that the US should continue to demonstrate strong military leadership in global affairs yet should not overuse the military. As the war in Ukraine enters its fifth year, with unrest growing in Iran, the broader Middle East, and Venezuela, Mr. Dimon said that the world is not a safe place and never will be. He said that the US’s military should be used to promote US interests overseas and ensure US safety. He lauded President Donald Trump for his military efforts including the deposition of Venezuelan president Nicolas Maduro and his indictment for narcoterrorism, although this operation has been considered illegal under international law, per the University of Cambridge and other sources. Despite promoting the use of the US military to secure key national security outcomes, Mr. Dimon said that approaches should not overuse the military and suggested that the US should not overstep other nations’ sovereignty only in certain cases. He called for the US to be more strategic in global affairs.

- On young voters questioning capitalism and the free market, Mr. Dimon said that corporations must think of national interests with their actions. He criticized corporate America for “fighting every tax policy” and for excessive political lobbying, which he said is part of the “political swamp” with which many voters are frustrated. He said that US K-12 education must be improved to better explain business and economic theory to the youth, so that they may make informed decisions about economic policy and not blame capitalism or socialism as a whole for their economic concerns. He said that things like the housing economy is “crippled” by rules and regulations mostly established by Democrats. Health and safety is widely considered to warrant regulation.

- Providing leadership suggestions, Mr. Dimon urged attendees to be involved, curious, and accept responsibility as leaders. He said that bad leaders continue to operate in the same way once they assume leadership, rather than changing their approach and growing over time. He said that leaders must earn their employees’ trust and respect, be factual and analytical, and must establish key deliverables for every meeting.

- The healthcare industry has exhibited tremendous growth since the first annual JP Morgan Healthcare conference. At this time, in 1983, Mr. Dimon said that both the healthcare industry and the number of investors were significantly smaller. Now, in 2025, 525 companies are in attendance at JPM, with over 10,000 investors. Since 1983, the industry has made incredible progress in cancer treatment, the invention of GLP-1 RAs, and much more, said Mr. Dimon. He believes that AI will further catalyze growth and be a powerful tool for drug discovery. “The US is not the best country in the world by health outcomes, but it is the country with the best medicines,” said Mr. Dimon. He hopes to inspire attendees to begin to change this paradigm through this conference and beyond.

It was terrific to hear the two calm, cool, and collected leaders in conversation together – we hope they continue to lead JP Morgan for a very long time. Although we didn’t hear anything about the new headquarters in New York City, we hope that the conference someday takes a mid-year field trip!

--by Kat Moon, Jeremy Alkire, Nour Khachemoune, Riya Chatterjee, Kayla Mathieu, Elizabeth Rose, Esther Min, Monica Oxenreiter, and Kelly Close