Novo Nordisk 4Q25 – D+O totals $11.6B in 4Q25 (-2% CER) and $45B (+10% CER) in 2025; strong uptake of oral Wegovy in January amid EOY weakness; 2026 guidance forecasts major decline in sales –

Executive Highlights

- Novo Nordisk presented its 4Q25 and full-year update today, led by CEO Mr. Maziar Mike Doustdar and CFO Mr. Karsten Munk Knudsen – see the press release, presentation, finance detail, webcast, and annual report.

- In sweeping leadership changes, Novo Nordisk announced that Mr. Jamey Millar will be the next EVP and Head of US Operations, and Ms. Hong Chow will become the EVP and Head of Product and Portfolio Strategy. They will be succeeding Mr. David Moore and Mr. Ludovic Helfgott, respectively. Mr. Millar was formerly CEO of UnitedHealth Group’s Optum Specialty Holding and has 30 years of experience in pharma industry. Ms. Chow previously served as the EVP and Head of China and International at Merck Healthcare.

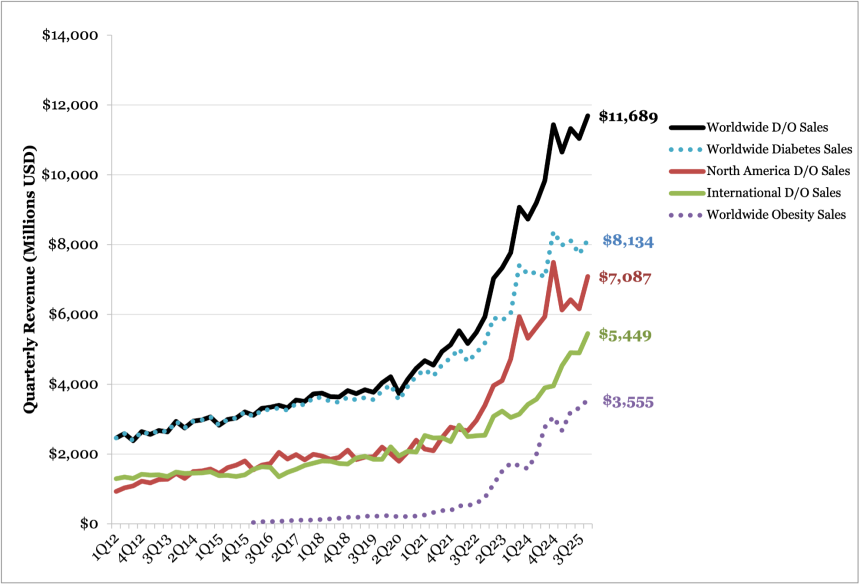

- Novo Nordisk’s diabetes and obesity portfolio totaled $11.6 billion in 4Q25, down 2% CER and up 5% sequentially. By geography, US sales totaled $7.0 billion (down 7% CER, +14% Q/Q), and OUS sales totaled $5.4 billion (+8% CER, +11% Q/Q).

- For 2025, Novo Nordisk generated nearly $45 billion in diabetes and obesity revenue, up 10% CER from 2024. Like at Lilly, growth was almost entirely driven by obesity sales, which totaled $3.5 billion, up 11% CER from 4Q24 and up 6% sequentially. Over the past year, Novo Nordisk has treated 45.6 million people, an increase of 400,000 patients (+1%) from 2024.

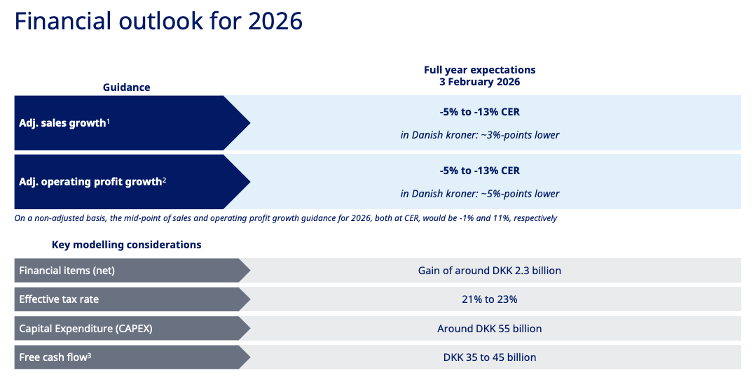

- Novo Nordisk shared conservative guidance for 2026 that predicts a 5-13% CER reduction in both sales and operating profit. This expectation is primarily driven by lower expected pricing in the US reflecting: (i) expanding use of cash-pay channel; and (ii) the impact of the US’ Most Favored Nation deal. While lower prices lead to volume increases, the speed and the extent to which the volume will increase is of course unknown at this stage. In international operations, Novo Nordisk predicts mid-single-digit growth, as well as loss of exclusivity of semaglutide in specific markets, including in Canada.

- Though GLP-1 RA sales for diabetes were far lower than expected, there was strength in some obesity sales in international markets. In 4Q25, sales totaled $9.4 billion (-6% YoY, +4% Q/Q). In 2025, US sales were $23 billion (+4% YoY), while OUS sales were $13 billion (+20% YoY). Full year sales totaled $36 billion, up 9% from 2024. Starting in mid-2026, under the Most Favored Nation deal, Medicare can access Ozempic (semaglutide for T2D) and Wegovy (semaglutide for obesity) for $245/month, with a co-pay of $50 per month. Starting in 2027, Ozempic, Rybelsus, and Wegovy will be available at ~$274 per month, down from ~$950/month under the Medicare Drug Price Negotiation Program.

- Ozempic: Global sales totaled $5 billion in 4Q25, up 1% CER from 4Q24 and up 4% sequentially. US sales totaled $3.5 billion (-2% CER, +4% Q/Q), and OUS sales totaled $1.5 billion (+8% CER, flat Q/Q). Ozempic recorded $19.6 billion in 2025 revenue, up 10% CER from 2024. In the US, Ozempic’s weekly prescriptions totaled ~610,000 units in the quarter, down from 670,000 in 3Q25, and captured 39% of the US incretin market.

- Wegovy: Sales totaled $3.4 billion in 4Q25, up 17% CER from 4Q24 and up 7% sequentially. US sales totaled $2.2 billion (-2% CER, +10% Q/Q), and OUS sales totaled $1.3 billion (+77% CER, +4% Q/Q). In the US, Wegovy has around 233,000 weekly prescriptions (down from 270,000 in 3Q25), which is nearly half of tirzepatide’s (469,000). Cash channel comprises ~30% of total prescriptions.

- Oral Wegovy: In January 2026, Novo Nordisk launched oral Wegovy as the only oral GLP-1 RA for obesity, following FDA approval in December 2025. In the week ending January 23, there were ~50,000 total weekly prescriptions, ~45,000 of which were through self-pay channel. While still early, the speed of uptake is significantly steeper compared injectable Wegovy and Lilly’s injected tirzepatide – likely a combination of factors including oral formulation, price, and efficacy.

- Unlike at Lilly, where only two of eight products had positive growth, some Novo Nordisk products showed growth and focus outside of the incretin class. In 4Q25, insulin sales totaled $2.1 billion, down 10% CER from 4Q24 and up 12% sequentially. US sales totaled $627 million, down 30% from 4Q24 and up 26% sequentially, and OUS sales totaled $1.5 billion, down 8% from 4Q24 and up 7% sequentially. In 2025, insulin revenue was $8.2 billion, down 4% from 2024.

4Q25 Financial Results for Novo Nordisk’s Major Diabetes Products

| Product | 4Q25 Revenue – USD millions | Year-Over-Year Reported Growth for 4Q25 | Sequential Reported Growth |

| GLP-1 (excluding Xultophy) | $9,428 | +4%* | +4% |

| Ozempic | $5,003 | +1% | +4% |

| Wegovy | $3,437 | +17% | +7% |

| Rybelsus | $834 | -19% | -3% |

| Victoza | $63 | -70% | 27% |

| Saxenda | $91 | -62% | -23% |

| Total Insulin | $2,083 | -8% | +12% |

| Basal Insulin | $715 | -12% | +12% |

| Tresiba | $479 | +18% | -16% |

| Levemir | $54 | -69% | +10% |

| Xultophy | $182 | -5% | +3% |

| Awiqli | $23 | n/a | +5% |

| Rapid-Acting Insulin | $767 | -19% | +19% |

| NovoLog | $636 | -24% | +16% |

| Fiasp | $132 | +154% | +32% |

| Premix Insulin | $394 | -12% | +6% |

| NovoMix | $190 | -15% | +13% |

| Ryzodeg | $204 | +4% | +1% |

| Human Insulin | $206 | -24% | -1% |

| Other | $66 | -12% | flat |

| Total Diabetes and Obesity Portfolio | $11,601 | -2% | +5% |

2025 Financial Results for Novo Nordisk’s Major Diabetes Products

| Product | 2025 Revenue – USD millions | Year-Over-Year Reported (CER) Growth |

| GLP-1 (excluding Xultophy) | $36,175 | +9% (+6%) |

| Ozempic | $19,586 | +6% (+10%) |

| Wegovy | $12,228 | +36% (+41%) |

| Rybelsus | $3,405 | -5% (-2%) |

| Saxenda | $497 | -53% (+52%) |

| Victoza | $461 | +45% (+43%) |

| Total Insulin | $8,173 | -4% (-1%) |

| Basal Insulin | $2,820 | -4% (+1%) |

| Tresiba | $1,851 | +22% (+26%) |

| Levemir | $257 | -64% (-64%) |

| Xultophy | $712 | +3% (+5%) |

| Awiqli | $64 | N/A |

| Rapid-Acting Insulin | $2,861 | flat (+3%) |

| NovoLog | $2,428 | -5% (-2%) |

| Fiasp | $433 | +51% (+54%) |

| Premix Insulin | $1,588 | -4% (-1%) |

| NovoMix | $759 | -16% (-14%) |

| Ryzodeg | $829 | +17% (+13%) |

| Human Insulin | $841 | -21% (-18%) |

| Other | $273 | -17% (-14%) |

| Total Diabetes and Obesity Portfolio | $44,621 | +7% (+10%) |

Table of Contents

-

Financial Highlights

- 1. D/O totals $11.6 billion (-2% CER) in 4Q25 and $44.6 billion in 2025 (+10% CER); guidance predicts 5-13% CER reduction in annual sales

- 2. GLP-1 RAs for T2D: Ozempic totals $5 billion (+1%), followed by Rybelsus ($834 million, -19%) and Victoza ($63 million, -70%)

- 3. Obesity revenue totals $3.3 billion (+18% CER), driven by continued uptake of Wegovy and strong launch of oral Wegovy

- 4. Insulin sales total $2.1 billion, including Tresiba (+18%), Fiasp (up 2.5x), and Xultophy (-5%); FDA decision for Awiqli expected in 1H26

- Pipeline Highlights

- Close Concerns’ Questions

- Analysts’ Q&A

Financial Highlights

1. D/O totals $11.6 billion (-2% CER) in 4Q25 and $44.6 billion in 2025 (+10% CER); guidance predicts 5-13% CER reduction in annual sales

In 4Q25, Novo Nordisk’s diabetes and obesity portfolio totaled $11.6 billion, down 2% CER and up 5% sequentially. US sales totaled $7.0 billion, down 7% CER from 4Q24 and up 14% sequentially. OUS sales totaled $5.4 billion, up 8% CER from 4Q24 and up 11% sequentially. In 2025, total diabetes and obesity revenue was $44.6 billion, up 10% CER from 2024. Over the past year, Novo Nordisk has treated 45.6 million people, an increase of 400,000 patients (+1%) from 2024.

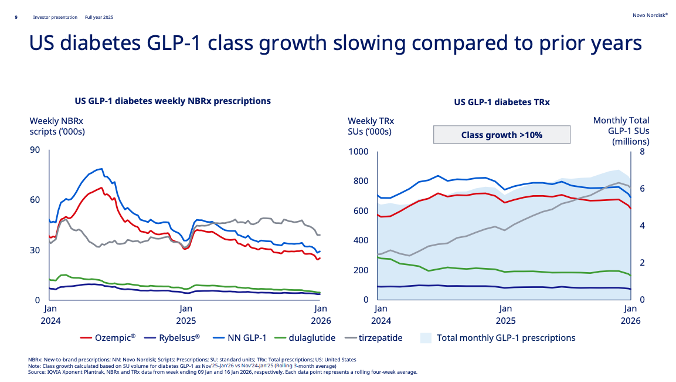

Similar to previous quarters, growth was driven by Obesity sales (Wegovy and Saxenda), which totaled $3.5 billion, up 11% CER from 4Q24 and up 6% sequentially. By geography, obesity sales in International Operations totaled $1.4 billion, growing 50% CER YoY, while US sales of $2.2 billion decreased by 4% CER. Meanwhile, GLP-1 RA sales for diabetes largely remained flat, totaling $5.1 billion in 4Q25, down 2% CER from 4Q24 and up 2% sequentially. As shown in the figure below, GLP-1 RA sales are slowing due to limited market growth in the US, as well as competition from Lilly’s Mounjaro.

Source: Novo Nordisk 4Q25 presentation, page 9

- Novo Nordisk expects headwinds due to price reductions in 2026. The guidance predicts a 5-13% CER reduction in both sales and operating profit. We note that capital expenditure (CAPEX) is ~$8.7 billion, which is greater than the free cash flow of $5.5-$7.1 billion (see figure below). During Q&A, management detailed several factors contributing to the conservative guidance.

- In the US, the company expects sales decline by the teens in 2026. This is primarily driven by lower price from: (i) expanding use of cash-pay channel; and (ii) the impact of the US’ Most Favored Nation deal. While lower prices lead to volume increases – as evidenced by cash channel comprising 30% of injectable Wegovy prescriptions – the speed and the extent to which the volume will increase remains unclear.

- In November 2025, Novo Nordisk entered agreements with the US government to lower prices of semaglutide. Under the Most Favored Nation deal, Medicare can access Ozempic (semaglutide for T2D) and Wegovy (semaglutide for obesity) for $245/month, with a co-pay of $50 per month. On TrumpRx, Wegovy and Wegovy pill will be offered at $350 and $150 per month, respectively. Under the Medicare Drug Price Negotiation Program, Ozempic, Rybelsus, and Wegovy will face a 71% cut to the list prices, down from ~$950 per month in 2024 to ~$274 in 2027. Mr. Knudsen said Medicare Part D reimbursement will be beneficial starting mid-year, but given the lag between physician education and patients’ access, larger benefit will be seen in 2027.

- For international operations, Novo Nordisk predicts mid-single-digit growth. Mr. Knudsen clarified that this figure is based on the previous trends (+8% CER in 4Q25 and +10% CER in 2H25), as well as loss of exclusivity of semaglutide in specific markets. Notably, Mr. Knudsen said that the loss of exclusivity in Canada is the biggest contributor; timing of generic launches will impact sales, however.

- As a reminder, Novo Nordisk lowered the 2025 guidance four times in the past year. While the full year sales (+10% CER) and operating profit (+6%) met the most recent guidance from 3Q25, these figures are significantly lower from the original guidance of 16-24% and 4-10%, respectively, from January 2025.

- In the US, the company expects sales decline by the teens in 2026. This is primarily driven by lower price from: (i) expanding use of cash-pay channel; and (ii) the impact of the US’ Most Favored Nation deal. While lower prices lead to volume increases – as evidenced by cash channel comprising 30% of injectable Wegovy prescriptions – the speed and the extent to which the volume will increase remains unclear.

Source: Novo Nordisk 4Q25 presentation, page 18

Novo Nordisk D/O Worldwide Financial Results – Past Five Quarters

Diabetes/ Obesity | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 |

| Revenue – USD billions (DKK billions) | $11.4 (DKK 80) | $10.7 (DKK 73) | $11.3 (DKK 72) | $11.0 (DKK 70) | $11.6 (74) |

| YOY Growth (CER) | +31% (+30%) | +21% (+19%) | +12% (+17%) | +5% (+11%) | -8% (-2%) |

| Sequential Reported Growth | +20% | -8% | -2% | -2% | +5% |

Novo Nordisk D/O Sales – 4Q25 Geographic Results

| Revenue – USD billions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth | |

| US | $7.0 (DKK 44.7) | -10% (-7%) | +14% |

| OUS | $5.4 (DKK 34.4) | +13% (+8%) | +11% |

2. GLP-1 RAs for T2D: Ozempic totals $5 billion (+1%), followed by Rybelsus ($834 million, -19%) and Victoza ($63 million, -70%)

Incretin-based therapies for T2D totaled $5.9 billion in 4Q25, down 5% from 4Q24 and up 4% sequentially. US sales totaled $3.9 billion, down 6% CER from 4Q24 and up 5% sequentially. OUS sales totaled $2.0 billion, down 2% CER from 4Q24 and flat sequentially. In 2025, GLP-1 RA sales totaled $152 billion, up 6% CER from 4Q24. The growth was largely driven by Ozempic (semaglutide for T2D), which comprised 84% of the total GLP-1 RA sales.

- Ozempic (once-weekly injectable semaglutide 0.5 mg, 1 mg, or 2 mg) revenue totaled $5 billion in 4Q25, up 1% CER from 4Q24 and up 4% sequentially. US sales totaled $3.5 billion, down 2% CER from 4Q24 but up 4% sequentially. Similar to 3Q25, Ozempic sales continued to be positively impacted by gross-to-net sales adjustments, though this was partially countered by loss of market share and lower realized pricing. OUS sales totaled $1.5 billion, up 8% CER from 4Q24 and up flat sequentially. Ozempic recorded $19.6 billion in 2025 revenue, up 10% CER from 2024. In 2025, US sales totaled $13.6 billion (+9% CER), and OUS sales totaled $5.9 billion (+10% CER).

- In the US, Ozempic’s weekly prescriptions totaled ~610,000 units in the quarter, down from 670,000 in 3Q25. Since 2Q25, Mounjaro has exceeded semaglutide in both new-to-brand and total prescriptions, with Lilly capturing 61% of the US incretin market compared with Novo Nordisk’s 39%.

- On pricing, in August 2025, the company launched a cash option for Ozempic at $499 per month for eligible self-paying patients. This reflects a 50% reduction from the list price of ~$1,000/month and applies to all three doses (0.5 mg, 1 mg, and 2 mg) of Ozempic auto-injectors. In addition, according to government agreements, Ozempic and Rybelsus are set to cost ~$277 per month starting in 2027 under MDPNP, while MFN pricing sets the drugs at $245 per month starting in mid-2026. During Q&A, management said that these negotiations will affect sales in 2027 more than in 2026.

Ozempic Worldwide Financial Results – Past Five Quarters

| Ozempic | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $4,841 (DKK 33.9) | $4,745 (DKK 32.7) | $5,005 (DKK 31.8) | $4,833 (DKK 30.7) | $5,002 (DKK 31.8) | $19,586 (DKK 127.1) |

| YOY CER Growth | +13% (+12%) | +18% (+15%) | +10% (+15%) | +3% (+9%) | +6% (+1%) | +6% (+10%) |

| Sequential Reported Growth | +14% | -3% | -3% | -3% | +4% | N/A |

Ozempic Sales – 4Q25 Geographic Results

| Ozempic | Revenue – USD millions (DKK billions) | YOY CER Growth | Sequential Reported Growth |

| US | $3,514 (DKK 22.4) | +1% (-2%) | +5% |

| OUS | $1,489 (DKK 9.5) | +9% (+8%) | flat |

Ozempic Sales (1Q18-4Q25)

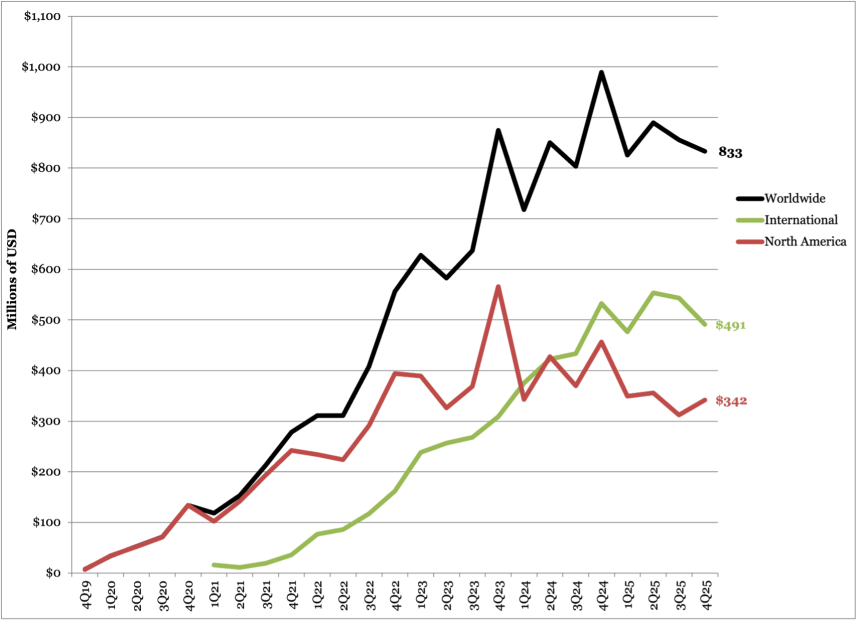

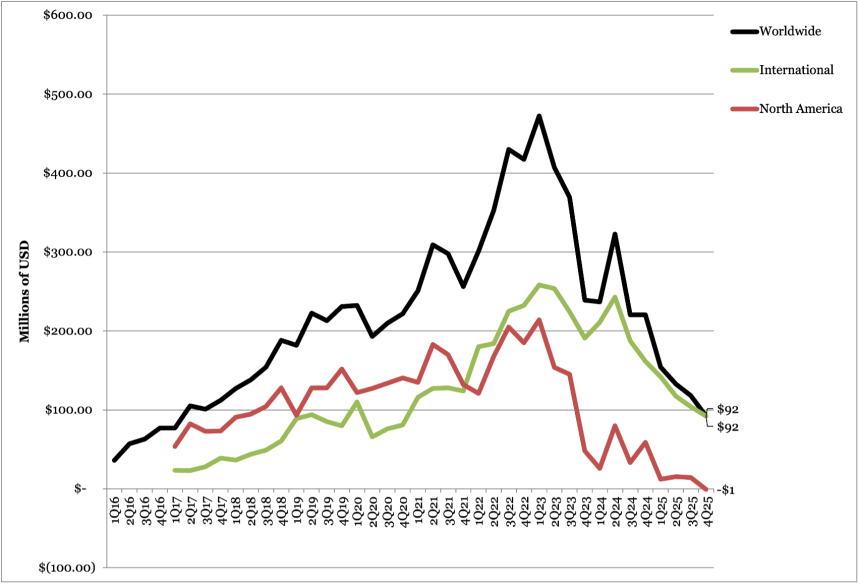

Rybelsus (oral semaglutide) sales totaled $834 million in 4Q25, down 23% from 4Q24 and down 4% sequentially. By geography, US sales totaled $342 million, down 30% from 4Q24 and up 10% sequentially. OUS sales totaled $491 million, down 18% from 4Q24 and down 10% sequentially. In 2025, Rybelsus totaled $3.4 billion in revenue, down 2% CER from 2024, with US sales of $1.4 billion (-15% CER) and international sales of $2 billion (+9% CER).

In its 2025 annual report, the company noted that Rybelsus sales have been impacted by shifting priorities towards other GLP-1 RA treatments.

Novo Nordisk Rybelsus Worldwide Financial Results – Past Five Quarters

| Diabetes/Obesity | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $989 (DKK (6.9) | $826 (DKK 5.7) | $890 (DKK 5.7) | $855 (DKK 5.4) | $834 (DKK 5.3) | $3,405 (DKK 22) |

| YOY Reported (CER) Growth | +18% | +13% | -5% (-1%) | flat (+4%) | -23% (-19%) | -5% (+2%) |

| Sequential Reported Growth | +27% | -18% | -1% | -4% | -3% | N/A |

Novo Nordisk Rybelsus Sales – 4Q25 Geographic Results

| Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth | |

| US | $342 (DKK 2.0) | -30% (-24%) | +10% |

| OUS | $491 (DKK 3.5) | -18% (-15%) | -10% |

Rybelsus Sales (4Q19-4Q25)

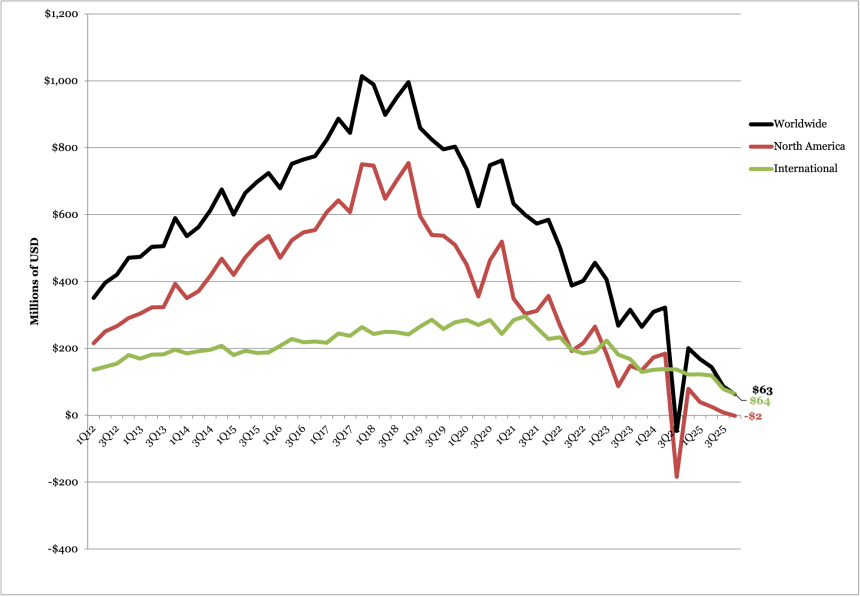

Victoza (liraglutide) sales totaled $63 million, down 70% CER and down 27% sequentially. US sales in 4Q25 were down 100% CER and down 122% sequentially with revenues of net negative $2 million. OUS sales totaled $64 million, down 52% CER and 18% sequentially. Victoza totaled $460 million in 2025 revenue, down 43% CER from 2024.

In 2025, US sales totaled $71 million (-71% CER), and international sales totaled $394 million (-30% CER). The company stated that the decline was driven by increased uptake of once-weekly GLP-1 RA.

Victoza Worldwide Financial Results – Past Five Quarters

| Victoza | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $201 (DKK 1.4) | $168 (DKK 1.2) | $144 (DKK (0.9) | $86 (DKK 0.5) | $63 (DKK 399) | $71 (DKK 3.0) |

| YOY (CER) Growth | -21% (-22%) | -46% (-46%) | -59% (-57%) | N/A (flat) | -71% (-70%) | -45% (-43%) |

| Sequential Reported Growth | +536% | -18% | -21% | -40% | -40% | N/A |

Victoza Sales – 4Q25 Geographic Results

| Victoza | Revenue – USD millions (DKK billions) | YOY (CER) Growth | Sequential Reported Growth |

| US | $-2 (DKK 0.05) | -102% (-100%) | -68% |

| OUS | $64 (DKK 0.5) | -53% (-52%) | -34% |

Victoza Sales (1Q12-4Q25)

3. Obesity revenue totals $3.3 billion (+18% CER), driven by continued uptake of Wegovy and strong launch of oral Wegovy

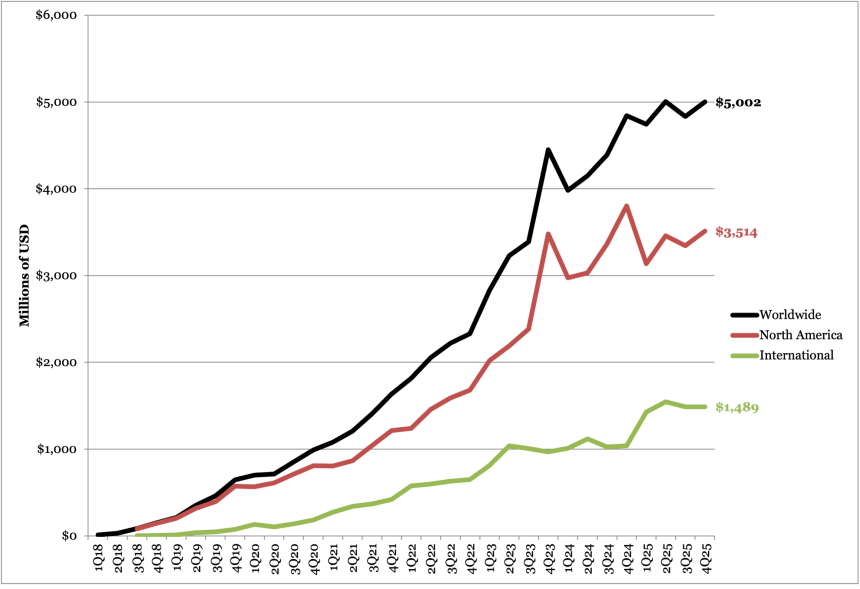

In 4Q25, obesity sales totaled $3.5 billion, up 11% CER from 4Q24 and up 6% sequentially. In the US, sales totaled $2.2 billion (-4% CER), while OUS sales totaled $1.4 billion (+50% CER), suggesting robust growth in international markets.

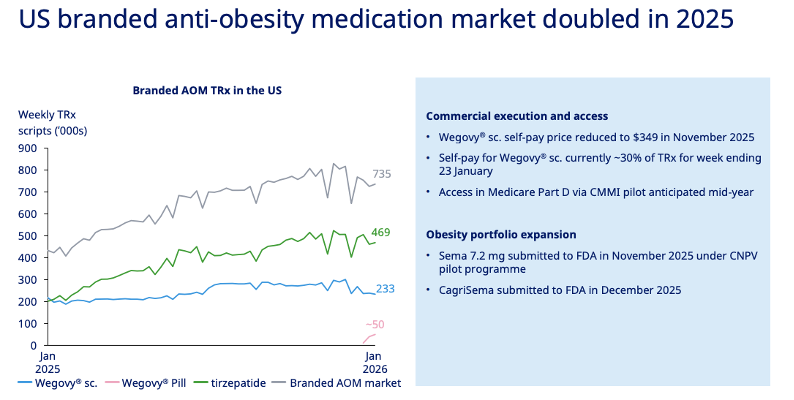

In 2025, obesity sales totaled $12.9 billion, up 31% from 2024, consisting of US sales of $8.1 billion (+15%) and OUS sales of $4.9 billion (+73%). Management noted that the obesity market in the US doubled the past year.

Source: Novo Nordisk 4Q25 presentation, page 11

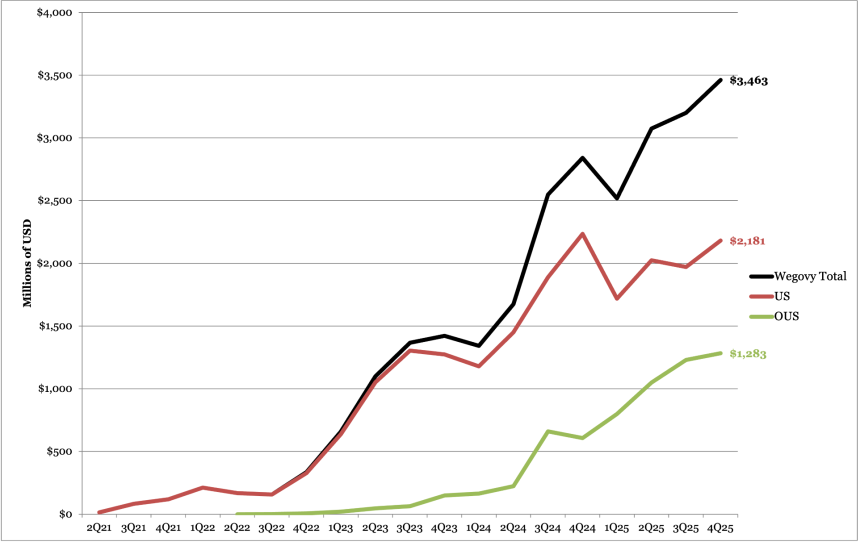

- Wegovy sales totaled $3.4 billion in 4Q25, up 17% CER from 4Q24 and up 7% sequentially. By geography, US sales totaled $2.2 billion, down 2% CER from 4Q24 and up 10% sequentially. OUS sales totaled $1.3 billion, up 77% CER from 4Q24 and up 4% sequentially. In 2025, Wegovy sales totaled $12 billion, up 41% CER from 2024. In the US, Wegovy has around 233,000 weekly prescriptions (down from 270,000 in 3Q25 and 280,000 in 2Q25), which is approximately half of Lilly’s tirzepatide prescriptions for the same time period (469,000).

- In the cash channel, Novo Nordisk lowered self-pay price of Wegovy in November 2025 to $349 per month, down from $499 per month. The lower price has increased the Wegovy uptake in the cash channel, which comprises ~30% of total weekly prescriptions. On a national level, under the Most Favored Nation agreement, Wegovy and Wegovy pill will be offered at $350 and $150 per month, respectively on TrumpRx, the US government’s direct-to-consumer platform.

- In the insured channel, Wegovy will be included in the Medicare Part D via the Center for Medicare and Medicaid Innovation (CMMI) pilot mid-year under the Most Favored Nation agreement. Medicare can access Ozempic (semaglutide for T2D) and Wegovy (semaglutide for obesity) for $245/month, with a co-pay of $50 per month. Under the Medicare Drug Price Negotiation Program, Ozempic, Rybelsus, and Wegovy will face a 71% cut to the list prices, down from ~$950 per month in 2024 to ~$274 in 2027. Mr. Knudsen said Medicare Part D reimbursement will be beneficial starting mid-year, but larger effects will be seen in 2027.

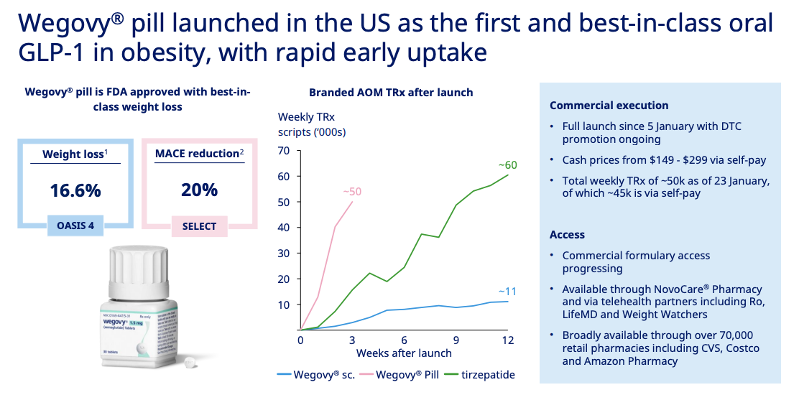

- In January 2026, Novo Nordisk launched oral Wegovy at over 70,000 pharmacies and telehealth platforms as the only oral GLP-1 RA for obesity, following FDA approval in December 2025. Management reported impressive uptake in the first three weeks of launch: in the week ending January 23, there were ~50,000 total weekly prescriptions, ~45,000 of which were through self-pay channel, where the drugs cost $149-$299 per month. While still early, the speed of uptake is significantly steeper compared injectable Wegovy and tirzepatide, as shown in the figure below. During Q&A, management said that the obesity market often reacts to the magnitude of weight loss. Given that Wegovy pill offers weight loss up to 16%, compared to 12% with Lilly’s oral small molecule GLP-1 RA, orforglipron, Mr Doustdar is confident that it will compete well. Management is also confident that its manufacturing capacity can meet the demand.

Source: Novo Nordisk 4Q25 presentation, page 10

- Saxenda sales totaled $91 million, down 62% CER from 4Q24 and down 23% sequentially. US sales totaled -$1 million, down 100% CER from 4Q24 and down 99% sequentially. OUS sales totaled $92 million, down 513 CER from 4Q24 and down 12% sequentially. In 2025, sales totaled $497 million, down 52% CER from 2024. While not mentioned in the call, we imagine that competition from newer generations of GLP-1 RAs has negatively impacted Saxenda sales.

Wegovy Worldwide Financial Results – Past Five Quarters

| Wegovy | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $2,841 (DKK 19.9) | $2,517 (DKK 17.4) | $3,074 (DKK 19.5) | $3,200 (DKK 20.4) | $3,437 (DKK 21.9) | $12,228 (DKK 79.1) |

| YOY Reported (CER) Growth | +107% | +83% | +68% (+75%) | +18% (+23%) | +10% (17%) | +36% (+41%) |

| Sequential Reported Growth | +15% | -13% | +13% | +4% | +7% | N/A |

Wegovy Sales – 4Q25 Geographic Results

| Wegovy | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | $2,164 (DKK 13.8) | -9% (-2%) | +10% |

| OUS | $1,273 (DKK 8.1) | +71% (+77%) | +4% |

Wegovy Sales (2Q21-4Q25)

Saxenda Worldwide Financial Results – Past Five Quarters

| Saxenda | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $220 (DKK 1.5) | $154 (DKK 1.1) | $133 (DKK 0.8) | $118 (DKK 0.8) | $91 (DKK 0.6) | $497 (DKK 3.2) |

| YOY Reported (CER) Growth | -3% | -35% | -62% (-61%) | -50% (-47%) | -62% (-62%) | -53% (-52%) |

| Sequential Reported Growth | +3% | -31% | -21% | -11% | -23% | N/A |

Saxenda Sales – 4Q25 Geographic Results

| Saxenda | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | -$1 (-DKK 0.01) | -100% (-99%) | -68% |

| OUS | $92 (DKK 0.6) | -53% (-53%) | -12% |

Saxenda Sales (1Q16-4Q25)

4. Insulin sales total $2.1 billion, including Tresiba (+18%), Fiasp (up 2.5x), and Xultophy (-5%); FDA decision for Awiqli expected in 1H26

In 4Q25, insulin sales totaled $2.1 billion, down 10% CER from 4Q24 and up 12% sequentially. US sales totaled $627 million, down 30% from 4Q24 and up 26% sequentially, and OUS sales totaled $1.5 billion, down 8% from 4Q24 and up 7% sequentially. In 2025, insulin revenue was $8.2 billion, down 4% from 2024.

While not mentioned in the call, Novo Nordisk’s insulin portfolio includes: (i) next-generation basal insulin Tresiba; (ii) fast-acting insulin Fiasp; (iii) fast-acting insulin NovoLog; and (iv) basal insulin/GLP-1 RA combination Xultophy. See the revenues below:

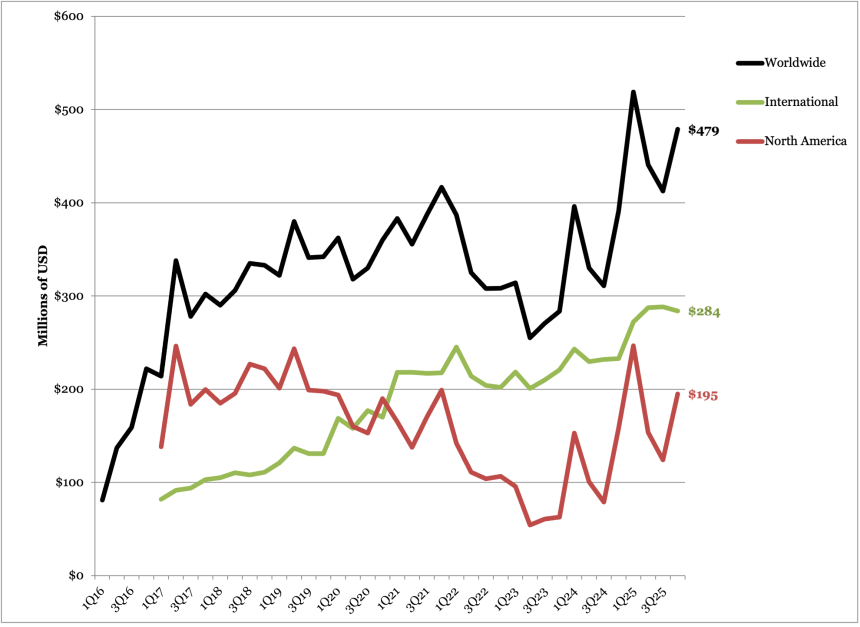

- Next-generation basal insulin Tresiba totaled $479 million, up 18% CER and up 16% sequentially. US sales totaled $195 million, up 41% CER and up 57% sequentially. OUS sales totaled $284 million, up 6% CER and down 2% sequentially. In 2025, sales totaled $1.9 billion, up 26% from 2024. In 2025, Tresiba sales totaled $1.9 billion, up 26% CER from 2024.

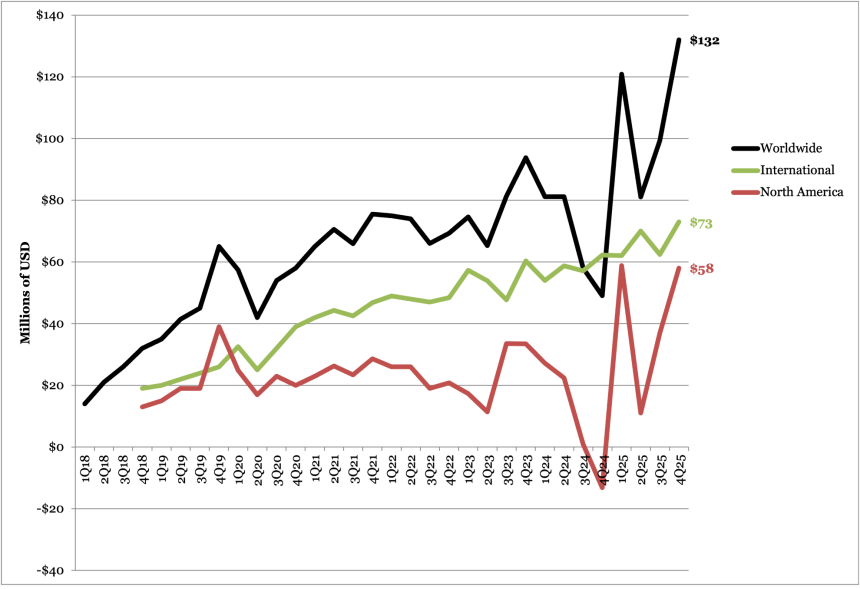

- Fast-acting insulin Fiasp sales totaled $132 million (+154% CER, +32% Q/Q) in 4Q25 and totaled $433 million (+54% CER) in 2025. Sales in the US totaled $58 million (+425% CER), and international sales totaled $73 million (+6% CER). In 2025, Fiasp sales totaled $33 million, up 54% CER from 2024.

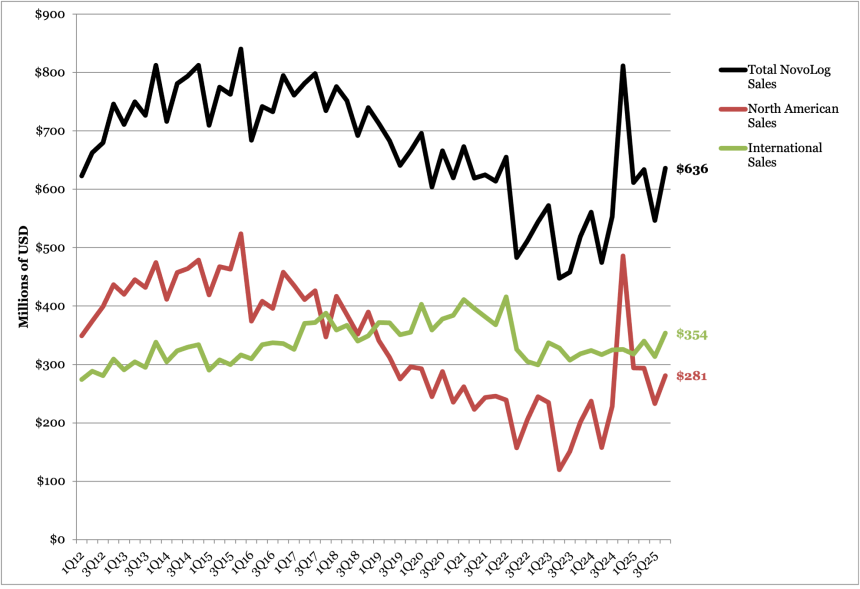

- NovoLog sales totaled $636 million (-24% CER, +16% Q/Q) and $2.5 billion in 2025 (-2% CER). By geography, North American sales totaled $281 million (-42% CER), and international sales totaled $354 million (-3% CER) in 4Q25. In 2025, NovoLog sales totaled $2.4 billion, down 2% CER from 2024.

- In 2024 and 2025, Novo Nordisk entered agreement with the US government to reduce drug prices. Under the first round of MDPNP agreement, Novo Nordisk has begun to provide rapid-acting insulins NovoLog and Fiasp at $199 per month, down 76% from the original list price of $495 per month, starting in January 1, 2026. Moreover, with the Most Favored Nation deal signed in November 2025, Novo Nordisk is expected to provide NovoLog and Tresiba for $35 per month supply. Given that the volume of insulin use in the Medicare population will not significantly increase, we imagine the new prices may further lower the revenue in future quarters.

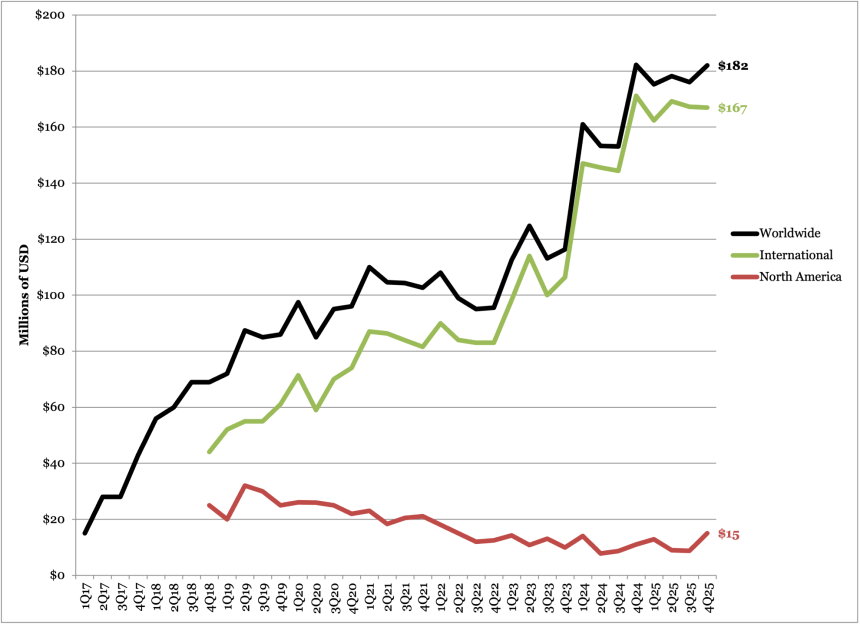

- Revenue for fixed-ratio basal insulin/GLP-1 RA combination Xultophy totaled $182 million, down 5% CER and up 3% sequentially. US sales totaled $15 million, up 33% CER and up 88% sequentially – demonstrating robust growth. OUS sales totaled $167 million, up 8% CER and flat sequentially. In 2025, Xultophy sales totaled $711 million, up 3% from 2024.

- Once-weekly basal insulin icodec, Awiqli, sales totaled $23 million in 4Q25, attributable to the more than a dozen countries in which it is approved, including Canada, the EU, Japan, Australia, and Switzerland for both T1D and T2D, and in China for T2D.

- In the US, in September 2025, Novo Nordisk announced its resubmission of its Biologics License Application (BLA) to the FDA for Awiqli in people with T2D, following the CRL in July 2024 raising concerns about the T1D indication. The resubmission is supported by the phase 3 ONWARDS program, which demonstrated robust A1c reductions with no significant increase in clinically significant hypoglycemia in people with T2D, compared to glargine or degludec. Novo Nordisk expects US decision in 1Q26.

Tresiba Worldwide Financial Results – Past Five Quarters

| Tresiba | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $391 (DKK 2.7) | $519 (DKK 3.6) | $441 (DKK 2.8) | $412 (DKK 2.6) | $479 (DKK 3) | $1,851 (DKK 12.1) |

| YOY (CER) Growth | +43% (+45%) | +30% (+27%) | +22% (+27%) | +24% (+31%) | +18% (+18%) | +21% (+26%) |

| Sequential Reported Growth | +30% | +31% | -22% | -6% | +16% | N/A |

Tresiba Sales – 4Q25 Geographic Results

| Tresiba | Revenue – USD millions (DKK billions) | YOY (CER) Growth | Sequential Reported Growth |

| US | $195 (DKK 1.2) | +106% (+41%) | -43% |

| OUS | $284 (DKK 1.8) | +6% (+6%) | -3% |

Tresiba Sales (1Q16-4Q25)

Fiasp Worldwide Financial Results – Past Five Quarters

| Fiasp | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $49 (DKK 0.3) | $121 (DKK 0.8) | $81 (DKK 0.5) | $99 (DKK 0.6) | $99 (DKK 0.6) | $433 (DKK 2.8) |

| YOY Growth | -46% (-45%) | +47% (+44%) | -9% (-5%) | +60% (+67%) | +154% (+67%) | +51% (+54%) |

| Sequential Reported Growth | -13% | +143% | -38% | +22% | +32% | N/A |

Fiasp Sales – 4Q25 Geographic Results

| Fiasp | Revenue – USD millions (DKK billions) | YOY Reported (CER) Growth | Sequential Reported Growth |

| US | $58 (DKK 368) | -- | +61% |

| OUS | $73 (DKK 469) | +5% (+7%) | +18% |

Fiasp Sales (1Q18-4Q25)

NovoLog Sales (1Q12-4Q25)

Xultophy Worldwide Financial Results – Past Five Quarters

| Xultophy | 4Q24 | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 |

| Revenue – USD millions (DKK billions) | $182 (DKK 1.3) | $175 (DKK 1.3) | $178 (DKK 1.1) | $176 (DKK 1.1) | $182 (DKK 1.1) | $711 (DKK 4.6) |

| YOY (CER) Growth | +62% (+64%) | +8% (+7%) | +6% (+10%) | +8% (+12%) | -10% (-5%) | +3% (+5%) |

| Sequential Reported Growth | +23% | -5% | -6% | -1% | +4% | N/A |

Xultophy Sales – 3Q25 Geographic Results

| Xultophy | Revenue – USD millions (DKK billions) | YOY Growth | Sequential Reported Growth |

| US | $15 (DKK 93) | +22% (+33%) | +88% |

| OUS | $167 (DKK 1.1) | -11% (-8%) | flat |

Xultophy Sales (1Q17-4Q25)

Pipeline Highlights

1. Pipeline updates: New data for CagriSema and amycretin highlight next‑generation incretin potential

The company continues to advance multiple late-stage assets, positioning its pipeline for continued leadership in obesity and cardiometabolic disease.

- CagriSema (fixed-dose combination of semaglutide 2.4 mg and cagrilintide 2.4 mg). For people with T2D, this past week, the company announced positive topline results from the phase 3 REIMAGINE 2 trial (n=2,728), which evaluated CagriSema in adults with T2D inadequately managed on metformin with or without SGLT-2 inhibitors. At Week 68, CagriSema demonstrated superior A1c reduction of 1.91 percentage point (vs. 1.76 percentage points with semaglutide 2.4 mg alone) from a mean baseline of 8.2%. While a 10% differential in A1c was positive, the ~34% weight loss seen with CagriSema was very striking. This follows the results from the REIMAGINE 3 trial (n=274) from 4Q24, in which CagriSema demonstrated a 2.3 percentage point reduction in A1c, as well as a 12% reduction in body weight, in people with T2D on once-daily basal insulin with or without metformin.

- Looking forward, the REIMAGINE 1 trial (n=189) of CagriSema vs. placebo in people with T2D treated with diet and exercise is expected to read out in 1Q26. In addition, the company will discuss the regulatory pathway for CagriSema in T2D, following results from the ongoing REDEFINE 3 CVOT (n=7,000), which is expected to complete in October 2027.

- In people with obesity, the company submitted a New Drug Application (NDA) to the FDA in December 2025 for CagriSema as an adjunct to lifestyle intervention for the management of long-term weight loss in adults who are overweight or have obesity and at least one weight-related comorbid condition.

- Results from the phase 3b REDEFINE 4 trial (n=809) comparing CagriSema vs. tirzepatide 15 mg in adults with obesity are expected in 1H26. During Q&A, Novo Nordisk reaffirmed its confidence in the CagriSema program, clarifying that REDEFINE 4 (n=809) mirrors the dosing approach used in REDEFINE 1 (n=3,417) and will test noninferiority before testing superiority against tirzepatide. He emphasized that learnings from REDEFINE 1 – particularly the need for longer-duration studies to fully capture weight‑loss trajectories – shaped the design and expectations for the broader REDEFINE series, including the ongoing REDEFINE 11 trial, expected to complete in October 2028.

- Separately, the company plans to initiate phase 3b trial of cagrilintide high-dose in 2H26.

- Semaglutide 7.2 mg. High-dose semaglutide has achieved several regulatory milestones. In the US, the company filed with the FDA for approval in people with obesity under the CNPV pilot program in November 2025, with US decision expected in 1H26. In the EU, high-dose semaglutide (7.2 mg) and its single-dose-device formulation for obesity have been submitted to the regulatory authorities in July and October 2025, with decisions expected in early 2026 and 2H26, respectively. Excitingly, in January 2026, the UK’s MHRA approved 7.2 mg dose of Wegovy for adults with obesity, which will be delivered as three injections of semaglutide 2.4 mg. In the ongoing regulatory discussions, we hope titration can be a major area of focus.

- The submissions are based on the results of the STEP UP (n=1,407) and STEP UP T2D (n=512) program presented at ADA 2025, in which semaglutide 7.2 mg achieved up to 21% weight loss across several trials.

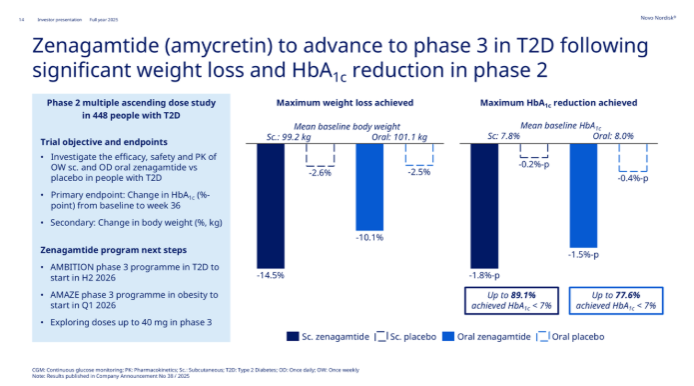

- Zenagamtide (amycretin). The company announced topline results of the phase 2 trial (n=448) in November 2025. In people with T2D, subcutaneous and oral amycretin conferred up to 15% and 10% weight loss, respectively at Week 36, compared with 3% for placebo. Amycretin also demonstrated a mean A1c reduction of 1.8 percentage points with the injectable formulation and 1.5 percentage points with the oral formulation, compared with 0.2 and 0.4 percentage points with injectable and oral placebo, respectively. Looking forward, the phase 3 AMAZE program for obesity will begin in 1Q26 and AMBITION trial for T2D in 2H26. The company plans to explore doses up to 40 mg. As background, the phase 2 trial evaluated doses up to 40 mg for subcutaneous formulation and 50 mg for oral formulation.

- UBT251 (tri-agonist). While not discussed in the call, Novo Nordisk will initiate phase 2 trial in 2H26. According to 3Q25 call (slide 78), tri-agonists are designed to offer greatest weight loss, surpassing CagriSema and amycretin.

Close Concerns’ Questions

1. How does the company expect the 2027 policy change implementation to reshape Ozempic’s revenue profile?

2. How do patients initiating oral Wegovy differ from those initiating injectable Wegovy? What different patient segments are the two formulations addressing?

3. How might the flexible dosing titration scheme used in REDEFINE 11 inform real-life titration in clinical settings? How will it impact discontinuation rates?

4. How does the company plan to position oral amycretin relative to Rybelsus, oral Wegovy, and future oral incretin candidates?

5. How is early OUS uptake informing expectations for US launch readiness for Awiqli?

6. What might leadership changes signal for the future of Novo Nordisk? What do the new leadership members, Mr. Jamey Millar (EVP, head of US operations) and Ms. Hong Chow (EVP, head of Product and Portfolio Strategy), hope to bring to the company?

--by Kayla Mathieu, Jeremy Alkire, Kat Moon, Monica Oxenreiter, and Kelly Close

Analysts’ Q&A

On guidance

Q (James Quigley, Goldman Sachs): Thanks for taking my question. First, I’m just trying to triangulate your guidance. You're suggesting low-single-digit growth in international operations and, that would suggest minus 20% in the US. Could you give us a sense of how this breaks down between volumes and price at a high level, particularly given your key competitors suggested those are mid-teens pricing on a global basis this morning?

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): With the International Operations delivering 8% growth in the fourth quarter of last year and around 10% in the second half, that's the run rate we're entering 2026. Then, adjust for LoE in specific markets on semaglutide, then you get to mid-single digit growth for International. And consequently, based on our guidance, then residual leaves the US growth to be in the teens in terms of sales decline. So, that's the key factors.

I would say the US decline is driven by price declines, and it's driven by both investments in market access; The cash channel in the US is also being built at a different price point, so channel mix is a factor. And then the MFN impact, where we announced a quarter ago that it will have a low single-digit impact on group sales. So, meaning roughly double in the US. So, the key notion is of course with these price reductions, to what extent are we then able to convert that into expanding volume reach and volumes in the marketplace?

It's early days. We have built assumptions in. Clearly, we've looked at the first four weeks of the Wegovy pill launch where we're very encouraged, as Dave showed just before, and the same on Wegovy injectable. We're looking to the tune of 30% of Wegovy injectable scripts now being cash driven, so also building on that. We are seeing a volume response to the lower prices. Exactly how the year pans out remain to be seen because we have a number of variables at play. But it is price declines that drive the US down.

Q (Sachin Jain, Bank of America): I've got two more on guidance, if I may. Framing James's question slightly differently, I think you roughly phrased it as underlying growth, less three sets of headwinds, are often low-single-digit. I'm just trying to understand between 3Q25 and the guidance today, what shifted you from that sort of low-single digit to now minus 5% to 13%. So, the mid- to high-single digit delta versus consensus, how much that is volume and price, and within pricing dynamics, what's the new component? Second, I have a question on what needs to happen for you to achieve the bottom end of your guidance. Thank you.

A (Mr. Mike Doustdar, President and CEO): As you recall, I didn't guide for 2026 at our 3Q25 call, so that's the starting point. As we also note in our current release, we based our guidance on the latest trends we see in the market. The guidance we put out now is based on the run rate we left 2025 with, so 4Q25 performance, as I alluded to before, and then whatever triggering events and expectations and assumptions around the future that we have. So those are the key parts that we build in.

What do we know more today compared to 3Q25? We have some more nuances on the run rate in international operations. You see the 8% growth in the fourth quarter and of course, some more market intel on more detailed pricing and reimbursement choices in some of the markets there. In the US, what we know that beyond the 4Q25 closeout is really about the Wegovy pill uptake in the first month, as Dave alluded to, which we're very happy with, and then the Wegovy injectable cash business and the response to the lowering of the initiation prices to $199. So that's really kind of the key fundamental changes since three months ago.

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): It's important to remember that we've been experiencing this for some years now, that the obesity market is significantly more dynamic than most other markets, where it's much more stable prescription trends through normal GPs. The macro variable that can both be positive and negative is the dynamics in the obesity market. We’re not concerned about the expansion of the markets. We saw it more than double in 2025. So we're very confident in continued expansion of the market, but the variables I'm alluding to are competitive dynamics, as always, gross to net dynamics that are being forecasted with a lag, and then also the sourcing and channel dynamics impacting pricing and volume of Wegovy pill, and how that is impacting both Wegovy injectable but also how a competitive launch plays into all of this. So, I'd say it's classic variables, but it's in a very dynamic market segment.

Q (Peter Verdult, BNP Paribas): I'm not going to ask you to go line by line every assumption, but can you comment on the spirit of the guidance you provided? Is this reflecting genuine concerns on competition, or are you simply starting the year as conservatively as you can to prevent this persistent earnings downgrade story from continuing through 2026?

A (Mr. Mike Doustdar, President and CEO): I'll start by saying we have all acknowledged how volatile and dynamic the obesity market is with lots of moving parts. The way we guide is we discuss and talk to our operating units. We look at the macro trends and put the latest information we have in place. We start by looking at the last year's finish and the run rate to that, especially the fourth quarter, but even more so gradually looking at the three months within the Q4 data that we have available. So, that's a starting point.

Then, we go ahead and try to see the new data we have available. Karsten alluded to it. We have four weeks of pill data. It's incredibly encouraging. And we consider that and it's in the guidance basically, of course not fully knowing what's going to happen the next 11 months, but we make some good assumptions around that. There are also things that we have previously discussed with all of you. Think about the LOE in international operations. That hasn't really changed. It was there before, and it is there now. We have not seen the impact of that yet. It will come into place starting from 2Q26, and so will some of the other things on the op side that will come in 2Q26.

We also touched upon Medicare. Medicare is a group of people that we would love to provide GLP-1 products to, but we haven't started yet, and it's going to get going in the second part of the year. So we make assumptions around that. We put the midpoint and our own targets and then we give it the plus and minus the four points on each side, and that's how we've done it in the past. That's how we've done it this year.

Q (Simon Baker, Rothschild & Co): Two quick questions, if I may. The first one really is just going back to the guidance question that's been repeatedly asked. Conceptually, would it be fair to say, because you have high visibility on pricing impact and low visibility on volume uplift, that it is one of the key things that is reflected in your guidance? Second, could you update us on your assumptions for generic competition in IO, specifically Canada? The reason I ask is we understand that all of the semaglutide generics have had notices of deficiency slapped on them by Health Canada, and the expectation is they will not resolve until the midyear. So, generic semaglutide in Canada is a 2H26 rather than a 1H26 phenomenon. I'd be interested to get your thoughts on that and the extent, if any, to which that's reflected in the guidance.

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): I'd say for mature reimbursed brands, I think they have very mature established trend lines for volume trends measured as TRx, and we have a good feeling for the prices being contracted, et cetera. So, for our mature reimbursed brands, I'd say that's reasonably straightforward. Where we see the uncertainty is in the self-pay channel, because the price elasticity in the self-pay channel is something that we're still exploring. As Dave was covering before, we've seen a fantastic uptake of the Wegovy pill here in the first four weeks. But we also know that obesity self-pay is a super-dynamic segment. So, exactly how that works across a year, to what extent there's seasonality, et cetera, sourcing, cannibalization, competition. Clearly, there are uncertainties there, and we put our best assumptions in and it can go both ways. We can both have an upside and a downside, and that's why we work with a range.

For Canada specifically, as we said in prior quarters, semaglutide loss of exclusivity in international markets will impact group sales by low single-digits. Canada is the biggest contributor. And of course, we put in assumptions around timing of generic approvals and launches. We don't have detailed insights into the status of those files and remediation of these Notices of Deficiencies. But obviously, the time is the key variable in terms of impact. I think the direction of travel is the same, but there could be both an upside and a downside to our guidance, depending on the pace of approval of generics in Canada. So, it remains to be seen.

On Medicare

Q (James Quigley, Goldman Sachs): On the Medicare and MFN deal, how are you thinking about the potential speed here? Your competitor suggested the unlock could be pretty fast starting from July 1, but the guidance suggests slower uptake here, so what are the basis of your assumptions around the speed of unlock?

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): On Medicare and impact from Medicare Part D and the MFN deal, we do expect that we will have a benefit starting around mid this year, having Wegovy reimbursed in Medicare Part D, and hence, being available for seniors under a reimbursed setting. We have included that in our guidance. But at this point, given the lag times of educating physicians and admin staff, understanding how it works, and for patients to access that benefit, it will be a gradual ramp with limited benefit this year and a bigger benefit into 2027.

On oral Wegovy

Q (Richard Vosser, JPMorgan): Thinking about formulary access for Wegovy, you highlighted the access for oral Wegovy in a pill, but how are you thinking about that access in the commercial channel this year? It seems like maybe employers would be incentivized to maybe reduce access, given the availability of products in the cash channel at lower prices. So, just your thoughts on that and how that might affect the mix and volumes in that channel.

A (Mr. David Moore, Executive Vice President of US Operations): On the injectable side, we see relatively stable access. And, of course, we have discussions every year to maintain that level of access. And you've heard us talk about before, we're very interested in reducing that friction and making the experience easier for patients. We did have some states that have decided to not cover AOMs. For example, California is a big one, but I will say that with the lower prices that are available today, we will continue to reengage with those states with the hopes that we can increase access in Medicaid as well.

On the pill side, what you heard me mention is we've seen some positive progress in just the first month. We started out the month of January having CVS covering it right out of the gate, and then we quickly were able to add Prime, Optum, and Anthem, and we will continue to build that over the course of the year. We expect that there will be both plans and employers that will be interested in covering the pill.

Q (Mike Nedelcovych, TD Cowen): Given the strong launch of Wegovy pill, is there any risk of supply outages in 2026? For example, if adoption persists at this current high level, could Novo service that demand through the end of the year with its current capacity?

A (Mr. Mike Doustdar, President and CEO): Over the last period, I have spoken on a number of occasions to how confident we are with regards to the Wegovy pill supply. We have said that we launched the pill in the US at a time where we will be confident enough to know we will not run into a supply situation anymore. We have seen an incredible uptake in the first month. Today, I will reaffirm to you that we feel incredibly confident that we will be able to supply the US market.

Q (Harry Sephton, UBS): I want to start by asking what your expectations are for the sustainability of the Wegovy pill demand. Is there any evidence from Novo Nordisk's Rybelsus experience that points to any variation in the stay time on therapy versus the injectable, and how to think about the demand for the pill through the competitor’s orforglipron launch? And then, my second question is on the economics of the Wegovy pill. Given the much lower price point and the much higher API demand, how does the gross margin contribution of the Wegovy pill compare to the injectable?

A (Mr. Mike Doustdar, President and CEO): When you think about the sustainability of a growth and demand, two things come to my mind. Competitive pressure, as well as how much you push yourself into doing something despite the competitors. Let me start with the first one. We have gone all-in. This has been the best launch, partially also because we have really put in all the activities and the promotions that we could think of, not least of course the partnership with all of our e-health players. Being available in 70,000 retail pharmacies today has been partially the reason behind that incredible uptake.

But then, of course, the question comes, what happens after competition arrives? Can you uphold this? Is it sustainable? I would say that the last two years has taught us something very specific with the obesity market. It has taught us that the number one criterion for a patient picking up anti-obesity medication is the magnitude of weight loss. And when you look at this, then you realize, based on our latest trial, we have shown that when you take the drug, the Wegovy pill gives you 16.6% weight loss, in addition to all the CV benefits and the great stuff that it has with 16.6% weight loss.

We've also read the data from our competing product and have seen that they are at 12.4%. If you round those things, then you get to 17% and 12%. If you ask pretty much any patients and certainly ask me, which one would you rather take, losing 17% weight loss or 12%, I know my answer. And we have seen the answer from 170,000 employees coming on very quickly, recognizing that this is not just a pill. It's a peptide. It's a large protein inside a pill that gives you that incredible efficacy. And that has been giving us a lot of optimism, and we will continue of course pushing this through and promoting it. Don't be surprised if you see in the big game on Sunday, you see us visible, and we will basically make sure that we'll do our utmost to make this pill a success.

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): On gross margin, the short version is that the gross margin on Wegovy pill is below that of Wegovy injectable, but it's important to know that it's lower on gross margin level, but it's still an attractive gross margin. So we are all in pushing the pill. And, of course, the overarching intention is to expand the markets and not cannibalize from our own products.

Q (Thibault Boutherin, Morgan Stanley): On the profile of Wegovy pill, I want to understand the adherence. Could you help us understand what happens to a patient if they miss the pill for a day or a couple of day? How does that impact efficacy in terms of weight loss? And similarly on tolerability, if a patient is on the highest dose, and for some reason, miss a few days of pill, can they go back and resume on 25 mg, and how do side effects look like?

A (Mr. Martin Holst Lange, Executive Vice President of Development): On the Wegovy pill, we do know that in general, when patients are in chronic treatment, sometimes they skip a dose. It is important to remind ourselves that the half-life of semaglutide, once in steady state, is very long – in the subcutaneous state, this allows for once-weekly doses. That basically means that when you're on a stable dose on the Wegovy pill and then you skip a dose, it doesn't have a huge impact on your blood exposure in that period of time, and you can also then re-initiate at the 25 mg dose without experiencing any untoward effects. So, from that perspective, semaglutide is semaglutide, and we are benefiting from the long half-life of semaglutide also in the oral delivery. Other orals with shorter half-life would have a much different profile, because that would both impact the potential efficacy, but also the potential tolerability if you skip one or two doses.

On compounding

Q (Richard Vosser, JPMorgan): And maybe a second question on compounded volume. Obviously, a very strong oral launch, and you're saying new patients. But any evidence that those lower prices are stymieing the compounder volume and any idea that you're taking share using the oral from compounders?

A (Mr. David Moore, Executive Vice President of US Operations): We haven't seen a change yet. It's early days. The compounding market, what we're seeing right now is what we would consider relatively stable. I can tell you, as of this week, we have over 170,000 people that are on the Wegovy pill, and most of that is self-pay. And we get daily feeds, because of the way that we went to market. And so, we certainly expect that there could be some switching that's coming from compounding, but it's a little bit early to tell, and we don't get any of that longitudinal data. But we'll certainly be researching that as more data comes in.

On 7.2 mg Wegovy dosing

Q (Carsten Lønborg Madsen, Danske Bank): On the high-dose Wegovy approval, which we hopefully will see soon, will you be launching immediately? Can you confirm that and in which type of pen will you be launching?

A (Mr. Mike Doustdar, President and CEO): As you know, we have filed in December last year under the CNPV voucher program, and we have announced that we should expect the approval hopefully in this quarter. As soon as we get the approval, we are ready to launch. So, we will not sit on that regulatory approval. And we will go all-in again, because I think this is really important that the world understands that medicine is dosed differently, and depending on how you dose things, you get different effect of it.

And right now, semaglutide at 2.4 milligram is giving us 15%, 16% weight loss. Tirzepatide at 15 milligram dosing gives you 20%, 21%. We have shown in a step-up that when you increase the dose of semaglutide to 7.2 mg, you get very close to on par with tirzepatide. And I think it's actually very important that the world gets to know this, and then they can judge that on top of on par weight loss, you have also CV benefit, kidney benefit, and then a liver benefit, and then people can pick and choose which option they want. So, it's very important that we go all-in with that, and we're planning to do so.

On REDEFINE

Q (Peter Verdult, BNP Paribas): I realize you're not going to change the messaging on REDEFINE 4 at this juncture, but can you at least remind us on trial design? Was flexible dosing allowed as we saw in REDEFINE 1 or was it more fixed in nature for CagriSema and tirzepatide in REDEFINE 4? Are there any major trial differences we need to be aware of when we compare REDEFINE 4 to 1?

A (Mr. Martin Holst Lange, Executive Vice President of Development): So, REDEFINE 1, you're absolutely right. We basically have no new news. So, we're not going to change the story. REDEFINE 4 is comparing CagriSema and tirzepatide in an obese population on weight loss, assessing for noninferiority first, followed by superiority testing. The dosing was similar to REDEFINE 1. As you recall, we took some learnings from REDEFINE 1, including that we needed to do longer studies. And I think we maintain what we've always said for REDEFINE 4, but we also are looking forward to REDEFINE 1, where we'll see the full weight loss potential of CagriSema.

Q (Mike Nedelcovych, TD Cowen): Martin, I have to admit your response to the earlier question struck me as somewhat ominous. Why do you think we will have to wait for REDEFINE 1 readout to see the full weight loss potential of CagriSema? Why could it not be revealed by REDEFINE 4, given the changes that were made to the trial?

A (Mr. Martin Holst Lange, Executive Vice President of Development): On REDEFINE 4, we always have to think about, when we do amendments to ongoing trials, we cannot fully guide what will happen. We can extend the study. But we also have to acknowledge that the learnings that we took from REDEFINE 1 was, in part, we needed to do longer treatment duration. But it was actually also paradoxically, in part, to drive even more flexible dosing, securing that we actually get more patients to the highest target, but using longer time. That, we cannot change in REDEFINE 4. We have optimized that in REDEFINE 1.

We tried to optimize the trial duration in REDEFINE 4. But in REDEFINE 1, we have taken all the learnings on what we call flexible titration. I'm not sure I still like the word, but we put what we call flexible titration to use in REDEFINE 1. We can already now see that that does really make a difference to the patients and how they act in the trial. So, I still have a lot of optimism on REDEFINE 4. But I think the full weight loss potential, we'll only learn when we do the full trial duration and the flexible dosing that really will drive patients to use CagriSema in the optimized way.

On Ozempic and MFN pricing

Q (Thibault Boutherin, Morgan Stanley): When does the MFN negotiated price kick in for Medicare and Medicaid this year? And is there any associated volume uplift, given it's already covered, or should we expect market share loss to sort of erase the benefit?

A (Mr. David Moore, Executive Vice President of US Operations): With respect to Ozempic, as you know, we have Medicare coverage right now in diabetes. And so, with respect to MFN, as well as MFP, that's more of a 2027 event. Of course, you know, we did make Ozempic available in self-pay. As I mentioned, we're seeing about 8,000 scripts a week now in self-pay for those patients that don't have coverage. But the MFN and MFP is more of a 2027 event.

On CapEx

Q (Carsten Lønborg Madsen, Danske Bank): In terms of CapEx this year, for a relatively high CapEx level in terms of billions being spent, can you confirm that the API build-out is on track, because it feels like this entire program is taking longer and is being much more expensive than what we expected some years ago?

A (Mr. Karsten Munk Knudsen, Executive Vice President & CFO): And as I said early on then, we are moving downwards in terms of CapEx. This is the first step-down, and then we expect to see a steeper slope in the coming years. And it really links to finalization of projects approved in prior years. As it is with projects, some are ahead, some are behind. But in the broad scheme, we are on track. Specifically, for API, we do expect to have some of the new major API facilities online already this year and more to come in the coming years.