JPM 2026 Full Report –

Executive Highlights

- The 44th Annual JP Morgan (JPM) Healthcare Conference wrapped earlier this month at the Westin St. Francis Hotel in San Francisco. This year, the meeting convened 525 companies and over 9,000 attendees across the healthcare industry, from large pharmaceutical and device companies to early clinical-stage biotech firms and non-profit organizations. We appreciate JPM for organizing dynamic conversations on innovation, market changes, and health policy.

- Diabetes, obesity, and cardiometabolic disease remained dominant themes throughout the conference,reflecting the continued importance of these conditions in both clinical innovation and commercial focus. Across presentations, speakers discussed therapeutic efficacy alongside maintenance and long-term clinical outcomes. GLP-1 RAs and other next-generation incretin-based therapies were featured prominently, with expanding discussion around combination therapy approaches and differentiation between incretins beyond degree of weight reduction.

- Technology and data infrastructure were discussed as critical factors of scaling, with a strong focus on CGM, AID systems, digital health platforms, and real-world data integration. Speakers highlighted the importance of interoperability and clinician workflow integration as patient adoption expands toward broader populations. Specifically, the opportunity to deeper penetrate US and international markets through coverage expansions and strengthened guidelines for both CGM and AID was a focus of conversation as companies explored how to bring their products to more patients.

- Beyond company updates, the conference hosted several fireside chats with leaders across the ecosystem to explore the present and future of the US’ healthcare ecosystem. JPMorgan CEO Mr. Jamie Dimon led the first of this series, touching on a variety of topics including his perspective on global affairs and the role of corporations and healthcare organizations in this ecosystem. Several administrators from CMS – including Dr. Mehmet Oz (CMS Administrator), Mr. Daniel Brillman (Deputy Administrator and Director), Ms. Stephanie Carlton (Deputy Administrator & Chief of Staff), Mr. Chris Klomp (Deputy Administrator & Director), and Ms. Amy Gleason (Strategic Advisor) – later joined to discuss their approaches to improving long-term US health, and US Commissioner of Food and Drugs Dr. Marty Makary gave a talk on multiple initiatives at the FDA and innovation within the context of population-level health outcomes.

- See our top highlights below across pipeline innovation in diabetes therapy and technology, clinical trial advancements, US public health policy, AI’s role in healthcare, and the economic and geopolitical climate. For a look at our on-the-ground view of the conference, see our Day #1, Day #2, Day #3, and Day #4 coverage, as well as our Resource Hub.

Table of Contents

-

Diabetes Therapy Highlights

- AbbVie: Interest in entering obesity arena by leveraging familiarity with cash-pay channel and compounding market

- Amgen: PCSK-9 inhibitor Repatha highlighted as key to Amgen’s growth through 2030; extensive discussion of long-acting T2D and obesity candidate MariTide

- Amphastar: Dr. Jack Zhang shares updates on glucagon, GLP‑1 RAs, and insulin biosimilars

- Arrowhead Pharmaceuticals: RNA interference treatments for obesity to advance to phase 2b trial

- AstraZeneca: Cardiometabolic focus for 2030 and beyond led by aldosterone synthase inhibitor baxdrostat, PCSK-9 laroprovstat, and GLP-1 RAs in development

- Bayer: Kerendia (finerenone) demonstrates blockbuster potential for CKD and heart failure; pricing pressures with Eylea (aflibercept)

- Biocon: Addressing global non-communicable diseases like diabetes; generics and biosimilar business restructuring

- Biomea Fusion: Phase 2 data for Icovamenib and phase 1 results of GLP-1 RA BMF-650 expected in 2026

- Corcept Therapeutics: Dr. Joseph Belanoff highlights broad implications of cortisol modulation, including hypercortisolism, obesity, and diabetes

- Esperion: Updated US lipid-lowering guidelines to include bempedoic acid offering; international expansions; combination therapy

- Ionis Pharmaceuticals: Tryngolza gains traction in treatment of FCS ahead of broader launch; pelacarsen for Lp(a) risk reduction on track for launch in 2027

- J&J: CEO Mr. Joaquin Duato outlines diversified growth strategy with momentum in cardiovascular portfolio

- Kailera Therapeutics: CEO Mr. Ron Renaud highlights diversified GLP-1 RA pipeline for obesity treatment

- Lexicon Pharmaceuticals: Dr. Mike Exton highlights SGLT-1/2 inhibitor sotagliflozin, pilavapadin for DPN, and non-incretin obesity candidate

- Lilly: Mr. David Ricks shares insights about obesity market, payment channels, and clinical pipeline including orforglipron

- Madrigal: “10% of 10%” of global MASH patients treated; detailed approaches to combination therapy including GLP-1 RAs and DGAT-2 inhibitors

- Merck: “Democratizing” PCSK9 therapy and combinations with Lp(a); MK 3000 as a potential new mechanism of action for diabetic macular edema

- Novartis: De-risked pipeline driving post-Entresto growth; Leqvio as the foundational therapy for the company’s cardiorenal metabolic franchise

- Novo Nordisk: Mr. Mike Doustdar on mastering cash channel, reframing perception of the semaglutide, and clinical pipeline with CagriSema, cagrilintide, and amycretin

- Pfizer: Dr. Albert Bourla shares vision of obesity treatment landscape with Metsera’s assets and reflects on MFN and tariffs

- Regeneron: CEO Dr. Leonard Schleifer and CSO Dr. George Yancopoulos emphasize internal R&D engine, Eylea HD momentum, and obesity strategy

- Roche: Targeting a “top three” role in obesity through petrelintide, pegozafermin, and more; anti-VEGF Vabysmo returns to growth after market challenges

- Sana Biotechnology: Continuing strides for allogeneic islet cell therapy with developed with hypoimmune technology in people with T1D

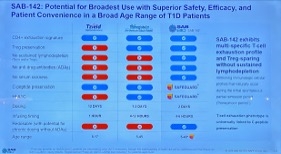

- SAB Bio: Mr. Samuel Reich on differentiating features of SAB-142 as a disease modifying therapy for T1D

- Sanofi: Strategies and progress across mid- to late-stage development projects; teplizumab receives approval in the EU for stage 2 T1D

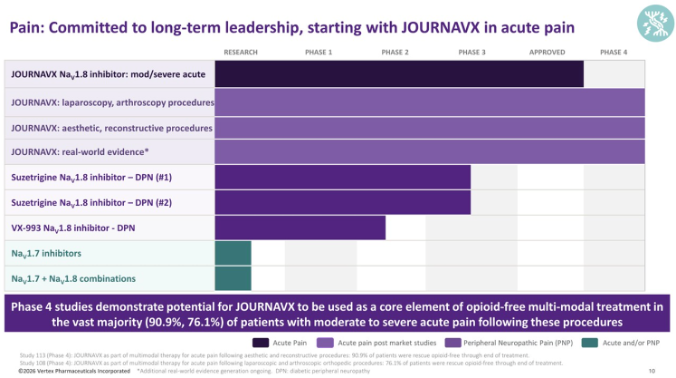

- Vertex: Journavx (suzetrigine) shows strong growth in the pain sector with potential indication for diabetic peripheral neuropathy

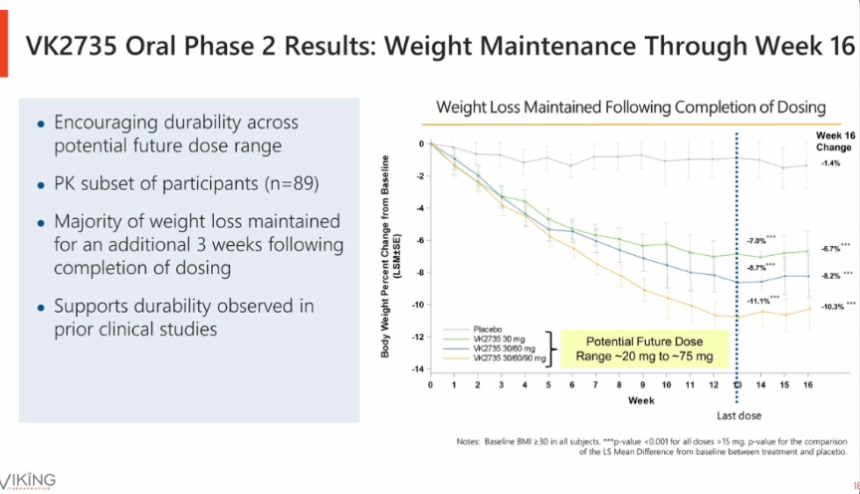

- Viking: Dr. Brian Lian highlights oral and injectable VK2735 (dual GLP-1/GIP RA) and amylin agonist for obesity

- Zealand Pharma: Dr. Adam Steensberg highlights survodutide and petrelintide; clinical data expected in 2026

-

Diabetes Technology Highlights

- Dexcom: Preliminary full-year 2025 revenue of $4.66 billion (+16%) and 4Q25 revenue of $1.26 billion (+13%); global userbase grows over 25% to 3.5 million

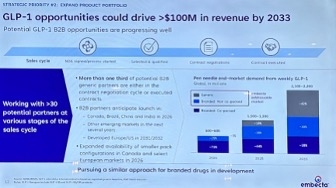

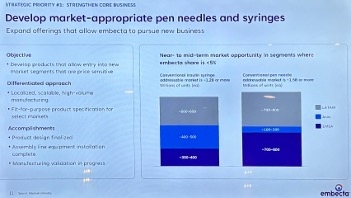

- embecta: GLP-1 RAs offer >$100 million annual opportunity; “market-appropriate” products for China and other geographies

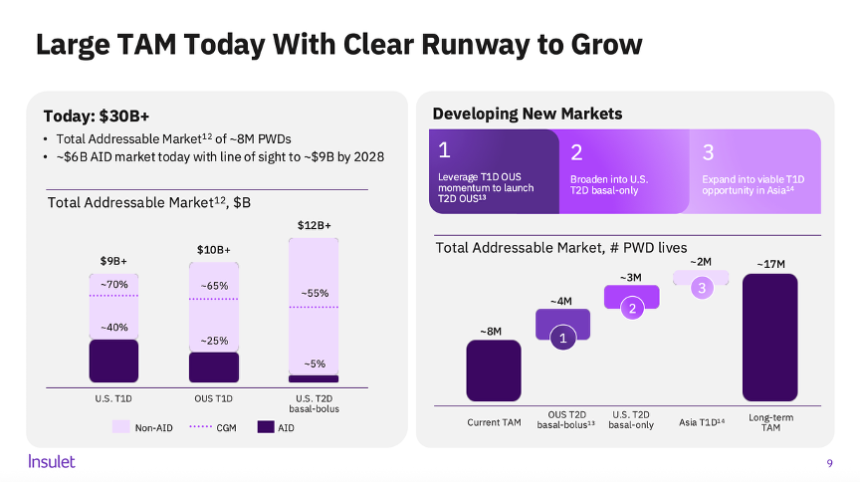

- Insulet: President and CEO Ms. Ashley McEvoy highlights growth opportunity across US T1D, US T2D, and OUS T1D; robust innovation pipeline through 2028

- Medtronic: With Diabetes business spinoff expected by the end of 2026, management highlights four new generational growth platforms

- Omada Health: Preliminary full-year 2025 revenue of ~$257 million (+52%); 2026 will see investment in GLP-1 RA Care Track and AI tools

- Teva Pharmaceuticals: Teva to shift from generics firm to global biopharmaceutical company

- Verily: Progress on Verily Pre for clinical research facilitation and Verily Me for telehealth

- Virta Health: Tailwinds from GLP-1 RAs; combining the platform with pharmacotherapy for sustained weight loss and metabolic benefit

- Ypsomed: CFO Mr. Samuel Künzli reviews product launches and global manufacturing expansion in 2025; one billion unit manufacturing capacity targeted for 2030

- JPM’s Jeremy Meilman welcomes over 9,000 attendees, reflecting on four decades of global health industry

- San Francisco Mayor Mr. Daniel Lurie welcomes business, scientific, and medical leaders to San Francisco

- Fireside Chat Fascinates: JPMorgan Chase CEO Mr. Jamie Dimon in conversation with Ms. Terry-Ann Burrell on geopolitics, the free market, leadership suggestions, and healthcare innovation

- *NEW* Mass General Brigham: Systemwide transformation and strategic expansion

- *NEW* Cleveland Clinic: Applying AI and delivering complex care at a global scale

- *NEW* Mayo Clinic: Embedding AI across care, research, and operations

- *NEW* Intermountain Health: AI and proactive care across the American West

- CMS comes to SF: Dr. Mehmet Oz and CMS leadership discuss GLP-1 RAs, long-term health, MFN, and MAHA

- The FDA’s Dr. Marty Makary on optimized regulation, accelerating the 12-year approval timeline, and additives in our food supply

- From agentic AI to longevity: ARPA-H’s strategy for breakthrough health innovation

- Employer coverage at crossroads: Managing GLP-1 RAs and breakthrough therapies

- Technology and strategy to capture Asia’s growing patient markets

- The growing strength of Chinese biotechnology: Gaining trust and partnership

Diabetes Therapy Highlights

AbbVie: Interest in entering obesity arena by leveraging familiarity with cash-pay channel and compounding market

In this morning session, CEO Mr. Robert Michael shared updates on AbbVie. As background, AbbVie is a global pharmaceutical company with a market cap of $390 billion. Its focus areas span immunology, oncology, neuroscience, ophthalmology, aesthetics, and infectious diseases. Blockbuster drugs include autoimmune disease medications Humira (adalimumab) –which is now facing loss-of-exclusivity – IL-23 inhibitor Skyrizi (risankizumab-rzaa), and JAK inhibitor Rinvoq (upadacitinib). Botox (onabotuliumtoxinA) used for cosmetic purposes is also a multi-billion-dollar product made by AbbVie.

- AbbVie expresses interest in entering the obesity arena. In March 2025, AbbVie entered a partnership with Gubra to develop and commercialize a long-acting amylin analog, GUB014295, for obesity. Mr. Michael said that amylin agonist class is promising due to its favorable tolerability profile. AbbVie will continue to expand its obesity portfolio beyond GUB014295 through business development and licensing strategy and plans to differentiate its portfolio with improved tolerability and durability of weight loss. Moreover, Mr. Michael believes that AbbVie is well-positioned especially given its familiarity with the cash-pay channel and compounding market. Notably, the compounding business had become the second largest segment in the aesthetics market “over a matter of a few quarters.”

- As a reminder, the candidate conferred dose-dependent weight loss up to 3% at six weeks, compared to 1% weight gain with placebo, in a phase 1 SAD trial. The candidate is currently evaluated in a phase 1 multiple ascending dose (MAD) study (n=124), which is recruiting participants and is estimated to complete in April 2026. While early, Mr. Michael said that the candidate has a potential to be “differentiated amylin,” and is eager to see more data.

Amgen: PCSK-9 inhibitor Repatha highlighted as key to Amgen’s growth through 2030; extensive discussion of long-acting T2D and obesity candidate MariTide

Amgen CEO Mr. Robert Bradway discussed Amgen’s approach to general medicine in great detail, including MariTide, Repatha (evolocumab), and olpasiran, which are major cardiovascular therapies for the company. Mr. Bradway first highlighted Amgen’s “broad and deep” portfolio across four therapeutic areas: general medicine, rare disease, oncology, and inflammation. He emphasized consistent execution across financial performance, regulatory progress, and late‑stage pipeline advancement. The company had five successful FDA approvals in 2025, with 10% year-over-year revenue growth and 14 products annualizing at $15 billion. In general medicine, Amgen is focusing on heart attacks, stroke, hypercholesterolemia, osteoporosis, chronic weight management, T2D, and obesity-related conditions. Repatha, a PCSK-9 inhibitor that lowers LDL cholesterol levels to prevent strokes and heart attacks, received high attention throughout the presentation, as did GIP antagonist/GLP-1 RA MariTide and Lp(a)-lowering olpasiran. Looking ahead, Amgen is developing a number of key therapies and is further integrating new technology and AI into its research and commercialization processes. Mr. Bradway also discussed the recent acquisition of Dark Blue Therapeutics and Disco Pharmaceuticals as opportunities for further growth.

- GIP antagonist/GLP-1 RA MariTide was discussed in detail, underscoring its potential as a differentiated long‑acting therapy for both obesity and T2D. Looking back at 2025, Mr. Bradway highlighted the six global phase 3 studies of MariTide that Amgen initiated in 2025. The company sees opportunity for MariTide in chronic weight management, atherosclerotic cardiovascular disease, heart failure, obstructive sleep apnea, and T2D. Phase 2 data showed robust reductions in A1c and weight with monthly dosing, alongside favorable cardiometabolic improvements and a tolerability profile consistent with the GLP‑1 class. In chronic weight management, the majority of participants who achieved ≥15% weight loss maintained the loss for a second year on lower monthly or quarterly dosing, with very low rates of nausea and vomiting. He said that the therapy has garnered high interest with its differentiated approach to obesity and related conditions. He highlighted MariTide’s strong treatment efficacy with monthly or even quarterly dosing in development, and that tolerability at initiation improves with multi-step dose escalation. Mr. Bradway also said that the therapy is very well tolerated at target doses and at maintenance doses. Amgen expects to establish the use of MariTide as a long-term maintenance therapy and as potentially the first monthly therapy for T2D. The company is preparing a phase 3 program to evaluate MariTide in T2D.

- The six phase 3 studies are:

- MARITIME-1, which has completed enrollment in adults living with obesity or overweight but without T2D;

- MARITIME-2, which has completed enrollment in adults with obesity or overweight with T2D;

- MARITIME-CV, which is enrolling adults living with established ASCVD and obesity or overweight;

- MARITIME-HF, which is enrolling adults living with heart failure with preserved or mildly reduced ejection fraction and obesity; and

- MARITIME-OSA-1 and MARITIME-OSA-2, which were both initiated in 3Q25 in adults living with obstructive sleep apnea.

- Recall that full results of the 52-week phase 2 trial of once-monthly MariTide in obesity with and without T2D were presented at ADA 2025. Major takeaways included the high GI adverse event rates despite robust weight and A1c reductions. In the treatment efficacy estimand, MariTide conferred up to 20% weight loss vs. 2.6% with placebo at 52 weeks. For the treatment policy estimand, MariTide conferred up to 16% weight loss compared to 2.5% with placebo.

- GI adverse events. Rates of nausea and vomiting were very high across the MariTide arms. In the non-dose escalation arms, nausea was reported by 77-87% of participants, and vomiting was reported by 68-92% of participants. Dose escalation appeared to lower the rates of adverse events; however, nausea, vomiting, and constipation rates still remained high. During today’s presentation, Mr. Bradway characterized the safety and tolerability profile as consistent with the GLP-1 RA class overall and focused on the therapeutic promise of a once-monthly or once-quarterly drug. He said that real-world experience with incretins has always demonstrated challenges such as high discontinuation rates, high treatment burden, and high required dosing frequency. Amgen believes that MariTide is suited to this challenge and that quarterly dosing can still maintain weight loss. In the second year of MariTide treatment, the therapy was very well tolerated including at quarterly doses, with a very low incidence of nausea and vomiting and no new safety signals observed.

- The six phase 3 studies are:

- PCSK-9 inhibitor Repatha is one of six major growth drivers for Amgen, expected to be a key driver of product sales in 2026 and through the end of the decade. Mr. Bradway highlighted the therapy’s strong commercial performance, up 33% from 4Q24 and annualized at approximately $3 billion, and pointed to the October 2025 VESALIUS‑CV results showing a 36% reduction in first heart attack among patients without prior cardiovascular events and 25% reduction in 3-point MACE. Mr. Bradway emphasized that more than 100 million people worldwide are not at LDL‑C targets, and penetration is still in the single digits. Amgen sees a substantial runway for expansion. He highlighted the strong clinical evidence supporting the use of the therapy and its ability to reduce in risk of first myocardial infarction in people who have never had one. During Q&A, Mr. Bradway said that Repatha was the first therapy with such demonstrable preventative effects and that it provides a new therapeutic option for patients who otherwise have optimized care, including with statins. He said that Amgen hopes to “change heart disease’s status as one of the world’s leading killers.”

- In November 2025, full results of the phase 3 VESALIUS-CV study (n=12,257) were presented at AHA, which evaluated the effects of PCSK-9 inhibitor Repatha (evolocumab) in people with high CV risk without prior atherosclerotic CVD (myocardial infarction [MI] or stroke) – including people with diabetes and/or atherosclerosis. Impressively, evolocumab conferred 20% risk reduction in all cause death, 25% risk reduction in MACE-3, and 19% risk reduction in MACE-4 at five years.

- Olpasiran, first-in-class siRNA molecule targeting Lp(a), was also highlighted for its innovative promise in general medicine. Mr. Bradway highlighted olpasiran as one of Amgen’s most important late‑stage cardiometabolic programs, emphasizing its potential to address what he described as the “residual risk” in cardiovascular disease. He noted that one in five people carries genetically elevated Lp(a), a risk factor that cannot be modified by diet or exercise, and reiterated that phase 2 data showed 95–100% reductions in Lp(a). Amgen expects the phase 3 Ocean(a)-Outcomes trial (n= 7,297) to clarify whether lowering Lp(a) can meaningfully reduce cardiac events, and Mr. Bradway stressed that if the trial confirms this, olpasiran could represent a major advance for patients at high cardiovascular risk. Mr. Bradway noted that results are expected sometime in 2027.

- On biosimilars, Mr. Bradway highlighted that through 3Q25, biosimilars grew 42% from 4Q24, and the portfolio has now generated ~$13 billion in cumulative revenue. He framed the business as a demonstration of Amgen’s ability to “reliably and safely supply” complex biologics at scale, with the slides noting that the second wave of launches (including Eylea biosimilar Pavblu) is driving current growth while a third wave advances through phase 3 development.

Amphastar: Dr. Jack Zhang shares updates on glucagon, GLP‑1 RAs, and insulin biosimilars

CEO Dr. Jack Zhang and CFO Mr. Bill Peters highlighted Amphastar’s dual‑strategy growth model, pairing strategic acquisitions like Baqsimi with internally developed complex generics, biosimilars, and novel peptides (see the webcast and presentation slides). The presentation noted that by 2026, proprietary and biosimilar programs will represent 85% of the pipeline, up from 37% in 2021. This shift is supported by sustained R&D investment and expanding technical capabilities across peptides, intranasal delivery, and recombinant DNA biologics.

- Amphastar’s branded pipeline continues to be led by Baqsimi’s (nasal glucagon) projected $250-275 million peak sales and strong US growth following its June 2023 acquisition from Lilly. Mr. Peters noted that only 12% of insulin users currently fill a glucagon prescription, up from 10% at acquisition, leaving substantial room for greater penetration. Internationally, Mr. Peters stated that Amphastar will withdraw from several unprofitable markets after its three-year contractual commitment ends in June 2026, improving the overall margin profile.

- On pipeline updates, AMP‑018, the company’s generic injectable GLP‑1 RA, is planned for a launch in 2027. He said that Amphastar is beginning third‑party sales of GLP‑1 Active Pharmaceutical Ingredient (APIs) in China, marking a strategic shift from internal‑only API use.

- On insulin, Amphastar’s biosimilar insulin programs – AMP‑004 (Novolog) and AMP‑005 (recombinant human insulin) – continue to advance. For AMP‑004, the FDA accepted the company’s biosimilar application in April 2025, and it is currently under review. Mr. Peters noted that while AMP‑025 (insulin degludec) remains in development, Amphastar may pause the program given current market conditions.

Arrowhead Pharmaceuticals: RNA interference treatments for obesity to advance to phase 2b trial

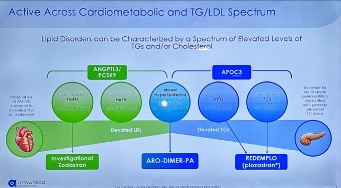

Dr. Chris Anzalone (Arrowhead Pharmaceuticals CEO) highlighted Arrowhead’s RNA interference (RNAi)-based therapy portfolio. Arrowhead is a clinical-stage biopharmaceutical company with a market capitalization of $8.9 billion and cash and investments of $920 million, excluding $200 million each from Sarepta and Novartis and $930 million from recent public offerings. The company is focused on developing RNAi therapies using its targeted RNAi molecule (TRiM) platform for a wide range of diseases. Arrowhead launched its first medicine Redemplo (plozasiran) – an RNAi treatment that targets APOC3 – for familial chylomicronemia syndrome (FCS) in November 2025 and continues to advance 20 early, mid, and late-stage clinical programs across cardiometabolic, pulmonary, liver, and neuromuscular indications. Dr. Anzalone emphasized that the TRiM platform can be applied to seven cell types (i.e., liver, lung, skeletal muscle, central nervous system, adipose tissue, ocular, and cardiomyocyte) with more to come, positioning Arrowhead as a “clear leader” of RNAi therapies.

- Obesity pipeline. Dr. Anzalone established what he envisions as the future of obesity care: (i) recognizing the heterogeneity of obesity; (ii) reducing visceral fat for cardio-kidney-metabolic outcomes; and (iii) combining therapies to further reduce cardiovascular risks. He noted that people with obesity and T2D lose less weight with incretin-based therapies, and therefore, positioned RNAi-based therapies as a potential treatment option to address unmet needs. Arrowhead is advancing ARO-INHBE (n=120) and ARO-ALK7 (n=126) studies in people with obesity with or without diabetes in phase 1/2a trials. ARO-INHBE inhibits Activin E, while ARO-ALK7 reduces the expression of ALK7, both of which are known to regulate energy homeostasis in adipose tissue. According to interim data announced last week, ARO-INHBE significantly reduced serum Activin-E by 85% on average, visceral fat by 9.9% at Week 16, and 16% with two doses at Week 24. In people with obesity and T2D, adding ARO-INHBE to tirzepatide doubled weight loss compared to tirzepatide monotherapy. Meanwhile, ARO-ALK7 decreased ALK7 gene expression by up to 88%, and conferred up to a 13.6% reduction in visceral fat (compared to a 0.5% increase with placebo) at Week 8.

- While remaining cautious about interpreting the early data, Dr. Anzalone expressed excitement about initiating phase 2b studies as soon as possible. Specifically, Arrowhead aims to assess the use of add-on therapies in combination with other GLP-1 RAs or as maintenance therapies following discontinuation of GLP-1 RAs. Beyond these candidates, Arrowhead hopes to expand its obesity pipeline with dimers and new targets for the liver and adipocytes.

- Lipid pipeline. As shown in the slide below, Arrowhead’s portfolio addresses both elevated LDL-C and triglycerides, including homozygous (HoFH) and heterozygous familial hypercholesterolemia (HeFH), severe hypertriglyceridemia (sHTG), FCS, and mixed hyperlipidemia. Redemplo (plozasiran), an RNAi therapy for APOC3, has been approved by the FDA and launched in November 2025. Zodasiran, an RNAi targeting ANGPTL3, has demonstrated a 41% reduction in LDL-C in people with HoFH and a 62% reduction in people taking PCSK9 inhibitors in a phase 2 trial (n=18), suggesting an additive benefit. It is currently being evaluated in a phase 3 trial (n=60). ARO-DIMER-PA is the first dual RNAi therapy targeting APOC3 and PCSK9. Preclinical studies in monkeys showed a significant reduction in non-HDL-C, LDL-C, and triglyceride levels. Arrowhead expects to launch phase 1/2 study for mixed hyperlipidemia in this month, with initial data expected at the end of 3Q26.

AstraZeneca: Cardiometabolic focus for 2030 and beyond led by aldosterone synthase inhibitor baxdrostat, PCSK-9 laroprovstat, and GLP-1 RAs in development

Dr. Aradhana Sarin (CFO) presented AZ’s 2025 broad-scale results and outlook for the decade to come, with a focus on cardiometabolic health second only to oncology. Since the company’s FY 2024 report, AZ has presented 16 positive phase 3 trial readouts with five key focus areas in therapeutics: oncology, cardiovascular, renal & metabolism (CVRM), respiratory & immunology, vaccines & immune therapies, and rare disease. Dr. Sarin discussed the company’s goal to achieve $80 billion in total revenue by 2030 with sustained growth for 2030 and beyond. She said that the Inflation Reduction Act and the loss of exclusivity of Farxiga (dapagliflozin) and other drugs have continued to lower revenue, which reached $54.1 billion in 2024, yet has been offset by growth in the company’s existing portfolio and the upcoming launch of key NMEs. Among other therapies, she highlighted baxdrostat (a selective aldosterone synthase inhibitor for hypertension and primary aldosteronism), Farxiga fixed dose combinations, and laroprovstat (a PCSK-9 inhibitor) as key therapies in development that will propel AZ’s growth in the remainder of this decade. Beyond 2030, she discussed weight management and CV risk factors, cell therapy and T-cell engagers, gene therapy, next-generation IO biospecifics, and antibody-drug conjugates and radioconjugates as areas of focus for the future. AZ hopes to play a role in addressing sustained cardiometabolic disease burden worldwide. Dr. Sarin also touched on the company’s specific approaches to AI, including an AI Development Agent for drug synthesis and quantitative continuous scoring to identify patients most likely to respond to treatment.

- Positive baxdrostat trial results were highlighted as helping drive AZ’s momentum across a diverse pipeline.In September 2025, results from the phase 3 BaxHTN trial for uncontrolled hypertension were announced at ESC 2025 and simultaneously published in NEJM (n=796). At 12 weeks, participants receiving baxdrostat 2 mg achieved a mean reduction of 15.7 mmHg, while those on 1 mg saw a 14.5 mmHg reduction, compared with a 5.7 mmHg reduction in those receiving placebo. These results correspond to a placebo-adjusted reduction of 9.8 mmHg with 2 mg baxdrostat and 8.7 mmHg with baxdrostat 1 mg. Results were consistent across both the uncontrolled and treatment‑resistant hypertension subgroups. Dr. Sarin said that phase 3 trial results from 2025 including BaxHTN and the phase 3 Bax24 trial for resistant hypertension present a $10 billion dollar opportunity for AZ.

- Baxdrostat is currently under FDA Priority Review. As announced in December 2025, the Prescription Drug User Fee Act (PDUFA) date for the therapy is anticipated in 2Q26. If approved, the therapy could address a major need in cardiovascular care in patients with limited treatment options. Dr. Sarin said that, upon approval, AZ expects the therapy’s adoption to proceed from specialists to primary care.

- Addressing weight management and cardiovascular risk factors will form a key part of AZ’s long-term strategy. Dr. Sarin said that AZ hopes to establish a role and eventually lead in a new weight management paradigm and in cardiovascular risk factors. She also said that AZ is uniquely positioned to deliver novel small molecule combinations and committed to “accelerating programs into late-stage development.” Dr. Sarin then highlighted three phase 3 trials ongoing for laprovstat as well as phase 2 trials of:

- Elecoglipron (a small-molecule GLP-1 RA) with readout expected in 1H26;

- AZD6234 (an amylin receptor agonist) with readout expected in 1H26; and

- The combination of AZD9550 (a dual glucagon/GLP-1 RA) and AZD6234, with readout expected in 2H26.

- Phase 3 data for laroprovstat, an oral PCSK-9 inhibitor, are expected in 2027. Dr. Sarin said that laroprovstat holds great potential because it is a once-daily, small molecule therapy with no fasting or food restrictions. In phase 2b trials, the therapy demonstrated an over 50% reduction in LDL cholesterol on top of standard-of-care statins. In 2Q25, AZ initiated three phase 3 clinical trials for AZD0780 (laroprovstat), which are all actively recruiting:

- AZURE-LDL (n=2,800) will evaluate LDL-C reduction in patients with dyslipidemia and a history of clinical ASCVD or who are at risk of a first ASCVD event.

- AZURE-HeFH (n=405) will evaluate LDL-C reduction in patients with heterozygous familial hypercholesterolemia.

- AZURE-Outcomes (n=15,100) will evaluate the time to first event of any component of MACE-Plus, a composite endpoint that includes death, myocardial infarction, stroke, revascularization, heart failure, and thromboembolic events. Patients included will either have dyslipidemia and established ASCVD or will be at high risk of a first ASCVD event.

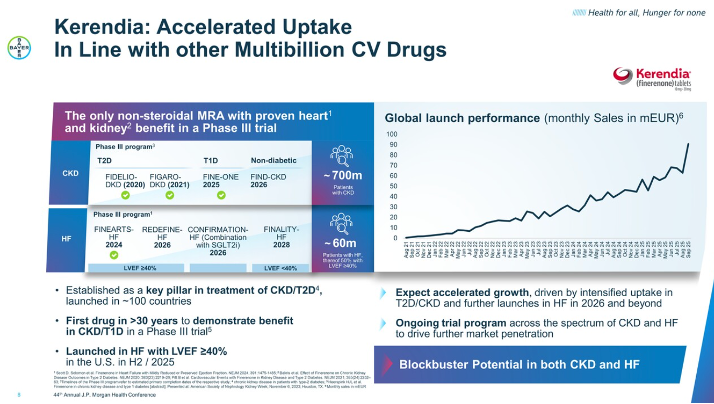

Bayer: Kerendia (finerenone) demonstrates blockbuster potential for CKD and heart failure; pricing pressures with Eylea (aflibercept)

Mr. Stefan Oelrich (Bayer President of Pharmaceuticals Division) shared updates on Bayer’s therapies, including: (i) non-steroidal MRA Kerendia (finerenone); and (ii) anti-VEGF Eylea (aflibercept). See the webcast and presentation slides here. What a success is Kerendia! We never tire of hearing how many people it is helping.

- Kerendia demonstrates blockbuster potential for CKD and heart failure. Mr. Oelrich called Kerendia the next blockbuster drug and included it as one of the key growth drivers of 2025, especially as it has demonstrated accelerated growth in T2D, CKD, and heart failure. Bayer initially pursued Kerendia for the treatment of CKD and T2D, establishing it as a key pillar across ~100 countries. Then, Bayer progressed Kerendia for a heart failure indication to encompass a broader population. At ESC 2024, results of the phase 3 FINEARTS-HF (n=6,001) trial showed that Kerendia demonstrated a 16% relative risk reduction of the primary composite outcome of total heart failure outcomes and cardiovascular death over 32 months among patients with HFmrEF or HFpEF. Following these groundbreaking results, Kerendia received FDA approval for the treatment of heart failure in July 2025. With indications for CKD and heart failure, Mr. Oelrich emphasized Kerendia’s efficacy, expecting accelerated growth driven by increased uptake and further launches in 2026 and beyond.

- Several phase 3 trial results are expected in CKD and heart failure. In 2026 alone, the following trials are expected to complete: (i) FIND-CKD trial (n=1,584) of Kerendia in adults with non-diabetic CKD; (ii) REDEFINE-HF trial (n=5,200) of Kerendia in hospitalized heart failure patients; and (iii) CONFIRMATION-HF trial (n=1,500) of the combination of Kerendia and SGLT-2 inhibitor in hospitalized patients with heart failure. Mr. Oelrich said these ongoing trials across the spectrum of CKD and heart failure are expected to drive further market penetration.

- Kerendia’s potential for T1D. At ASN 2025 in Houston, Bayer announced results from the phase 3 FINE-ONEtrial (n=241) of Kerendia in people with T1D and CKD. Kerendia significantly reduced UACR by 25% compared to placebo at six months. Echoing Mr. Bill Anderson’s (Bayer CEO) remarks during Bayer’s 3Q25 call, Mr. Oelrich emphasized that Kerendia is the first therapy in 30 years to demonstrate positive results in addressing CKD in this population. This is fantastic, particularly given all the risk of kidney disease the longer someone has had T1D. Now this is a therapy indication that we hope gets special treatment!

- Kerendia’s uptake, translated. Bayer has previously predicted a slow uptake of Kerendia, but Mr. Oelrich expressed confidence that the uptake would continue at a fast rate. In fact, we know, of course, Kerendia has shown accelerated uptake in line with “other multibillion-dollar cardiovascular drugs” – look at this curve below Mr. Oelrich said this area has limited options with high unmet needs, and therefore, positioned Kerendia as a promising treatment. He compared Kerendia to statins when they first emerged in the field – statins are used, of course, to lower cholesterol levels, and so many are seeing and experiencing Kerendia reducing risk of kidney disease. It has put UACR on the map, all right!

- Eylea sales remain stable but face increasing pricing pressures. While Mr. Oelrich strongly emphasized Eylea’s leadership in the retinal market and positioned it as the number one anti-VEGF treatment at JPM 2025, he spoke minimally about this product in today’s meeting. As background, Bayer exclusively markets Eylea outside the US, while Regeneron is responsible for US sales. Mr. Oelrich said the conversion from Eylea to Eylea HD (aflibercept 8mg), the only drug for extended treatment intervals (up to five months for nAMD and DME), is “going well.” He also said Eylea sales are “stable for now,” but commented that the company continues facing pricing pressures and expects to see more challenges with emerging biosimilars in the field.

Biocon: Addressing global non-communicable diseases like diabetes; generics and biosimilar business restructuring

Biocon Group CEO Mr. Shreehas Tambe presented the company’s approach to non-communicable diseases and diabetes in particular. Mr. Tambe said that the Biocon Group is a global biopharmaceutical company consisting four arms. Biocon Biologics, which develops biosimilars, represents 62% of revenue and has the goal of expanding access to affordable, lifesaving biotherapeutics. Biocon, the company’s generics business, forms 17% of total revenue. Syngene, the group’s research arm, represents 21% of revenue with a market cap of $2.9 billion. Finally, Bicara develops novel biologics and is NASDAQ-listed with a market cap of $1.1 billion.

Mr. Tambe emphasized Biocon Group’s history of improving access to life-saving therapeutics. In 2004, the company launched India’s first recombined human insulin, and in 2021 commercialized the first interchangeable insulin glargine in the US. In 2024, the company expanded to the ocular complication arena, receiving the first US FDA approval for biosimilar aflibercept for the treatment of eye diseases such as AMD and DME. In 2025, the company received approval and commercialized the first interchangeable insulin aspart in the US and has also offered a number of essential oncology therapies.

- Biocon Group plans to help address a shift in global disease burden from communicable to non-communicable diseases. Mr. Tambe said that Biocon has seen a significant change in global need since the 1990s. Non-communicable disease such as cancer, diabetes, musculoskeletal, and autoimmune diseases now form a very significant portion of global disease burden that Biocon plans to address. He pointed to a number of the company’s current biosimilars and generics, such as the approved therapies glargine U100, liraglutide, aspart, dapagliflozin, and recombinant human insulin for diabetes and obesity as an example of Biocon’s work on this front. In company’s pipeline for diabetes care, Mr. Tambe identified semaglutide, tirzepatide, and glargine U100. When combined with the company’s offerings in oncology and immunology, these therapies will address over 60% of global disease burden, he said. The company hopes to serve one-in-five of all people taking insulin specifically.

- Biocon Group will combine its generics and biosimilar businesses into one entity. Current companies Biocon and Biocon Biologics will become one under “Biocon,” biosimilars, insulins, peptides, and complex generics. Mr. Tambe said that this will help the businesses maximize research & development, manufacturing, and commercialization. The move will also allow Biocon to cross-leverage aspects of its portfolio and commercial infrastructure.

- Mr. Tambe said that Biocon hopes to build upon its strong launch momentum going into 2026. In the US, wave one of the first interchangeable insulin aspart, Kirsty, launched in September 2025, and the therapy has already launched in the rest of the world. In the GLP-1 RA arena, Ladiazyl and Lobezyl (generic liraglutide) have launched in the UK and select EU markets and have been filed in the US. Generic semaglutide has been filed in Canada, Brazil, the US, and in other select markets. With these anticipated approvals and its business restructuring, Biocon Group hopes to begin to address the rise in non-communicable diseases.

Biomea Fusion: Phase 2 data for Icovamenib and phase 1 results of GLP-1 RA BMF-650 expected in 2026

In this afternoon session, Dr. Mick Hitchcock, interim CEO of Biomea Fusion, highlighted key programs: icovamenib and the GLP-1 RA BMF-650. He first began by emphasizing that current treatments for T2D primarily address downstream metabolic symptoms, rather than the disease pathway. Icovamenib is an oral covalent menin inhibitor that promotes beta cell proliferation and function in people with T2D. This candidate was developed based on human physiology: pregnant or lactating women were found to suppress menin, leading to beta cell expansion and insulin secretion. Preclinical studies in rats and human islet cells confirmed that menin inhibition promotes beta cell proliferation.

- In the phase 2b COVALENT-111 trial, icovamenib significantly reduced A1c values by 1.2 percentage points (vs. a 0.3 percentage point increase with placebo) and increased C-peptide level by 29% (vs. 2%) in the severe insulin-deficient subgroup (~60% of T2D) at Week 52. Dr. Hitchcock pointed out that a short 12-week dosing period induced epigenetic changes for beta cell regeneration, resulting in sustained improvement in A1c values for a year. Moreover, a post-hoc analysis found that icovamenib is especially efficacious in people on GLP-1 RA therapy whose baseline A1c was >7.0%. Icovamenib conferred a 1.2 percentage point reduction in A1c in this population compared to a 0.6 percentage point increase with placebo. This finding showed that Icovamenib was generally well-tolerated, with no reports of adverse event-related discontinuations or serious adverse events. Ultimately, Dr. Hitchcock said that icovamenib could offer patients a short-term oral treatment, rather than lifelong insulin use.

- Looking ahead, Biomea Fusion will evaluate icovamenib in the phase 2b COVALENT-211 trial for people with insulin-deficient T2D (~20% of T2D) and the phase 2 COVALENT 212 trial for people with difficult-to-manage T2D already on GLP-1 RAs (70% of people taking GLP-1 RAs). Both trials will begin recruiting in 1Q26, and 26-week results are expected in 4Q26.

- During Q&A, Dr. Hitchcock said that the “win scenario” for icovamenib would be conferring a ≥0.5% A1c reduction at 26 weeks to remain “approvable.” An A1c reduction by 1.8-2.0% would allow icovamenib to be competitive. He also clarified that the phase 3 trials for icovamenib could be smaller programs, given that the drug is administered for 12 weeks and thus is not considered a “chronic agent.”

- BMF-650 is an oral small molecule GLP-1 RA. It is currently evaluated in the phase 1 GLP-131 trial in people with obesity (BMI ≥30 kg/m2) who are otherwise healthy; 28-day weight loss results are expected in 2Q26. Dr. Hitchcock said that BMF-650 is designed for better bioavailability and has the potential to deliver more consistent efficacy than other oral GLP-1 RAs like orforglipron. Moreover, BMF-650 has the same chemotype as orforglipron, as opposed to the chemotype to which the now-discontinued danuglipron, lotiglipron, and TERN-601 belonged. This chemotype, as well as preclinical studies in monkeys, gives Biomea Fusion confidence that BMF-650 will not cause liver-related safety issues.

- During Q&A, Dr. Hitchcock defined success for BMF-650 as involving a competitive weight loss magnitude, favorable tolerability, a faster titration scheme, and durability of weight loss.

Corcept Therapeutics: Dr. Joseph Belanoff highlights broad implications of cortisol modulation, including hypercortisolism, obesity, and diabetes

In this afternoon session, CEO Dr. Joseph Belanoff discussed Corcept Therapeutics’ focus on cortisol modulation.He first explained that cortisol regulates metabolism, immune system, apoptosis, and psychiatric health. Excess cortisol is often an underlying driver of the Cushing syndrome (hypercortisolism); cardiometabolic diseases like hypertension, diabetes, obesity, and metabolic dysfunction-associated steatohepatitis (MASH); cancer; and neurological diseases like Alzheimer’s. Hence, cortisol modulation has a potential for broad therapeutic opportunities.

- Dr. Belanoff reviewed the findings of the CATALYST trial, highlighting the higher-than-expected prevalence of hypercortisolism. To many experts’ surprise, Part 1 (n=1,113) found that nearly a quarter of individuals with difficult-to-manage T2D had underlying hypercortisolism. Moreover, in Part 2 (n=252) of the trial, Korlym (mifepristone), a glucocorticoid receptor antagonist and a treatment for hypercortisolism, significantly lowered mean A1c (1.5 percentage points vs. none with placebo), weight, and visceral fat. Given the high prevalence of hypercortisolism, Dr. Belanoff estimates that the drug has potential to reach $2 billion in annual revenue.

- Corcept Therapeutics is developing relacorilant (a highly selective glucocorticoid receptor agonist) for the treatment of hypercortisolism with hypertension and/or hyperglycemia. Relacorilant aimed to address the limitations of Korylm as a non-selective progesterone and glucocorticoid antagonist (which could also be used to induce abortion). In the phase 3 GRACE program, the candidate significantly lowered systolic blood pressure by 12.6 mmHg and A1c by 0.7 percentage points from a baseline of 7.1%. Despite these results, Corcept Therapeutics received a Complete Response Letter from the FDA in December 2025, noting that more evidence of effectiveness is necessary to show favorable benefit-risk assessment. Dr. Belanoff said that the company plans to meet with the agency soon to discuss its concerns, provide additional analyses, or potentially appeal the decision.

- In MASH, miricorilant, a selective glucocorticoid receptor, is currently evaluated in a phase 2 MONARCH (n=175) study among patients with biopsy-confirmed MASH. The trial has completed enrollment, with results expected by year-end 2026. In phase 1b trial, miricorilant demonstrated 30% reduction in liver fat, as well as improvement in liver health and fibrosis, with favorable tolerability profile.

Esperion: Updated US lipid-lowering guidelines to include bempedoic acid offering; international expansions; combination therapy

Esperion CEO Mr. Sheldon Koenig presented the company’s approach to expansion, profitability, and its bempedoic acid portfolio. He began by saying that Esperion is in a strong financial position, with a strong balance sheet, durable cash flows, and an attractive profit and loss profile. He said that the company will reach sustainable profitability in 2026. Esperion’s current offerings are nexletol (bempedoic acid) and nexlizet (bempedoic acid/ezetimibe). Bempedoic acid is an ATP citrate lyase inhibitor that reduces low-density lipoprotein (LDL) cholesterol levels. It was first approved in the US in February 2020 and offers therapeutic opportunity for patients unwilling or unable to take statins, as well as for use in combination therapy. Mr. Koenig discussed Esperion’s impressive international reach, pipeline, and scientific approach.

- Esperion plans to strengthen and expand the bempedoic acid franchise beyond nexletol and nexlizet. Mr. Koenig identified six major catalysts that will drive growth for Esperion in 2026 and beyond. Most prominently, bempedoic acid is expected to be included in updated US lipid-lowering guidelines by the end of February. This will follow guidelinesreleased by the European Society of Cardiology (ESC) in September 2025, which recommend bempedoic acid in patients who are unable to take statin therapy to achieve their LDL-C goals. Market exclusivity is also expected in 2026, as well as further commercial investment, an oral triple combination therapy, international expansion, and improved gross margins.

- On the updated US lipid-lowering guidelines, Mr. Koenig drew parallels to the treatment of hypertension and of T2D, where combination therapy is now the standard of care after years of having one leading therapy. He said that the management of high cholesterol will now move towards combination therapy including bempedoic acid based on key outcome study data. In a March 2023 study published in NEJM (n= 13,970), bempedoic acid reduced the incidence of myocardial infarction by approximately 14% and incidence of coronary revascularization by 19%.

- Preclinical development continues for Esperion’s triple combination therapies, which include bempedoic acid, ezetimibe, and statin therapy (atorvastatin or rosuvastatin). The company first announced the oral triple combination in 4Q24, positioning it as a next-generation option for LDL-c lowering.

- Mr. Koenig highlighted Esperion’s partner-led international expansion, asking the audience to think of the company as a global franchise. Esperion’s bempedoic acid franchise is currently approved in 41 countries. In Europe, Asia, and South America, Daiichi Sankyo is leading the expansion efforts, with over 600,000 patients treated to date. In Japan, Esperion launched in December 2025 in partnership with Otsuka. The company plans to work with Neopharm Israel to expand to the nation in 1H26, and with CSL Seqirus to seek approvals in Australia and New Zealand, which are expected in 4Q26. In Canada, Esperion has partnered with HLS therapeutics and expects approval in 2026.

- Mr. Koenig also said that the company is also seeking portfolio growth through partnerships, with key areas of focus in cardiometabolic health, kidney disease, diabetes, and rare and orphan diseases. He said that Esperion will not seek any very large acquisitions and will instead pursue strategic acquisitions that are immediately accretive. Mr. Koenig also spoke of “activating” consumers in 2025 with plans to continue this in 2026 – Esperion has launched publicity buttons reading, “Can’t take a Statin? Make NEXLIZET Happen!” as well as non-skippable ads on streaming platforms. Mr. Koenig said that most consumers have not attempted to skip the ads, which he framed as a positive sign for therapeutic awareness.

Ionis Pharmaceuticals: Tryngolza gains traction in treatment of FCS ahead of broader launch; pelacarsen for Lp(a) risk reduction on track for launch in 2027

CEO Dr. Brett Monia highlighted Ionis’s cardiometabolic franchise, emphasizing the commercial momentum of Tryngolza (olezarsen) for the treatment of familial chylomicronemia syndrome (FCS), and the potential of pelacarsen to reshape Lp(a)-driven cardiovascular risk. Tryngolza was approved in December 2024 in the US and September 2025 in the EU for FCS. It generated more than $100 million in US net revenue in its first year, with Dr. Monia describing “overwhelmingly positive” patient feedback and strong physician reauthorization rates. Ionis is preparing a broader launch in severe hypertriglyceridemia (SHTG), for which phase 3 CORE and CORE-2 trial data showed 72% fasting triglyceride reduction, 86% of patients below the pancreatitis risk threshold, and an 85% reduction in acute pancreatitis events. Dr. Monia confirmed that the supplemental NDA was submitted in December and that Ionis has requested priority review. If granted, approval could come as early as July 2026.

- On Lp(a), Dr. Monia reiterated enthusiasm for pelacarsen, developed in partnership with Novartis, and positioned it as a first-in-class siRNA therapy targeting genetically elevated Lp(a). He emphasized that phase 2 data showed >95% reductions in Lp(a) levels. The phase 3 HORIZON outcomes trial (n=8,323) is expected to read out in 1H26, with Dr. Monia Ionis anticipating a 2027 launch pending positive results. Dr. Monia noted that the trial is powered to detect a 20% relative risk reduction overall and 25% in patients with very high Lp(a), but emphasized that given the lack of approved therapies, a 10-15% reduction in cardiovascular events would be considered a meaningful win and may be sufficient for Novartis to pursue approval.

J&J: CEO Mr. Joaquin Duato outlines diversified growth strategy with momentum in cardiovascular portfolio

In this standing-room-only session, CEO Mr. Joaquin Duato discussed J&J’s top priorities in 2026, which include MedTech, cardiovascular business, as well as surgery and ophthalmology sectors. Mr. Duato especially spotlighted J&J’s cardiology franchise, which is approaching $9 billion, anchored by cardiac ablation, heart failure device company Abiomed, and calcified arterial disease with Shockwave Medical. Notably, J&J plans to launch the Shockwave C2 Aero coronary catheter in 2026, reinforcing its leadership in interventional cardiology. While there was no direct mention of diabetes or obesity, we are excited about these advancements given that cardiovascular disease is the leading cause of mortality in this population. Mr. Joaquin also shared insights into how J&J navigates the dynamic business environment with the Trump administration.

- Mr. Duato reiterated the company’s goal to manufacture the majority of its advanced medicines used in the US, with two new plants underway in North Carolina for biologics manufacturing and Pennsylvania for cell therapy manufacturing, part of a $55 billion investment plan. The sites were announced as part of an agreement with the US government that will allow access to medicines at discounted rates for millions of patients. In exchange, the company’s pharmaceutical products are exempt from tariffs. Moreover, as part of the Most Favored Nation deal announced in November 2025, the company will also be participating in the direct-to-consumer platform TrumpRx to offer J&J medicines at discounted rates, joining other companies like Pfizer, Lilly, and Novo Nordisk. Mr. Duato viewed these agreements as a “step in the right direction,” as they expand access to medicines and give companies exception from tariffs, allowing the companies to focus on “what [they] do best” – developing, manufacturing, and commercializing medicines.

Kailera Therapeutics: CEO Mr. Ron Renaud highlights diversified GLP-1 RA pipeline for obesity treatment

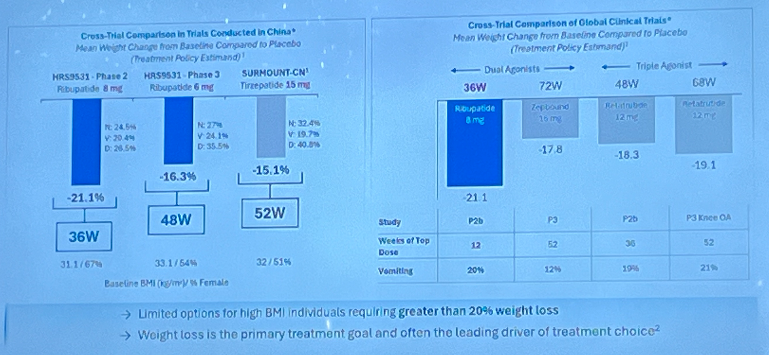

In a morning symposium, CEO Mr. Ron Renaud highlighted Kailera Therapeutics’ obesity pipeline and its broader business strategies. As background, Kailera is a California- and Massachusetts-based clinical-stage company launched in October 2024 with $400 million Series A financing round. It develops an obesity pipeline acquired in May 2024 from Jiangsu Hengrui Pharmaceuticals. Kailera has exclusive global development and commercialization rights outside of Greater China for four metabolic disease assets, as Mr. Renaud detailed in his presentation. He began by highlighting that over half of US adults with obesity are projected to have a BMI ≥35 kg/m2 by 2030. Moreover, 68% of participants in SURMOUNT-1 with baseline BMI ≥35 kg/m2 did not reach BMI <30 kg/m2, indicating significant unmet needs in people with severe obesity.

- Ribupatide (KAI-9531) is an injectable dual GLP-1/GIP RA designed to be more efficacious than tirzepatide, by making GLP-1 agonism three times more potent and GIP agonism half as potent as tirzepatide. KAI-9531 also has a half-life of seven days, compared to five days for tirzepatide. In a phase 2 trial (n=61), ribupatide conferred placebo-adjusted weight loss of 21.1% at Week 36 with a higher dose of 8 mg. In a phase 3 trial (n=567), KAI-9531 6 mg previously achieved up to 17.5% mean weight loss without a plateau at Week 48, with 44% of participants achieving ≥20% weight loss.

- While cautious to make cross-trial comparisons, he noted that ribupatide conferred greater weight loss than tirzepatide and retatrutide at shorter study durations. See figure below.

- Looking forward, ribupatide is evaluated in three ongoing phase 3 KaiNETIC trials (n=1,600, 1,700, and 1,200) for doses up to 10 mg for over 76 weeks. One trial includes participants with T2D, while another includes those with high BMI ≥35 kg/m2. Kailera announced today that the first participants randomized in the phase 3 KaiNETIC program have been dosed.

- Kailera also has other GLP-1 RA-based candidates:

- Oral ribupatide is progressing into phase 2 in 2026. In a phase 1 trial, the candidate conferred 5.4% weight loss at Week 4, and 6.3% experienced vomiting, suggesting potentially favorable tolerability profile.

- Oral KAI-7535, a once-daily oral small molecule GLP-1 RA, will progress to phase 2 in 2026, as well. In primary and post-hoc analyses of a phase 2 trial, KAI-7535 led to 9.5-15% weight loss with low liver risk.

- KAI-4729, a once-weekly GLP-1/GIP/glucagon triple agonist, is intended to deliver strong weight loss and improved liver fat reduction. In preclinical studies, KAI-4729 showed the potential to confer greater weight loss than retatrutide. This candidate will progress to phase 1 in 2026.

- During Q&A, when asked about the impact of semaglutide’s loss of exclusivity in the early 2030s, when these candidates are expected to launch, Mr. Renaud shared confidence that its focus on people with severe obesity (BMI ≥35 kg/m2) and robust clinical data can help Kailera secure reimbursement. To another question about pipeline diversity, Mr. Renaud said that additional mechanisms of action will be needed in parallel or as an add-on to GLP-1 RA-based therapies. However, he believes that GLP-1 RAs will remain backbone treatments, and Kailera’s candidates have a strong potential to be differentiated assets as GLP-1 RA therapies.

Lexicon Pharmaceuticals: Dr. Mike Exton highlights SGLT-1/2 inhibitor sotagliflozin, pilavapadin for DPN, and non-incretin obesity candidate

CEO Dr. Mike Exton discussed Lexicon Pharmaceuticals’s clinical pipeline spanning cardiometabolic diseases and diabetic peripheral neuropathy (DPN). He first explained that Lexicon was founded in 1995 as a genetically informed drug discovery company. From ~5,000 genes identified in the Genome5000 project, the company developed multiple drug candidates, two of which have been approved. Lexicon also continues to advance novel targeted therapies, such as: (i) sotagliflozin for hypertrophic cardiomyopathy (HCM) and T1D; (ii) pilavapadin for DPN; and (iii) LX9851 for obesity and weight management. The company has $125 million in cash and cash equivalents with a runway into 2027.

- Dual SGLT-1/2 inhibitor sotagliflozin is currently approved for heart failure under the brand name Inpefa. In the US, where Lexicon removed all commercial operations as of November 2024, Dr. Exton said that Lexicon’s virtual salesforce team continues to support patients. Outside the US and EU, its partner Viatris secured approval in UAE for worsening heart failure and filed for regulatory approval in Saudi Arabia, Canada, Australia, New Zealand, Mexico, and Malaysia. Dr. Exton also highlighted additional indications that Lexicon is pursuing:

- HCM. Sotagliflozin is currently being evaluated in the phase 3 SONATA-HCM trial (n=500). Lexicon has initiated all trial sites and aims to complete enrollment in 1H26, with topline data expected in 1Q27. Dr. Exton explained that the dual inhibition of SGLT-1 and SGLT-2 allows sotagliflozin to target both obstructive (due to outflow tract obstruction) and non-obstructive HCM (due to altered metabolism) by directly modifying cellular energetics in the heart. Moreover, he believes that the once-daily dosing and safety profile position sotagliflozin to be a potential first-line agent for HCM.

- T1D. Under the brand name Zynquista, sotagliflozin is also being evaluated as an adjunct-to-insulin therapy for glycemic management in people with T1D. Dr. Exton said that a Type D meeting with the FDA confirmed that the STENO1 (n=200) trial is sufficient to support NDA resubmission. Lexicon estimates that resubmission and regulatory decision will occur in 2026.

- The STENO1 trial (n=200) is an open-label study that evaluates the cardiovascular effects of several interventions in adults with T1D. The trial was initiated in July 2024 and is expected to complete in July 2029.

- LX9851 is an oral non-incretin candidate that inhibits Acyl-CoA Synthetase 5 (ACSL5) and is being evaluated for weight management. In March 2025, Novo Nordisk entered an exclusive licensing agreement to develop and commercialize LX9851. Consistent with its 3Q25 update, Lexicon completed all IND-enabling studies and delivered results to Novo Nordisk in 2025, achieving the initial requirements for a $10 million milestone payment. Dr. Exton said that the company has the potential to achieve an additional $20 million in milestone payments in 2026. Preclinical data have shown potential benefits for lipid lowering and MASH.

- Pilavapadin is an oral non-opioid AAK1 inhibitor (LX9211) being evaluated for adults with moderate-to-severe DPN. At EASD 2025, Lexicon announced results of the phase 2b PROGRESS trial, which showed an early separation in pain scores between pilavapadin and placebo. Dr. Exton said that Lexicon is now seeking a partner to conduct phase 3 trials. He also highlighted several legislative initiatives to support non-opioid innovations in chronic pain. These include the Alternatives to PAIN Act, aimed at improving access to non-opioid medications for Medicare Part D beneficiaries, and the FDA’s draft guidance from September 2025 on non-opioid analgesics for chronic pain.

Lilly: Mr. David Ricks shares insights about obesity market, payment channels, and clinical pipeline including orforglipron

In a packed afternoon symposium, CEO Mr. David Ricks shared reflections from 2025 and vision for the coming years for Lilly. He first celebrated that this year marks 150 years of Lilly’s existence and leading innovation since 1876. He then offered reflections about the past couple of years. After a “choppy, unclear year” in 2024 with uncertainty about supply, access, and drug uptake, Lilly delivered strong performance in 2025, stabilizing all three of those factors. There is no longer a shortage of tirzepatide; negotiations with the US government expanded access with lower price burden for patients; and LillyDirect reached more patients through cash channel. Moreover, Lilly continues to advance its clinical pipeline, including tirzepatide (dual GLP-1/GIP RA), orforglipron (oral GLP-1 RA), retatrutide (triple GLP-1/GIP/glucagon RA), eloralintide (long-acting amylin agonist), brenipatide (dual GLP-1/GIP RA), and six additional programs in phase 1. Mr. Ricks said these candidates have the potential to treat one billion people worldwide with obesity, cardio-renal-metabolic diseases, obstructive sleep apnea, and potentially even neurological or inflammatory diseases. Indeed, the indications continue to expand, as a recent phase 3 TOGETHER-PsA trial (n=271) showed significant benefits of tirzepatide when administered together with Taltz (ixekizumab) in people with psoriatic arthritis. In a dialogue with Mr. Chris Schott (Managing Director, JPMorgan), Mr. Ricks shared his insights about the obesity market, payment channels, and the competitive landscape.

- On orforglipron, which delivered key phase 3 results for T2D and obesity last year, Mr. Ricks said that regulatory filing submitted to the FDA under the new priority voucher program. Approval is expected in 2Q26. Mr. Ricks speculated that oral formulation would be helpful for patients with aversion to needles, perception of escalating medicine from lifestyle modifications to injectable medicines, or those already on polypharmacy. Moreover, orforglipron can be a promising option for those who want weight maintenance. In a blinded phase of a clinical trial, orforglipron conferred greater weight loss in people who discontinued semaglutide and gained modest weight in those who took tirzepatide; ultimately, orforglipron stabilized weight loss from either of the two medications. He especially believes that orforglipron would be more dominant than injectable GLP-1 RAs in OUS markets, where launch is expected in 2026 and 2027. Responding to Mr. Mike Doustdar’s (CEO, Novo Nordisk) comment on a clinical trial protocol, in which participants were directed to wait two to four hours after statin administration, Mr. Ricks said that the protocol was largely due to the timing of clinical development – Lilly had simply not conducted drug interaction studies with statins when initiating the trial.

- On different payment channels, Mr. Ricks said that Medicare has better penetration than the commercial market. Because government coverage often becomes the standard, the inclusion criteria for coverage tend to be more based on science. For tirzepatide, the criteria include people with overweight and comorbidities (e.g., CVD, peripheral artery disease, and prediabetes) or obesity – which Mr. Ricks said is significantly better than most commercial coverage. Moreover, with the recent Most Favored Nation negotiation – which Mr. Ricks characterized as a “unique deal” – out-of-pocket cost is “reasonable” at $50. He believes that all states will follow this standard for Medicaid programs and hopes that the coverage will spill over to commercial channels. Mr. Ricks added that incretin-based therapies offer preventive benefits, which is even more beneficial for countries with higher healthcare costs, as the return-on-investment is greater.

- On the commercial channel, he shared that new pharmacy benefit managers (PBMs) are emerging with more price transparency. He advocated for greater transparency is needed in the US, including what the post-rebate cost will be.

- LillyDirect, Lilly’s direct-to-consumer platform, has been very successful. He said that the price transparency with knowing the exact cost before buying, as well as notices for renewal cycle, allows patients to take charge of their own health.

- On the overall obesity market, Mr. Ricks welcomed companies entering the obesity landscape. He emphasized that Lilly will maintain its excellence in R&D and “multiple shots on goal” strategy to develop differentiated candidates. Looking forward, he expects more swings in 2026, especially given the uncertainty about the volume. Hence, the company will likely provide a guidance with a broader range. Finally, he also pointed to its AI initiatives, including its collaboration with NVIDIA, as opportunities for growth.

Madrigal: “10% of 10%” of global MASH patients treated; detailed approaches to combination therapy including GLP-1 RAs and DGAT-2 inhibitors

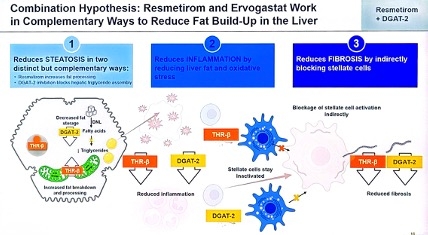

Madrigal CEO Mr. Bill Sibold, CMO Dr. Dave Soergel, and CFO Ms. Mardi Dier discussed the company’s approach to growth in 2026 and beyond, highlighting its recent expansion to a three-product portfolio. Mr. Sibold said that Madrigal has three areas of growth for the future: (i) delivering on the best-in-industry drug launch of Rezdiffra; (ii) progressing towards an indication for stage F4 fibrosis (cirrhosis, F4c); and (iii) extending leadership through pipeline expansion. The company will focus on combination therapy with Rezdiffra and the phase 2 oral DGAT-2 inhibitor ervogastat (which the company licensed from Pfizer just last Friday), combination therapy with SYH2086 (a small molecule oral GLP-1 RA licensed from CSPC Pharmaceutical Group in July 2025), and the F4c indication in 2026. With over 29,500 patients on therapy as of 3Q25, Madrigal still has significant potential for expansion – the market of 315,000 patients with diagnosed F2/F3 fibrosis is about 10% penetrated, which represents only 10% of all patients thought to have MASH. Many patients remain undiagnosed. This “10% of 10%” strategy of addressing a greater patient population fuels Madrigal’s optimism for the future. Mr. Sibold also compared the launch of Rezdiffra to the launch of specialty therapeutics for irritable bowel disease, rheumatoid, and psoriasis over the past thirty years. He explained that therapies for these conditions were all once thought to be very niche markets, yet all three have now grown to over $20 billion markets. Madrigal believes that the liver health market is only at the cusp of its future growth.

- Oral DGAT-2 inhibitor ervogastat offers promise for Madrigal’s pipeline. Three days ago, Madrigal announced that it has entered an exclusive global license agreement with Pfizer for ervogastat, as well as and two early-stage candidates for the treatment of MASH. Pfizer received an upfront payment of $50 million and is eligible for milestone payments and royalties on net sales. Madrigal has rights to develop, manufacture, and commercialize ervogastat globally. Dr. Soergel discussed the mechanism of action of the therapeutic class: DGAT-2 inhibitors block the enzyme called diacylglycerol acyltransferase 2 (DGAT-2), which catalyzes the final step of triglyceride synthesis and storage in the liver, lowering lipotoxic fat and inflammation. The therapy will be delivered orally and is expected to be combined with Rezdiffra, as the therapies work in distinct, complementary ways.

- In 2026, Madrigal will conduct a drug-drug interaction study of the two therapies, with a phase 2 combination study anticipated to start in 2027 following regulatory discussions. In previous studies, ervogastat has demonstrated impressive liver fat reduction, with up to 61% percent of patients considered super responders (a 50% reduction of liver fat from baseline over 48 weeks). This represents significant clinical improvement to liver fibrosis.

- Combination therapy with oral GLP-1 RA MGL-2086 was also a focus of discussion. In July 2025, Madrigal entered an exclusive global license agreement with China-based CSPC Pharmaceutical Group for SYH2086, a preclinical oral small molecule and orforglipron derivative. The therapy, now known as MGL-2086, has the potential to improve Rezdiffra’s efficacy in combination therapy. Dr. Soergel explained that weight loss of ≥5% significantly improves Rezdiffra’s efficacy, emphasizing that the company is therefore targeting such modest weight loss as opposed to greater proportions. He said that a MGL-2086 phase 1 single ascending dose study will begin in 2Q26.

- Madrigal seeks an expanded indication for compensated MASH cirrhosis, also known as stage 4 fibrosis (F4c). A significant unmet need remains in this disease stage, with an estimated addressable patient population of 245,000. There is a high urgency to treat these patients as there is a 42-fold greater risk of liver-related mortality. Management said that F4c outcomes trial data are estimated to be delivered in 2027, and that two-year data from MAESTRO-NASH OUTCOMES provides confidence in the future results. With over 10,000 current or past prescribers of Rezdiffra, Mr. Sibold said that adoption of the therapy for F4c is expected to be rapid upon approval with the therapy’s growing familiarity. As the therapeutic landscape continues to change rapidly, Madrigal says it is tracking to be first to market for this indication and more.

Merck: “Democratizing” PCSK9 therapy and combinations with Lp(a); MK 3000 as a potential new mechanism of action for diabetic macular edema

Merck Chairman and CEO Mr. Robert Davis highlighted a new wave of late-stage assets on Monday afternoon, which extend the company’s reach beyond its historic core of oncology medicines. Enlicitide (oral PCSK9 inhibitor), MK 3000 (tetravalent, tri-specific Wnt antibodies), and the oral Lp(a) small molecule underscore Merck’s expansion into cardiometabolic disease. For a company that developed its Januvia franchise for presumably $1 - $2 billion, that has yielded well over $50 billion in revenue, we are very intrigued by the way that the company discussed Enlicitide – very efficacious, very safe, and very easy to take (our way of describing “tolerable”).

- Overall pipeline and financial portfolio framing. Merck projects over $70 billion in commercial opportunity by mid-2030, representing a $20 billion increase from 2025. Ten key programs, which notably include Enlicitide, account for around 70% of the $70 billion in sales. Nearly all have first-in-class potential with multi-billion peak sales. Four of those ten have already launched or have positive phase 3 data, while the remainder are expected to have major phase 3 readouts in the next 12-18 months. Positively, Mr. Davis shared that half of the $70 billion is expected to be clinically de-risked via phase 3 readouts by the end of 2026, with near-complete de-risking expected by the end of 2027.

- Enlicitide. Mr. Davis characterized Enlicitide as a therapy that was designed to be a potent LDL-lowering pill, with effects that “looked like the antibodies” – functioning as a “biologic in a pill.” In 2025, Enlicitide had three clinical readouts: (i) CORALreef Lipids (n=2,912); (ii) CORALreef HeFH (n=303); and (iii) CORALreef AddOn (n=301). Results demonstrated ~97% adherence and adverse event rates similar to placebo, supporting a broad use profile. Notably, it sounded like Merck hopes to “democratize” PCSK9 with Enlicitide by offering an affordable pill which can be widely accessed in the US and globally – as compared to a more niche, injectable therapy. We were extremely moved by Mr. Davis’ discussion of how good cholesterol scores could look and be. We will be extremely interested in watching how guidelines are discussed in the month and years ahead, particularly given some of the results at AHA.

- MK 3000. Mr. Davis highlighted MK 3000 as a potential new mechanism of action for the treatment of diabetic macular edema (DME). Phase 3 readouts of the BRUNELLO (n=984) and BAROLO (n=1,054) trials are targeted for September 2026. Mr. Davis emphasized that timing is “well ahead” of what was initially expected.

- Lp(a) oral small molecule. Merck acquired the Lp(a) small molecule candidate through a transaction with Longray and hopes to develop it as a combination therapy with Enlicitide – thereby combining a PCKS9-mediated LDL lowering with Lp(a) reduction in patients with a high cardiovascular risk. This combination, notably, was presented as part of a broader cardiometabolic plan which also includes Enlicitide-statin combinations, reflecting a company philosophy of being “first or best” and then planning “what’s next.”

Novartis: De-risked pipeline driving post-Entresto growth; Leqvio as the foundational therapy for the company’s cardiorenal metabolic franchise

CEO Dr. Vas Narasimhan’s presented Novartis as a focused “pure‑play medicines” company entering a “catalyst‑rich” period on Monday morning. He detailed a diversified pipeline that expects to compensate for Entresto’s (an angiotensin receptor-neprilysin inhibitor) loss of exclusivity in July 2025 and sustain ~5% annual growth through 2030.

- Overall pipeline and financial portfolio framing. Dr. Narasimhan shared 14 in‑market blockbusters and nine additional brands with multi‑billion‑dollar sales potential in Novartis’s portfolio. Moreover, the company is hosting six active launches and expects 15 submission‑enabling readouts over the next two years. Dr. Narasimhan shared that the company targets ~5% annual growth through 2030, which is supported by a deep portfolio of patent-protected assets.

- Dr. Narasimhan described Novartis’ cardiovascular risk reduction portfolio as being built “on the back of Leqvio” – a foundational lipid‑lowering medicine. The company intends to extend its cardiovascular risk-reduction portfolio with “siRNAs to more infrequently administered medicines,” signaling interest in its RNA‑based programs that designed to improve durability and reduce patient burden of treatment in chronic cardiovascular disease.

- Dr. Narasimhan also shared excitement on Novartis’ “portfolio of assets in the renal space.” While specific candidates were not specifically named today’s presentation or Q&A, Novartis’ renal assets were considered to be in the company’s late-stage plan for a 2026-2030 catalyst and subsequent launch cycle.

Novo Nordisk: Mr. Mike Doustdar on mastering cash channel, reframing perception of the semaglutide, and clinical pipeline with CagriSema, cagrilintide, and amycretin

In this extremely packed converation, CEO Mr. Maziar Mike Doustdar shared his perspectives on the challenges Novo Nordisk has faced and its vision for 2026 and onward. He began by reiterating Novo Nordisk’s commitment to treating obesity, diabetes, and comorbidities. Given that only 7% of people with diabetes and 2% of those with obesity are prescribed GLP-1 RAs or obesity medications worldwide, there is a significant unmet need that Novo Nordisk can address. That said, Novo Nordisk had a turbulent year in 2025 due to market challenges from continued compounding business, competition, and pricing pressure. Mr. Doustdar characterized these challenges as the “curse of a leader” of having to navigate clinical development and commercialization through trial-and-error. For over a decade, Novo Nordisk often faced doubts for developing medications for obesity, a condition previously considered as a lifestyle choice. Mr. Doustdar said that in 2025, the company had to critically recognize that the landscape had significantly changed, and that Novo Nordisk was no longer alone in the field. He further detailed what Novo Nordisk would have done differently and what key priorities the company will pursue in 2026.

- On the overall strategy for 2026, Mr. Doustdar highlighted three key goals: (i) master direct-to-patient and cash channels; (ii) expand the market through Wegovy pills; and (iii) reframe market perception of injectable semaglutide by launching higher dosage options. On the former, he recognizes that patients in the US – even those with insurance – face significant barriers to accessing medications, like prior authorizations. These obstacles had led to a rise of other entities like compounders. Novo Nordisk will thus continue to focus on cash channels in the US, “meeting the patients where they are.”

- When asked about the Most-Favored-Nation deal, Mr. Doustdar said that Novo Nordisk and the government negotiated carefully to determine the “sweet spot” at which volume increase balances the lower price. While he is confident about the future outlook, he said that there will be “short-term pain” because volume will not double immediately.

- On the Wegovy pill, Mr. Doustdar emphasized that it delivers ~15% weight loss, equivalent to injectable Wegovy, as well as cardiovascular benefits – indicating a promising label. He also believes that the oral formulation will broaden the market to a “large extent.” People who may be needle-aversive, cannot refrigerate Wegovy pens (e.g., due to frequent traveling), or are concerned about “escalating” treatments from lifestyle modification to injectable medication may contribute to the uptake. When asked about the food restriction, Mr. Doustdar said that approximately 2.4 million people have been prescribed with Rybelsus, and there was no evidence in the market that the food restriction hinders the uptake. He also added that we do not know what orforglipron’s label will look like. According to clinical trial protocols, participants taking statins were directed to wait two to four hours before taking orforglipron, for instance. On this comment, Lilly’s CEO Mr. David Ricks said in his symposium that the protocol was largely due to the timing of clinical development – Lilly had simply not conducted drug interaction studies with statins when initiating the clinical trial.

- On injectable GLP-1 RAs, Mr. Doustdar outlined Novo Nordisk’s plan to reframe the injectable obesity market, emphasizing that the company’s priority is to “change the current market perception” by demonstrating that semaglutide can reliably deliver >20% weight loss when appropriately dosed. He noted that the upcoming 7.2 mg semaglutide dose is designed to match or exceed the efficacy of newer competitors and argued that the current narrative – treating Lilly’s higher‑dose agents as inherently “next‑generation” and semaglutide as an older, less potent molecule – is fundamentally imbalanced. Mr. Doustdar stressed that this perception is driven almost entirely by dose, not by underlying biology, and that once the company brings the 7.2 mg dose to market, the comparison will become more balanced as semaglutide demonstrates equivalent 20% weight loss in the phase 3b STEP UP trial (n=1,407), along with its already‑proven cardiovascular, liver, and renal benefits, which competitors have not yet matched in outcomes data or labeling. He framed this as a necessary correction to a market that has overemphasized weight loss percentages while undervaluing semaglutide’s broader clinical profile.

- On the clinical pipeline, Mr. Doustdar highlighted CagriSema (fixed-dose cagrilintide and semaglutide) and amycretin as important late-stage assets. Based on results from the REDEFINE 1 trial, where CagriSema demonstrated 20% weight loss, compared to a reduction of 11.5% with cagrilintide 2.4 mg, 14.9% with semaglutide 2.4 mg, and 3.0% with placebo, the company submitted an NDA to the FDA in December 2025. The company is preparing for late‑stage development and multiple indication expansions. He also emphasized the standalone potential of cagrilintide monotherapy, which is now in phase 3 and aimed at patients who prioritize tolerability over maximal weight loss. Meanwhile, amycretin, a dual GLP‑1/GIP agonist, is advancing toward phase 3 based on positive phase 2 results and represents a key component of Novo Nordisk’s strategy to deliver both higher efficacy and improved GI tolerability.