3Q25 Industry Roundup – Diabetes market nears $30 billion (+25%), led by GLP-1 RAs; obesity sales total $6.9 billion (+48%) contributing to 32% growth for combined diabetes and obesity markets –

Executive Highlights

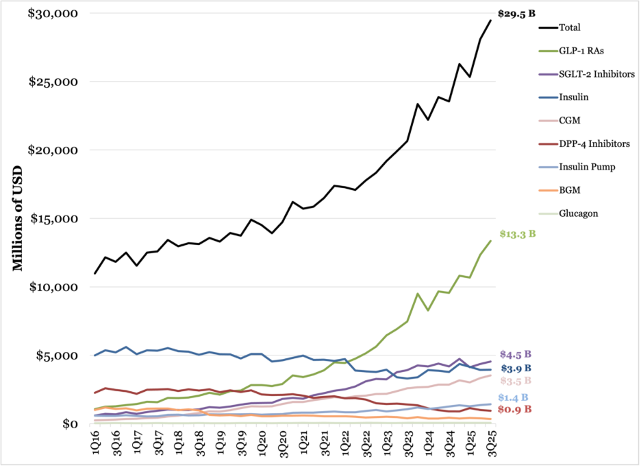

- The global diabetes market came close to hitting a brand-new threshold in 3Q25, reaching nearly $30 billion, up a remarkable 25% from 3Q24 and up 5% sequentially.

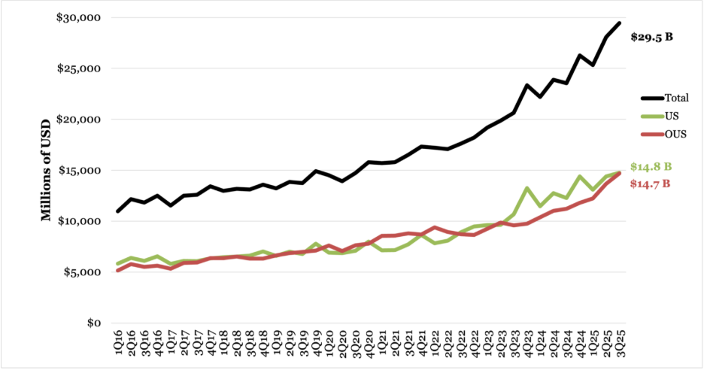

- By geography, total sales in the diabetes market were split almost exactly evently between the US and OUS markets, which totaled $14.8 billion (+20% YoY, +2% Q/Q) and $14.9 billion (31% YoY, +7% Q/Q), respectively. It was quite compelling to us how big the growth was globally – wow! And, a look at “fourth quarters” over the years show increases followed by declines, so we are hopeful as well as optimistic about the quarter. Consistent with previous quarters, GLP-1 RAs, which grew at 40% in 3Q25, represented 63% of the growth, which doubled in 3Q25. Continuous glucose monitors, up 24% in 3Q25, had the next highest contribution of growth, at 11%, followed by SGLT-2 inhibitors (6%), insulin pumps (2.6%), insulin injectables (2.5%), and DPP-4 inhibitors (0.9%). Those last four groups grew 23%, 13%, 4%, and 6%, respectively. BGM was the only sector whose sales declined in 3Q25, by 19% from 3Q24 reflecting an extremely robust quarter. We expect another robust quarter in 4Q25, the reporting for which starts tomorrow with J&J and Thursday with Abbott.

- Global obesity sales hit $6.9 billion in 3Q25, up 48% from 3Q24 and 5% sequentially. The combined diabetes and obesity market totaled $36 billion, up a nearly unbelievable 32% from 3Q24 and up 5% sequentially. By geography, US sales totaled $5.5 billion, up 73% from 3Q24 and up a whopping 34% sequentially. OUS sales totaled $1.3 billion, up 74% from 3Q24 on a small base and up 2% sequentially. Lilly’s Zepbound led the obesity market for the second consecutive quarter (+185%, + 6% sequentially), capturing 52% of global sales, while Novo Nordisk’s Wegovy captured 46% market share (+23%, +4% sequentially). The obesity market has been dynamic to say the least, with evolving competitive landscape, pricing pressure from the Most-Favored-Nation negotiations, and increasing use of cash-pay channels. We imagine this breakdown will evolve positively in 4Q25, given the momentum and strong interest in the field that is being propelled by obesity and CGM/AID.

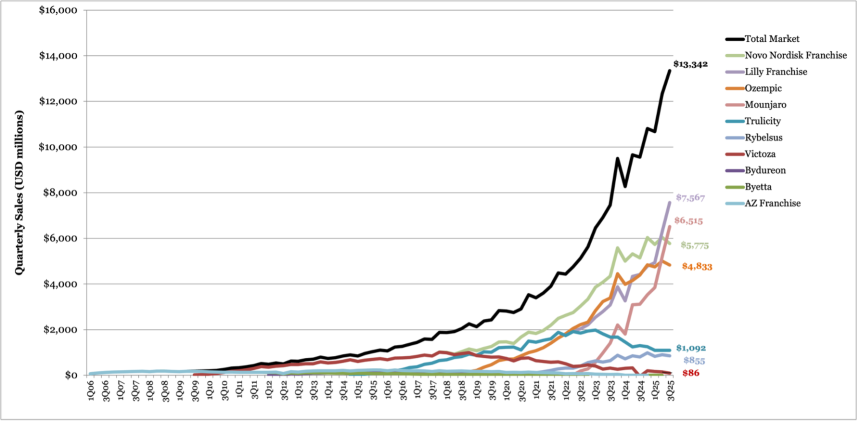

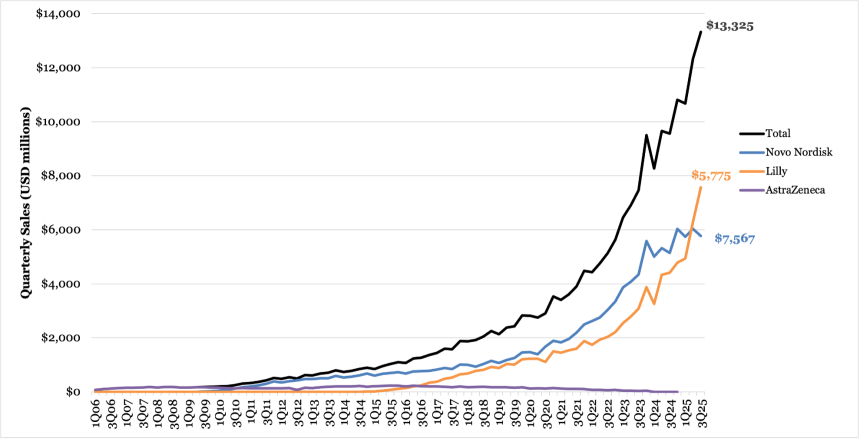

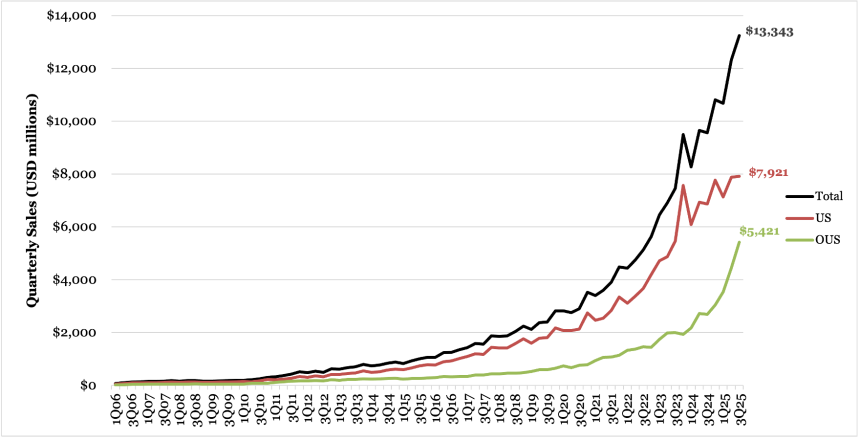

- Diabetes therapy revenue in 3Q25 totaled $23 billion, up 23% from 3Q24 and up 5% sequentially. By geography, US and OUS sales were exactly even at $11.5 billion (+17% YoY, +3% Q/Q) and $11.5 billion (+30% YoY, +8%), respectively, reflecting robust growth in the OUS market led by GLP-1/multi-incretin sales of $5.4 billion (+2x). By medication classes, GLP-1/multi-incretin sales of $13.3 billion (+40% YoY, +7% Q/Q) represented by far the largest revenue class, more than double the size of the second largest contributor, SGLT-2 inhibitors of $5.1 billion (+23% YoY, +18% Q/Q).

- Diabetes GLP-1/Multi-Incretin Agonists ($13.3 billion, +40%): Since 2006, GLP-1 RAs have generated a cumulative revenue of more than $198 billion, including $142 billion in US sales and $57 billion in OUS sales – it is striking that to date, over 70% of GLP-1 RA sales have happened stateside. Indeed, by geography, 3Q25 sales totaled nearly $8.0 billion in the US (up 15% from 3Q24 and up 1% sequentially) and $5.4 billion OUS (up over 2x from 3Q24 and up a whopping 22% sequentially).

- For the second quarter in a row, Lilly’s Mounjaro (tirzepatide for diabetes) led the market, surpassing Novo Nordisk’s Ozempic (semaglutide for diabetes) and capturing 49% of total 3Q25 sales (up from 33% in 3Q24). Novo Nordisk followed with 42% market share (down from 46% in 3Q24). In the pipeline, candidates like orforglipron, CagriSema, and amycretin continue to advance along clinical development for diabetes and obesity.

- SGLT-2 inhibitors ($5.1 billion, +23%): Since 2013, SGLT-2 inhibitors have generated $92 billion in cumulative revenue, reflecting greater appreciation for the therapeutic class's benefits for glycemic, heart, and kidney health. By geography, the gap between US and OUS sales has increased over the years, with US sales totaling $1.8 billion (+19%, +9% Q/Q) and OUS sales totaling $3.4 billion (+25%, +23% Q/Q). BI/Lilly’s Jardiance (empagliflozin) sales totaled $2.9 billion, up 40% from 3Q24 and up 39% sequentially. The therapy captured 56% market share, returning to the lead position after two quarters of sale improvement by BI/Lilly’s biggest competitor. AstraZeneca’s Farxiga (dapagliflozin) revenue totaled $2.1 billion (+10%, -1% Q/Q) and captured 41% of market share. Sales for Merck’s Steglatro (ertugliflozin) totaled $132 million, down 28% from 3Q24 and down 3% sequentially. With SGLT-2 inhibitor patents beginning to expire, generic versions of SGLT-2 inhibitors will become available over the next few years, which is expected to increase access to these therapies.

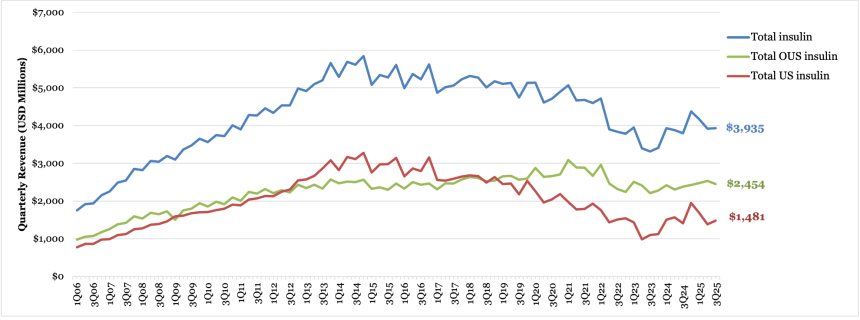

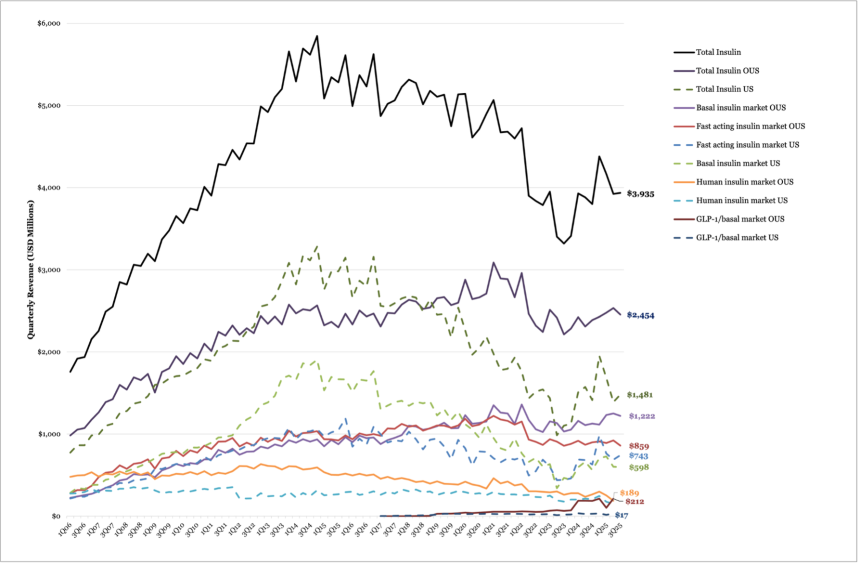

- Insulin ($3.9 billion, +4%): Sales in 3Q25 increased 4% from 3Q24 and remained flat sequentially. US revenue totaled $1.5 billion, up 10% from 3Q24 and 7% sequentially, and OUS revenue totaled $2.5 billion, up 1% from 3Q24 and down 4% sequentially. Since 2006, insulin has generated $340 billion in cumulative revenue.By company, Novo Nordisk’s insulin portfolio captured 46% of global insulin sales (down from 47% in 2Q25), followed by Lilly (28%, flat from 28%) and Sanofi (26%, up from 25%), remaining consistent with previous quarters. We are very curious how much investment the three companies are each putting into insulin.

- Basal insulin sales totaled $1.8 billion (+8%, -2% Q/Q). US sales totaled $598 million (+6%, -1% Q/Q), and OUS sales totaled $1.2 billion (+8%, -2% Q/Q). It’s fascinating to see how international basal sales continue to grow, while US basal sales are now only about one-third of the total.

- Rapid acting insulin sales totaled $1.6 billion (+5%, -1% Q/Q). US sales totaled $743 million (+18%, +8% Q/Q) and OUS sales totaled $859 million (-5%, -7% Q/Q).

- Human insulin sales totaled $385 million (-19%, +11% Q/Q). US sales totaled $196 million (-5%, +31% Q/Q) and OUS sales totaled $189 million (-29%, +27% Q/Q). It’s interesting to see that human insulin sales are effectively split between US and OUS

- Basal insulin/GLP-1 fixed ratio combinations contributed $124 million to the insulin market (+17%, -3% Q/Q). In the US, basal/GLP-1 RA sales totaled $16 million (+14%, flat Q/Q), and OUS sales totaled $109 million (+17%, -3% Q/Q) – the international field owns this market.

- DPP-4 Inhibitors ($949, +6%): DPP-4 inhibitor sales increased 6% from 3Q24 and down 5% sequentially. US revenue reached $336 million (+194%, +4% sequentially) and OUS revenue totaled $613 million (-22%, -10% sequentially). Merck’s Januvia franchise, which includes Januvia (sitagliptin) and Janumet (fixed-dose sitagliptin + metformin), continued to lead the market (62% of share), totaling $625 million in revenue (+107% YoY, flat Q/Q). BI/Lilly’s Tradjenta (-22% YoY, -22% Q/Q) captured 21% of market share, while Novartis’ Galvus (-21% YoY, +2% Q/Q) captured 13%. Overall declines in DPP-4 inhibitors are thought to be partly driven by competition from other oral agents, such as SGLT-2 inhibitors, as well as generic competition in markets like China and Japan.

- Diabetes GLP-1/Multi-Incretin Agonists ($13.3 billion, +40%): Since 2006, GLP-1 RAs have generated a cumulative revenue of more than $198 billion, including $142 billion in US sales and $57 billion in OUS sales – it is striking that to date, over 70% of GLP-1 RA sales have happened stateside. Indeed, by geography, 3Q25 sales totaled nearly $8.0 billion in the US (up 15% from 3Q24 and up 1% sequentially) and $5.4 billion OUS (up over 2x from 3Q24 and up a whopping 22% sequentially).

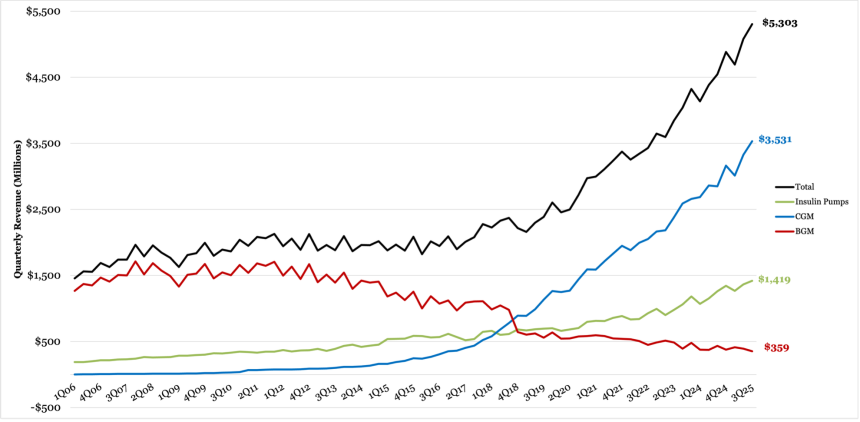

- Diabetes technology revenue in 3Q25 totaled $5.3 billion, up 17% from 3Q24 and 4% sequentially. CGM sales represented the majority of revenue – over two-thirds - followed by insulin pumps representing 27% of total revenue and BGM, as reported by public companies, at nearly 7%. Sales by geography were again divided nearly equally, with US sales of $2.6 billion, up 16% from 3Q24 and 3% sequentially, while international sales totaled $2.7 billion, up 17% from 3Q24 and 5% sequentially.

- CGM growth in 3Q25 was broadband across companies and geographies, totaling $3.5 billion (+24% from 3Q24, +6% sequentially). US sales totaled $1.7 billion, up 20% annually and 1% sequentially, compared to OUS sales of $1.8 billion, up 28% and 12%, respectively. Growth partly reflects increasing CGM adoption among people with T2D, with OTC CGM bringing those with T2D not on insulin and those in the wellness space. We estimate the global CGM userbase, excluding OTC CGM, to be over 11.5 million users as of 3Q25.

- 3Q25 brought another strong quarter for insulin pumps and AID ($1.4 billion, +13%) driven by accelerating T2D uptake, expanding pharmacy access, and continued international momentum. US pump revenue totaled $821 million, up 12% from 3Q24 and 8% sequentially, while OUS pump revenue totaled $598 million, up 14% from 3Q24 and flat sequentially. Insulet maintained its lead in market share by revenue with 49%, followed by Medtronic (31%), Tandem (18%), and Beta Bionics (2%). We estimate that the global AID userbase represents over 1.5 million individuals, representing double-digit growth from 3Q24.

- BGM revenue in 3Q25 totaled $359 million, declining both annually (-17%) and sequentially (-8%)from a high base. This continues a trend of several quarters of decline amid continual pricing pressure and most frequent testers (still) moving to CGM. For the two remaining public BGM companies, Abbott and Roche, we estimate combined 3Q25 US sales of $72 million, down 4% annually but up 10% sequentially, while international sales totaled $287 million, down 20% from 3Q24 and 12% sequentially.

Table of Contents

Overall Diabetes Market

Graph 1: Aggregate Market Sales by Category (1Q06 – 3Q25)

Graph 2: Aggregate Market Sales by Geography (1Q16 – 3Q25)

Diabetes Therapy

GLP-1 and Multi-Incretin Agonists

In 3Q25, the revenue for diabetes GLP-1 and multi-incretin agonists totaled $13.3 billion, up 40% from 3Q24 and up 7% sequentially. Since 2006, GLP-1 RAs have generated a cumulative revenue of more than $198 billion, including $142 billion in US sales and $57 billion in OUS sales. By geography, 3Q25 sales totaled $7.9 billion in the US (up 15% from 3Q24 and up 1% sequentially) and $5.4 billion OUS (up over 2x from 3Q24 and up 22% sequentially).

For the second quarter in a row, Lilly’s Mounjaro (tirzepatide for diabetes) led the market, surpassing Novo Nordisk’s Ozempic (semaglutide for diabetes) and capturing 49% of total 3Q25 sales (up from 33% in 3Q24). Novo Nordisk followed with 42% market share (down from 46% in 3Q24).

- Lilly’s Mounjaro, a dual GIP/GLP-1 RA, totaled $6.5 billion in 3Q25 (+109%, +25% Q/Q). For the second quarter in a row, Mounjaro led the diabetes GLP-1 RA market – capturing 49% of global sales, as well as 45% of TRx and 54% of new-to-brand Rx (NBRx) by the end of 3Q25. In comparison, Mounjaro captured 42% of TRx and 50% of NBRx in 2Q25. Mounjaro is now launched in most major OUS markets, including Mexico, Brazil, China, and 52 other countries. In India, tirzepatide vials were approved in March 2025, and Mounjaro KwikPen was approved in June 2025 and launched in August 2025. Separately, Lilly raised the price of Mounjaro in the UK in September 2025 by 45% to 170%, depending on the dosage, for people on private insurance. Lilly explained that UK list prices had been significantly lower than those in other European countries to support early NHS access, and that these prices better align with European market pricing.

- In clinical development, the full readout of the phase 3 SURPASS-CVOT trial (n=13,299), which compared Mounjaro to Trulicity (dulaglutide) in people with T2D and established CV, was presented at EASD 2025. Trial results demonstrated that Mounjaro reduced the risk of MACE by 8 percentage points compared to Trulicity.

- Trulicity sales continued to decline in 3Q25, totaling $1.1 billion globally, down 19% from 3Q24 and down 4% sequentially. By geography, US sales totaled $707 million, down 24% from 3Q24 and down 5% sequentially. OUS sales totaled $345 million, down 6% from 3Q24 and down 1% sequentially. In 4Q24, Lilly attributed the decline to competitive dynamics with newer medicines like Mounjaro.

- Novo Nordisk’s Ozempic totaled $4.8 billion (+9%, -3% Q/Q) in 3Q25. In the US, Ozempic’s weekly prescriptions totaled ~670,000 units in 3Q25, down from 690,000 in 2Q25. Since 2Q25, Mounjaro has exceeded semaglutide in both new-to-brand and total prescriptions (737,000 for tirzepatide vs. 670,000 for semaglutide). To improve uptake in the cash channel, Novo Nordisk launched a cash option for Ozempic at $499 per month for eligible self-paying patients in August 2025. This price reflects a 50% reduction from the list price of ~$1,000/month and applies to all three Ozempic auto-injector doses (0.5 mg, 1 mg, and 2 mg). Moreover, Novo Nordisk continued to expand partnerships in 3Q25 to increase patient access, including with retail pharmacies like Costco, CVS, and Walmart.

- Rybelsus (oral GLP-1 RA) totaled $855 million in 3Q25, down 4% from 3Q24 and flat sequentially. US sales totaled $312 million (-18% CER, -3% Q/Q), and OUS sales totaled $543 million (-15% CER, +2% Q/Q). On the regulatory side, Novo Nordisk obtained approval for CV indications in the US and the EU for oral semaglutide (14 mg). FDA decision for high-dose oral semaglutide (25 mg) is expected in 4Q25.

- Victoza (liraglutide) totaled $86 million, flat CER from 3Q25 and down 40% sequentially, with declines driven by the movement of GLP-1 RA market to next-generation incretin-based therapies, as well as the multiple launches of generic liraglutide. Year-to-year sales growth was marked as flat in the company’s report because Victoza sales totaled $47 million in 3Q24, due to negative prior-year adjustments from higher Medicaid exposure in the US.

- In the pipeline, Lilly has announced several phase 3 trial results for orforglipron, a once-daily oral small-molecule GLP-1 RA, in adults with overweight or obesity without (ATTAIN) or with T2D (ACHIEVE). Novo Nordisk submitted CagriSema (a once-weekly injection of fixed combination cagrilintide 2.4 mg and semaglutide 2.4 mg) for FDA approval in December 2025based on the phase 3b REDEFINE 1 (n=3,417) and REDEFINE 2 trials (n=1,206). Amgen added two more trials to its global phase 3 program of once-monthly MariTide (dual GLP-1 RA and GIP receptor antagonist) in 3Q25, among other trial progress updates. Other candidates in the pipeline include GLP-1/glucagon dual RA (such as Altimmune’s pemvidutide and BI/Zealand’s survodutide), GLP-1/GLP-2 RA (Zealand’s dapiglutide), GLP-1/amylin analog (Novo Nordisk’s oral amycretin), and subcutaneous and oral GLP-1/GIP RA (Viking’s VK2735). For a full breakdown of what’s to come, see our GLP-1/multi-incretin agonist competitive landscape here.

- AstraZeneca no longer reports revenue for Byetta as of 1Q22 or Bydureon as of 1Q24. Nonetheless, AstraZeneca remains invested in treatments for obesity and/or T2D and is running several phase 2b trials for oral GLP-1 RA (AZD 5004), dual GLP-1/glucagon RA (AZD9550), and long-acting once-weekly amylin (AZD6234).

Graph 3: GLP-1 Agonist Total Sales (1Q06 – 3Q25)

Graph 4: GLP-1 Agonist Sales by Company (1Q06-3Q25)

Table 1: 3Q25 GLP-1 Agonist Sales

| Revenue (Millions) | Growth | Sequential Growth | Share of Market | |

| Ozempic | $4,833 | +9% | -3% | 36% |

| Mounjaro | $6,515 | +109% | +25% | 49% |

| Trulicity | $1,092 | -19% | -4% | 8% |

| Rybelsus | $855 | +4% | -4% | 6% |

| Victoza | $86 | Flat | -40% | 1% |

| Total | $13,342 | +40% | +7% | -- |

*This total does not include sales for AstraZeneca’s Bydureon, which were not disclosed for the first time in 1Q24.

Graph 5: GLP-1 Agonist Sales by Geography (1Q06-3Q25)

Table 2: 3Q25 GLP-1 Agonist Geographic Breakdown

| 3Q25 US Revenue (Millions) | US Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS Growth | OUS Sequential Growth | |

| Ozempic | $3,344 | +1% | -3% | $1,489 | +9% | -4% |

| Mounjaro | $3,550 | +49% | +8% | $2,965 | +307% | +56% |

| Trulicity | $707 | -24% | -5% | $345 | -6% | -1% |

| Rybelsus | $312 | -18% | -3% | $543 | +15% | +2% |

| Victoza | $8 | Flat | -68% | $78 | -48% | -34% |

| Total | $7,921 | 15% | +1% | $5,421 | 102% | +22% |

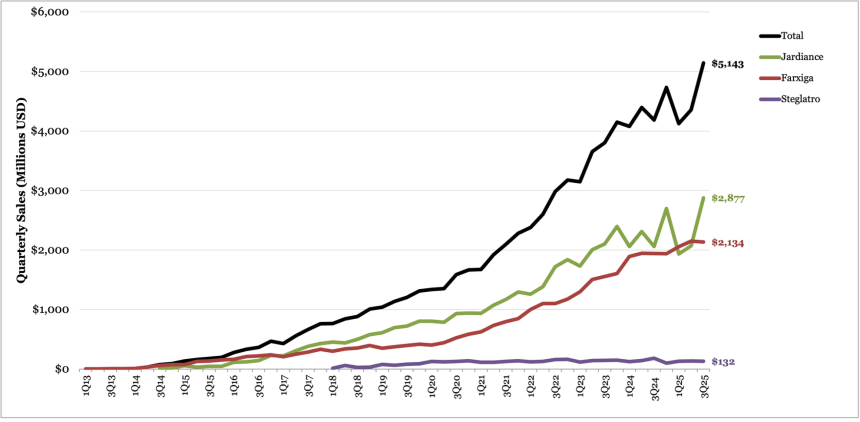

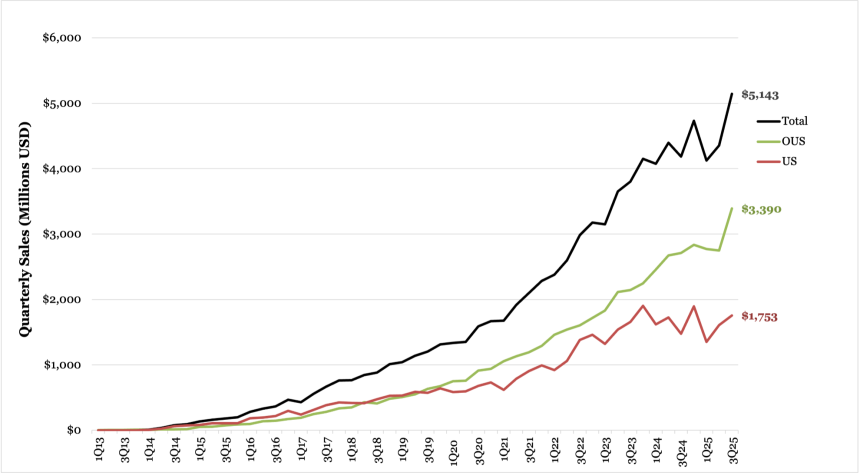

SGLT-2 Inhibitors

In 3Q25, SGLT-2 inhibitor sales totaled $5.1 billion, up 23% from 3Q24 (without Invokana) and up 18% sequentially. By geography, US sales totaled $1.8 billion (+19%, +9% Q/Q) and OUS sales totaled $3.4 billion (+25%, +23% Q/Q). The gap between US and OUS sales has increased over the years – US sales make up just 34% of sales in 3Q25, down from 37% in 2Q25. This is a shift from 2013-2016, when over 75% of SGLT-2 inhibitor sales came from the US. In comparison, GLP-1 RA sales in 3Q25 totaled $13.3 billion, 59% of which was from US revenue. Since we started tracking the SGLT-2 inhibitor market in 2013, SGLT-2 inhibitors have accumulated $92 billion in cumulative revenue, reflecting greater appreciation for the therapeutic class's benefits for glycemic, heart, and kidney health.

- Boehringer Ingelheim/Lilly’s Jardiance (empagliflozin) sales totaled $2.9 billion, up 40% from 3Q24 and up 39% sequentially. The therapy captured 56% market share, returning to the lead position after two quarters of Farxiga sale improvement. US sales totaled $1.3 billion, up 26% from 3Q24 and up 11% sequentially. OUS sales totaled $1.6 billion, up 53% from 3Q24 and up 74% sequentially.

- OUS sales include a $200 million sales-based milestone payment in 3Q25 from Boehringer Ingelheim. When excluding the milestone payment, Jardiance revenue totaled $759 million, up 10% from 3Q24 and 10% sequentially, and OUS sales totaled $335 million, down 5% from 3Q24 and up 8% sequentially.

- AstraZeneca’s Farxiga (dapagliflozin) revenue totaled $2.1 billion (+10%, -1% Q/Q) and captured 41% of market share. US sales of Farxiga totaled $441 million (+7%, +5% Q/Q), while OUS sales were $1.7 billion (+11%, -2% Q/Q). AZ attributed overall growth to increased global demand, primarily for the treatment of CKD and HF. The growth of the SGLT-2 inhibitor class overall is supported by cardiorenal guidelines, informed by trial‑proven reductions to HF hospitalizations, and the slowing of CKD progression.

- Farxiga continues to lead the class internationally, capturing 50% of the OUS market, while Jardiance captured 47%. Farxiga sales first surpassed Jardiance sales OUS in 1Q21 and the therapy has since continued to lead the class internationally.

- Sales for Merck’s Steglatro (ertugliflozin) totaled $132 million, down 28% from 3Q24 and down 3% sequentially. The therapy captured 3% market share. US revenue totaled $40 million, down 28% from 3Q24 and down 3% sequentially. OUS revenue totaled $92 million, down 28% from 3Q24 and down 2% sequentially.

- 3Q25 marked the eleventh quarter since J&J stopped reporting Invokana revenue, and we officially stopped estimating sales beginning in 1Q24. From 2013 to 2022, when sales were reported, Invokana totaled $7.9 billion. One of the patents for Invokana’s three indications expired April 11, 2025 according to the FDA’s Orange Book. This included indications for the treatment of T2D, reduction of MACE in people with T2D, and reduction of end-stage kidney disease in people with chronic kidney disease and T2D. Based on these changes to exclusivity, the generic launch of Invokana is expected on November 11, 2031.

- Since April 2023, Mark Cuban Cost Plus Drug Company has offered Invokana for sale. While initially priced at $235/month, the drug is now offered at $535/month. This cost is slightly lower than the drug’s retail price, which ranges from $584-669/month.

- Since June 2025, Theracos Bio’s Brenzavvy (bexagliflozin) has also been commercially available by prescription through the Mark Cuban Cost Plus Drug Company for $50 (not including shipping and handling) for a 30-day supply.

- Generic versions of SGLT-2 inhibitors will become available over the next few years, which is expected to increase access to these therapies. Recent publications have demonstrated that most people currently eligible for SGLT-2 inhibitors do not receive them. In November 2023, the FDA tentatively approved generic versions of two SGLT-2 inhibitors – dapagliflozin and canagliflozin – developed by Mumbai-based Lupin, which will likely launch once branded products begin to go generic.

- The patent for Farxiga’s indication for glycemic management in people with T2D, as well as in combination with exenatide, expired on October 4, 2025. It was first approved by the FDA in early 2014. Farxiga’s method of use patents for CKD extend as far as October 4, 2029, with additional renal patents extending through April 1, 2041 and July 18, 2039. Patent protections related to cardiovascular indications, including risk reduction for hospitalization due to heart failure, are expected to expire on September 9, 2040. Notably, since January 2024, AZ has partnered with Prasco to sell an authorized generic version of dapagliflozin.

- Jardiance’s compound patent is set to expire in 2029 in the US, in 2029 in Europe, and in 2030 in Japan. Jardiance has achieved multiple indications across glycemic, CVD, and kidney health, including chronic kidney disease in the US and the UK in September 2023, which has contributed to its strong prescription growth. The approval of Jardiance was based on EMPA-KIDNEY (n=6,609), the largest kidney outcomes trial using an SGLT-2 inhibitor.

- Steglatro’s patent is set to expire in 2030 in the US and in 2029 in the EU, China, and Japan. Although the therapy is currently only indicated for glycemic management, a phase 3 trial investigating Steglatro in youth with T2D was completed in April 2025. This is the second study of an SGLT-2 inhibitor in the pediatric population, following the publication of a phase 3 trial investigating AZ’s Farxiga in youth and young adults (ages 10-24 years) in The Lancet in April 2022. In future updates, we are curious if Merck will present results and seek regulatory approval for an indication that includes children.

We continue to wonder how progress in this drug class might be made for people with T1D, given that CKD affects 20-40% of people with T1D.[1] Few approved treatment options currently exist for people with T1D and CKD, and the broader SGLT inhibitor class may have limitations of use in people with T1D due to the risk of diabetic ketoacidosis (DKA). With adjunctive therapies and technologies like Abbott’s dual CGM-CKM, currently in development and discussed at ADA 2025, it is possible that expanded options may allow people with T1D to benefit from SGLT inhibitors safely.

Graph 6: SGLT-2 Inhibitor Sales (1Q13-3Q25)

Table 3: 3Q25 SGLT-2 Inhibitor Sales

| Global Revenue (Millions) | Global YOY Growth | Global Sequential Growth | Global Share of Market | |

| Jardiance (estimated Lilly+BI) | $959 ($2,877) | +40% | +39% | 56% |

| Farxiga | $2,134 | +10% | -1% | 41% |

| Steglatro (est.) | $132 | -28% | -3% | 3% |

| Total | $5,143 | +23% | +18% | -- |

Graph 7: SGLT-2 Inhibitor Sales by Geography (1Q13-3Q25)

Table 4: 3Q25 SGLT-2 Inhibitor Geography Breakdown

| 3Q25 US Revenue (Millions) | US YOY Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS YOY Growth | OUS Sequential Growth | |

| Jardiance (Lilly+BI estimated revenue) | $424 ($1,272) | +26% | +11% | $535 ($1,605) | +53% | +74% |

| Farxiga | $441 | +7% | +5% | $1,693 | +11% | -2% |

| Steglatro (est.) | $40 | -28% | -3% | $92 | -28% | -2% |

| Total | $1,753 | +19% | +9% | $3,390 | +25% | +23% |

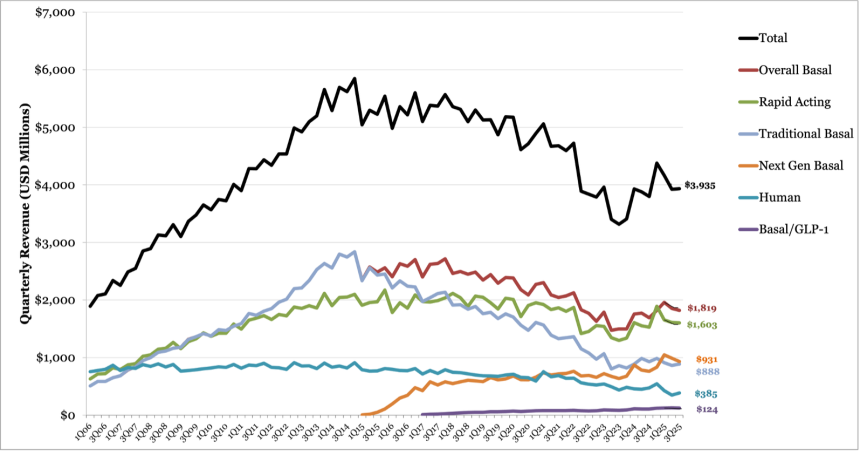

Insulin

Global insulin sales totaled $3.9 billion in 3Q25, up 4% from 3Q24 and flat sequentially. By geography, US revenue totaled $1.5 billion, up 10% from 3Q24 and 7% sequentially, and OUS revenue totaled $2.5 billion, up 1% from 3Q24 and down 4% sequentially. Since 2006, insulin has generated $340 billion in cumulative revenue.

- Basal insulin sales totaled $1.8 billion (+8%, -2% Q/Q). US sales totaled $598 million (+6%, -1% Q/Q), and OUS sales totaled $1.2 billion (+8%, -2% Q/Q). Next generation basal insulins, which include Toujeo, Tresiba, and Ryzodeg[1], totaled $931 million (+22%, -6% Q/Q), while traditional basal insulins, including Lantus, Levemir, and Basaglar, totaled $888 million (-4%, +3% Q/Q).

- Rapid acting insulin sales totaled $1.6 billion (+5%, -1% Q/Q). US sales totaled $743 million (+18%, +8% Q/Q) and OUS sales totaled $859 million (-5%, -7% Q/Q). Next-generation rapid-acting insulins, which include NovoMix, Apidra, Admelog, Fiasp, Afrezza, and Ryzodeg, totaled $457 million (+4%, -4% Q/Q). Traditional rapid-acting insulins – Novolog and Humalog – totaled $1.1 billion (+5%, +1% Q/Q).

- Human insulin sales totaled $385 million (-19%, +11% Q/Q). US sales totaled $196 million (-5%, +31% Q/Q) and OUS sales totaled $189 million (-29%, +27% Q/Q).

- Basal insulin/GLP-1 fixed ratio combinations contributed $124 million to the insulin market (+17%, -3% Q/Q). In the US, basal/GLP-1 RA sales totaled $16 million (+14%, flat Q/Q), and OUS sales totaled $109 million (+17%, -3% sequentially). We calculated the basal/GLP-1 RA contribution to the insulin market as 50% of the total sales for the class (with the other 50% contributing to the GLP-1 RA market).

In 3Q25, Novo Nordisk’s insulin portfolio captured 46% of global insulin sales, followed by Lilly (28%) and Sanofi (26%). These percent shares have remained generally consistent since 2006. In 3Q24, Novo Nordisk captured 47%, Lilly’s share remained the same, and Sanofi’s was 25%.

The inclusion of basal insulin Fiasp and NovoLog in the Medicare Drug Price Negotiation Program (MDPNP), with discounted prices (down 75% to $199/month), took effect on January 1, 2026. We are curious to see how this may affect Novo Nordisk’s revenue and market share. Moreover, the Most-Favored Nation negotiation includes Novo Nordisk’s NovoLog and Tresiba, which will be sold at a monthly list price of $35 to Medicaid/Medicare, down from ~$140 (down 75%) and $508 per month (down 93%), respectively. Sanofi’s insulins will also be sold at $35 per month at TrumpRx, down 65-93% from the original list price.

Table 5: Insulin Market 3Q25 Category Breakdown

| 3Q25 Revenue (Millions) | YOY Growth | Sequential Growth | |

| Basal | $1,819 | +8% | -2% |

| “Next Gen” Basal | $931 | +22% | -6% |

| “Traditional” Basal | $888 | -4% | +3% |

| Rapid-acting | $1,603 | +5% | -1% |

| “Next Gen” Rapid-acting | $457 | +4% | -4% |

| “Traditional” Rapid-acting | $1,146 | +5% | +1% |

| Human | $385 | -19% | +11% |

| Basal/GLP-1 | $124 | +17% | -3% |

| Total Insulin | $3,932 | +3% | flat |

Graph 8: Overall Insulin Sales by Category (1Q06-3Q25)

Table 6: Insulin Market 3Q25 Growth Geographic Breakdown

| 3Q25 US Revenue (Millions) | US YOY Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS YOY Growth | OUS Sequential Growth | |

| Basal | $598 | +6% | -1% | $1,222 | +8% | -2% |

| “Next-Gen” Basal | $189 | +37% | -16% | $742 | +19% | -3% |

| “Traditional” Basal | $409 | -4% | +8% | $479 | -5% | -2% |

| Rapid-acting | $743 | +18% | +8% | $859 | -5% | -7% |

| “Next-Gen” Rapid-acting | $123 | -60% | +35% | $334 | -8% | -13% |

| “Traditional” Rapid-acting | $620 | +12% | +4% | $526 | -2% | -3% |

| Human | $196 | -5% | +31% | $189 | -29% | flat |

| Basal /GLP-1 | $16 | +14% | -4% | $109 | +17% | -2% |

| Total | $1,553 | +10% | +7% | $2,375 | flat | -4% |

Graph 9: Overall Insulin Sales by Geography (1Q06 – 3Q25)

Graph 10: Overall Insulin Sales by Geography and Category (1Q06 – 3Q25)

Basal Insulin

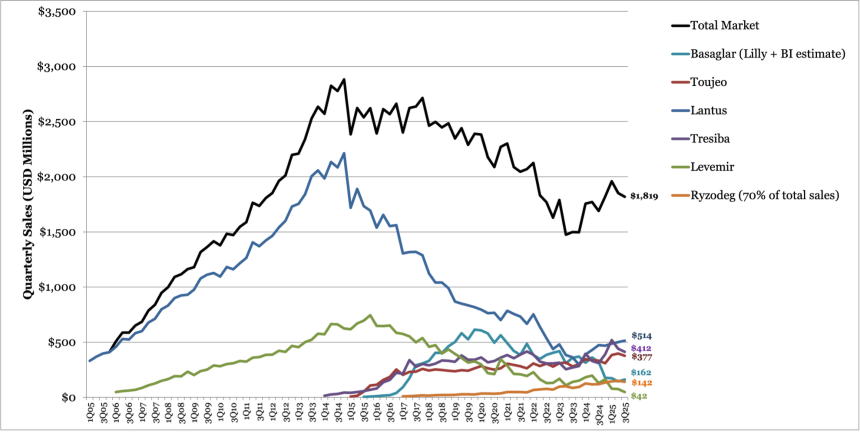

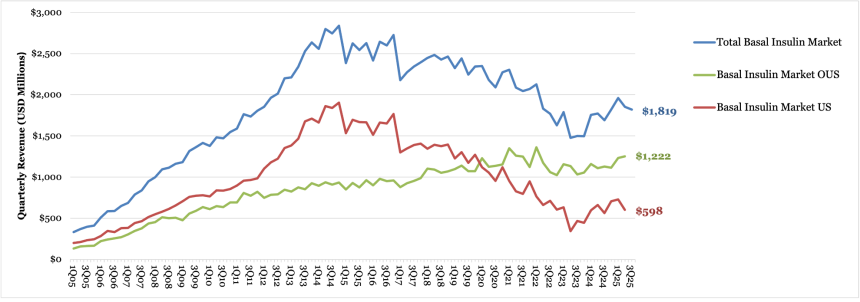

The basal insulin market totaled $1.8 billion in 3Q25 (+8%, -2% Q/Q). By geography, US sales totaled $598 million (+6%, -1% Q/Q), while OUS sales totaled $1.2 billion (+8%, -2% Q/Q). Next generation basal insulins totaled $931 million (+22%, -6% Q/Q), and traditional basal insulins totaled $888 million (-4%, +3% Q/Q). Since 1Q06, basal insulin sales have totaled $151 billion in cumulative revenue.

- Sales for Sanofi’s Lantus totaled $514 million in 3Q25, up 2% from 3Q24 and 3% sequentially, demonstrating steady growth after a period of decline beginning in early 2022. Sales in the US totaled $251 million (+22%, +8% Q/Q) and OUS sales totaled $263 million (-13%, -1% Q/Q). Since 2Q24, Lantus sales in the US increased by volume due to the “unavailability of a competing medicine,” which likely refers to Novo Nordisk’s Levemir. The therapy was discontinued in the US in December 2024. Levemir will also be discontinued in the UK by the end of 2026. Customer demand is expected to normalize in 2026 as windfall sales diminish.

- Sales for Novo Nordisk’s next-generation basal insulin Tresiba totaled $412 million in 3Q25 (+24% YOY, -6% Q/Q). Sales in North America totaled $124 million, up 106% from 3Q24 and down 43% sequentially. International sales totaled $288 million, up 6% YOY and down 3% sequentially. While Tresiba revenue in 3Q25 is down compared to 2Q25 and 1Q25 – the quarter that marked the first break in Tresiba’s overall growth trend since 1Q24 – growth remains strong following Levemir’s discontinuation in the US in December 2024. Moreover, Novo Nordisk announced plans in December 2024 to reduce US list prices for Fiasp and Tresiba by over 70% beginning in 2026.

- Sales for Sanofi’s next-generation basal insulin Toujeo totaled $377 million in the quarter, growing 6% from 3Q24 and down 5% sequentially. Sales in the US totaled $65 million, down 2% YOY and down 8% sequentially. International sales totaled $312 million, up 7% YOY but down 4% sequentially. Growth was attributed to increased sales in the Rest of World (+14% CER), where Toujeo continues to increase its share in the basal insulin market. In the US and EU, sales also increased (+7% CER in the US; +5% CER in the EU). In 3Q25, Toujeo captured the third largest global market share (21%), following Tresiba (23%) and Lantus (28%). Of note, Sanofi announced a $35/month price cap for all of its insulins (Toujeo, Lantus, and Soliqua) in the US in September 2025, regardless of insurance status. We’ll be interested to see how the expansion will impact uptake among other initiatives in its patient affordability program, the Insulins Valyou Savings Program.

- 3Q25 sales for traditional basal insulin Levemir totaled $49 million, down 63% YOY and down 34% sequentially. This is expected given that Novo Nordisk announced it would discontinue Levemir in the US in November 2023 due to constraints, formulary losses, and availability of alternative options. A full brand discontinuation, including the Levemir vial, went into effect on December 31, 2024.

- Novo Nordisk’s Awiqli (once-weekly insulin icodec) is approved in the EU, Switzerland, and Canada. In the US, approval remains pending, with Awiqli receiving a Complete Response Letter (CRL) from the FDA in July 2024. The CRL outlined requests related to the manufacturing process and the therapy’s T1D indication, which must be resolved before the review can proceed. Novo Nordisk did not mention further details on the status of Awiqli in the US in its past four quarterly reports.

- Lilly’s once-weekly insulin efsitora alfa was submitted for regulatory approval for T2D in the US in 3Q25. The submission was based on the phase 3 QWINT program, which investigated efsitora alfa compared to insulin glargine and insulin degludec. Full results of the QWINT-1, 3, and 4 trials were announced at ADA 2025, with QWINT-2 and 5 announced at EASD 2024. Notably, the QWINT-1 trial demonstrated non-inferior A1c reduction (1.3%) compared to insulin glargine (1.3%). The QWINT-3 trial also showed non-inferior A1c reduction (7.2%) compared to insulin degludec (7.3%) from a baseline of 7.8%. For QWINT-4, no significant difference was seen in A1c reduction by insulin efsitora alfa (1.07%) or insulin glargine (1.07%).

- Weekly basal insulin may shift the paradigm of basal insulin treatment for T2D, allowing patients to avoid a significant number of injections per day. Lilly also submitted insulin efsitora alfa for regulatory approval in the EU in 2Q25.

Table 7: 3Q25 Basal Insulin Sales

| 3Q25 Revenue (Millions) | YOY Growth | Sequential Growth | Share of Market | |

| Basaglar (BI + Lilly estimate) | $324 | flat | +12% | 18% |

| Toujeo | $377 | +6% | -5% | 21% |

| Lantus | $514 | +2% | +7% | 28% |

| Tresiba | $412 | +24% | -6% | 23% |

| Levemir | $49 | -63% | -34% | 3% |

| Ryzodeg | $203 | +18% | -5% | 7% |

| Total | $1,819 | +8% | -2% | -- |

Graph 11: Basal Insulin Sales (1Q05 – 3Q25)

Table 8: Basal Insulin Sales 3Q25 Geographic Breakdown

| 3Q25 US Revenue (Millions) | US YOY Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS YOY Growth | OUS Sequential Growth | |

| Basaglar (BI + Lilly estimate) | $80 | -6% | +18% | $82 | +8% | +6% |

| Toujeo | $65 | -2% | -8% | $312 | +7% | -4% |

| Lantus | $251 | +22% | +8% | $263 | -13% | -1% |

| Tresiba | $124 | +106% | -43% | $288 | +6% | -3% |

| Levemir | -- | -105% | -- | $53 | -23% | -21% |

| Ryzodeg | -- | N/A | -- | $203 | +18% | -5% |

| Total | $598 | +6% | -1% | $1,222 | +8% | -2% |

Graph 12: Basal Insulin Sales by Geography (1Q05 – 3Q25)

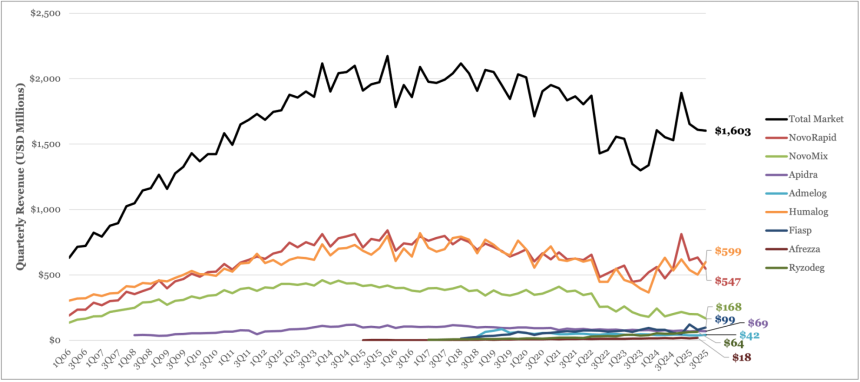

Rapid-Acting Insulin

The rapid-acting insulin market totaled $1.6 billion in 3Q25, up 5% from 3Q24 and down 1% sequentially. US sales totaled $742 million, 18% YOY and up 8% sequentially. OUS sales totaled $859 million, down 5% YOY and down 7% sequentially.

- Lilly’s Humalog and Novo Nordisk’s NovoLog continued to lead the class, capturing 37% and 34% of the market, respectively. Combined sales for Humalog and generic insulin lispro totaled $599 million in 3Q25, up 12% from 3Q24 and up 19% sequentially. US sales totaled $387 million, up 20% from 3Q24 and up 27% sequentially. OUS sales totaled $212 million, up 1% from 3Q24 and up 7% sequentially. NovoLog sales totaled $547 million, down 2% CER and down 14% sequentially. By geography, US sales totaled $233 million, up 5% CER and down 21% sequentially. OUS sales totaled $313 million, down 7% CER and down 8% sequentially.

- Sales of MannKind’s inhaled insulin Afrezza totaled $18.5 million, up 10% YOY and up 5% Q/Q, continuing to capture 1% of the market. This growth was primarily driven by increased support among T1D prescribers, with new prescriptions rose 31% in 3Q25 and total prescriptions increasing 27% from 3Q24, reflecting Afrezza’s expanded presence among providers. As a reminder, in 2Q25, the company announced that it submitted a supplemental Biologics License Application (sBLA) for Afrezza in pediatrics, based on data from the INHALE-1 study in children aged 4-17, which was accepted by the FDA in October 2025.

- Generic and biosimilar competition is also increasing, and we imagine that this will affect sales. Biocon Biologic’s Kirsty received FDA approval in July 2025, marking the first and only interchangeable biosimilar to Novo Nordisk’s rapid-acting insulin NovoLog (insulin aspart). In February 2025, the FDA approved Sanofi’s Merilog (insulin aspart-szjj) as the first biosimilar to NovoLog. In the pipeline, Adocia and Tonghua Dongbao’s BioChaperone Lispro (ultra-rapid insulin) continues to advance, demonstrating non-inferiority in A1c reduction compared to Humalog, in phase 3 trials.

Table 9: 3Q25 Rapid-Acting Insulin Sales

| Revenue (Millions) | YOY Growth | Sequential Growth | Share of Market | |

| NovoLog | $547 | -2% | -14% | 34% |

| Humalog | $599 | +12% | +19% | 37% |

| NovoMix | $168 | -17% | -16% | 10% |

| Apidra (est.) | $69 | -5% | -5% | 4% |

| Fiasp | $99 | +67% | +22% | 6% |

| Admelog (est.) | $42 | -5% | +10% | 3% |

| Ryzodeg | $61 | +18% | -5% | 4% |

| Afrezza | $19 | +10% | +5% | 1% |

| Total | $1,602 | +5% | -1% | -- |

*Ryzodeg revenue is split 70/30 between basal insulin/rapid-acting insulin. Revenue for Admelog and Apidra are estimated using YOY for Sanofi’s “other diabetes” portfolio and the US vs. OUS revenue ratio from 4Q20.

Graph 13: Rapid Acting Insulin Sales (1Q06 – 3Q25)

Table 10: 3Q25 Rapid-Acting Insulin Sales Geographic Breakdown

| 3Q25 US Revenue (Millions) | US YOY Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS YOY Growth | OUS Sequential Growth | |

| NovoLog | $233 | +5% | -21% | $313 | -7% | -8% |

| NovoMix | $23 | +61% | +14% | $144 | -23% | -20% |

| Humalog | $387 | 19% | 27% | $212 | +1% | 7% |

| Apidra (est.) | $7 | -5% | -5% | $62 | -5% | -5% |

| Admelog (est.) | $38 | -5% | +10% | $4 | -5% | +10% |

| Fiasp | $37 | 3,600% | +235% | $62 | -1% | -11% |

| Afrezza | $18 | +1% | +23% | -- | -- | -- |

| Ryzodeg | -- | -- | -- | $61 | +19% | -6% |

| Total | $743 | +18% | 8% | $859 | -5% | -7% |

**MannKind’s Afrezza is marketed in Brazil, following approval in June 2019, but the company does not break out Afrezza revenue in Brazil. The vast majority of Afrezza’s revenue is thought to come from the US, so we have not listed international revenue here.

Graph 14: Rapid Acting Insulin Sales by Geography by Quarter (1Q06 – 3Q25)

Basal Insulin/GLP-1 RA Fixed Ratio Combination

In 3Q25, revenue for Novo Nordisk’s Xultophy (degludec/liraglutide) and Sanofi’s Soliqua (glargine/lixisenatide) totaled $124 million, up 17% from 3Q24 and down 2% sequentially. By geography, US sales totaled $15 million, up 14% YOY and 4% sequentially. OUS revenue was $105 million, up 17% YOY and down 2% sequentially.

- Following trends from past quarters, Xultophy continued to lead the market in 3Q25, with 71% market share, up 1% sequentially from 2Q25. Sanofi’s Soliqua accounted for the remaining 29% with $36 million in sales.

- Considering the overwhelming success of semaglutide and other incretin-based therapies, we believe that many patients could benefit from this fixed-dose combination therapy. Studies have shown that combination therapy may help minimize adverse side effects (including weight gain) that are often seen with insulin therapy. Further, combination therapy may provide more clinically robust improvements in A1c, help HCPs facilitate treatment intensification, and improve treatment adherence.

- Results from the phase 4 SOLI-SWITCH study (n=162) presented at ATTD 2025 support such uses, demonstrating that Soliqua reduced A1c by 1.2% at Week 24 from a mean baseline of 8.5%. Moreover, 38% of participants achieved an A1c <7.0% and saw a median body weight reduction of 0.9 kg (2 lbs). Read more about fixed-ratio basal insulin/GLP-1 RA in Sanofi’s industry symposium at ATTD 2025.

Table 11: 3Q25 Basal Insulin/GLP-1 Receptor Agonist Combination Sales

| Revenue (Millions) | Growth | Sequential Growth | Share of Market | |

| Soliqua | $36 | +20% | -6% | 29% |

| Xultophy | $88 | +15% | -1% | 71% |

| Total | $124 | +17% | -2% | -- |

Graph 15: Basal Insulin/GLP-1 Receptor Agonist Combination Sales (1Q17 – 3Q25)

Table 12: 3Q25 Basal Insulin/GLP-1 Receptor Agonist Combination Geographic Breakdown

| 3Q25 US Revenue (Millions) | US Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS Growth | OUS Sequential Growth | |

| Soliqua | $11 | +19% | -5% | $25 | +21% | -7% |

| Xultophy | $4 | +1% | -2% | $84 | +16% | -2% |

| Total | $15 | +14% | +4% | $109 | +17% | -2% |

Graph 16: Basal Insulin/GLP-1 Receptor Agonist Combination by Geography (1Q17 – 3Q25)

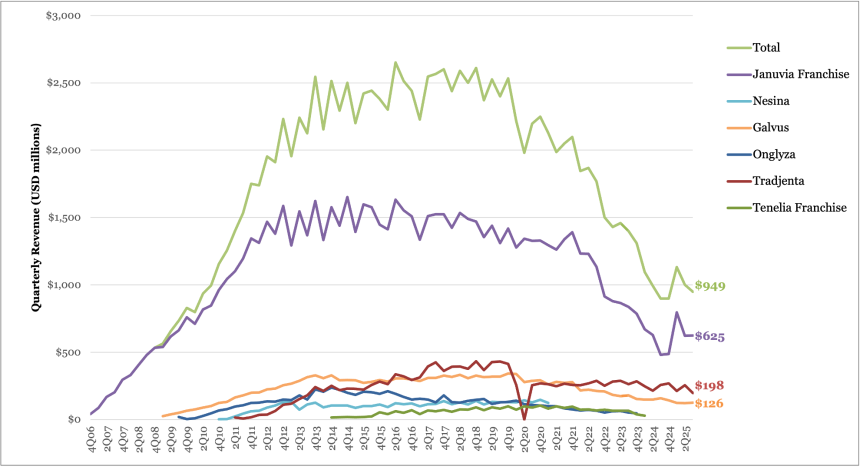

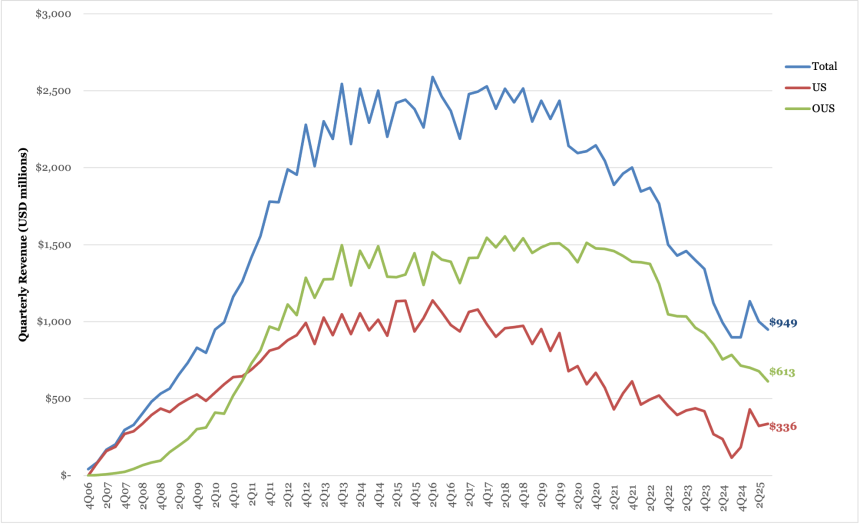

DPP-4 Inhibitors

In 3Q25, DPP-4 inhibitor sales totaled $949 million, up 6% from 3Q24 and down 5% sequentially. US revenue reached $336 million (+194%, +4% sequentially) and OUS revenue totaled $613 million (-22%, -10% sequentially). Overall declines in DPP-4 inhibitors are thought to be partly driven by competition from other oral agents, such as SGLT-2 inhibitors, which are recommended by the ADA as a first-line therapy for people with diabetes and higher comorbidity risks. In a recent survey from dQ&A (n=2,796), just 9% of patients with T2D on oral diabetes therapies were also taking a DPP-4 inhibitor.

- Merck’s Januvia franchise, which includes Januvia (sitagliptin) and Janumet (fixed-dose sitagliptin + metformin), continued to hold the greatest DPP-4 inhibitor market share in the field, which increased slightly to 66%. The Januvia franchise totaled $625 million, up a remarkable 107% from 3Q24 and flat sequentially. US sales totaled $336 million, up 310% from 3Q24 and up 18% sequentially. OUS sales totaled $289 million, down 28% from 3Q24 and down 15% sequentially.

- Merck attributed the sharp increase in sales in the US to higher net pricing in the US. Offsetting this growth, Merck said that international declines were explained by lower demand for the therapies in international markets due to generic competition, especially China. Generic versions of Januvia and Janumet are expected to enter the US market in May 2026 following patent expiration in China and Europe. Off-patent DPP-4 inhibitors include Tradjenta, Galvus, and Onglyza, with more patent expirations imminent.

- BI/Lilly’s Tradjenta estimated revenue totaled $198 million (-22%, -22% Q/Q), capturing 21% of market share. No US sales were reported this quarter by Lilly. Lilly’s partner BI, who is responsible for US sales, is private and has not publicly reported sales for Tradjenta. OUS sales totaled $198 million, down 11% from 3Q24 and down 9% sequentially.

- Novartis’s Galvus (vidagliptin), which is only available in internationally, followed Tradjenta with sales of $126 million (-21%, +2% Q/Q) and 13% market share. Management attributed the decline to continued generic competition.

- For other therapies, recall that Daiichi Sankyo stopped reporting sales of DPP-4 inhibitors Tenelia (teneligliptin) in 3Q24, and AstraZeneca permanently discontinued Onglyza (saxagliptin) in March 2023 due to a “business decision,” presumably related to now-resolved lawsuits and patent expirations in 2023.

DPP-4 inhibitors may still have an important role in diabetes management and perhaps even in diabetes prevention for select populations. In the VERIFY trial, early combination therapy with a DPP-4 inhibitor and metformin led to 26 more months with an A1c value ≤7.0% compared to metformin monotherapy.

Table 13: 3Q25 DPP-4 Inhibitor Sales

| 3Q25 Revenue (Millions) | Growth | Sequential Growth | Share of Market | |

| Merck’s Januvia Franchise | $625 | 107% | Flat | 66% |

| Tradjenta (estimated Lilly + BI) | $198 | -22% | -22% | 21% |

| Novartis’ Galvus | $126 | -21% | +2% | 13% |

| Total | $949 | +6% | -5% | -- |

Graph 17: DPP-4 Inhibitor Total Sales by Company (4Q06 – 3Q25)

*Onglyza is no longer included in our graph as AZ stopped reporting revenue in 1Q24. Recall that onglyza was discontinued in the US in March 2023.

Table 14: 3Q25 DPP-4 Inhibitor Geographic Breakdown

| 3Q25 US Revenue (Millions) | US Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS Growth | OUS Sequential Growth | |

| Merck’s Januvia Franchise | $336 | +310% | +18% | $289 | -28% | -15% |

| Tradjenta (estimated Lilly + BI) | $0 | -- | -- | $198 | -11% | -9% |

| Novartis’ Galvus | $0 | -- | -- | $126 | -21% | +2% |

| Total | $336 | +194% | +4% | $613 | -22% | -10% |

Graph 18: DPP-4 Inhibitor Sales by Geography (4Q06 – 3Q25)

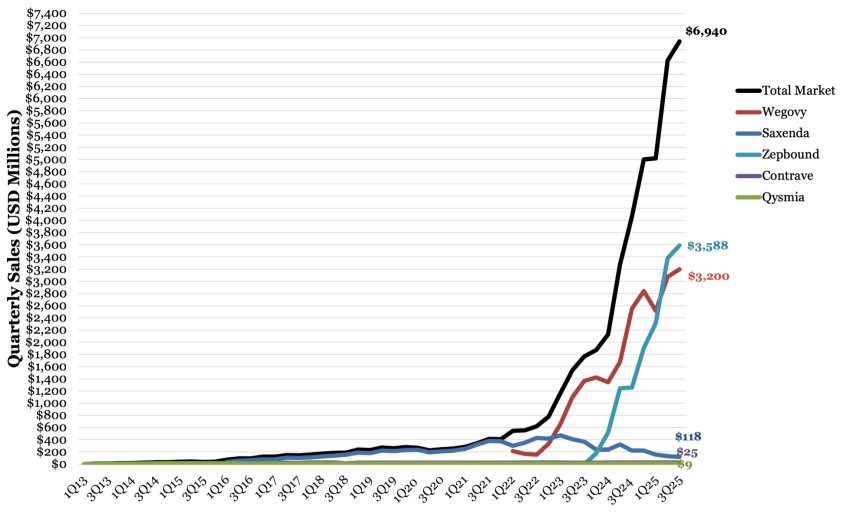

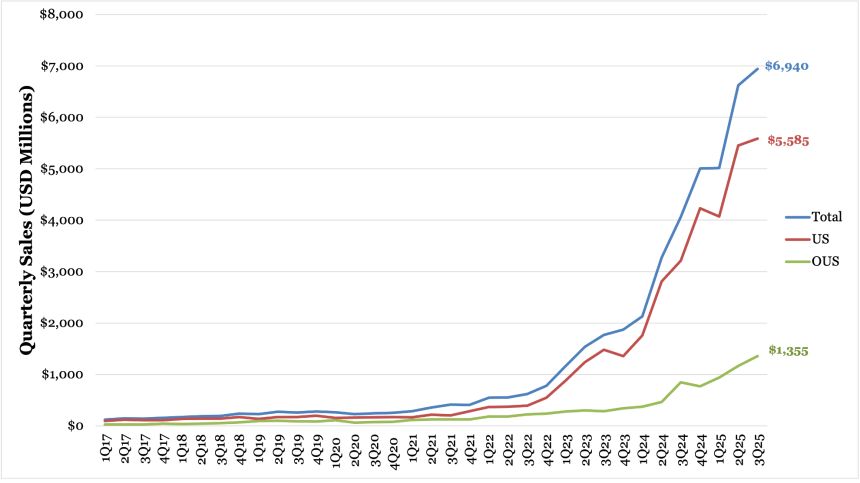

Obesity

In 3Q25, the obesity market totaled more than $6.9 billion, up 71% from 3Q24 and up 5% sequentially. US sales totaled $5.5 billion, up 73% from 3Q24 and up 34% sequentially. OUS sales totaled $1.3 billion, up 74% from 3Q24 and up 2% sequentially. Since 2006, the obesity market has generated $49.3 billion in cumulative revenue.

- For the second quarter in a row, Lilly’s Zepbound (tirzepatide for obesity) surpassed Novo Nordisk’s Wegovy (semaglutide for obesity) by both revenue and prescriptions. Zepbound totaled $3.6 billion, up 3x from 3Q24 and up 6% sequentially, capturing more than half (52%) of global sales. Since its approval in November 2023 and US launch in 4Q23, Zepbound sales recorded $10.8 billion in cumulative revenue. In its third quarter of launch in OUS markets, sales for Zepbound totaled $20 million, up more than 10x from 2Q25. Zepbound has also maintained its leadership in the US obesity market since 1Q25, capturing 63% of total prescriptions (TRx) and 71% of new-to-brand prescriptions (NBRx) at the end of 3Q25. In comparison, Zepbound captured 66% of TRx and over 68% of NBRx at the end of 2Q25.

- On insurance, management attributed the slight decrease in TRx share to the CVS Caremark’s decision in July 2025to select Novo Nordisk’s Wegovy as its preferred GLP-1 RA for obesity on its template formularies. Nevertheless, the increase in NBRx reflects continued demand for Zepbound despite coverage shifts in the quarter under study.

- Both Optum Rx (affiliated with UnitedHealth Group) and Express Scripts (affiliated with Cigna), maintain access to both drugs. In addition, new pharmacy benefit programs, like Evernorth (affiliated with Cigna) have a cap of $200 in monthly out-of-pocket costs for Wegovy and Zepbound.

- In the cash channel, Zepbound vials, sold at discounted cash prices on LillyDirect, accounted for almost 30% of TRx (over one million prescriptions) and over 45% of new prescriptions in 3Q25. These numbers reflect an increase from 2Q25, when vials accounted for 20% of TRx and 35% of NBRx. As background, LillyDirect was launched in the US in January 2024 and provides direct home delivery of prescription medications for diabetes, obesity, and migraines. With the launch of 12.5 mg and 15 mg doses of Zepbound vials in June 2025, patients who refill within 45 days of their first order can access Zepbound at $349/month for 2.5 mg and $499/month for subsequent doses (5 mg, 7.5 mg, 10 mg, 12.5 mg, and 15 mg).

- On insurance, management attributed the slight decrease in TRx share to the CVS Caremark’s decision in July 2025to select Novo Nordisk’s Wegovy as its preferred GLP-1 RA for obesity on its template formularies. Nevertheless, the increase in NBRx reflects continued demand for Zepbound despite coverage shifts in the quarter under study.

- Wegovy (semaglutide for obesity) captured 46% of the obesity market in 3Q25. While Wegovy’s market share growth was flat from 2Q25 at 46%, it decreased from 50% in 1Q25, 57% in 4Q24, and 51% in 2Q24 due to Lilly’s Zepbound gradually capturing a greater market share. Wegovy sales totaled $3.2 billion in 3Q25, up 18% from 3Q24 and up 4% sequentially. Wegovy has now launched in more than 45 countries, an increase from 35 countries in 2Q25 and 25 countries in 1Q25. In the US, there were 270,000 weekly prescriptions in 3Q25 (down from 280,000 in 2Q25), and 2.5x volume growth of the branded obesity market in the US.

- Given the lower-than-anticipated sales and business developments, Novo Nordisk revised the 2025 guidance four times. In 3Q25, Novo Nordisk said the sales growth for 2025 is expected to be 8-11%, on the lower end of the former expectation of 8-14% announced in 2Q25 and a nearly 11 percentage point reduction from the original guidance of 16-24% from January 2025. In addition, operating profit growth for 2025 is expected at 4-7% (down from 4-10%).

- On accessibility, Novo Nordisk continues to increase options for insured and cash channels. As a reminder, NovoCare Pharmacy, launched in March 2025, is a direct-to-patient platform that offers Wegovy single-dose pens for $499/month for cash-paying patients. Novo Nordisk also announced partnerships with telehealth platforms, including Ro and LifeMD, in April 2025, as well as GoodRx and Costco to further expand access. Wegovy prescriptions via NovoCare Pharmacy, including telehealth collaborations, total ~10,000 weekly prescriptions (flat from 2Q25), in addition to 16,000 weekly prescriptions (down from 17,000 in 2Q25) in the retail cash channel. In 3Q25, management shared that the cash market accounts for ~10% of total Wegovy prescriptions. The low penetration in the cash channel was attributed to the compounding business in 2Q25.

- On the insured channel, Wegovy has coverage for about 55 million people with obesity in the US, aligning with the coverage reported in the past four quarters. In addition, more than 10 million people are estimated to have coverage through Medicaid, which includes people with obesity and weight-related comorbidities like cardiovascular disease. However, due to increased healthcare expenditures, several states, including California, North Carolina, Pennsylvania, Connecticut, and Michigan, announced plans to end or scale back coverage of Wegovy. In October 2025, Novo Nordisk announced that it lobbied to maintain Medicaid reimbursement for Wegovy across 14 US states.

- As a reminder, for commercial payers, in May 2025, CVS Caremark selected Wegovy as the preferred obesity treatment on its commercial template formularies, effective July 2025. Management expects the exclusivity of Wegovy as the branded medication at CVS to continue in 2026.

- Generic semaglutide has emerged this year. Novo Nordisk’s semaglutide lost its data exclusivity in Canada earlier this month, on January 4th. Given that its patent, which granted Novo Nordisk exclusive rights to manufacture and sell semaglutide in Canada, lapsed in 2020, generic companies like Sandoz and Hims & Hers can file for regulatory approval for generics.

- Oral Wegovy, received FDA approval in December 2025 for weight loss, based on the phase 3 OASIS-4 (n=307) and SELECT trials (n=17,604). In OASIS-4, oral semaglutide 25 mg conferred up to 14% weight loss compared to 2% with placebo and in the SLECT trial, injectable semaglutide 2.4 mg reduced major adverse CV events (MACE) risk by 20% at Week 104 in people with obesity or who were overweight, but without diabetes. Earlier this month, Novo Nordisk launched the oral pill in more than 70,000 pharmacies in the US, including CVS and Costco, and select telehealth providers, such as NovoCare Pharmacy, Ro, LifeMD, Weight Watchers, and GoodRx. Following the launch, Amazon announced that the oral pill is available on its digital pharmacy platform Amazon Pharmacy, further increasing options for convenient access to this new formulation.

- Sales for Novo Nordisk’s Saxenda (liraglutide for obesity) totaled $118 million in 3Q25, down 50% from 3Q24 and down 11% sequentially. US sales totaled $14 million, up 8% from 3Q24 and down 8% sequentially. OUS sales totaled $104 million, down 51% from 3Q24 and down 11% sequentially. As Wegovy and Zepbound continue to dominate the obesity market, Saxenda captured less than 2% in 3Q25, down from 5% in 2Q24.

- In the pipeline, several candidates for obesity continue to advance. Following the full phase 3 REDEFINE 1 trial readout at ADA 2025, Novo Nordisk plans to file CagriSema (fixed combination of cagrilintide 2.4 mg and semaglutide 2.4 mg) for FDA approval early this year. In 3Q25, management reiterated that the REDEFINE 4 trial was amended based on learnings from the REDEFINE 1 trial, with a base case of noninferiority and upside potential for superiority against Lilly’s Zepbound. Even if REDEFINE 4 does not show statistically significant superiority on weight loss, Novo Nordisk still sees CagriSema as a differential candidate with benefits on gastrointestinal tolerability and cardiovascular outcomes, given evidence from REDEFINE 3. In July 2025, the company submitted high-dose Wegovy (semaglutide 7.2 mg) to the EU based on phase 3 STEP UP trial. In October 2025, the company also submitted a variant application for semaglutide 7.2 mg in a single-dose pen. This submission is based on the STEP UP and STEP UP T2D program presented at ADA 2025, in which semaglutide 7.2 mg achieved up to 21% weight loss across several trials. Novo Nordisk expects a regulatory decision for semaglutide 7.2 mg early this year and approval of semaglutide 7.2 mg in a single-dose pen in 2H26.

- In 3Q25, Lilly shared results of the phase 3 ATTAIN-2 trial of oral GLP-1 RA orforglipron in people with obesity or overweight with T2D. These results follows data from the ATTAIN-1 trial of oral GLP-1 RA, orforglipron, announced in 2Q25, which demonstrated 12% weight loss in people with obesity or overweight. The company has completed the necessary steps to initiate global regulatory filings for the obesity indication with the completion of the ATTAIN-2 trial. Filings are set to begin imminently, with a launch expected this year.

- Innovent Biologics’ dual GLP-1/glucagon RA mazdutide (4 mg and 6 mg) was approved in China for weight management in June 2025. BI/Zealand continues to evaluate dual glucagon/GLP-1 RA survodutide in phase 3 SYNCRHONIZE program. Topline results of the phase 3 SYNCRHONIZE-1 (n=727) and SYNCHRONIZE-2 trials (n=756) for people with overweight or obesity without or with T2D, respectively, are expected in 1H26. Meanwhile, dual GLP-1/GLP-2 RA dapiglutide development was discontinued in 3Q25 due to an “increasingly crowded” incretin-based therapy landscape.

- A growing number of candidates target improved weight‑loss quality by limiting lean‑mass loss. At EASD 2025 Regeneron shared results from the phase 2 COURAGE trial (n=1,005), assessing trevogrumab (anti‑GDF8/anti‑myostatin), alone or paired with garetosmab (anti‑activin A), as an add‑on to Novo Nordisk’s semaglutide in adults with obesity. The analysis showed that trevogrumab, with or without garetosmab, preserved about 50-80% of the lean mass typically lost with semaglutide alone. Lilly’s phase 2 trial of bimagrumab (activin receptor antagonist) was discontinued in September 2025 due to “strategic business reasons.” Scholar Rock’s apitegromab (promyostatin and latent myostatin inhibitor) reduced lean mass loss by 55% at Week 24, compared to tirzepatide alone, in people with overweight or obesity in the phase 2 EMBRAZE trial (n=87) announced in June 2025, but no new updates were given in 3Q25.

Graph 19: Anti-Obesity Medication Total Sales (1Q13 – 3Q25)

Table 15: 3Q25 Anti-Obesity Medication Sales

| Revenue (Millions) | YOY Reported Growth | Sequential Reported Growth | Share of Market | |

| Wegovy | $3,200 | +18% | +4% | 46% |

| Zepbound | $3,588 | +185% | +6% | 52% |

| Saxenda | $118 | -50% | -11% | 2% |

| Contrave (est.) | $25 | N/A | N/A | Flat |

| Qsymia (est.) | $9 | N/A | N/A | Flat |

| Total (est.) | $6,940 | +71% | +5% | -- |

Table 16: 3Q25 Anti-Obesity Medication Geographic Breakdown

| 3Q25 US Revenue (Millions) | US YOY Reported Growth | US Sequential Growth | 3Q25 OUS Revenue (Millions) | OUS YOY Reported Growth | OUS Sequential Growth | |

| Wegovy | $1,970 | +6% | -3% | $1,230 | +62% | +17% |

| Zepbound | $3,568 | +84% | +6% | $20 | N/A | +1,220% |

| Saxenda | $14 | +1% | -8% | $104 | -53% | -11% |

| Contrave (est.) | $25 | Flat | Flat | Flat | -- | -- |

| Qsymia (est.) | $9 | Flat | Flat | Flat | -- | -- |

| Total (est.) | $5,585 | +73% | +34% | $1,355 | +74% | +2% |

Graph 20: Anti-Obesity Medication Geographic Sales (1Q17 – 3Q25)

Glucagon

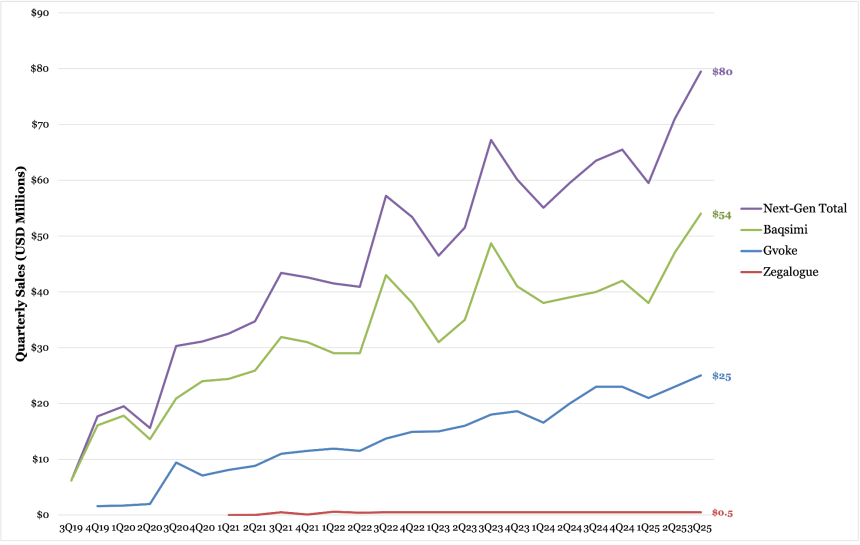

In 3Q25, ready-to-use glucagon sales totaled $80 million, up 25% from 3Q24 and up 13% sequentially. Growth was driven by Amphastar’s Baqsimi ($54 million, +33%), followed by Xeris’s Gvoke ($25 million, +10%). According to the ADA, approximately 8.4 million people with diabetes in the US take insulin or sulfonylureas and are thus at risk of severe hypoglycemia. Glucagon products can be lifesaving medications for patients experiencing severe hypoglycemia.

- Amphastar’s Baqsimi sales totaled $54 million in 3Q25, up 33% from 3Q24 and up 14% sequentially. As the only FDA-approved non-injectable, nasal glucagon for severe hypoglycemia, Baqsimi captures 68% of the next-generation glucagon market. Notably, Amphastar took full control of Baqsimi from Lilly in 1Q25. 3Q25 was the second consecutivequarter in which Baqsimi’s revenue exceeded the peak quarterly sales reported under Lilly’s ownership ($43 million in 3Q22).

- The company expects the market to grow steadily, as the percentage of glucagon prescriptions among people on insulin has increased from 10% in 2023 to 12% today. Peak sales are forecasted to be $250-$270 million.

- Xeris’s Gvoke revenue totaled $25 million in 3Q25, up 10% from 3Q24 and up 7% sequentially. Sales resulted from an increase in Gvoke prescriptions (~68,000), down 3% from 3Q24 and up 5% sequentially. The company continues to educate patients and providers to increase the uptake broadly, with even more who could benefit from ready-to-use glucagon, Xeris captured ~32% of the ready-to-use glucagon market.

Graph 21: Ready-to-Use Glucagon Sales (3Q19 – 3Q25)

Table 17: 3Q25 Ready-to-Use Glucagon Sales

| 3Q25 Revenue (Millions) | YOY Growth | Sequential Growth | Share of Ready-to-Use Market (by revenue) | |

| Baqsimi | $54 | +15% | +15% | 68% |

| Gvoke | $25 | +8% | +8% | 31% |

| Zegalogue (est.) | $0.5 | - | - | 1% |

| Total | $80 | +25% | +13% | -- |

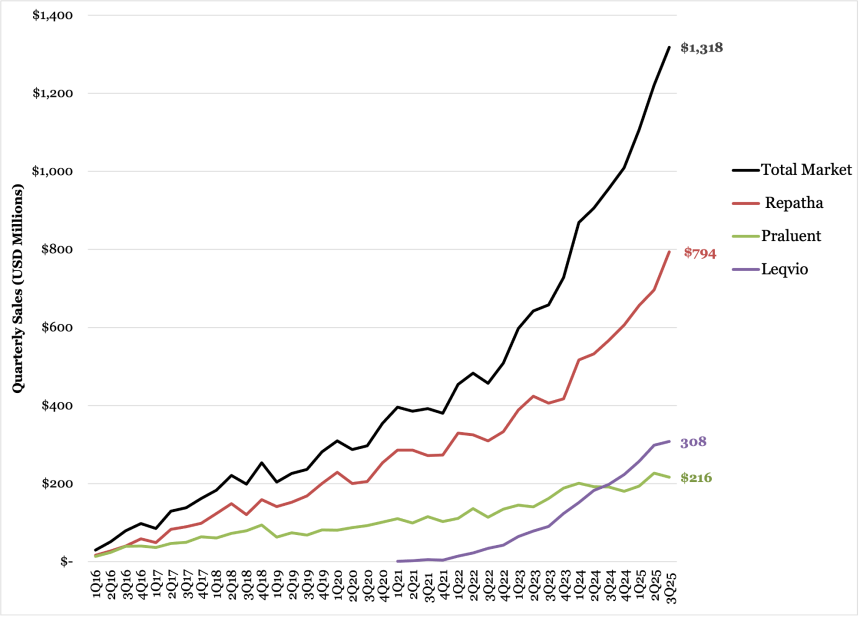

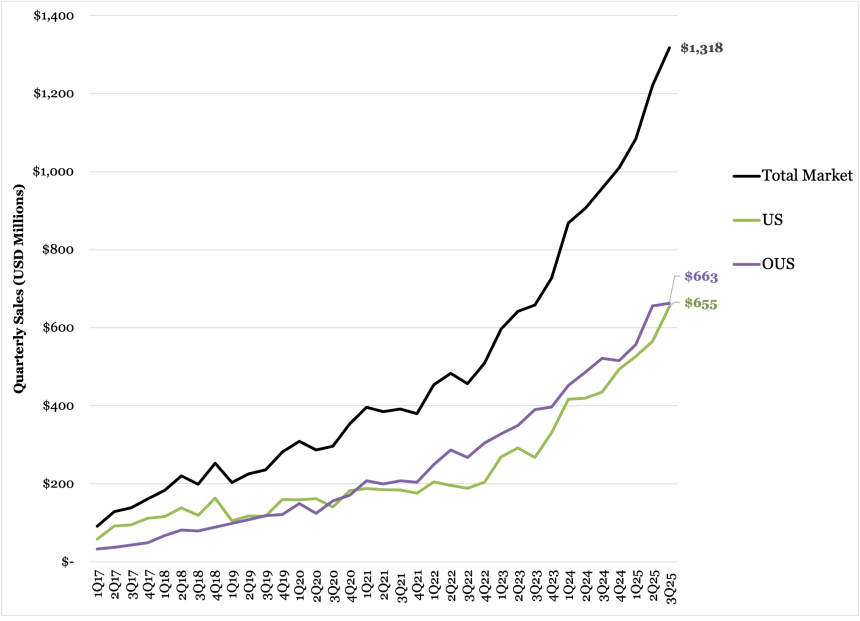

PCSK9 Inhibitors

In 3Q25, the PCSK9 inhibitor market totaled $1.3 billion, up 38% from 3Q24 and up 8% sequentially. In the US, sales totaled $655 million, up 51% from 3Q24 and up 16% sequentially. The OUS market totaled $663 million, up 27% from 3Q24 and up 1% sequentially.

- Amgen’s Repatha (evolocumab) captured 60% of the market (up from 57% in 2Q25), with the revenue of $794 million, up 40% from 3Q24 and up 14% sequentially. US sales totaled $442 million, up 57% from 3Q24 and 22% sequentially, while OUS sales totaled $352 million, up 23% from 3Q24 and 5% sequentially.

- In the landmark VESALIUS-CV trial (n=12,257), presented at AHA 2025, PCSK-9 inhibitor Repatha (evolocumab) lowered LDL-c by 55% compared to placebo at Week 48 in people with diabetes and/or atherosclerosis. Moreover, evolocumab lowered the risk of all-cause mortality by 20% and MACE-3 by 25%. Specifically in people with diabetes but not atherosclerosis, evolocumab led to 29% reduction in MACE-3. This finding supports low LDL-c goals (<55 mg/dL) in people with diabetes or early-stage atherosclerosis, changing the treatment paradigm.

- In the pipeline, the ongoing phase 4 EVOLVE-MI study (n=6,017) investigates Repatha administered within 10 days of acute MI to reduce the risk of CV events. The trial is expected to complete in May 2027.

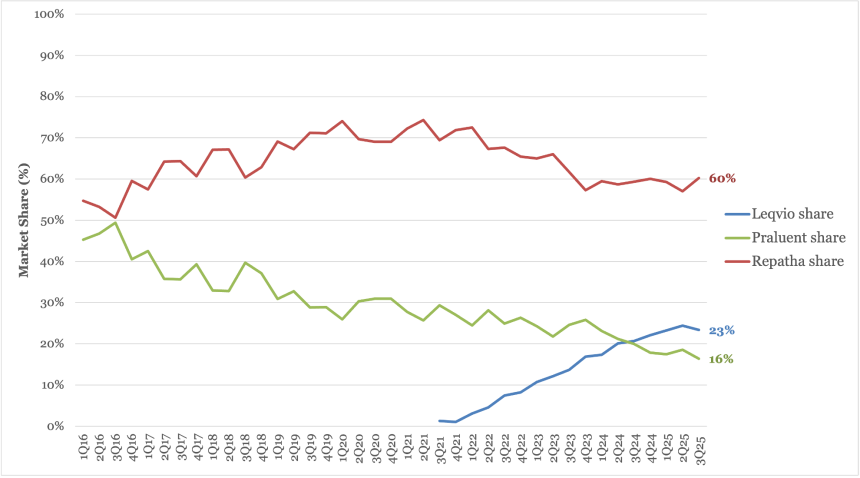

- Novartis’s infusion-based Leqvio (inclisiran) captured 23% of the market in 3Q25 (down from 24% in 2Q25). Sales totaled $308 million in 3Q25, up 23% from 3Q24 and up 3% sequentially. In the US, sales totaled $146 million, up 45% from 3Q24 and up 6% sequentially, and OUS sales totaled $162 million, up 67% CER from 3Q24 and up 1% sequentially. The continued increase in prescription (+44%) in the US drove the growth, as well as “out-of-pocket” market expansion in China. Novartis continues to launch Leqvio in OUS markets. Leqvio is commercially available in 87 countries.

- In the pipeline, V-DIFFERENCE (n=1,776) evaluated Leqvio in reduction of hypercholesterolemia plus optimized lipid lowering therapy (LLT). Full results were published in AHJ in August 2025, demonstrating Leqvio conferred LDL-C-target rates in 85% of patients with LLT, compared to 31% on placebo and LLT. Leqvio continues to be evaluated in the following trials:

- VICTORION-1-PREVENT trial (n=14,013) for primary prevention of cardiovascular events, which is expected to complete in April 2029; and

- ORION-4 (n=16,124) and VICTORION-2-PREVENT (n=17,004) trials for secondary prevention of CV events in people with established CVD, which are expected to complete in 2026 and 2027, respectively.

- In the pipeline, V-DIFFERENCE (n=1,776) evaluated Leqvio in reduction of hypercholesterolemia plus optimized lipid lowering therapy (LLT). Full results were published in AHJ in August 2025, demonstrating Leqvio conferred LDL-C-target rates in 85% of patients with LLT, compared to 31% on placebo and LLT. Leqvio continues to be evaluated in the following trials:

- Sales for Regeneron and Sanofi’s Praluent (alirocumab) captured 16% of the market, totaling $216 million in 3Q25, up 13% from 3Q24 and down 5% sequentially. In the US, which Regeneron is responsible for, totaled $67 million, up 26% from 3Q24 and up 2% sequentially. OUS sales, where Sanofi is responsible for commercialization and pays royalties to Regeneron, totaled $148 million, up 2% CER from 3Q24 and down 7% sequentially.

- In the pipeline, Merck is evaluating oral PCSK9 inhibitor enlicitide decanoate (previously called MK-0616) for hypercholesterolemia in phase 3 program. Excitingly, the third phase 3 CORALreef Lipids trial (n=2,760), evaluating enlicitide decanoate vs. placebo in a broader population with hypercholesterolemia, met all primary and secondary endpoints, demonstrating significant LDL-c reduction. CORALreef Outcomes (n=14,550) trial, assessing cardiovascular outcomes, has completed enrollment and is expected to be completed in November 2029.

Graph 22: PCSK9 Inhibitor Sales (1Q16 – 3Q25)

Table 18: 3Q25 PCSK9 Inhibitor Sales

| Revenue (Millions) | YOY Growth | Sequential Growth | Share of Market | |

| Repatha | $794 | +40% | +14% | 60% |

| Praluent | $216 | +13% | -5% | 16% |

| Leqvio | $308 | +56% | +14% | 23% |

| Total | $1,318 | +38% | +8% | -- |

Graph 23: PCSK9 Inhibitor Sales by Geography (1Q17 – 3Q25)

Table 19: 3Q25 PCSK9 Inhibitor Geographic Breakdown

| 2Q25 US Revenue (Millions) | US YOY Growth | US Sequential Growth | 2Q25 OUS Revenue (Millions) | OUS YOY Growth | OUS Sequential Growth | |

| Repatha | $442 | +57% | +22% | $352 | +23% | +5% |

| Praluent | $67 | +26% | +2% | $149 | +7% | -7% |

| Leqvio | $146 | +45% | +6% | $162 | +67% | +1% |

| Total | $655 | +51% | +16% | $663 | +27% | +1% |

Graph 24: PCSK9 Inhibitor market share (1Q16 – 3Q25)

Diabetes Technology

Graph 25: Total Diabetes Technology Market (1Q06 – 3Q25)

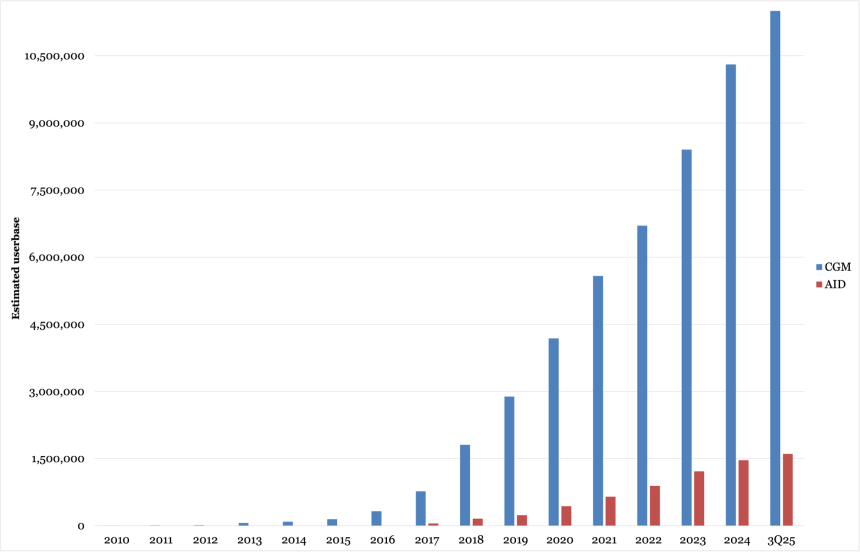

Graph 26: Combined CGM and AID Userbase Estimates Through 3Q25

Continuous Glucose Monitors

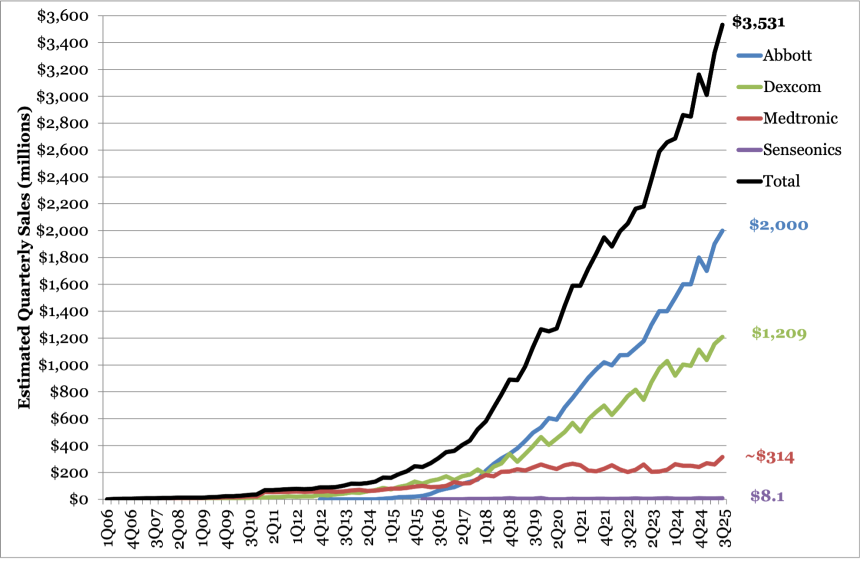

The CGM market delivered another strong quarter in 3Q25, with sustained growth from Abbott, Dexcom, Medtronic, and Senseonics in both revenue and user base. Revenue and userbase growth reflected continued sensor upgrades, expanded coverage for people with T2D and those not on insulin across geographies, and growing OTC contributions to company’s quarterly sales. Sequentially, all four companies posted revenue increases, though estimated user base expansion outpaced revenue growth, likely consistent with broader coverage and lower-cost sensors entering the market.

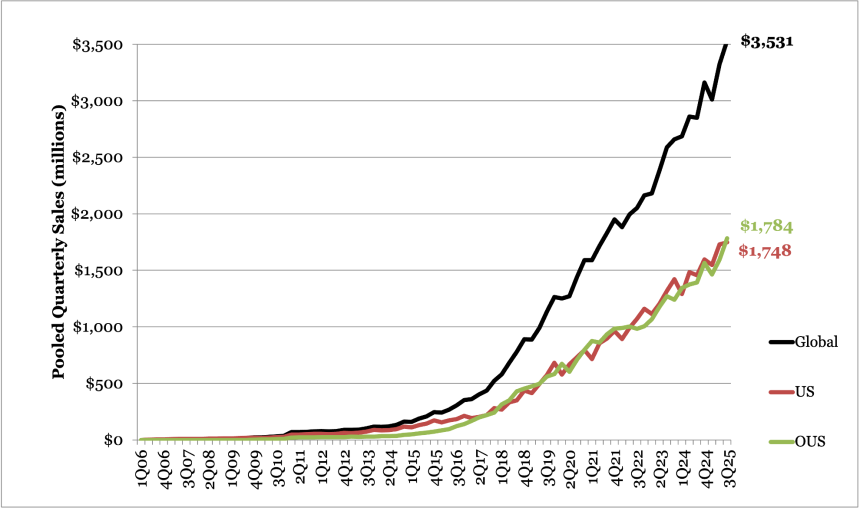

- Overall, CGM revenue totaled $3.5 billion 3Q25, up 24% from 3Q24 and 6% sequentially. This growth continues to reflect the expanding adoption of CGMs among people with T2D, supported by broader reimbursement in both the US and international markets, alongside early contributions from Dexcom and Abbott’s over-the-counter sensors (Stelo and Lingo, respectively), which have been commercially available for over a year.

- By geography, US sales totaled $1.7 billion, up 20% from 3Q24 and nearly flat (+1%) sequentially. International CGM revenue totaled $1.8 billion, up 28% from 3Q24 and up 12% sequentially, as Abbott, Dexcom, and Medtronic all reported record quarterly revenue OUS. Abbott highlighted continued strength in OUS adoption, particularly in Europe and Asia. Dexcom emphasized strength in Dexcom’s ONE+ and G-series platforms in the T2D population, following expanded international coverage for the population; this included increasing penetration in France and Canada’s basal-only markets. Medtronic also reported continued OUS strength in 3Q25, citing strong MiniMed 780G and Simplera Sync adoption more than one year after the seven-day sensor began rolling out internationally.

Graph 27: CGM Sales by Geography (1Q06 – 3Q25)

- The number of CGM users internationally continue to grow. At the end of 3Q25, we estimate[1] the global CGM userbase at over 11.5 million people, up nearly 16% from 3Q24 and approximately 5% sequentially. We estimate over 7.5 million using FreeStyle Libre, over 3.3 million using Dexcom CGMs, ~750,000 using Medtronic CGM, and ~10,000 using Senseonics CGM. Abbott and Dexcom together represented >90% of the global CGM userbase.

- Global market share in 3Q25 largely mirrored historic trends:

- Abbott continued its leadership in the market with approximately $2 billion in FreeStyle Libre revenue (+25% from 3Q24, +5% sequentially), accounting for 57% of global revenue. International growth (+29%) outpaced that in the US (+19%), likely supported by several international FreeStyle Libre launches and integrations earlier in 2025.

- Dexcom’s 3Q25 revenue totaled $1.2 billion (+22% from 3Q24, +4% sequentially), representing 34% of global CGM revenue. Dexcom saw strong and similar performances from both the US (+21%) and OUS (+22%) due to expanded international T2D coverage.

- We estimate that Medtronic’s 3Q25 CGM revenue totaled ~$314 million (+25% from 3Q24 and 21% sequentially), capturing ~9% of the global CGM market. Estimated OUS growth (+33%) surpassed that in the US (+13%), with management pointing to Simplera Sync’s continued strength in the EU and recent US launch as key catalysts for growth; the company also reported strong pre-order rates for its 15-day Abbott-partnered sensor, Instinct. We are curious to see updates on what utilization looks like in its first quarter on the market.

- Senseonics posted $8.1 million in revenue in 3Q25 (+88% from 3Q24, +23% sequentially), representing <1% of the market. US sales more than doubled – up 2.6 times 3Q24 revenue – amid continued adoption of Eversense 365 and growth of its office consignment program, while OUS revenue declined 10% from 3Q24. We are curious how the new control over Eversense commercialization and marketing, effective January 1, 2026, as well as the integration with Sequel’s twiist AID system will impact uptake and revenue in future quarters.

- Beyond market share by revenue, the 3Q25 market share by userbase also remained relatively consistent with 3Q24 and 2Q25: Abbott captured nearly two-thirds of global CGM users (65%), followed by Dexcom with 29%, Medtronic with 6%, and Senseonics capturing <1% of global users.

- In CGM innovation, in software, Dexcom rolled out My Dexcom Account, a redesigned digital service hub, in 3Q25, as well as Smart Basal, an in-app insulin titration module for individuals with T2D, in 4Q25. The FDA also cleared MiniMed 780G for use in T2D, making it the third system in the US to receive the indication. On the hardware side since 3Q25, Medtronic rolled out Simplera Sync and Instinct in the US and Dexcom launched its G7 15 Day CGM for US adults with diabetes in December 2025.

- Meanwhile, OTC CGM offerings are gaining traction. Dexcom’s Stelo continued to receive app updates to better personalize insights and simplify ordering and reordering workflows ahead of a broader app update expected in 2026. Since the conclusion of the quarter, Abbott expanded its Lingo offerings by partnering with Withings to offer Lingo on its connected health platform; it also began selling the OTC CGM brick-and-mortar at Walmart and Walgreens, and enabled Lingo compatibility with Android devices. These developments highlight the rapidly evolving CGM landscape, with innovation spanning hardware, software, and OTC applications seeking to expand patient choice and further improve outcomes.

Quarterly reports: Abbott 3Q25, Dexcom 3Q25, Medtronic 3Q25, Senseonics 3Q25

Graph 28: Total CGM Market (1Q06 – 3Q25)

Table 20: Revenue Roundup Table: CGM Market (3Q25)

| 3Q25 | Revenue (millions) | YOY Change | Sequential Change |

| Abbott | $2,000 | 25% | +5% |

| Dexcom | $1,209 | 22% | +4% |

| Medtronic (est.) | $314 | 25% | +21% |

| Senseonics | $8.1 | 88% | +23% |

| Total | $3,531 | 24% | +6% |

Table 21: Estimated CGM Market Share by Userbase and Revenue (3Q25)

| Company | Userbase (estimated) | Market Share (by userbase) | Revenue (millions) | Market Share (by revenue) |

| Abbott | 7,500,000 | 65% | $2,000 | 57% |

| Dexcom | 3,300,000 | 29% | $1,209 | 34% |

| Medtronic | 775,000 | 6% | $314 | 9% |

| Senseonics | 10,500 | <1% | $8.1 | <1% |

| Total | ~11,585,000 | -- | $3,531 | -- |

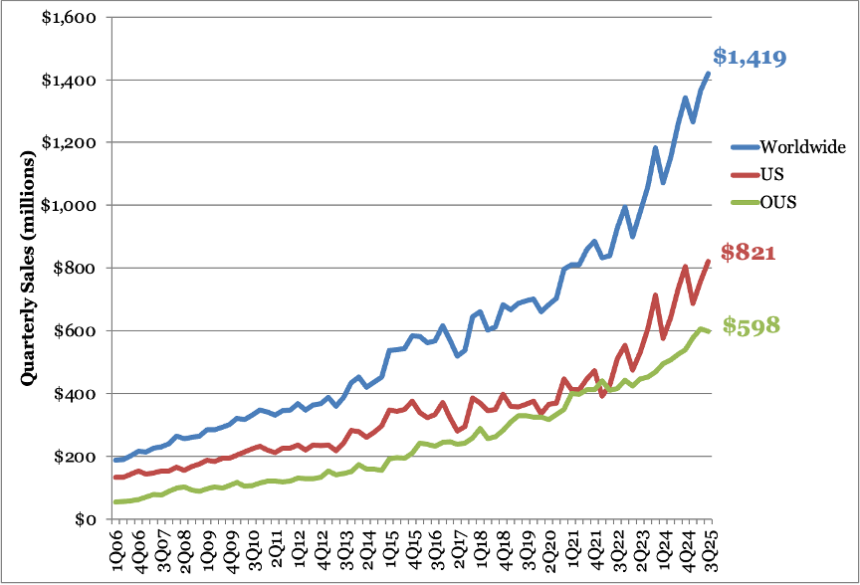

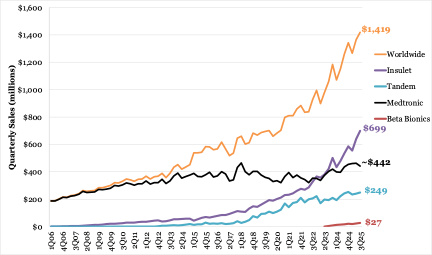

Insulin pumps and AID

Insulin pump revenue in 3Q25 totaled $1.4 billion, up 13% from 3Q24 and 4% sequentially, a continuation of strong pump growth observed in recent years. By geography, US pump revenue totaled $821 million, up 12% from 3Q24 and 8% sequentially, while OUS pump revenue totaled $598 million, up 14% from 3Q24 and flat sequentially. US sales drove most (54%) of the growth, consistent with last quarter, but down from 64% in 3Q24.

- In the quarter, Insulet led worldwide pump growth (87%), followed by Medtronic (4%), Beta Bionics (6%), and Tandem (3%). Insulet has been the dominant growth driver since Omnipod 5’s US launch in 2Q22, and it drove further growth through its international launches of Omnipod 5 and accelerating T2D adoption in the US.

- Insulet maintained its market share by revenue (49%) lead for the 12th consecutive quarter. Growth was driven by record new user starts across both US and OUS markets, with particularly strong momentum internationally (+46%). Management highlighted the expanding uptake in existing European markets, including France, the UK, and Germany, as well momentum with newer launches such as Canada and Australia. In the US, people with T2D accounted for more than 35% of new starts in 3Q25, up from ~30% in 2Q25 and roughly 25% prior to FDA clearance.

- Medtronic held 31% market share, down from 35% in 3Q24 and 34% in 2Q25. US performance reflected anticipation of Medtronic’s new sensors, as the company began accepting Simplera Sync orders in 3Q25 and opened Instinct pre-orders soon after – the company reported more than 35,000 US customer orders and pre-orders for the two next-generation sensors by quarter end. Internationally, Medtronic continued to see strong MiniMed 780G uptake, supported by broader availability of Simplera Sync and newly expanded CE-Mark indications for T2D, pregnancy, and preschoolers.

- Tandem took 18% of the market, supported by steady US revenue growth and continued momentum with Control-IQ+. In 3Q25, the company completed its pilot and expanded commercialization of Control-IQ+ for individuals with T2D, while pharmacy channel access continued to scale, with PBM coverage now surpassing 40% of US lives. Growth remained driven largely by MDI conversions, representing roughly two-thirds of new starts.

- Rounding out the field, Beta Bionics held an estimated 2% market share. The company reported a record 5,334 new iLet pump user starts in 3Q25 (+68% YOY), driven primarily by MDI conversions and expanding pharmacy channel access, which reached the “low 30s” percentage of new starts.

- AID systems continue to drive insulin pump sales, with the estimated global AID userbase representing over 1.5 million individuals. Userbase updates and estimates suggest double-digit growth from 3Q24. At Insulet’s Investor Day in November, management shared that the company now serves more than 600,000 Omnipod 5 users worldwide. In Medtronic’s S-1 filing related to the planned IPO of Diabetes business, the company shared that its business serves more than 640,000 insulin pump users across 80 countries as of October 2025. Ypsomed last announced in May 2025 that the mylife Loop AID system achieved 70,000 active users – with roughly 2,000 users added every month, we estimate over 77,000 users of the system at the end of 3Q25. We estimate Beta Bionics’ userbase to be 29,500 users the end of the quarter. The Roche/Dexcom/Diabeloop AID system has not announced userbase updates, nor has Sequel for the newly launched twiist AID system in the US.

- Despite strong momentum, AID adoption remains meaningfully lower than CGM adoption, reflecting differences in eligible populations. We estimate the ratio of AID to CGM users – which we call the “Aaron Ratio” in honor of Breakthrough T1D CEO Dr. Aaron Kowalski’s efforts to make AID a reality – to be ~14% in 3Q25, flat from 14% in 2024 and 2023 and up slightly from 13% in 2022.

- In pipeline updates, several companies continued to advance next-generation hardware, sensor operability, and algorithm automation.

- Beta Bionics is advancing both its next-generation Mint patch pump and bihormonal iLet. In 3Q25, the company completed a PK-PD “bridging” trial for glucagon, developed by Xeris, which management said supported plans to initiate a 4Q25 human feasibility study of the full dual-hormone iLet before pivotal trials and simultaneous regulatory submissions. Beta Bionics also reiterated that its Mint patch pump remains on track for a 2027 commercial launch. The company received FDA 510(k) clearance in late September for several iLet usability updates.

- Insulet continued to position interoperability and algorithm upgrades as key adoption factors. Omnipod 5 integrated with Dexcom’s G7 15 Day at launch in the US, and FreeStyle Libre 3 Plus integration remains slated for 1H26. On the algorithm front, the company completed enrollment for the STRIVE pivotal trial of SmartAdjust 2.0 and the EVOLUTION2 T2D feasibility study evaluating its fully closed-loop system in individuals with T2D.

- Medtronic emphasized growth from new sensor launches and expanding MiniMed 780G indications. In 3Q25, the company highlighted the continued ramp of Simplera Sync and growing US momentum for its FreeStyle Libre-based Instinct sensor, noting more than 35,000 US customer orders and pre-orders for the two sensors by quarter end and over 9,000 HCPs placing orders as first-time Medtronic prescribers. Meanwhile, MiniMed 780G received CE-Mark for three significant label expansions in July: (i) use in individuals with T2D on insulin therapy; (ii) use during pregnancy; and (iii) use in children as young as two years old, lowering the minimum age from seven years. The FDA also cleared SmartGuard as an iAGC, enabling compatibility with Instinct. Longer term, Medtronic shared that FDA submission is expected for MiniMed Flex in 1Q26 and for MiniMed Fit in fall 2026. The company also said that FDA authorization was granted to initiate a US pivotal trial for its third-generation fully closed-loop algorithm, Vivera.

- Tandem highlighted faster progress in software and hardware updates alongside its push to broaden access. In 3Q25, the company launched t:slim X2 integration with FreeStyle Libre 3 Plus in the US and reiterated expectations for FDA clearance of Mobi Android control. On hardware, Tandem said Mobi Tubeless entered its final stage of testing to support a 510(k) submission by year-end, with an expected 2026 launch. Tandem also maintained that it expects to initiate a pivotal study for its fully closed-loop algorithm in 2026 through its University of Virginia partnership.

Quarterly reports: Insulet 3Q25, Medtronic F2Q26, Tandem 3Q25, Beta Bionics 3Q25

Graph 29: Insulin Pump and Delivery Sales by Geography (1Q06 – 3Q25)

Graph 30: Insulin Pump and Delivery Sales by Company (1Q06 – 3Q25)

Table 22: Revenue Roundup Table: Insulin Pump Market (3Q25)[1]

3Q25 | Revenue (millions) | YOY Change | Sequential Change | Market Share (by revenue) |

Insulet | $706 | +30% | +9% | 49% |

Medtronic (est.) | $442 | +1% | flat | 31% |

Tandem | $249 | +3% | +4% | 18% |

Beta Bionics | $27 | +54% | +32% | 2% |

Total | $1,419 | +19% | +8% | -- |

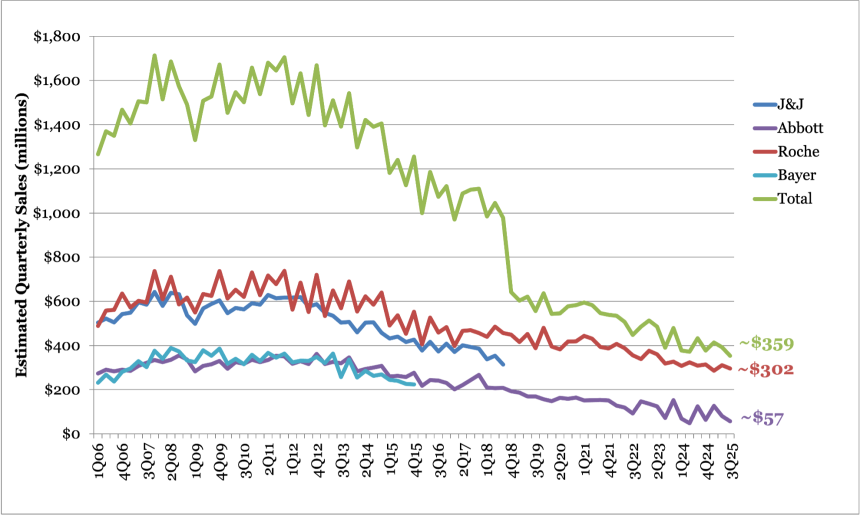

Blood Glucose Monitors and “Other”

For the two public companies in the BGM market, Abbott and Roche, we estimated that combined 3Q25 revenue totaled $359 million, down 17% from 3Q24 and 8% sequentially. We estimate that US sales totaled $72 million, down 4% from 3Q24 but up 10% sequentially, while international sales totaled $287 million, down 20% from 3Q24 and 12% sequentially.

- For Abbott, we estimate BGM sales totaled $57 million in 3Q25, down 54% from 3Q24 and 30% sequentially. Roche no longer reports standalone Diabetes Care sales after merging this business into the Near Patient Care segment within its Diagnostics division last year. However, Roche reported that its BGM business declined 2% from 3Q24, enabling us to estimate $302 million in sales, down 3% sequentially.

- Despite year-over-year and sequential BGM revenue declines in 3Q25 from high bases in the US and OUS, BGM revenue has stabilized in recent quarters. Historical category decline was reflective of: (i) increasing CGM coverage and uptake among a broader population, such as T2D; and (ii) negative pricing trends. We presume this stabilization of BGM revenue reflects the continued demand for BGM amidst rising global diabetes rates, despite continual pressure from increasing CGM uptake among a broader population and negative pricing trends.

- As always, we note that it is difficult to gauge the full size of the market and its dynamics because: (i) Roche no longer reports Diabetes Care revenue; (ii) Abbott reports CGM and overall glucose monitoring revenue to just two digits, requiring estimation of its BGM revenue; and (iii) many major BGM companies are now private – e.g., LifeScan (formerly part of J&J), Ascensia (formerly part of Bayer), i-SENS (acquirer of AgaMatrix), etc. According to our model, to-date BGM market revenue among publicly reporting companies nears $100 billion since 2006, which, of course, understates true revenue in this ecosystem.

In 3Q25, the “Other” diabetes technology category totaled $271 million. This category includes embecta’s revenue of $264 million (-8%) and Insulet’s non-diabetes Omnipod revenue of $7.1 million (-30%). We no longer include revenue from NeuroMetrix following electroCore’s acquisition of most of NeuroMetrix’s assets in December 2024, including Quell (its neurostimulator indicated for the relief of fibromyalgia and lower-extremity chronic pain) but excluding DPNCheck (its diagnostic rapid point-of-care test for detecting peripheral neuropathy).

Quarterly reports: Abbott 3Q25 and Roche 3Q25

Graph 31: Total BGM Market (1Q06 – 3Q25)