Lilly 4Q25 – D+O sales total nearly $15 billion (+59%), driven by Mounjaro and Zepbound in the US and OUS; orforglipron approval expected in 2Q26; six retatrutide trial readouts in 2026 –

Executive Highlights

- Lilly presented its 4Q25 update today in a call led by CEO Mr. Dave Ricks, CFO Mr. Lucas Montarce, CSO Dr. Daniel Skovronsky, and President of Lilly Cardiometabolic Health Dr. Kenneth Custer – see the press release, webcast, presentation slides, and financial workbook.

- Sales for Lilly’s diabetes and obesity portfolio totaled $14.5 billion in 4Q25, up an astounding 59% from 4Q24 and up a very strong 11% sequentially. Lilly sales for diabetes and obesity seemed to be strong in virtually every geography, with US revenue of $10 billion up 54% and OUS sales of nearly $4.5 billion, up 72%. US growth was primarily volume driven, growth that was clipped by 5% reflecting lower realized prices.

- Sequentially, the US was much stronger than OUS, which makes sense at year-end – sequentially, US sales rose 13%, while OUS sales rose 3%.

- US sales represented about 70% of the total, while OUS reflected the balance.

- Moving forward, we will be interested to see the extent to pricing cuts influence volume gains – it wasn’t much this quarter, but for current products, we imagine the real pricing cuts are ahead. We imagine novel products will be premium priced.

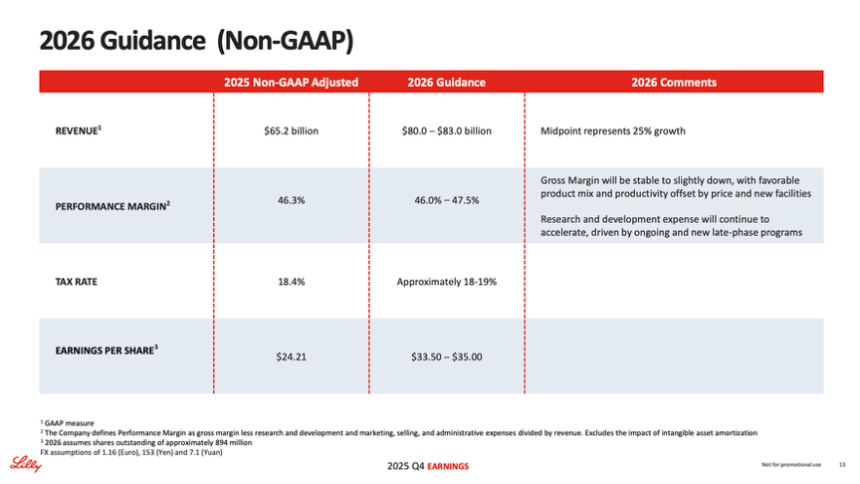

- Lilly’s overall revenue totaled $65.2 billion in 2025, exceeding its year-end guidance that was raised by ~$3.8 billion from an original guidance to $63-$63.5 billion in 3Q25. Accordingly, given its strong obesity business performance, Lilly set its 2026 guidance at $80-83 billion – representing a remarkable 23% projected revenue growth. This outlook serves as stark contrast to Novo Nordisk’s 2026 guidance, which was announced today as a reduction of -5 to -13% CER.

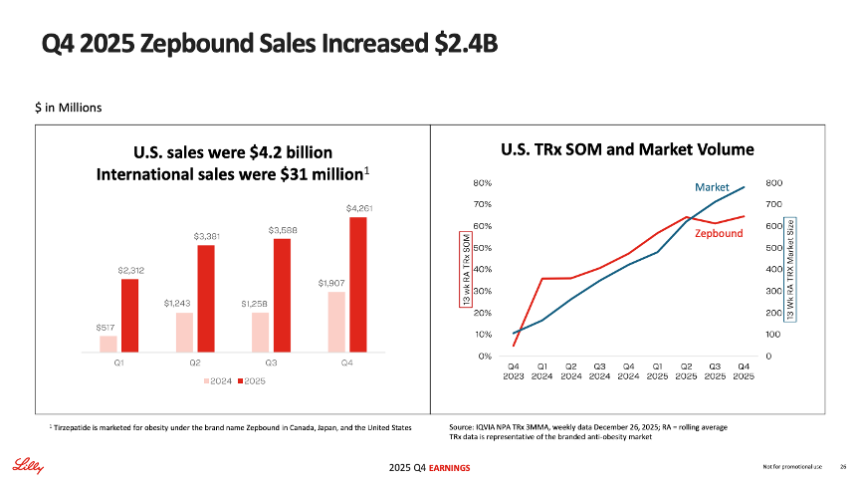

- In 4Q25, Zepbound (tirzepatide for obesity) sales totaled $4.3 billion, up over 2x from 4Q24 and up 19% sequentially. Recall that Zepbound is currently only commercialized in Canada, Japan, and the US. US sales comprised over 99% of global sales in 4Q25, with $4.2 billion in revenue. For the fourth consecutive quarter, Zepbound led the obesity market, capturing 65% of total prescriptions (TRx) and 69% of new-to-brand prescriptions (NBRx) at the end of 4Q25, according to Lilly.

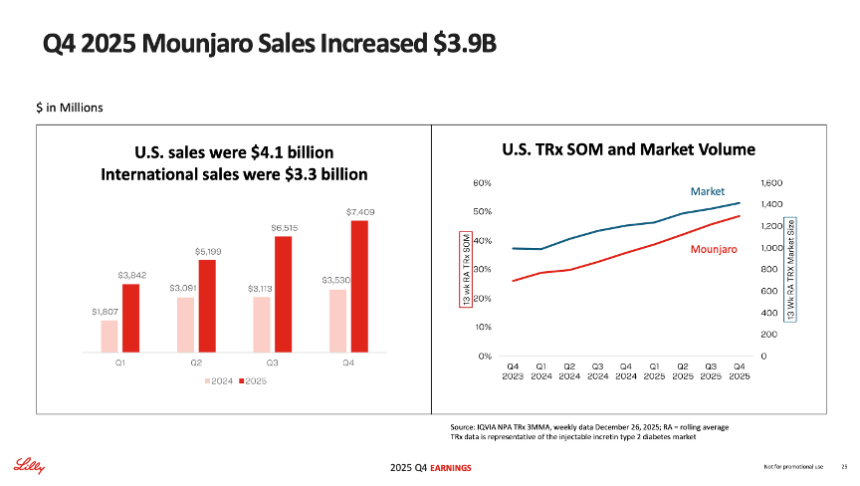

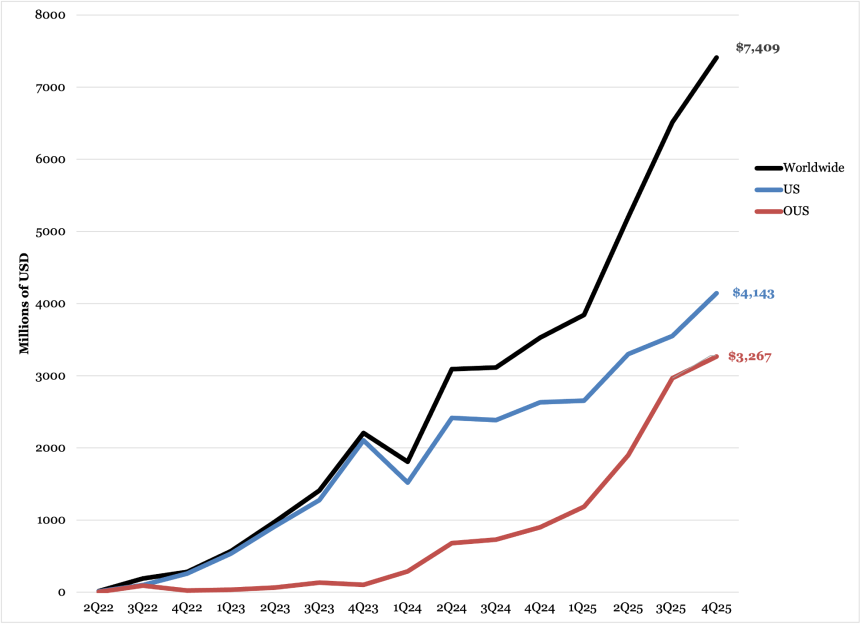

- Mounjaro (tirzepatide for T2D) sales totaled $7.4 billion, more than doubling 4Q24 and increasing 14% sequentially. US revenue was $4.1 billion, up 58% YOY and up 17% sequentially. Management said that US growth was driven by volume growth and partially offset by a decline in price. Mounjaro also expanded its market leadership, reaching over 55% of new prescriptions by the end of the quarter, similar to 54% in 3Q25.

- Lilly said that it has now completed the international launch of Mounjaro in 55 countries in all major markets. Mounjaro is currently reimbursed for T2D in nine countries.

- Lilly’s progress in the development of orforglipron (a once-daily, oral, small molecule GLP-1 RA) was a thread woven throughout today’s call. Since the company’s last report in 3Q25, Lilly has submitted orforglipron to the FDA for the management of obesity. On today’s call, Lilly confirmed that US approval is expected in 2Q26. The therapy has also been submitted in 40 other markets around the world, both for obesity and for T2D. We’re very interested in the degree to which orforglipron may be able to help people with recently diagnosed T2D – could it help delay T2D, similar to how TZield delays T1D?

- Extensive discussion ensued on Novo Nordisk’s oral Wegovy, orforglipron’s most direct competitor. Mr. Custer said that Lilly believes a number of interested and eligible patients have been “sitting on the sidelines waiting for an oral option and will quickly seek orforglipron prescriptions once it is approved” ...

- Lilly also discussed its triple GLP-1/GIP/glucagon RA candidate retatrutide as a cornerstone of its metabolic pipeline. Dr. Skovronsky said that Lilly expects to read out six additional phase 3 trials for retatrutide in 2026, including the remainder of the TRIUMPH obesity program and the TRANSCEND T2D program. This will include readouts for the TRIUMPH 1/2/3 trials and TRANSCEND 1/2/3.

- Ultimately, of eight products in diabetes affecting tens of millions of patients, there was positive growth only in Lilly’s two incretin products, Mounjaro and Zepbound. We are curious how the stakeholders in insulin, DPP-4 inhibitors, SGLT-2 inhibitors, and second generation GLP-1 (Trulicity) feel. Mounjaro and Zepbound represent 80% of Lilly’s diabetes and obesity revenue in 4Q25, which has increased from 50% in 4Q24.

4Q25 Financial Results for Lilly’s Major Diabetes and Obesity Products

| Product | 4Q25 Revenue (millions) | YOY Reported Growth | Sequential Reported Growth |

| Mounjaro | $7,409 | +110% | +14% |

| Trulicity | $1,037 | -17% | -1% |

| Jardiance/Glyxambi (royalty for Lilly) | $768 | -36% | -20% |

| Humalog | $529 | -15% | -12% |

| Humulin | $180 | -36% | +2% |

| Basaglar | $145 | -18% | -11% |

| Zepbound | $4,261 | +123% | +19% |

| Tradjenta (royalty for Lilly) | $79 | -18% | +11% |

| Total Diabetes | $14,492 | +59% | +11% |

2025 Financial Results for Lilly’s Major Diabetes Products

| Product | 2025 Revenue (millions) | YOY Reported Growth |

| Mounjaro | $22,965 | +99% |

| Trulicity | $4,276 | -19% |

| Jardiance/Glyxambi (royalty for Lilly) | $3,431 | +3% |

| Humalog | $2,168 | -7% |

| Humulin | $705 | -23% |

| Basaglar | $626 | -8% |

| Zepbound | $13,542 | +175% |

| Tradjenta (royalty for Lilly) | $318 | -10% |

| Total Diabetes | $48,161 | +63% |

Table of Contents

-

Financial Highlights

- 1. Diabetes and obesity portfolio sales total $14.5 billion (+59%), driven by Mounjaro and Zepbound; 2026 revenue guidance issued at $80-83 billion

- 2. Zepbound: Sales total $4.3 billion, up over 2x; Zepbound KwikPen (four fixed doses) approved in the US; self-pay pricing for single-dose vials lowered by $50-$100 per month

- 3. Mounjaro: Sales total $7.4 billion (+2x); international launch of Mounjaro complete in 55 markets; nine countries offer reimbursement

- 4. Trulicity: Revenue totals $1.0 billion (-17%), continuing the therapy’s downward trend as a “late lifecycle product”

- 5. Jardiance: Sales total $768 million (-36%), with comparison negatively impacted by one-time benefit of $300 million

- 6. Humalog: Revenue totals $529 million (-14%); biosimilar competition expected to increase

- 7. Basaglar: Sales total $145 million, steady from previous quarters

- 8. Tradjenta: Revenue totals $79 million (-18%), mirroring the broader DPP-4 market

-

Pipeline Highlights

- 1. Orforglipron: US approval for weight management expected in 2Q26, international in late 2026-early 2027; positioned as strong competitor to oral Wegovy

- 2. Retatrutide: Six phase 3 trial readouts expected in 2026 including TRIUMPH 1/2/3 for obesity and TRANSCEND-T2D 1/2/3; therapy targeted for patients with very high baseline BMI

- 3. Other diabetes-related candidates

- Analyst Q&A

- Close Concerns’ Questions

Financial Highlights

1. Diabetes and obesity portfolio sales total $14.5 billion (+59%), driven by Mounjaro and Zepbound; 2026 revenue guidance issued at $80-83 billion

Sales for Lilly’s diabetes and obesity portfolio totaled $14.5 billion in 4Q25, up 59% from 4Q24 and up 11% sequentially. US revenue accounted for 69% of global revenue, slightly down from 72% in 4Q24 yet up from 68% in 3Q25.

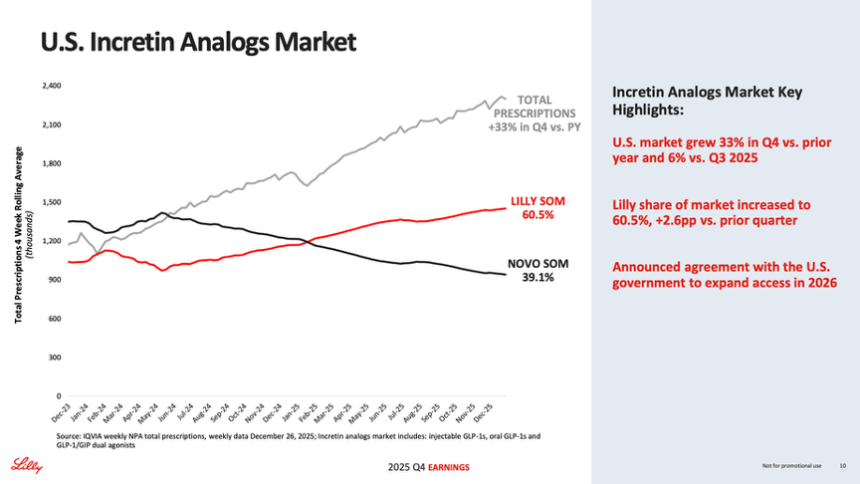

US sales totaled $10.1 billion, up 54% from 4Q24 and up 13% sequentially. Growth was attributed to a 50% increase in volume but partially offset by a 5% decrease due to lower realized prices. Mounjaro and Zepbound were the primary growth drivers in the US. For the fourth consecutive quarter, Lilly led the incretin-based therapy market (presentation slide 10, below), with Lilly’s medicines capturing 61% of total prescriptions (TRx) – up from 45% in 4Q24 and 58% in 3Q25. For T2D, Mounjaro captured 55% of new-to-brand prescriptions (NBRx) share, alongside 48% of incretin-class prescriptions for 4Q25 in the US. Moreover, Zepbound accounted for 69% of NBRx obesity management prescriptions and 65% of all obesity management prescriptions in the US during the same time period.

OUS sales totaled $4.4 billion, up 72% from 4Q24 and up 3% sequentially. Growth was mainly driven by a 46% increase in volume and by a one-time benefit of $300 million related to Jardiance. This was associated with an amendment to the company’s collaboration with Boehringer Ingelheim (BI) in 4Q24. Of note, Mounjaro is indicated for both T2D and chronic weight management in most OUS countries, except for Canada and Japan, where the therapy is only approved for use in T2D.

Source: Lilly 4Q25 presentation slides, page 10

Lilly’s overall revenue totaled $65.2 billion in 2025, exceeding its year-end guidance that was raised to $63-$63.5 billion in 3Q25, a ~$3.8 billion increase compared to 1Q25 projections. Accordingly, given its strong obesity business performance, Lilly set its 2026 guidance at $80-83 billion for the total company – representing a remarkable 23% projected revenue growth. This outlook serves as stark contrast to Novo Nordisk’s 2026 guidance, which was also announced today as a reduction of -5 to -13% CER.

Source: Lilly 4Q25 presentation slides, page 13

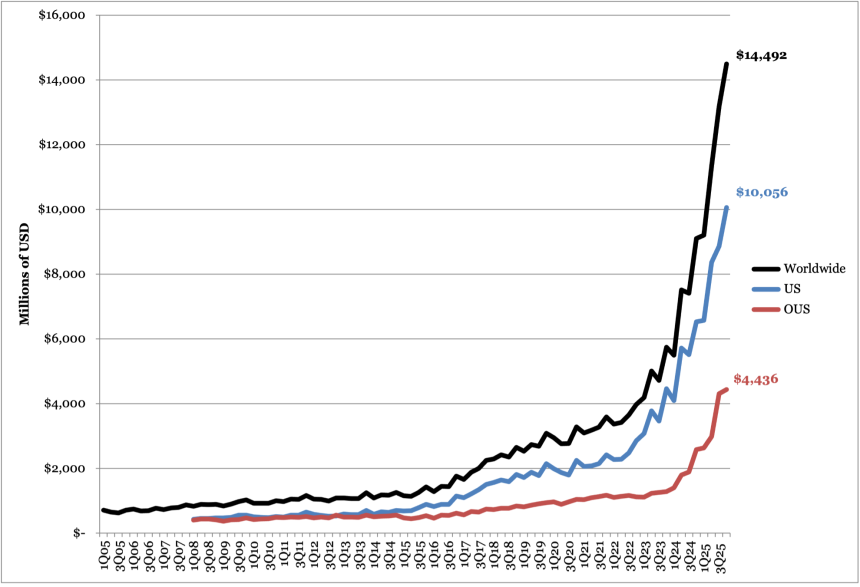

Lilly Diabetes Worldwide Financial Results – Past Five Quarters

| Overall Diabetes | 4Q23 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $9,106 | $9,208 | $11,343 | $13,118 | $14,492 | $48,161 |

| YOY Reported Growth | +59% | +68% | +51% | +77 | +59% | +63% |

| Sequential Reported Growth | +23% | +1% | +23% | +16% | +11% | n/a |

Lilly Diabetes – 4Q25 Geographic Results

| Overall Diabetes | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $10,056 | +54% | +13% |

| OUS | $4,436 | +72% | +3% |

Lilly’s Overall Diabetes Sales (1Q05 - 4Q25)

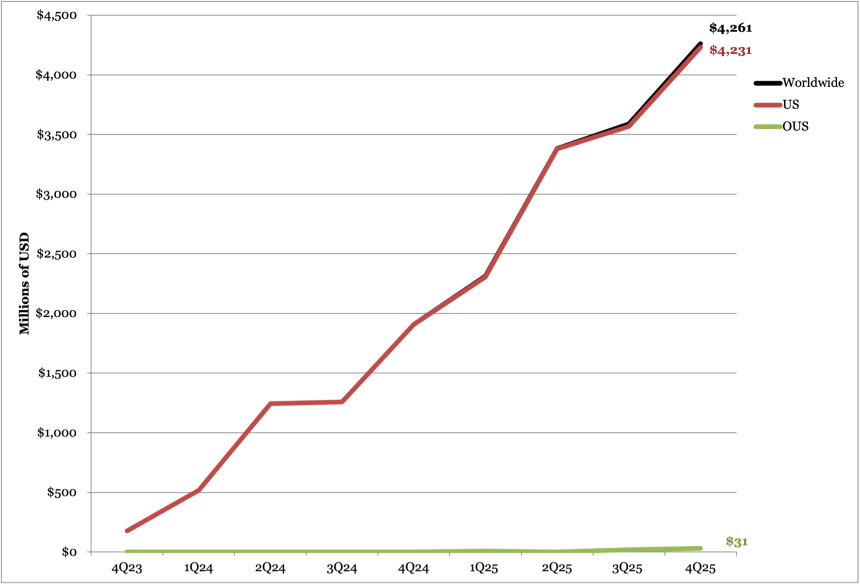

2. Zepbound: Sales total $4.3 billion, up over 2x; Zepbound KwikPen (four fixed doses) approved in the US; self-pay pricing for single-dose vials lowered by $50-$100 per month

In 4Q25, Zepbound (tirzepatide for obesity) sales totaled $4.3 billion, up over 2x from 4Q24 and up 19% sequentially. Recall that Zepbound is currently only commercialized in Canada, Japan, and the US. US sales comprised over 99% of global sales in 4Q25, with $4.2 billion in revenue. Management attributed US sales growth to increased demand, which was partially offset by lower realized prices. OUS revenue, which totaled $31 million in 4Q25, was framed as a platform for growth in 2026 considering recent and upcoming launches in major emerging markets.

For the fourth consecutive quarter, Zepbound led the obesity market, capturing 65% of total prescriptions (TRx) and 69% of new-to-brand prescriptions (NBRx) at the end of 4Q25. In comparison, Zepbound captured 63% of TRx and 71% of NBRx at the end of 3Q25. Zepbound previously experienced a slight decrease in TRx share following a loss of access on CVS Caremark’s national template formulary, which selected Novo Nordisk’s Wegovy as its preferred therapy in July 2025. During today’s call, management emphasized that Zepbound remains covered by the two other major PBMs in the US and that Lilly continues to engage in negotiations to expand access to its therapies.

- In the self-pay channel, Zepbound vials were about one-third of new patient obesity medication prescriptions in 4Q25. As background, LillyDirect was launched in the US in January 2024 to provide a direct home delivery service for prescription medications for diabetes, obesity, and migraines. Management shared today that the platform reached its one-millionth patient in 4Q25. Zepbound vials, which were made accessible in June 2025 through LillyDirect’s Self Pay Pharmacy Solutions and the Zepbound Self Pay Journey Program, are the platform’s most popular offering.

- For patients who refill within 45 days after their first purchase, Zepbound now costs $299/month for 2.5 mg, $399/month for 5 mg, and $449/month for subsequent doses (7.5 mg, 10 mg, 12.5 mg, and 15 mg). The self-pay prices, which were lowered in December 2025 during Lilly’s pricing negotiations with the US government, represent a marked decrease from previous listings. Previously, prices were $349/month for 2.5 mg and $499/month for all higher doses (5 mg, 7.5 mg, 10 mg, 12.5 mg, and 15 mg). Similarly, in Canada, Lilly lowered prices so that a four-week supply of 2.5 mg and 5 mg doses will be priced at CAD $300 (~$217 USD), while higher 7.5 mg and 10 mg doses will cost CAD $420 (~$305 USD).

- Notably, in in October 2025, Lilly entered its first retail collaboration with Walmart Pharmacy to launch a pick-up option for people with valid prescriptions for single-dose Zepbound vials. While the partnership was not mentioned during today’s call, management has previously shared that LillyDirect has significantly increased access for patients, and that it expects retail presence to further expand availability. It’s interesting from our view that Lilly and Walmart are the two companies outside tech to have hit and exceed $1 trillion in market cap.

- For Medicare beneficiaries, management shared today that access for obesity medications, including Zepbound and Mounjaro, is expected no later than July 1, 2026. Medicare benefices with Medicare Part D – the voluntary, prescription drug benefit that provides coverage for prescription medication for an additional premium – will pay a co-pay of $50/month. Management highlighted this co-pay as a “compelling value proposition” that should support patient uptake. Within a few years, management continued, Lilly believes that its anti-obesity medications will “demonstrate significant cost savings to the Medicare program.”

- On the regulatory front, Lilly received FDA approval for its Zepbound KwikPen and multi-use vials last month. The news, which was discussed in today’s call, appears in the FDA’s prescribing information that was revised in January 2026. Management shared today that it expects to launch an offering that includes four fixed Zepbound doses in a single pen in the US within “the next few weeks.”

- On clinical development, tirzepatide continues to be evaluated for weight maintenance, in adolescents with obesity or overweight, T1D, and for chronic kidney disease. Of notable interest in today’s call was the phase 3 TOGETHER-PsA trial (n=279), which investigated the concomitant use of the immunotherapy Taltz (ixekizumab) and Zepbound in adults with obesity or overweight and moderate-to-severe psoriatic arthritis[1]. Interestingly, combination therapy demonstrated superior improvement compared to Taltz monotherapy via both weight-dependent and weight-independent mechanisms. Management highlighted TOGETHER-PsA topline results in today’s call as evidence for the positive effect that incretins may have on other diseases, independent of the class’s weight loss effects.

- In 4Q25, Lilly also added one new phase 3 study, the SYNERGY-Outcomes trial (n=4,500), that will investigate tirzepatide for metabolic dysfunction-associated steatotic liver disease (MASLD).

Source: Lilly 4Q25 presentation slides, page 26

Zepbound Financial Results – Past Five Quarters

| Zepbound | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $1,907 | $2,312 | $3,381 | $3,588 | $4,261 | $13,542 |

| YOY Reported Growth | n/a | +347% | +172% | +185% | +123% | +175% |

| Sequential Reported Growth | +52% | +21% | +46% | +6% | +19% | n/a |

Zepbound – 4Q25 Geographic Results

| Zepbound | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $4,231 | 122% | +19% |

| International | $31 | n/a | +57% |

Zepbound Sales (4Q23-4Q25)

Source: Close Concerns Knowledge Base

3. Mounjaro: Sales total $7.4 billion (+2x); international launch of Mounjaro complete in 55 markets; nine countries offer reimbursement

In 4Q25, Mounjaro (tirzepatide for T2D) sales totaled $7.4 billion, more than doubling compared to 4Q24 and up 14% sequentially. US revenue was $4.1 billion, up 58% YOY and up 17% sequentially. Management said that US growth was driven by volume growth and partially offset by a decline in price. Mounjaro also expanded its market leadership, reaching over 55% of new prescriptions by the end of the quarter.

Source: Lilly 3Q25 presentation slides, page 25

OUS sales totaled $3.3 billion, up nearly 4x (+263%) from 4Q24 and up 10% sequentially. Management said that growth was driven by double digit volume growth in Europe, Japan, and China. In other markets, volume doubled, driven by the launch of Mounjaro in new markets. The therapy has launched in all major markets and has seen particular success in Latin America and in Asia.

- As of last week, the European Medicines Agency (EMA) declined to support Lilly’s request for an expansion of the Mounjaro label to include HFpEF. However, the agency has agreed to change Mounjaro's label to include information from the trials that support its use.

- Lilly said that it has now completed the international launch of Mounjaro in 55 countries in all major markets. This includes India, where tirzepatide vials were approved in March 2025 and the Mounjaro KwikPen was approved in June 2025 and launched in August 2025. Lilly is exploring various commercialization strategies; for example, in October 2025, Lilly partnered with Mumbai-based Cipla to distribute and promote Mounjaro KwikPen in India under a second brand name, Yurpeak. Management again acknowledged today that reimbursement for obesity drugs remains limited in OUS markets, including India, where all patients must self-pay for the therapy. Currently, approximately 75% of OUS revenue is from people with obesity paying out of pocket, while the remaining 25% is from T2D.

- Mounjaro is currently reimbursed for T2D in nine countries. Mr. Jonsson said that Lilly is exploring ways to gain reimbursement in other nations and that Lilly will maintain discipline in terms of pricing. In December 2025, China became the latest market to offer reimbursement for Mounjaro. The country’s National Healthcare Security Administration (NHSA) announced that Lilly’s Mounjaro (tirzepatide) for T2D will be added to the country’s new commercial insurance innovative drug list. The list aims to guide private health insurers in offering expanded coverage for high-cost, innovative therapies that are currently too expensive or novel to qualify for inclusion on the national public reimbursement drug list. Lilly said that this reimbursement move will impact OUS pricing moving forward.

- Recall that in the UK in September, Lilly raised the list price of Mounjaro from £92-£122 to £133-£330 ($125-$165 to $180-$446) for people on private insurance but not those receiving care through the National Health Service (NHS). The new pricing translates to an increase of 45% to 170%, depending on the dosage. Lilly explained that UK list prices had been significantly lower than other European countries to support early NHS access. This increase is said to better align pricing with other European markets, where Mounjaro costs €410 per month ($477) in the Netherlands and DKK 2,237 per month ($349) in Denmark, as two examples.

Mounjaro Worldwide Financial Results – Past Five Quarters

| Mounjaro | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD Millions | $3,530 | $3,842 | $5,198 | $6,515 | $7,409 | $22,965 |

| YOY Reported Growth | +60% | +113% | +68% | +109% | +110% | +99% |

| Sequential Reported Growth | +13% | +9% | +35% | +25% | +14% | n/a |

Mounjaro – 4Q25 Geographic Results

| Mounjaro | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $4,143 | +58% | +17% |

| International | $3,267 | +263% | +10% |

Mounjaro Sales (2Q22-4Q25)

Source: Close Concerns Knowledge Base

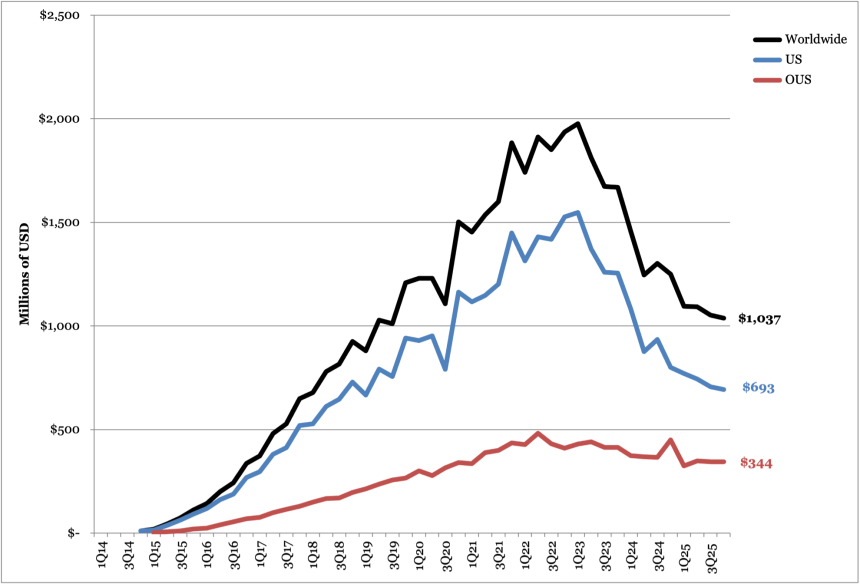

4. Trulicity: Revenue totals $1.0 billion (-17%), continuing the therapy’s downward trend as a “late lifecycle product”

Trulicity (dulaglutide) sales totaled $1.0 billion globally, down 17% from 4Q24 and down 1% sequentially. By geography, US sales totaled $693 million, down 13% from 4Q24 and down 2% sequentially. OUS sales totaled $344 million, down 24% from 4Q24 and flat sequentially. While today’s call did not discuss the factors contributing to the decline in Trulicity sales, management shared that they expected either flat or declining growth for “late lifecycle products,” which include Trulicity, Taltz (ixekizumab for plaque psoriasis), and Verzenio (abemaciclib for certain types of breast cancer). Previously, in 4Q24, Lilly attributed the decline in Trulicity sales to competitive dynamics with newer medicines like Mounjaro.

In pricing, Trulicity was announced last week as one of the 15 drugs included in the third cycle of negotiations from the Medicare Drug Price Negotiation Program (MDPNP). Trulicity will be covered under Medicare Part D, with a negotiated list price of $389/month (representing a 61% decrease from its current list price). This change is projected to take effect in 2028. As background, Medicare expenditures for Trulicity totaled $4.9 billion in 2024-2025.

Trulicity Worldwide Financial Results – Past Five Quarters

| Trulicity | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $1,250 | $1,095 | $1,092 | $1,052 | $1,037 | $4,276 |

| YOY Reported Growth | -25% | -25% | -12% | -19% | -17% | -19% |

| Sequential Reported Growth | -4% | -12% | flat | -4% | -1% | n/a |

Trulicity – 4Q25 Geographic Results

| Trulicity | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $693 | -13% | -2% |

| International | $344 | -24% | flat |

Trulicity Sales (4Q14-4Q25)

Source: Close Concerns Knowledge Base

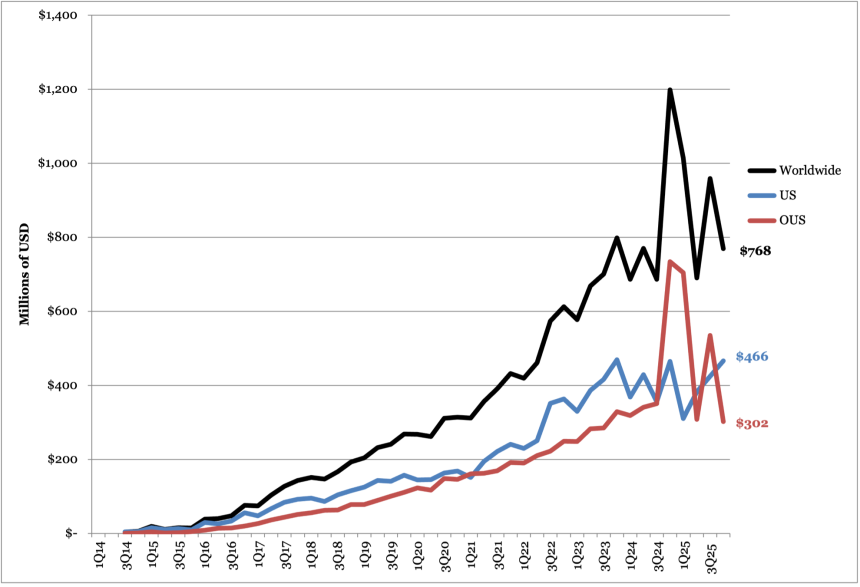

5. Jardiance: Sales total $768 million (-36%), with comparison negatively impacted by one-time benefit of $300 million

Sales for SGLT-2 inhibitor Jardiance (empagliflozin) totaled $768 million, down 36% from 4Q24 and down 20% sequentially. US sales totaled $466 million, flat from 4Q24 and up 10% sequentially. OUS sales totaled $302 million, down 59% from 4Q24 and up 44% sequentially. In 3Q25, OUS sales included a $200 million sales-based milestone payment from Boehringer Ingelheim (BI). When excluding the 3Q25 milestone payment, sequential revenue for Jardiance grew 1% globally and was flat OUS.

Also in 4Q24, OUS growth was inflated by a one-time payment of $300 million associated with an amendment to Lilly’s collaboration agreement with BI for Jardiance. Excluding the $300 million payment, revenue decreased 14% globally and 30% OUS.

- At the end of 2024, Lilly stopped reporting Jardiance’s share of prescriptions in the US. However, in 4Q24, Jardiance led the SGLT-2 inhibitor market with over 65% in total prescriptions. Later, in 2Q25, Jardiance captured 48% market share, slightly behind AZ’s Farxiga (49%).

SGLT-2 inhibitors will begin to go generic over the next few years. Jardiance’s compound patent is set to expire in 2029 in the US, 2029 in Europe, and 2030 in Japan. Nevertheless, Jardiance has won multiple indications, including for glycemic management, heart, and kidney health. Accordingly, Jardiance (10 mg or 25 mg) will remain protected under patent for the treatment of people with T2D and renal impairment until April 2034.

Lilly’s Worldwide Jardiance Revenue – Past Five Quarters

| Jardiance | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Lilly Revenue (Lilly+BI est.) – USD Millions | $1,198 ($2,694) | $1,014 ($1,933) | $690 ($2,070) | $959 ($2,877) | $768 ($2,304) | $3,431 ($10,293) |

| YOY Reported Growth | +50% | +48% | -10% | +40% | -36% | +3% |

| Sequential Reported Growth | +75% | -15% | -32% | +39% | -20% | n/a |

Lilly’s Jardiance – 4Q25 Geographic Results

| Jardiance | Revenue – USD Millions | YOY Reported Growth | Sequential Reported Growth |

| US | $466 | flat | +10% |

| OUS | $302 | -59% | +44% |

Lilly’s Jardiance Sales (3Q14-4Q25)

Source: Close Concerns Knowledge Base

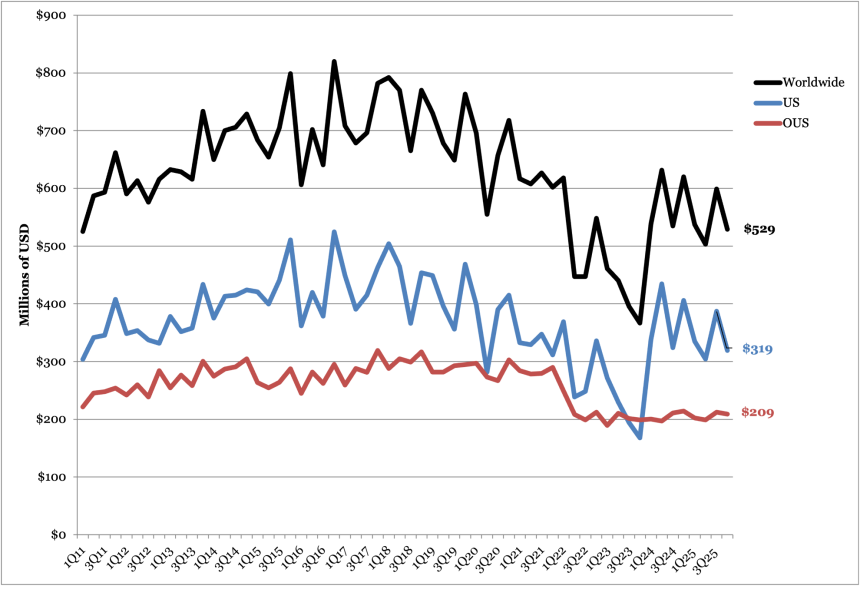

6. Humalog: Revenue totals $529 million (-14%); biosimilar competition expected to increase

Combined revenue for Humalog (insulin lispro) and generic insulin lispro totaled $529 million in 4Q25, down 14% from 4Q24 and down 12% sequentially. US sales totaled $319 million, down 21% from 4Q24 and down 18% sequentially. OUS sales totaled $209 million, down 2% from 3Q24 and down 2% sequentially.

- We imagine that increased generic and biosimilar competition will continue to affect sales globally. Biocon Biologics’ Kirsty (insulin aspart-xjhz) received FDA approval in July 2025, marking the first and only interchangeable biosimilar to Novo Nordisk’s rapid acting insulin NovoLog (insulin aspart) in the US. In February 2025, the FDA approved Sanofi’s MeriLog (insulin aspart-szjj) as the first biosimilar to NovoLog.

- While not approved yet, Adocia and Tonghua Dongbao’s BioChaperone Lispro (an ultra-rapid insulin) previously demonstrated noninferior A1c reduction and significant reduction to postprandial glucose levels compared to Humalog in a phase 3 trial for people with T1D (n=509). Adverse events and rates of hypoglycemia were similar between the two therapies. Topline results were announced during Adocia’s 3Q25 call.

In March 2023 and September 2023, Lilly reduced the price of generic insulin lispro to $25 per vial and the price of Humalog to $82 per vial, respectively. For lispro and Humalog, the price reduction included 10 mL and 3 mL vials, cartridges, KwikPens, and Junior KwikPens, but did not include the Tempo Pen – a smart, Bluetooth-compatible version of the KwikPen.

Humalog Worldwide Financial Results – Past Five Quarters

| Humalog | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $620 | $537 | $503 | $599 | $529 | $2,168 |

| YOY Reported Growth | +69% | flat | -20% | +12% | -14% | -7% |

| Sequential Reported Growth | +16% | -13% | -6% | +19% | -12% | n/a |

Humalog – 4Q25 Geographic Results

| Humalog | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $319 | -21% | -18% |

| International | $209 | -2% | -2% |

Humalog Sales (1Q11-4Q25)

Source: Close Concerns Knowledge Base

7. Basaglar: Sales total $145 million, steady from previous quarters

Sales for BI/Lilly’s insulin glargine Basaglar totaled $145 million in 4Q25, down 18% from 4Q24 and down 11% sequentially. US sales totaled $54 million, down 47% from 4Q24 and down 33% sequentially. OUS sales totaled $91 million, up +21% from 4Q24 and +11% sequentially.

While Lilly did not mention Basaglar its press release or earnings call, as expected due to the company’s current focus on weight management, 4Q25 sales are relatively consistent with the overall decline in revenue seen in the last four years, as shown in the graph below. We imagine that the continued decline likely stems from competitive pressures on pricing and volume in the Medicaid segment, which began in August 2021.

Basaglar Worldwide Financial Results – Past Five Quarters

| Basaglar | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $177 | $174 | $145 | $162 | $145 | $626 |

| YOY Reported Growth | -5% | +10% | -20% | flat | -18% | -8% |

| Sequential Reported Growth | +10% | -2% | -17% | +12% | -11% | n/a |

Basaglar – 4Q25 Geographic Results

| Basaglar | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $54 | -47% | -33% |

| International | $91 | +21% | +11% |

Basaglar Sales (3Q15-3Q25)

Source: Close Concerns Knowledge Base

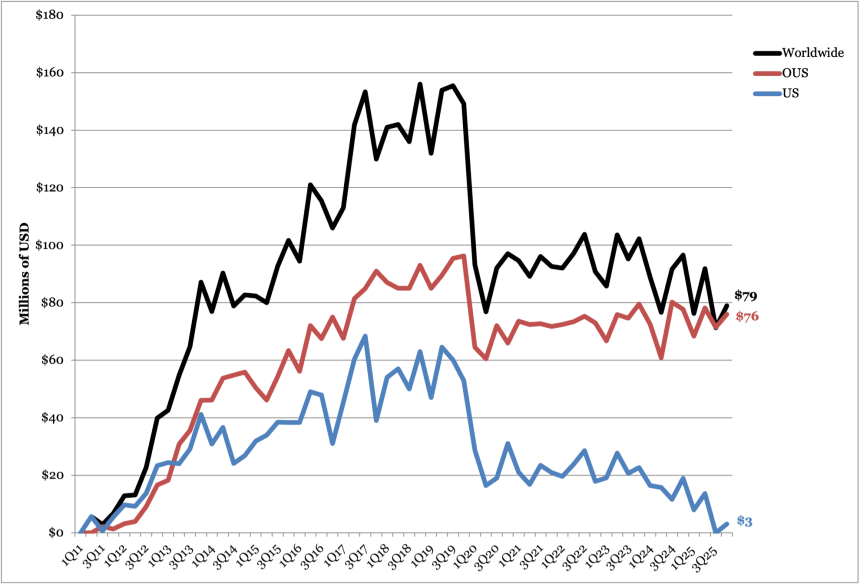

8. Tradjenta: Revenue totals $79 million (-18%), mirroring the broader DPP-4 market

DPP-4 inhibitor Tradjenta revenue totaled $79 million in 4Q25, down 18% from 4Q24 and up 11% sequentially. OUS sales totaled $76 million, down 2% from 4Q24 and flat sequentially. US sales totaled $3 million, down 84% from 4Q24 and flat sequentially. Recall that Lilly’s partner BI, which is responsible for US sales, is a private company and has not publicly reported sales for Tradjenta.

- Tradjenta’s declining sales trajectory is consistent with the broader DPP-4 inhibitor market. In 3Q25, the DPP-4 class generated $949 million in total sales, up 6% from 3Q24 but down 5% from the prior quarter. This decline thereby likely reflects switches by some patients from DPP-4 inhibitors to other therapies, like SGLT-2 inhibitors and GLP-1 RAs given their benefits beyond glycemic management.

Tradjenta Worldwide Financial Results – Past Five Quarters

| Tradjenta | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions | $97 | $76 | $92 | $71 | $79 | $318 |

| YOY Reported Growth | -5% | -14% | +20% | -22% | -18% | -10% |

| Sequential Reported Growth | +5% | -21% | +20% | -22% | +11% | n/a |

Tradjenta – 4Q25 Geographic Results

| Tradjenta | Revenue – USD millions | YOY Reported Growth | Sequential Reported Growth |

| US | $3 | -84% | flat |

| International | $76 | -2% | +6% |

Tradjenta Sales (2Q11-4Q25)

Source: Close Concerns Knowledge Base

Pipeline Highlights

1. Orforglipron: US approval for weight management expected in 2Q26, international in late 2026-early 2027; positioned as strong competitor to oral Wegovy

Lilly’s progress in the development of orforglipron (a once-daily, oral, small molecule GLP-1 RA) was a thread woven throughout today’s call. Since the company’s last report in 3Q25, Lilly has submitted orforglipron to the FDA for the management of obesity. On today’s call, Lilly confirmed that US approval is expected in 2Q26. The therapy has also been submitted in 40 other markets around the world, both for obesity and for T2D. During Q&A, Mr. Jonsson said that the launch of orforglipron in most international markets is expected in the first half 2027 due to established approval timelines in these nations. In some markets, such as in the UAE, a late 2026 launch may be possible if national approval boards use the pending US approval as reference.

- Orforglipron is expected to be submitted for the management of T2D in the US and EU in 2026. In addition to the initial submission for chronic weight management, Lilly plans to pursue a glycemic management indication, beginning with these two markets. Recall that the phase 3 ACHIEVE-5 trial (n=751) showed that orforglipron conferred an A1c reduction of 1.5% to 1.9% across doses compared to 0.8% on placebo (from a mean baseline A1c value of 8.5%). During Q&A, management also confirmed that Lilly is in discussions with pharmacy benefit managers (PBMs) concerning coverage for orforglipron at launch.

- Extensive discussion was devoted to oral Wegovy, orforglipron’s most direct competitor. In December 2025, the FDA approved Novo Nordisk’s Wegovy pill (once-daily oral semaglutide 25 mg) as the first oral incretin-based therapy for weight management. In the one month following approval, oral Wegovy showed high demand with approximately 50,000 prescriptions. Lilly said that the launch of oral Wegovy has validated its belief that effective oral GLP-1 RAs are a source of market expansion, not competition for injectables. Mr. Custer said that Lilly believes a number of interested and eligible patients have been “sitting on the sidelines waiting for an oral option,” and that oral Wegovy has seemingly seen the most interest from new patient starts in the class. He said that the market expansion driven by oral Wegovy is positive for Lilly as the company feels that orforglipron’s profile is competitive. Mr. Custer said that real-world data and patient satisfaction with the lack of food or water restrictions for orforglipron will help the therapy compete when launched.

- Mr. Yuffa said that orforglipron will have similar pricing to oral Wegovy when launched. Oral Wegovy is currently priced at $149/month for self-pay for the 4.0 mg dose as a limited time offer for new patients. On TrumpRx, a government direct-to-consumer platform, Wegovy pills and orforglipron will be priced at $150 per month and $346 per month, respectively, per the initial November 2025 announcement.

- Dr. Skovronsky discussed the positive topline results from the ATTAIN-MAINTAIN study announced in December 2025. The phase 3 ATTAIN-MAINTAIN trial (n=376) studied orforglipron for weight maintenance after the use of injectable GLP-1 RAs. Participants were either overweight or had obesity (BMI >25.0 kg/m2) and had multiple weight-related comorbidities. For patients initiating semaglutide treatment at the start of the SURMOUNT-5 trial, the mean starting weight was 250 lbs, which dropped over 15% to 209 lbs over 72 weeks. After switching to orforglipron for 52 weeks, the mean weight was 211 lbs, reflecting just a 1% body weight gain. For patients who started tirzepatide in the SURMOUNT-5 trial, the mean weight was 255 lbs, dropping 22% to 200 lbs over 72 weeks. After 52 weeks on orforglipron, the mean weight was also 211 pounds, representing a 6% body weight gain. Dr. Skovronsky said today that the average weight difference was just 0.9 kg. Full results are to be presented later this year.

- Trials for other indications have also been explored for orforglipron. A phase 3 trial for peripheral artery disease (PAD) is expected to be initiated this year, and Lilly is reportedly exploring orforglipron for stress urinary incontinence and hypertension.

2. Retatrutide: Six phase 3 trial readouts expected in 2026 including TRIUMPH 1/2/3 for obesity and TRANSCEND-T2D 1/2/3; therapy targeted for patients with very high baseline BMI

Lilly also discussed its triple GLP-1/GIP/glucagon RA candidate retatrutide as a cornerstone of its metabolic pipeline. Dr. Skovronsky said that Lilly expects to read out six additional phase 3 trials for retatrutide in 2026, including the remainder of the TRIUMPH obesity program and the TRANSCEND T2D program. This will include readouts for the TRIUMP 1/2/3 trials and TRANSCEND 1/2/3. He said that excitement is growing for retatrutide and positioned it as an example of a therapy that can lead the class. Earlier this week, Lilly announced a $3.5 billion investment in a new manufacturing facility in the Lehigh Valley in eastern Pennsylvania. The site will produce weight loss therapies such as tirzepatide and, specifically, retatrutide, when operational in 2031. Lilly’s decision to expand manufacturing in advance of the therapy’s approval further indicates its confidence in this therapy for its future.

- Strong topline results for the phase 3 TRIUMPH-4 (n=405) trial were announced in December 2025. The study was the first of the TRIUMPH program to complete and investigated retatrutide in people with obesity or overweight and osteoarthritis (OA). Participants taking retatrutide 12 mg lost an average of 29% of their body weight at 68 weeks.

- While many patients do not need to lose such a high percentage of their weight, Dr. Skovronsky said that there is an important role for retatrutide in helping people with higher baseline BMIs or helping patients with more severe obesity-related comorbidities. Interestingly, a proportion of patients with lower baseline BMIs discontinued treatment due to perceived excessive weight loss, further emphasizing the therapy’s efficacy.

- The therapy also reduced Western Ontario and McMaster Universities Arthritis Index (WOMAC) pain scores by an average of 4.5 points, which represents a 76% reduction in pain. This was accompanied by a significant improvement to physical function – over one in eight patients were completely free of knee pain by the end of the trial. Based on these data, Dr. Skovronsky said that retatrutide has the potential to become a knee treatment option for patients with certain complications.

- Lilly plans to submit the results of the core TRIUMPH program in 2026 to support applications for obesity and overweight, obstructive sleep apnea, and osteoarthritis.

- TRIUMPH-1 (n=2,300) assesses retatrutide in people with obesity or overweight and is expected to complete in May 2026.

- TRIUMPH-2 (n=1,000) investigates retatrutide in people with T2D and overweight or obesity and is expected to complete in May 2026.

- TRIUMPH-3 (n=1,800) evaluates retatrutide in people with obesity and established CVD, with study completion expected in May 2026.

- The TRANSCEND program is also investigating retatrutide in people with T2D and results are expected this year, as confirmed in today’s call.

- TRANSCEND-T2D-1 (n=480) assesses retatrutide in people with T2D and inadequate glycemic control with diet and exercise alone. The study is expected to complete in February 2026.

- TRANSCEND-T2D-2 (n=1,250) evaluates retatrutide compared to semaglutide in people with T2D and inadequate glycemic control with metformin and with or without SGLT-2 inhibitors. The study is expected to complete in January 2027, with primary completion in August 2026.

- TRANSCEND-T2D (n=320) investigates retatrutide in people with T2D and renal impairment with inadequate glycemic control on basal insulin with or without metformin and SGLT-2 inhibitor therapy. The study is expected to complete in October 2026.

- Retatrutide is also in phase 3 trials for high-risk metabolic dysfunction-associated steatotic liver disease (MASLD), chronic low back pain, and cardiovascular/renal outcomes. Management highlighted the MASLD indication specifically in today’s call, and the other indications were discussed in Lilly’s investor presentation (slide 18). As discussed in our yearly reflections, liver health has become a key area of focus for companies treating metabolic diseases, including Novo Nordisk, Roche, and Pfizer in 2025. This trend appears to continue into 2026, with Lilly now entering the arena.

3. Other diabetes-related candidates

The table below reflects other updates to Lilly’s diabetes-related products in development in alphabetical order. Items highlighted in yellow indicate changes to the pipeline in 4Q25.

| Candidate | Phase | Timeline/Notes |

| Automated Insulin Delivery System/Smart Pens | Not applicable/approved | Connected Care Prefilled Insulin Pen under regulatory review as a new indication or line extension; Lilly signs international agreement with Roche, Glooko, Dexcom, and myDiabby to integrate its connected pen products so that users have flexibility in their analysis platform in May 2021; Lilly signs collaboration and licensing agreement with Welldoc in February 2021; Lilly gains non-exclusive global and exclusive US commercialization rights to Ypsomed’s YpsoPump and future mylife AID system in November 2020; US connected pen approved by FDA in 1Q19 (type 1 and 2); AID system advanced to “phase 2” on 4Q18 call; Feasibility study with Dexcom CGM and in-house pump/closed loop algorithm completed February 2018, initiated December 2017 |

| Bimagrumab (monoclonal antibody against ACVR2B) | Discontinued phase 2 trial in obesity/overweight without T2D | Phase 2 trial discontinued in September 2025; Full results of phase 2 presented at ADA 2025; Phase 2 study initiated in October 2024 for bimagrumab/tirzepatide combination therapy in obesity or overweight without T2D. |

| Brenipatide (injectable dual GLP-1/GIP RA) | Phase 3 (Alcohol use disorder), phase 2 (asthma), phase 2 (tobacco use disorder), phase 2 (bipolar disorder) | In 4Q25, Lilly launched additional trials evaluating the therapy for tobacco use disorder and bipolar disorder. In 3Q25, Lilly launched a phase 2 trial for asthma in phase 3 trials for alcohol use disorder (AUD) and AUD with hazardous alcohol use. |

| Eloralintide (amylin agonist long acting) | Phase 3 in obesity; Phase 2 in T2D | Phase 3 study (ENLIGHTEN-2) initiated in 4Q25 for obesity/overweight and T2D;Phase 2 study on combination therapy with tirzepatide in T2D 3Q24; Phase 2 initiated in February 2024; phase 1 initiated March 2022, expected completion January 2024 |

| Jardiance (empagliflozin) in post-myocardial infarction | Phase 3 | EMPACT-MI results presented at ACC 2024, failed to meet primary composite endpoint; Fast Track designation granted by FDA in September 2020 |

| Lepodisiran (siRNA) | Phase 3 | Phase 3 ACCLAIM-Lp(a) trial for reduction of major cardiovascular events in people with high Lp(a) and CVD or at risk of a heart attack or stroke initiated in March 2024; phase 1 results presented at AHA 2023. Completion is expected in March 2029. |

| Mazdutide (GLP-1/glucagon dual agonist, once-weekly oxyntomodulin) | Phase 2 (T2D), phase 2/3 (obesity), phase 2 (alcohol use disorder) | As of 4Q25, Lilly launched a trial evaluating Mazdutide for alcohol use disorder. Positive results for phase 3 GLORY-1 study of dual GLP-1/glucagon receptor agonist mazdutide in Chinese adults with obesity on January 2024; advanced into phase 2 for obesity in 4Q23; Phase 1 trial initiated November 2022, expected completion December 2023; Phase 1b results announced in obesity in October 2022; Positive topline phase 2 results announced July 2022; phase 2 study initiated August 2021 with estimated completion 3Q22; Phase 1 completed in July 2021; China-based Innovent Biologics licensed mazdutide from Lilly in 2019; Advanced into phase 1 in 4Q16; Oxyntomodulin analog under development for type 2 diabetes and NASH; First announced in May 2016 R&D update |

| Muvalaplin (Lp(a) inhibitor) | Phase 3 | Phase 3 initiated in 3Q25 with completion expected in March 2031. Announced plans in 1Q25 to initiate phase 3 trial later in 2025; phase 2 trial initiated in November 2022 |

| Nisotirostide | Phase 2 | Phase 2 announced 2Q25; Phase 1 completed in June 2023 for overweight or obese patients studying tolerability of LY3457263 when used with tirzepatide |

| Oral dual GLP-1/GIP agonist (LY3493269) | Phase 1 | Phase 1 trial initiated March 2023, with expected completion September 2023; Phase 1 trial initiated May 2021, completed in November 2021; Announced in 3Q19 update; Moved to phase 1 in 4Q19 |

| PYY (peptide YY) analog in diabetes | Phase 1 | Phase 1 in obesity initiated November 2022, exp. completion May 2023; Phase 1 study in diabetes initiated June 2022, expected completion September 2023; Added to pipeline in 4Q20 |

| ANGPTL3 siRNA in CVD | Phase 2 | Entered phase 2 development in 3Q22; Phase 1 study completed May 2022; Licensed by Kyttaro Therapeutics in April 2022 to treat ASCVD; Added to pipeline in 4Q20 |

| Long-acting GIPR agonists in diabetes | Phase 1 | Phase 1 initiated June 2022, expected completion October 2023; Phase 1 completions October 2021, November 2021 and December 2021; Added to pipeline in 4Q20 |

| PNPL3 siRNA | Phase 1 (MASH) | Added to pipeline 2Q22; phase 1 study in NAFLD initiated June 2022 with expected completion November 2024 |

| Relaxin-LA in heart failure | Phase 1 | Phase 2 in HFpEF initiated February 2023, with expected primary completion in November 2023; Phase 1 study completed in May 2022; Added to pipeline in 1Q21 |

Lp(a) siRNA in cardiovascular disease (LY 3819469) | Phase 1 | Phase 2 trial initiated October 2022, exp. Primary completion October 2023; Phase 1 completed November 2022 |

GLP-1 receptor non-peptide agonist 2 (GLP-1/NPA 2) (LY3549492) | Phase 2 | Phase 2 trial initiated in 4Q24; Added to pipeline in 2Q24 |

| GIP/GLP-1 co-agonist 3 | Phase 1 | Added to pipeline in 2Q24 |

| PCSK9 Editor | Phase 1 | Phase 1 VERVE-102 trial announced 2Q25 for patients with familial hypercholesterolemia |

| ANGPTL3 Editor | Phase 1 | Phase 1 VERVE-201 trial announced in 2Q25 for patients with refractory hyperlipidemia |

| Beta cell encapsulation therapy for type 1 diabetes | Preclinical | Lilly entered partnership with Sigilon in April 2018; Sigilon will file IND; Afterward, Lilly will lead in-human trials |

Analyst Q&A

On orforglipron

Q (Evan Seigerman, BMO Capital Markets): So, a year from now on this call, I'd love for you to characterize what you would [Technical Difficulty] orforglipron launch. Specifically, what are some of the metrics that you're looking to meet? I know you're not going to give guidance, but some qualitative kind of commentary would be most helpful. Thank you.

A (Mr. David Ricks, CEO): Great. Thanks for the question, Evan. And kind of a little bit, but I think you were just asking about a year from now, what are some things we'll be tracking on for orforglipron. So, I think for that question, maybe we'll go to Ken to maybe talk about some things that we'll be looking at.

A (Mr. Ken Custer, Executive VP): Sure. Thanks for the question about orforglipron. We're really excited to have this medicine submitted not just in the US, but now 40 countries and looking forward to launches beginning this year. As I think about success factors for us going forward maybe towards the end of the year, we'll be looking at a few things, first of which is market expansion. We're very encouraged by what we're seeing with oral Wegovy as it validates our belief that there's a substantial number of people with overweight and obesity who have been sitting on the sidelines waiting for an oral option. It looks like these are mostly new starts. That means it's expanding the market, and that's good news for Lilly. We feel really good about the competitiveness of our profile. We've talked about that a lot on previous calls. I think we're at the point now where we're going to pivot to how do the real-world results play out. We think this is going to be about patient satisfaction. And our profile, which is simple with no restrictions on food and water intake, could make a big difference in the real world. So, we're excited to get off to the races here, see this market expand, and really look at overall patient satisfaction scores and real-world efficacy with these agents. Thanks.

Q (Courtney Breen, Bernstein): Just building on the question around orforglipron, you mentioned that you have submitted in 40 countries. Traditionally you tend to think about a full-year cycle for most approvals in many countries around the world. Can you just help us understand, if you're anticipating any kind of accelerated pathways that you might be able to access in these ex-US countries that would enable launch in 2026 for orforglipron, similar to some of the pathways that are available in the US and you've been able to garner one of them? Thank you so much.

A (Mr. Patrik Jonsson, Executive VP): Thank you very much, Courtney. As I think we shared in the prepared remarks, outside of the US, it's mainly going to be a matter of launching the first half of 2027. There will be a few markets late 2026, and a few exceptions for countries like, for example, the UAE that might reference an FDA approved of orforglipron. So mainly a play late 2026 for international markets.

On Mounjaro

Q (Chris Schott, JP Morgan): Great. Thanks so much for the question, and congrats on all the progress here. Can, I just ask about international Mounjaro? This seemed like this was a very significant upside driver, at least relative to Street numbers in 2025. And I'm just interested in your thoughts on the ramp from here as we think about the $3.3 billion 4Q result you just reported, I know last year was about a lot of new market launches, and now you're in those markets, like, how do we think about sequential growth from these levels? Thank you.

A (Patrik Jonsson, Executive VP): Thank you very much, Chris. Well, you are right. Q4 was a very strong quarter for Mounjaro also outside the US. And as Lucas referred to, we became the shadow market leader for total incretins also internationally. When you look at 2026, I would just reflect back on 2025, we had major launches, more or less in every quarter with the exception of Q4. So, I would actually look forward as a base for the 2026 growth but also consider that there was a slight impact in Q4, driven by the NRDL listing in China, effective 1/1/2026, which slightly impacts the purchasing pattern in China in December, So Q4, as a base for 2026.

Moving forward, our business now, OUS is 75% chronic weight management, and that's pretty much out of pocket, 25% is reimbursed for type 2 diabetes. So, the priorities for 2026 will pretty much be market expansion, driving more penetration through patient activation when it comes to chronic weight management.

And for type 2, we are leaning in to gain reimbursement in more countries we're currently reimbursed in nine, with last one being China with the NRDL. And we will do that with a maintained discipline in terms of pricing.

So, I think overall we are well-positioned for a continued growth for Mounjaro outside the US in 2026.

On Zepbound

Q (Geoff Meacham, Citi): Dan, I have a question for you. The together results are really super interesting. How are you thinking about the potential for combo therapies with Zepbound and either ENI [ph] or Oncology or Neuro? I wasn't sure you know what drives the investment priorities, whether it's the drug or the indication. And if there's a clear path to a labeling claim. Thank you.

A (Adrienne Brown, Executive VP): Sure. We see this as a significant opportunity. Obviously, more than a billion people worldwide have immune diseases like atopic dermatitis, psoriasis, IBD and asthma. But patients who have both immune diseases and obesity tend to have a higher disease burden.So, we're really excited about the opportunity to find new ways to combat the underlying inflammation – these diseases and potentially unlock better, longer lasting results for these patients. So, we have broad efforts underway to look at additional combinations.

We have the together -PsO trial evaluating the use of Taltz and Zepbound for adults with moderate to severe plaque psoriasis and obesity or overweight. We expect those top line results in the first half of 2026. We're also looking at the TOGETHER AMPLIFY-PsA and together AMPLIFY-PsO studies assessing the effectiveness of adding Zepbound, after starting Taltz for adults with PsA and moderate to severe plaque psoriasis.

We also have the Phase 3b COMMIT studies in both ulcerative colitis as well as Crohn's disease, where we're looking at the concomitant use of Omvoh and Zepbound and addressing outcomes for those patients.

And then the Phase 2 study of for people living with uncontrolled asthma. So, we're excited to continue to pursue the applications of incretins and unlocking better outcomes for people with immune diseases.

On other therapies

Q (Alex Hammond, Wolfe Research): Hey, guys. Thanks for taking the question. One on Eloralintide. For the weight loss results you guys presented last year look really strong. But given prescribers and patients seem more interested in more favorable tolerability, how should we think about the potential for lower doses of Elora and lower dose combos of Tirzepatide to potentially achieve a titration free placebo like tolerability with weight loss, let's say comparable to monotherapy GLP-1? Thank you.

A (Ken Custer, Executive VP): Yeah, thanks for the question, Alex. On Eloralintide and future avenues, yes, we were really excited about the data we shared at obesity last week, where patients achieved up to 20.1% weight loss with Eloralintide with excellent tolerability that was improved with titration.

In fact, in the 3mg, 6mg, 9mg titration group, I think we only had one incidence of vomiting out of more than 50 patients. So that compares, we think, really favorable versus the existing Incretin class. So, we see a big opportunity for Eloralintide in patients who maybe just can't tolerate Incretin. We know that 5% to 10% of patients in our trials tend to discontinue on the Incretin class, suggesting a pretty big opening given the size of the obesity market. Of course, we're also interested in thinking about Eloralintide in combination with other mechanisms in action and what you alluded to with GIP plus GLP-1 plus Amylin.

It's a very sort of physiological construct. Three nutrient stimulated hormones. And we've shared that. We are exploring that idea in the clinic. Nothing to share yet, but stay tuned, maybe towards the end of this year. We're testing other possible combinations, including a GIP agonist Macupatide, Eloralintide as well. And so really just trying to understand the range of options, and like you said, is there really an optimal, very simple permutation of mechanisms that could allow minimal or no titration with competitive efficacy?

On pricing, coverage, and costs

Q (Terence Flynn, Morgan Stanley): Great. Congrats on the quarter. I had a question on the guidance high level, Lucas. Just wondering if you can talk about what's embedded for Medicare volume ramp in the back half of the year and how that might drive the range we're seeing on the revenue side? And then if that's had any impact on employer opt-ins on the commercial side. I know you guys previously talked about how that might have some impact to get some of the other employers over the hurdle on coverage. So just wondering if you're starting to see that yet.

A (Lucas Montarce, CFO): Yes. Terence, thank you for the question. Maybe starting with Medicare, as highlighted in the call text, basically, we are expecting that access to be granted no later than July 1. And as I mentioned all along, this will take time to build over time, but we feel very, very positive about the opportunity to bring anti-obesity medications to patients in Medicare.

As I mentioned, again, the co-pay $50 for the patients will be a compelling value proposition as well. There is a bolus of patients that we have nowadays in the Lilly direct business that we believe are also Medicare patients. So, expect that bolus, I think it's between 10% to 20% will actually move into the Medicare space. I think that will happen relatively fast and we will continue to build on top of that.

So that's kind of the drivers start to think about, again, the penetration. But we'll build over time. We think about, again, more about the size of the opportunity in Medicare thinking about 2027 as well.

The second part of your question was about the employer opt-in. I have Ilya right next to me here as well to talk about it.

But as you said, of course, again, the practice on physicians prescribing this medicine will become more natural and broader in the anti-obesity medications. And physicians will be, again, more broadly, basically also thinking about prescribing this in commercial. How that will then impact employer side, I think the message is clear, right.

Again, there is a clear recognition of the class as a chronic disease. And basically, that will in my eyes will propel also employers also to think about again this class and also employees to look for this class of medicines as well to be covered as well. But I don't know if it's anything else that you would like to add Ilya.

A (Ilya Yuffa, Eli Lilly USA President): Yes, maybe just some additional context on some commercial opt-in. Obviously, we start the year roughly on balance, relatively stable. There are some employers adding coverage, some removing some coverage, but we're putting additional focus in the employer space.

We've stood up a team and also working with a number of third parties to actually provide alternative access channels to have some flexibility in design, transparency in the pricing and the initial conversations and feedback has been positive.

Of course, a lot of those decisions are for the following year. We anticipate having some of those decisions and increased coverage over time in the employer space. As we head into the back end of this year and mostly into 2027.

Q (Umer Raffat, Evercore): Thank you guys. Cash-pay I feel like has been a very important driver of growth among other drivers. And I'm just trying to think out loud what the long-term implications of that could look like, especially with all the competition coming?

On the one side, obviously, there's going to be tremendous brand loyalty, which is very important in cash-pay. But on the other side, the traditional PBM contracts and rebate wall may not apply. So, I'm just trying to think out loud how you're thinking about share retention and cash-pay in the long run? Thank you.

A (Patrik Jonsson, Executive VP): I think what we have been building over the last couple of years, learning a lot from the U.S., has really been the consumer centricity. And I think it's a matter of building platforms along the lines as we have done in the U.S. with Lilly Direct, where we are providing the opportunity for patients both to seek, start, and to statement. So, I think that's a massive that we need to continue to develop.

Yes. Just to add on, I think we've learned quite a bit. There are frictions in the system for a number of diseases in the U.S. and globally. Obviously, we've seen that happen in obesity. What we've built within Lilly Direct as a pretty significant scaled direct-to-consumer platform that helps address some of the frictions. Of course, we can continue to think about how we evolve that consumer experience and make this more seamless, at the same time, growing access across the different segments.

And so, I mean both will play an important role. And we continue to look for ways for us to scale as well as improve on the experience over time.

Q (Asad Haider, Goldman Sachs): Great. Thanks for taking the question and congrats on all the progress. Back to obesity with apologies, Mike, maybe just given the focus on pricing dynamics, can you just talk about what you're seeing in the contracting environment, broadly speaking, across the insulin portfolio? And also, what's your view on price elasticity in the cash channel as the year progresses? Thank you.

A (Ilya Yuffa, Eli Lilly USA President): Yeah, sure. Thanks for the question. Maybe just for the first part in terms of the commercial access and contracting, obviously we start the year with similar coverage as we ended 2025.

We continue to have coverage for Zepbound in two of the three large PBMs. We continue the conversations around expanding access in those PBMs for obviously, the introduction of Orforglipron, in Q2. So, we're in active discussions there.

From a pricing standpoint, we've been pretty transparent on pricing for 2026, as it relates to Part D as well as our direct-to-patient pricing, which we implemented at the end of December. And then we have ongoing conversations with improving and continuing access in the commercial segment.

In terms of price elasticity, we've seen overtime both in the U.S. and outside of the U.S., that affordability and opportunity on the entry as well as predictability cost for patients matter.

That's why the out of pocket in Part D of $50 is an affordable option as well as we've seen an increase in utilization of even Zepbound vial at the end of the year when we implemented improved entry price of 299 for Zepbound.

So, we continue to see that. And obviously we're seeing significant and encouraging uptake in the oral market, which is expansive, and bringing new patients to obesity treatment. We're excited to launch Orforglipron soon with the entry price being similar to oral semaglutide.

Q (James Shin, Deutsche Bank): One for David. For CMSs upcoming obesity demonstration, David, can you share any similarities or differences you foresee from what you went through previously during the Part D senior savings model for instance $35 copay rollout. Thank you.

A (David Ricks, CEO): Yeah, I mean, I think there are quite a quite a number of analogies to draw. I mean, first, arriving at a -- what would be perceived as a relatively low out-of-pocket is an important fact by itself. And while we know in this case, we're not moving from high out of pocket to low, only moving from covered plus low out of pocket.

And I think, patients who may be using GLP-1 and the data we have is that seniors are using these drugs at a lower rate than the general population, maybe because income in particular will benefit from that lower cost every month of $50. I think that's very expansionary to the class. And we'll draw a lot of interest from primary care prescribers who are concerned about the comorbidities of kind of lifetime overweight and obesity, which tend to manifest after 65 at a much higher rate.

The second thing is the consistency variance. And I think when we negotiated this with the government, we wanted to make sure that we weren't just building a program that went into the normal part D mass in terms of out-of-pocket costs but had a kind of that consistency independent of the absolute amount people pay. They get very frustrated with different amounts month to month. So, I think that's another important feature.

Thirdly, like the insulin deal, it's open to all innovators. And I think that's an important concept that the doctor and the patient choose the best therapy, which could be one from us, one from our competitor. It could be oral, could be injectable, could include future therapies from Lilly or others like Retatrutide or Eloralintide, when they're approved. So, I think that also has a parallel to what we did with insulin.

If you look back at that insulin pilot, utilization rates increased pretty dramatically in part D and frustration levels with that issue basically disappeared. I think this program has similar promise to be both enormously popular, drive a lot of new uptake. As I said, it's suppressed in the senior population who could probably benefit most, at least in the short term, from GLP-1 therapy. And I believe and I know the CMS does as well, that within a few years we'll demonstrate significant cost savings to the Medicare program.

So, that is different than the insulin part. But that's associated with new products being added. So, we're excited to get going. We expect this to be effective by July 1. Working through the details with the administration now and you'll hear more maybe on our Q1 call.

Q (Michael Yee, UBS): And I think LillyDirect, direct discussion, out-of-pocket business all enables those things. It's pretty interesting strategically because I don't think there's a good analog in our industry, and we're working through that and excited by the potential as we already see 1 million people in the US, hundreds of thousands more outside the US choosing this way to buy a medicine like Zepbound and Mounjaro.

A (Ilya Yuffa, Eli Lilly USA President): Yes. Thanks for the question. Obviously, we're excited about launching orforglipron assuming in Q2. As we think about the overall market and every launch in this space, you're launching in a larger market and greater consumer and provider awareness. We recognize that, and we look for learning from how we've launched previously. I think what's different here and people on the call have discussed this is that there is a -- typically in the cycle of launches, you start with access, build access over time and you see gradual uptake. What we've seen in this space, in particular, and obviously, we have a scale direct-to-consumer platform as part of that. You also have a significant self-pay and consumer awareness in this category. And so, our expectations are high in terms of what we expect for orforglipron in our launch. And we -- again, we expect this to be market expansive and bring new people to therapy for obesity. So that's our expectation for orforglipron over time.

Q (Mohit Bansal, Wells Fargo): Great. Thank you very much for taking my question. So, a strategic one, so I would love to understand what is your latest thinking on the importance of getting obesity related indications on the label?

Because we kind of get the mixed message, a little bit of mixed message when we talk to payers, because they kind of think that these drugs are just for obesity for now with NASH. They are still covering for obesity with NASh. But do you think this could be an overtime long-term differentiator here, now that you are going into indications like I&I as well at this point. Thank you.

A (Ilya Yuffa, Eli Lilly USA President): Sure. Thanks, Mohit, for the question. What we've seen thus far, even with Zepbound and looking at Medicare population around sleep apnea, we're seeing an increase in utilization and, thinking about obesity beyond weight and looking at outcomes related to obesity and a lot of comorbidities.

As Daniel mentioned, even in our psoriatic arthritis trial with Taltz, when we talk to employers as well as payers, they think about the multiple aspects of obesity and what that means for, coverage and cost long-term. So, we do see growing body of evidence to support covering obesity medications for population and having a positive impact to public health beyond just weight.

A (Ken Custer, Executive VP): So, thanks for the question on other potential avenues of expiry as it relates to complications and comorbidities. As our incretin portfolio and amylin portfolio expands, we're always facing the question of do we spend our resources replicating findings from previous incretins on comorbidities and complications where we know these drugs are efficacious, or do we push into new areas and generate new evidence?

You've probably seen with orforglipron, we're actually starting to explore new ideas like stress urinary incontinence, peripheral artery disease, and hypertension. We'll continue to look for new incretins in addition to what we've talked about in the INI space.

But we do also understand that with new molecules and new mechanisms, it's important to generate some data to continue to give prescribers and patients confidence that these medicines preserve the benefits of the previous class of medicines. So, we continue to do that, too. But very pleased, I think, with our overall balance of investment across the incretin portfolio in both sort of established and emerging mechanisms of diseases of interest.

On market expansion

Q (Steve Scala, TD Cowen): Well, thank you so much. 2026 revenue guidance is 15 billion to 20 billion higher than that delivered in 2025. Mounjaro and Zepbound are doing great, but we can kind of see their trajectory. Are there scenarios where these incremental sales can be delivered without or forego from being a $5 billion product in 2026? And does the guidance tell us that Lilly believes orals will grow the market and not cannibalize? Thank you.

A (Lucas E Montarce, CFO): Thank you for the question, Steve. Thinking about the guide again, you can do the math on that perspective. But when we think about the process, maybe start from there as always, we do a bottom-up approach on what we see in the marketplace and then across all the therapeutic areas and geographies as well. And we have again, a point of their guidance as kind of what is our goal for the year to start with? There are many multiples, pushes and pull. And I described that during the call text as well, talking about, again, the expansion in Medicare that Dave just covered, talking about the launch of Orforglipron as well and a continuation of growth that we expect to see both in the US and our US markets. I think it's fair to go back as well about the basically the price component as well that is embedded into the guide as well.

That's another component that is going to be actually accelerated in 2026, that erosion versus 2025. And I call out basically the low to mid-teens. That's a new component to basically some of the math that you were thinking about 2025 that you need to factor as when you're doing those, forecasting and models that you describe. In terms of your orforglipron question, I think it's important to highlight, looking at even just the last four weeks of the data of the competitor launch is mainly expansion of the market. So we are very, very encouraged from again the first month of seeing that data and is very much consistent with our expectations and our guide. We will see how much again that class will continue to grow, over the years. And we will update our guide throughout the year, depending on that.

Q (Akash Tewari, Jefferies): Hey, thanks so much. So Dave, you've mentioned that investors who really understand Lilly recognize it's a consumer stock. Can you talk about some consumer analogs you'd point investors towards when you're thinking about long-term penetration for both the US and ex-US for your weight loss product? And then maybe just on the cannibalization point. Is it fair to say your guide isn't expecting meaningful cannibalization of the oral and injectable obesity products versus what we've seen with Novo? Thank you.

A (David Ricks, CEO): Well, I think Lucas covered the cannibalization, but it's not what we're seeing right now nor is what we really expect. In a way, though, just strategically, it doesn't really matter to us. I think we're interested in having people on the medicine that they think and their doctor think is best for them. And if it comes from Lilly, that's our goal. So we're not too concerned about that, but I don't actually expect a ton of cannibalization, to be honest.

In terms of the consumer analogs, it's a difficult question. We -- I'd be open to your feedback on this. We spent a lot of time modeling out the trajectory of the out-of-pocket business. Patrick and Ilya commented on that. I think at the JPMorgan conference, I spoke about this. I think it is a bit of a wildcard in our short and midterm outlook because I am hard-pressed to think of an analog where you have this many people paying out of pocket for a prescription medication.

People could look back at the PDE wars and the ED drugs, we were part of that. We've learned some things from that, but it's not the same as this. You can look at cosmetics and aesthetics where it's quite common, but that also has some overlap, but not complete because here, you have really profound health benefits and noticeable results that really drives the success cycle for people in their lives that's kind of different.

So, I think it's hard for us to think about that. What we can do is take learning's from other industries that we're able to reduce consumer friction, unlock the power of first-party data and marketing, consider a platform and an interface with consumers that allows us to bring our really robust and deep pipeline that Ken has been talking about to market in a way that might be quite differentiated over time play with pricing opportunities, subscription models, these kinds of things, all that is in our future.

And I think LillyDirect, direct discussion, out-of-pocket business all enables those things. It's pretty interesting strategically because I don't think there's a good analog in our industry, and we're working through that and excited by the potential as we already see 1 million people in the US, hundreds of thousands more outside the US choosing this way to buy a medicine like Zepbound and Mounjaro.

Close Concerns’ Questions

- Will the price for orforglipron through TrumpRx match that of oral Wegovy, as suggested on today’s call?

- Will Lilly evaluate orforglipron and/or retatrutide in people with T1D and overweight or obesity?

- Might Lilly explore age-related effects of retatrutide, given concerns of excessive weight loss with the therapy?

- How does brenipatide (evaluated for substance use disorder) differ from tirzepatide, given that both are GLP-1/GIP RA? Is Lilly interested in exploring brenipatide’s potential efficacy in cardiometabolic diseases?

- Given the active M&A market, is Lilly interested in pursuing acquisitions for obesity or MASH-related candidates as competitors such as Novo Nordisk and Roche have done?

-- by Elizabeth Rose, Paul Moon, Nour Khachemoune, Monica Oxenreiter, and Kelly Close

[1] a chronic, autoimmune condition characterized by psoriasis, inflammation, and joint pain